A net balance of -26% for new buyer enquiries in February 2026 is not a minor statistical blip — it is a signal that demands a fundamental rethink of how chartered surveyors approach property valuation in a stalling market. The February 2026 RICS UK Residential Survey confirmed what many practitioners had suspected: demand-side weakness is accelerating, agreed sales are contracting, and short-term price expectations have turned decisively negative [1]. For surveyors, lenders, and property owners, the question is not whether the market has shifted but how valuations can remain defensible, accurate, and professionally robust amid this turbulence.

Valuation resilience under the February 2026 RICS survey requires more than acknowledging headline figures. It demands a structured methodology that incorporates weakening demand signals, regional price divergence, and forward-looking market indicators into every assessment. This article sets out the data, the risks, and the practical techniques that surveyors should deploy right now.

Key Takeaways

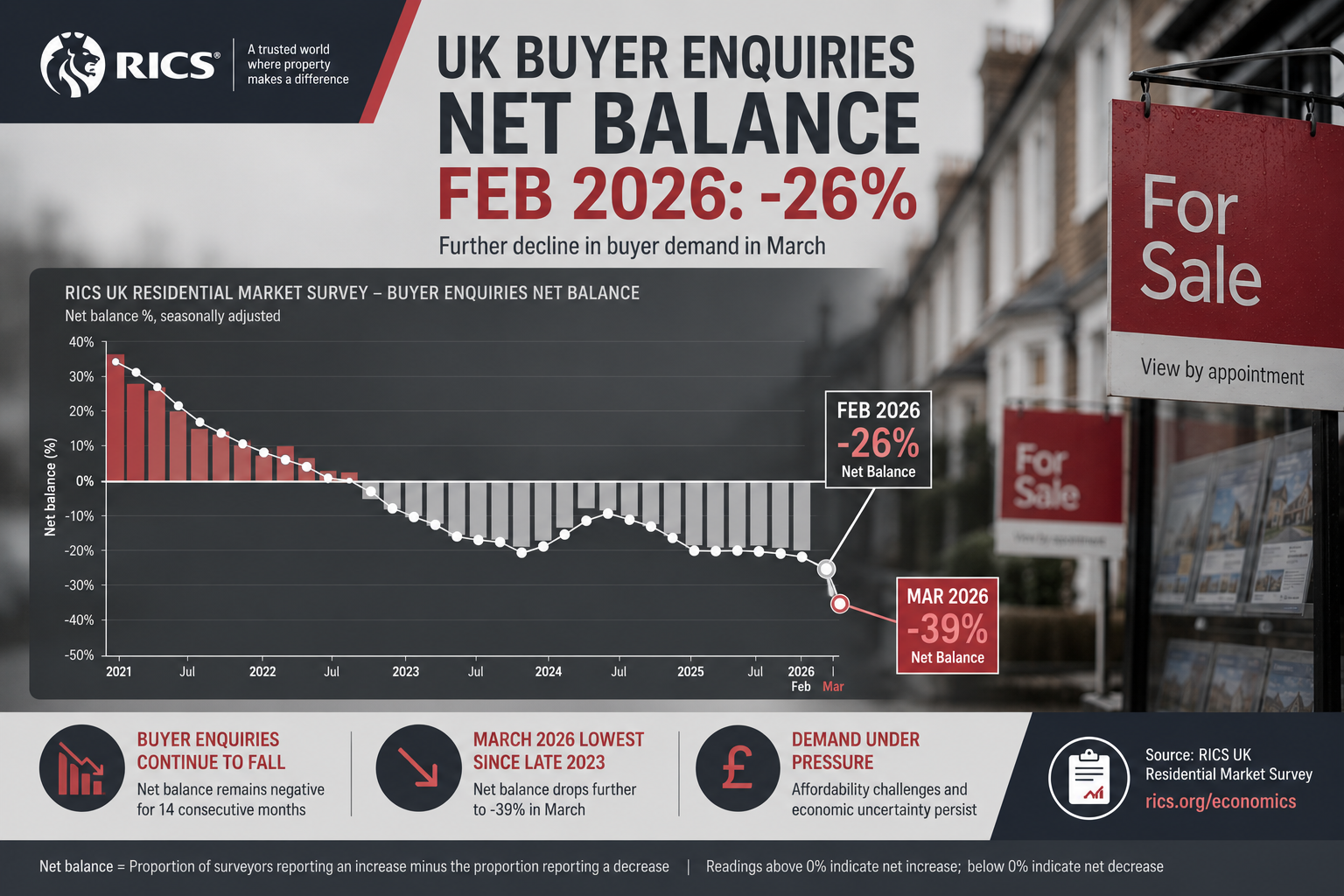

- New buyer enquiries fell to a net balance of -26% in February 2026, worsening to -39% in March — the weakest reading since August 2023.

