New buyer enquiries in the UK housing market collapsed to a net balance of -39% in March 2026 — the lowest reading since August 2023 [1]. For chartered building surveyors, that single statistic signals far more than a quiet quarter. It points to a profession navigating compressed demand, contested valuations, regulatory pressure, and a workforce stretched thin. The Spring 2026 Hot Topics for UK Building Surveyors: RICS Insights on Market Shifts and Valuation Challenges draws together five defining themes that are reshaping day-to-day practice, from how surveyors price their services to how they integrate sustainability into every report they write.

Key Takeaways

- Buyer demand has fallen sharply in early 2026, forcing surveyors to revise valuation methodologies and manage client expectations more carefully.

- Construction workloads remain broadly flat, though infrastructure and energy projects are providing pockets of growth.

- ESG factors are increasingly expected in valuations, yet data gaps and inconsistent market recognition continue to create professional risk.

- Technology adoption — including BIM, drones, and 3D laser scanning — is accelerating and becoming a competitive differentiator rather than a luxury.

- A persistent shortage of qualified surveyors is raising workloads, delaying projects, and intensifying recruitment competition across the sector.

The Housing Market Slowdown: What the Spring 2026 RICS Data Reveals

The RICS Residential Market Survey for early 2026 paints a sobering picture. Beyond the headline fall in buyer enquiries, the 12-month outlook for UK house prices has turned "broadly flat," with rising borrowing costs linked to ongoing geopolitical uncertainties playing a significant role in dampening confidence [2]. For building surveyors, this environment creates a specific set of professional pressures.

Why falling demand matters to surveyors

When transaction volumes drop, so does instruction volume. Surveyors who depend on pre-purchase survey instructions — particularly Level 3 full building surveys — feel the impact directly. Fewer sales completing means fewer reports commissioned. At the same time, those transactions that do proceed tend to involve more cautious buyers who scrutinise survey findings more closely and are more likely to use defect findings as negotiating leverage.

Price caution and renegotiation pressure

Surveyors are increasingly reporting that clients use survey findings to renegotiate purchase prices downward, even on defects that would previously have been absorbed without comment. This places greater responsibility on surveyors to produce reports that are both accurate and clearly reasoned. Vague condition ratings or ambiguous repair cost estimates are more likely to trigger disputes in a buyer's market.

"The sharp decline in buyer demand has led to valuation disputes, requiring surveyors to adjust methodologies to maintain accuracy." [4]

For surveyors advising on budgeting for repairs and restoration, precision has never been more commercially important. Clients expect cost guidance that reflects 2026 labour and material costs — not figures carried over from more stable market conditions.

Regional variation adds complexity

The slowdown is not uniform. London and the South East are experiencing sharper demand contractions than parts of the Midlands and North, where affordability ratios remain comparatively better. Surveyors operating across multiple regions need to apply locally calibrated comparable evidence rather than relying on national indices, which can mask significant local divergence.

Valuation Challenges in a Volatile Spring 2026 Market

The Spring 2026 Hot Topics for UK Building Surveyors: RICS Insights on Market Shifts and Valuation Challenges cannot be discussed without addressing the growing complexity of property valuation itself. Three interconnected pressures are converging: market volatility, ESG integration demands, and the challenge of pricing specialist or non-standard properties in thin markets.

Adjusting Methodologies for Weak Buyer Enquiries

When comparable transaction evidence thins out — as it does when buyer activity falls sharply — surveyors face genuine methodological challenges. The Red Book (RICS Valuation — Global Standards) requires valuers to use the best available evidence, but when recent sales are scarce, surveyors must be transparent about the weight they place on each comparable and the adjustments they apply [4].

Practical steps that are gaining traction in 2026 include:

- Extending the comparable search window while applying time adjustments to account for market movement

- Cross-referencing asking price data with agreed sale prices to identify the discount-to-asking-price trend in specific micro-markets

- Increasing reliance on rental yield evidence for investment properties where capital value comparables are limited

- Documenting uncertainty explicitly within valuation reports, in line with RICS guidance on material valuation uncertainty

For surveyors involved in inheritance tax valuations or matrimonial valuations, the stakes are particularly high. These valuations feed directly into legal processes where a challenged figure can have significant financial consequences for all parties.

ESG Factors: The Valuation Deadlock

One of the most debated topics in professional surveying circles in 2026 is how to incorporate environmental, social, and governance (ESG) factors into property valuations. The challenge is well-documented: valuers face genuine difficulty integrating ESG considerations due to a lack of sufficient comparable data and inconsistent market recognition of green premiums or brown discounts [8].

The core tension is this: sustainability features — high EPC ratings, heat pumps, solar panels, superior insulation — are widely accepted as adding long-term value. Yet in a market where buyers are already cautious, demonstrating a quantifiable premium for green credentials in the short term remains difficult.

| ESG Factor | Valuation Challenge | Current RICS Guidance |

|---|---|---|

| EPC Rating (A/B) | Limited comparables at top ratings | Note as a positive factor; quantify where evidence supports |

| Flood Risk | Increasingly material to value | Must be disclosed; impact varies by location |

| Carbon Retrofit Potential | Hard to price without cost estimates | Surveyors should flag retrofit obligations |

| Social/Community Factors | Largely unquantified in residential | Emerging guidance; watch RICS updates |

Surveyors who want to stay ahead of this issue should review the EPC and MEES building survey guidance and ensure their reports address energy performance in a way that is both compliant and commercially meaningful to clients.

Sustainability and Retrofitting: A Growing Advisory Role

With the UK government's energy efficiency targets tightening, building surveyors are being called upon to do more than assess current condition — they are expected to advise on retrofit pathways. This is particularly relevant for pre-1919 stock, which makes up a substantial portion of the UK's housing inventory and presents the greatest challenge in terms of environmental issues affecting older buildings.

Surveyors advising on retrofitting need to understand:

- The interaction between traditional breathable construction and modern insulation systems

- The risk of interstitial condensation when vapour barriers are incorrectly specified

- The implications of Minimum Energy Efficiency Standards (MEES) for landlords and commercial property owners

- The growing role of embodied carbon in whole-life assessments

This advisory function is expanding the scope of a standard building survey and, with it, the professional liability exposure surveyors carry. Clear report writing, appropriate caveats, and recommendations to obtain specialist advice where needed are essential risk management tools [6].

Construction Market Pressures, Technology Shifts, and the Workforce Crisis

Construction Workloads: Flat Overall, But Pockets of Growth

The RICS UK Construction Monitor for Q4 2025 reported overall workloads remaining flat, with a net balance of -6% [3]. However, the picture is more nuanced when broken down by sector. Infrastructure projects — particularly in energy, including renewables and grid upgrades — showed positive growth with a net balance of +12%. Private housing and commercial fit-out remain subdued.

For building surveyors with a construction monitoring or project management remit, this means:

- Energy infrastructure offers the strongest pipeline of new instructions in early 2026

- Private residential new-build remains constrained by planning delays and viability pressures

- Refurbishment and retrofit of existing stock is growing as an alternative to new construction

Surveyors involved in building regulation compliance testing will find demand increasing as retrofit projects must demonstrate compliance with updated Part L and Part F requirements.