- Agreed sales recorded a net balance of -12% in February, confirming broad transaction weakness across the UK market.

- Regional divergence is sharp: London (-40%), South East (-24%), and East Anglia (-26%) face significant downward pressure, while Northern Ireland, Scotland, and the North West remain firmer.

- Short-term price expectations dropped to -18% in February, but the twelve-month outlook holds at +33%, indicating a temporary rather than structural correction for many areas.

- Surveyors must adopt conservative, evidence-based valuation techniques that reflect weakened demand while avoiding over-correction that distorts long-term asset values.

Understanding the February 2026 RICS Data: What the Numbers Actually Mean

The RICS UK Residential Survey is one of the most closely watched leading indicators in the UK property market. Its net balance methodology — measuring the percentage of respondents reporting increases minus those reporting decreases — provides a real-time pulse on market sentiment. When that balance hits -26% for buyer enquiries, the market is telling surveyors something unambiguous: fewer buyers are actively searching, and those who are remain cautious [1].

The key February 2026 data points at a glance:

| Metric | February 2026 Net Balance | January 2026 Net Balance |

|---|---|---|

| New Buyer Enquiries | -26% | -15% |

| Agreed Sales | -12% | Not published |

| Short-Term Price Expectations | -18% | -6% |

| New Vendor Instructions | +2% | Broadly stable |

| 12-Month Price Expectations | +33% | Positive |

| Landlord Instructions (Rental) | -27% | Negative |

The deterioration from -15% in January to -26% in February represents a sharp single-month acceleration [1]. More concerning still, the trend continued into March 2026, with buyer enquiries falling to -39% — the weakest reading since August 2023 [2]. This sequential decline suggests that the February reading was not a one-off shock but the beginning of a sustained demand contraction.

What is driving this decline? The escalation of geopolitical tensions, particularly the ongoing Middle East conflict, has contributed to rising borrowing costs and eroded consumer confidence [2]. Mortgage affordability remains stretched for many first-time buyers and movers, and economic uncertainty is causing households to delay major financial decisions. Supply, meanwhile, has barely moved — new vendor instructions were essentially flat at +2% in February [1] — meaning the market is not flooded with stock but simply starved of willing buyers.

For surveyors, this combination of weak demand, stable supply, and deteriorating sentiment creates a particularly challenging valuation environment. Comparable transaction evidence becomes thinner, time-on-market extends, and the gap between asking prices and achievable sale prices widens.

Regional Price Divergence: Why a Single National Figure Is Misleading

One of the most important findings from the February 2026 RICS survey is the pronounced regional divergence in price trends. Treating the UK housing market as a single entity in 2026 would produce dangerously inaccurate valuations.

Regional performance breakdown (February 2026):

- London: Net balance of -40% — the most severe downward price pressure in the country

- South East: -24% — significant weakness, consistent with affordability constraints

- East Anglia: -26% — mirroring the national buyer enquiry decline

- Northern Ireland, Scotland, North West: Firmer price trends, with positive or near-neutral balances [1]

"The pronounced regional disparities in price trends and buyer demand require surveyors to adopt regionally differentiated strategies rather than applying blanket national adjustments." [3]

This divergence has direct implications for valuation methodology. A surveyor working in prime London or the commuter belt faces a fundamentally different evidence base than one operating in Belfast or Manchester. Comparable sales from six months ago may now be materially above achievable prices in London, while remaining broadly valid in Northern Ireland.

For commercial property valuations in London and the South East, the pressure is particularly acute. Reduced occupier demand, tightening yields, and weakening investor appetite compound the residential market signals.

Similarly, surveyors handling leasehold extension and enfranchisement valuations in London must now account for the -40% price sentiment balance when assessing relativity and hope value — adjustments that could meaningfully affect the premiums payable.

Valuation Resilience Under February 2026 RICS Survey: Core Methodological Adjustments

Achieving genuine valuation resilience under the February 2026 RICS survey conditions requires surveyors to move beyond passive observation of market data and actively integrate demand-side weakness into their methodologies. The following techniques represent best practice for the current environment [4].