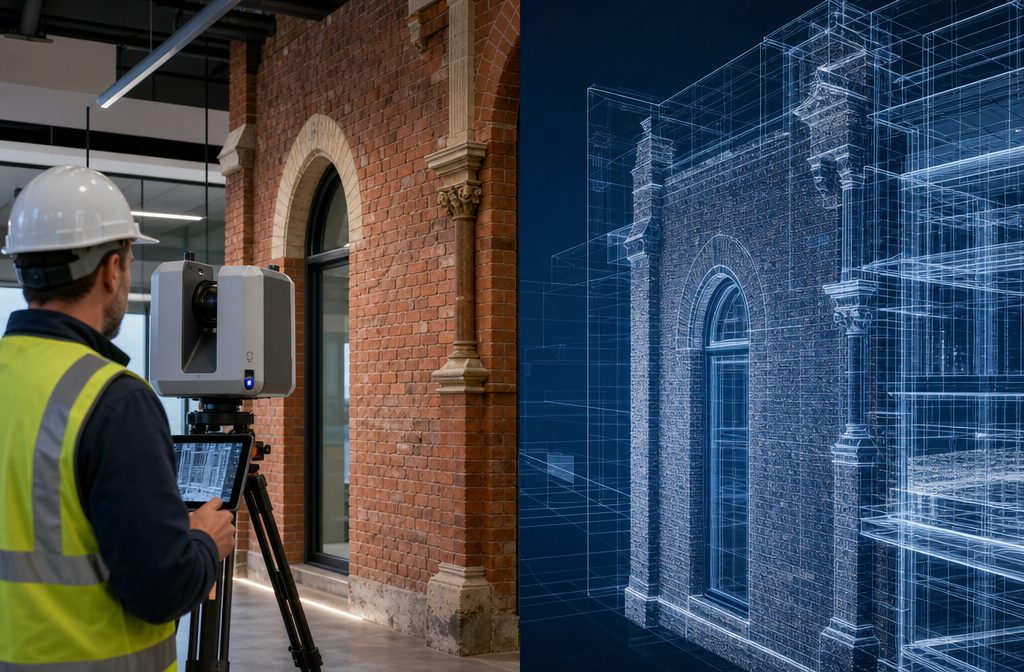

Technology Integration: From Optional to Expected

The adoption of Building Information Modelling (BIM), 3D laser scanning, drone surveys, and AI-assisted report generation has moved from early-adopter territory to mainstream expectation [6]. Clients commissioning large or complex surveys increasingly expect surveyors to deploy these tools as a matter of course.

Key technology trends shaping Spring 2026 practice include:

- Drone-assisted roof inspections reducing the need for scaffold access and cutting survey time on large or difficult-to-access buildings. Surveyors interested in this area can explore what RICS roof surveyors do and how aerial inspection is changing the discipline.

- 3D laser scanning and measured surveys delivering millimetre-accurate spatial data for heritage buildings, complex extensions, and dilapidations assessments. The measured building survey process has been transformed by this technology.

- AI-assisted defect identification using image recognition to flag potential issues from photographic evidence, reducing the risk of items being missed during inspection.

- Digital report platforms that allow clients to interact with findings, access linked photographs, and track remediation actions over time.

Surveyors who have not yet invested in these capabilities risk being undercut on both price and quality by competitors who can deliver faster, more detailed outputs. The business case for technology investment is strengthening as building survey timeframes come under client pressure.

The Workforce Shortage: A Structural Problem Demanding Strategic Solutions

Perhaps the most pressing operational challenge facing UK building surveying practices in 2026 is the acute shortage of qualified professionals. Nearly one in three quantity surveyor roles remained unfilled throughout 2025 [5], and the picture for building surveyors is similarly challenging, with recruitment difficulties reported across practices of all sizes [9].

The consequences are tangible:

- Project timelines are slipping as survey instructions cannot be fulfilled within client-expected windows

- Existing staff are carrying heavier workloads, increasing the risk of errors and professional liability claims

- Fee competition is intensifying as under-resourced practices undercut on price to win work they struggle to deliver

Strategies practices are adopting in 2026:

- Structured graduate pathways — partnering with universities and offering APC support to attract and retain early-career surveyors

- Flexible working models — remote report writing combined with on-site inspection days to widen the geographic pool of available talent

- Outsourced specialist functions — using third-party providers for niche assessments (e.g., structural engineering, damp specialists) rather than trying to employ all skills in-house

- Competitive fee structures — reassessing pricing to ensure sustainable margins that can fund competitive salaries [7]

The fee review point deserves particular attention. Surveyors are being encouraged across the profession to reassess whether their current pricing reflects the true value of their expertise, particularly given rising professional indemnity insurance costs, technology investment requirements, and the general inflationary environment [7].

Regulatory Updates and Practical Strategies for Chartered Surveyors

Keeping Pace with Legislative Change

The regulatory environment for building surveyors continues to evolve rapidly. Key areas demanding attention in Spring 2026 include:

- Building Safety Act implementation — the secondary legislation and guidance flowing from the 2022 Act continues to develop, with higher-risk building requirements affecting both new-build and existing stock. Surveyors advising on construction law matters need to stay current with the latest duty-holder requirements.

- Renters' Rights Bill — the ongoing reform of the private rented sector has direct implications for surveyors advising landlords on property condition, fitness for habitation, and compliance with Decent Homes standards.

- MEES tightening — the trajectory toward EPC Band C requirements for new tenancies continues, increasing demand for pre-letting surveys and retrofit advice.

- Biodiversity Net Gain — now mandatory for most new developments in England, this requirement is creating new advisory opportunities for surveyors with ecology knowledge.

Staying current with property market legislation changes is no longer optional — it is a core competency for any surveyor advising clients on acquisition, development, or management decisions.

Practical Strategies for Navigating Recovery Markets

The Spring 2026 Hot Topics for UK Building Surveyors: RICS Insights on Market Shifts and Valuation Challenges ultimately points toward a profession that must be proactive rather than reactive. The following strategies are gaining traction among leading practices:

- Diversify instruction types — balance pre-purchase surveys with dilapidations, expert witness work, insurance reinstatement valuations, and retrofit advisory to reduce dependency on transaction volumes

- Invest in CPD on ESG and sustainability — clients are asking questions that surveyors need to be qualified to answer

- Build referral networks — in a slower market, relationships with mortgage brokers, solicitors, and estate agents become more valuable as sources of instruction

- Review PI insurance cover — expanding scope of practice (particularly into ESG and retrofit) requires a corresponding review of professional indemnity cover

- Engage with RICS guidance actively — the institution is publishing updated guidance on valuation uncertainty, ESG, and technology at pace; practices that engage early gain a competitive advantage

Conclusion

The Spring 2026 landscape for UK building surveyors is defined by convergence: a softening transaction market, rising valuation complexity, accelerating technology adoption, tightening regulation, and a workforce under strain. None of these challenges is insurmountable, but each demands a deliberate professional response.

Actionable next steps for chartered surveyors in 2026:

- Review valuation methodology documentation to ensure it reflects current RICS guidance on material uncertainty and thin market conditions.

- Audit current report templates to confirm ESG and energy efficiency factors are addressed in a way that meets client expectations and regulatory requirements.

- Evaluate technology investment — particularly drone survey capability and digital reporting platforms — against the competitive landscape in your practice area.

- Conduct a fee review to ensure pricing is sustainable given rising costs and reflects the genuine expertise being delivered.

- Engage with RICS CPD resources and sector publications to stay ahead of Building Safety Act and MEES regulatory developments.

- Assess recruitment and retention strategies, including graduate pathways and flexible working models, to address the structural workforce shortage.

The surveyors who will thrive through 2026 and into recovery are those who treat these pressures not as disruptions but as the defining professional challenges of their era — and respond with the rigour and adaptability that RICS membership demands.

References

[1] Rising Number Of Surveyors Report Fall In Housing Market Activity Rics – https://www.mortgagesolutions.co.uk/mortgage-news/2026/04/09/rising-number-of-surveyors-report-fall-in-housing-market-activity-rics/

[2] UK Housing Market to Stagnate as Middle East Conflict Raises Borrowing Costs Says RICS – https://www.building.co.uk/news/uk-housing-market-to-stagnate-as-middle-east-conflict-raises-borrowing-costs-says-rics/5141680.article

[3] UK Construction Activity Remains Subdued Forward Indicators Signal Gradual Recovery – https://www.rics.org/news-insights/uk-construction-activity-remains-subdued-forward-indicators-signal-gradual-recovery

[4] Valuation Adjustments Amid February 2026 RICS Survey Slump Techniques For Weak Buyer Enquiries And Price Caution – https://princesurveyors.co.uk/blog/valuation-adjustments-amid-february-2026-rics-survey-slump-techniques-for-weak-buyer-enquiries-and-price-caution/

[5] Quantity Surveyor Shortages Impacting Building Survey Firms RICS 2025 Strategies For 2026 Project Delivery – https://kingstonsurveyors.com/quantity-surveyor-shortages-impacting-building-survey-firms-rics-2025-strategies-for-2026-project-delivery/

[6] SHW Building Surveying The 2025 Trends Challenges – https://www.shw.co.uk/articles/2025/shw—building-surveying—the-2025-trends–challenges.html

[7] Surveyor Rates Pricing UK 2026 – https://www.surveyors-valuers-uk.co.uk/article/surveyor-rates-pricing-uk-2026

[8] ESG Valuation Deadlock – https://ww3.rics.org/uk/en/journals/property-journal/ESG-valuation-deadlock.html

[9] Building Surveying Recruitment Trends 2025 – https://www.carriera.co.uk/insights/building-surveying-recruitment-trends-2025