Tighten the Comparable Selection Window

In a rapidly changing market, comparable sales from twelve months ago carry diminishing evidential weight. Surveyors should prioritise transactions completed within the last three months where possible, and apply explicit time adjustments to older comparables that reflect the deteriorating demand environment.

Where recent comparables are scarce — a common problem when agreed sales are running at a net balance of -12% [1] — surveyors should document this evidential gap clearly in their reports and apply a conservative adjustment range rather than defaulting to a single point estimate.

Apply Demand-Weighted Adjustments

The -26% buyer enquiry balance is not merely a sentiment indicator — it is evidence of reduced competition for available stock. Fewer competing buyers means less upward price pressure and longer marketing periods. Surveyors should:

- Extend assumed marketing period estimates to reflect reduced buyer pool depth

- Apply a demand discount to properties in regions with the weakest enquiry balances

- Stress-test valuations against a scenario where buyer enquiries deteriorate further toward the -39% March reading [2]

This approach is consistent with the guidance that surveyors should incorporate forward-looking market indicators into their assessments rather than relying solely on historical transaction evidence [4].

Separate Short-Term and Long-Term Value Signals

The February 2026 data presents a striking divergence between short-term and long-term price expectations. Near-term expectations fell to -18%, while the twelve-month outlook stands at +33% [1]. This gap is crucial for valuation purposes.

For a standard market valuation — which assumes a willing buyer and seller transacting in current market conditions — the short-term signal dominates. The -18% near-term expectation should inform conservative adjustments to achievable prices in the immediate term.

For longer-horizon valuations such as SIPP pension property valuations or inheritance tax valuations, the twelve-month positive outlook becomes more relevant, and surveyors should clearly articulate this distinction in their reports to avoid misinterpretation by clients or HMRC.

Strengthen Narrative Reporting

In volatile markets, the narrative section of a valuation report carries as much weight as the figure itself. Surveyors should explicitly reference:

- The February 2026 RICS survey findings and their regional relevance

- The specific demand metrics (-26% buyer enquiries, -12% agreed sales) that informed the assessment

- Any assumptions made about marketing period, buyer competition, and price trajectory

- The limitations of the comparable evidence base given reduced transaction volumes

This level of transparency protects the surveyor professionally and ensures that clients, lenders, and legal advisers understand the conditions underpinning the valuation figure.

Reassess Insurance Reinstatement Values Separately

It is worth noting that demand-side weakness does not affect reinstatement cost valuations in the same way it affects market valuations. Construction costs remain elevated regardless of buyer sentiment. Surveyors handling insurance reinstatement cost valuations should ensure clients understand that these figures operate on a different basis and should not be adjusted downward simply because the market is softening.

The Rental Market Dimension and Its Valuation Implications

The February 2026 RICS survey also revealed important dynamics in the rental sector that have indirect valuation consequences. Tenant demand was stable at a net balance of +2%, but landlord instructions remained deeply negative at -27% [1]. This persistent supply shortage in the rental market has two effects that surveyors must factor into their work.

First, properties with strong rental income potential retain relative value even as owner-occupier demand weakens. Buy-to-let investors and institutional landlords continue to seek yield, and this sustained demand provides a partial floor for certain property types and locations.

Second, the ongoing contraction in landlord supply — driven by regulatory changes, tax pressures, and rising finance costs — means that rental values are likely to remain firm or increase. For surveyors assessing properties with dual residential and investment appeal, this rental market tightness should be explicitly acknowledged as a value-supporting factor.

Understanding how to get an independent property valuation that properly accounts for both owner-occupier and investor demand is increasingly important in this bifurcated market.

Downside Protection Strategies for Surveyors and Their Clients

Valuation resilience under the February 2026 RICS survey conditions is not only about producing accurate figures — it is about protecting all parties from the consequences of over-valuation in a declining demand environment. The following strategies provide practical downside protection.

For lenders and mortgage valuations:

- Apply a minimum 5-10% demand discount in London and South East markets where the net balance has fallen to -40% and -24% respectively

- Flag properties with extended marketing histories as evidence of achievable price divergence from asking prices

- Require updated valuations for transactions where the original assessment is more than 90 days old, given the pace of market deterioration

For vendors and their advisers:

- Commission a pre-market independent property valuation that explicitly references current RICS survey conditions rather than relying on automated valuation models trained on historical data

- Consider the implications of the -18% short-term price expectation on pricing strategy and negotiation positioning

For buyers:

- Ensure any survey commissioned reflects current market conditions; a full building survey versus a homebuyer survey decision should be made with awareness that defects discovered in a falling market carry greater financial risk, as renegotiation leverage is reduced if demand recovers

For estate and probate purposes:

- Inheritance tax valuations completed in early 2026 should clearly document the market conditions prevailing at the date of death, including the RICS survey data, to support the valuation figure if challenged by HMRC

What the Twelve-Month Outlook Means for Valuation Strategy

The +33% twelve-month price expectation balance [1] is a significant counterweight to the short-term pessimism. It suggests that the majority of RICS survey respondents believe current conditions represent a temporary demand trough rather than the beginning of a prolonged structural decline.

This has important implications for how surveyors communicate their findings. A valuation produced in February or March 2026 reflects a specific point in time when demand is unusually suppressed. Clients — particularly those not transacting immediately — should understand that the current market value may not represent the property's medium-term worth.

The twelve-month price expectation balance of +33% indicates that surveyors broadly anticipate recovery, but the path there runs through a period of genuine short-term weakness that cannot be ignored in current valuations.

Surveyors should resist pressure from vendors or developers to anchor valuations to the twelve-month positive outlook rather than current market conditions. The professional and legal obligation is to reflect the market as it exists at the date of valuation, not as it might exist in twelve months' time. The positive outlook can and should be referenced in the narrative, but it must not inflate the headline figure.

For surveyors working across multiple regions, maintaining a clear understanding of how the Prince Chartered Surveyors approach to valuations integrates market intelligence with professional standards provides a useful framework for navigating these competing pressures.

Conclusion: Actionable Steps for Surveyors in a Weakening Market

The February 2026 RICS survey data presents a clear and urgent challenge. Valuation resilience under the February 2026 RICS survey conditions is achievable, but only through deliberate methodological adjustment, rigorous regional analysis, and transparent professional reporting.

Immediate actions for chartered surveyors:

- Update comparable databases to prioritise transactions from the last 90 days and apply explicit time adjustments to older evidence, particularly in London and the South East.

- Document demand conditions explicitly in every valuation report, referencing the -26% buyer enquiry balance and -12% agreed sales figure from the February 2026 RICS survey.

- Apply regional adjustments that reflect the significant divergence between London (-40%) and firmer northern markets — a single national adjustment is not defensible.

- Separate short-term and long-term value signals in client communications, ensuring that the -18% near-term expectation informs the headline figure while the +33% twelve-month outlook is contextualised appropriately.

- Stress-test valuations against the March 2026 deterioration to -39% buyer enquiries, particularly for lender clients who need downside protection built into their lending decisions.

- Engage clients proactively on the implications of current conditions for their specific valuation purpose — whether that is a market sale, an inheritance tax assessment, a pension fund asset, or a leasehold extension.

The market will recover — the twelve-month outlook suggests most surveyors believe this. But recovery does not exempt professionals from the obligation to reflect current reality accurately. In a market where buyer enquiries have fallen to -26% and are still declining, valuation resilience is built on evidence, transparency, and conservative professional judgement — not optimism.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026?utm_source=openai

[2] UK Housing Market Slows As Ongoing Middle East Conflict Raises Borrowing Costs – https://www.rics.org/news-insights/uk-housing-market-slows-as-ongoing-middle-east-conflict-raises-borrowing-costs?utm_source=openai

[3] Navigating RICS February 2026 Market Volatility Building Survey Demand Strategies When Buyer Enquiries Drop 26 And Regional Price Divergence Widens – https://www.canterburysurveyors.com/blog/navigating-rics-february-2026-market-volatility-building-survey-demand-strategies-when-buyer-enquiries-drop-26-and-regional-price-divergence-widens/?utm_source=openai

[4] Valuation Adjustments Amid February 2026 RICS Survey Slump Techniques For Weak Buyer Enquiries And Price Caution – https://princesurveyors.co.uk/blog/valuation-adjustments-amid-february-2026-rics-survey-slump-techniques-for-weak-buyer-enquiries-and-price-caution/?utm_source=openai

[5] Buyer Demand Collapse And Valuation Accuracy RICS February 2026 Data For Surveyors Navigating Geopolitical Uncertainty – https://princesurveyors.co.uk/blog/buyer-demand-collapse-and-valuation-accuracy-rics-february-2026-data-for-surveyors-navigating-geopolitical-uncertainty/?utm_source=openai