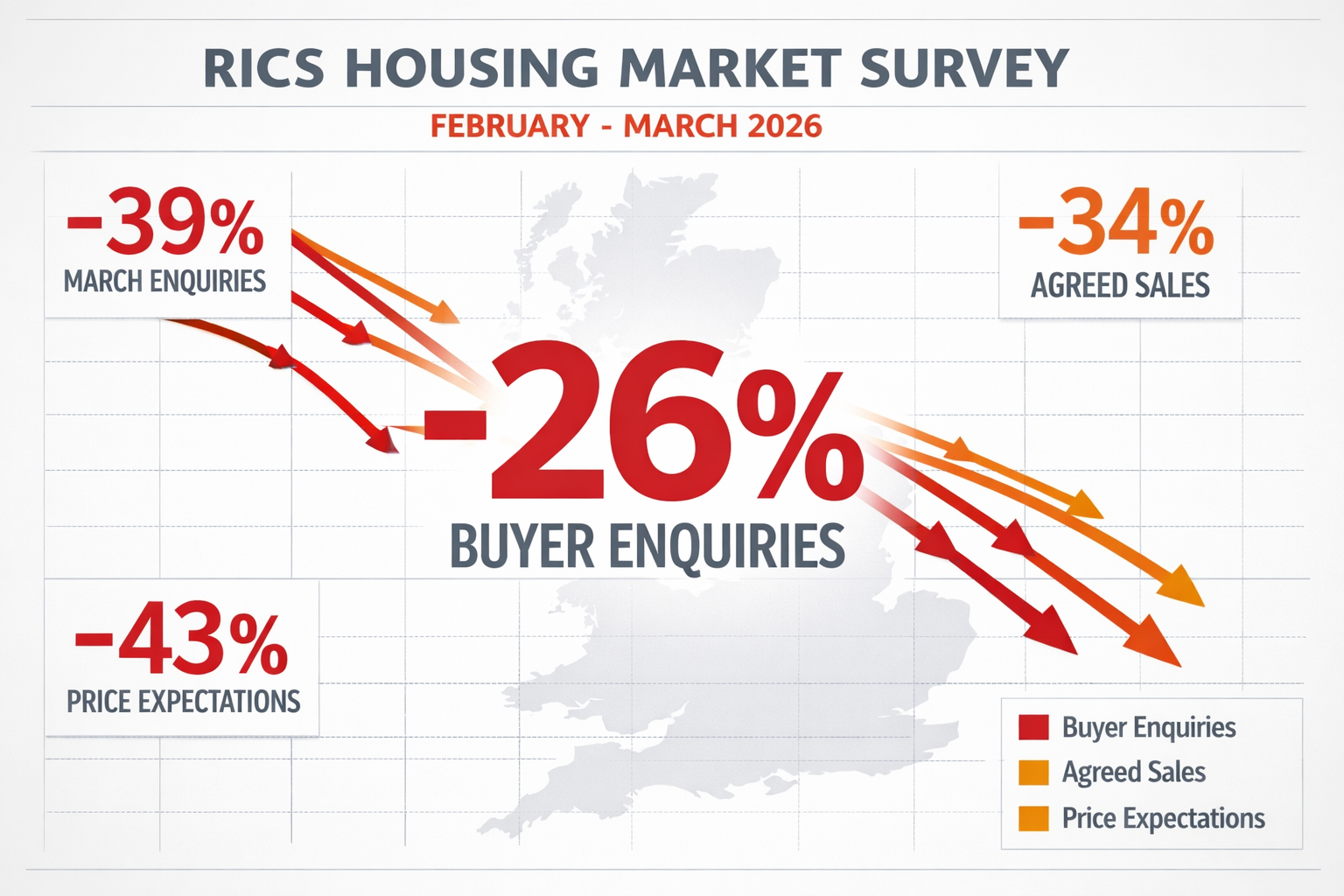

The February 2026 RICS Residential Market Survey revealed a stark reality: new buyer enquiries plummeted to a net balance of -26%, down from -15% in January, while short-term price expectations tumbled into deeply negative territory[1]. This dramatic deterioration signals a fundamental shift in the UK housing market, forcing chartered surveyors to recalibrate their valuation methodologies amid unprecedented buyer caution and weakening demand. For property professionals navigating Valuation Adjustments Amid February 2026 RICS Survey Slump: Techniques for Weak Buyer Enquiries and Price Caution, understanding how to maintain accuracy and credibility in assessments has become mission-critical.

The data paints a sobering picture: by March, buyer enquiries had collapsed further to -39%, marking a 31-month low, while agreed sales dropped to -34%—the weakest reading since summer 2023[3]. These metrics demand immediate strategic responses from valuation professionals who must balance historical comparables with rapidly evolving market sentiment.

Key Takeaways

- Buyer enquiries fell to -26% in February and -39% by March 2026, requiring surveyors to adjust valuation timelines and comparable selection criteria

- Short-term price expectations dropped to -43%, necessitating conservative valuation approaches and enhanced market condition commentary

- Regional divergence intensified, with London at -40% while northern regions showed resilience, demanding location-specific adjustment techniques

- Agreed sales volumes collapsed to 31-month lows, creating data scarcity challenges for comparable evidence and transaction-based valuations

- Professional valuation adjustments must incorporate forward-looking market indicators rather than relying solely on historical transaction data

Understanding the February 2026 RICS Survey Data and Market Context

The February 2026 RICS survey data represents more than statistical fluctuation—it captures a fundamental market recalibration triggered by macroeconomic uncertainty and geopolitical instability. The -26% net balance for new buyer enquiries means significantly more chartered surveyors reported declining interest than increasing activity, a pattern that intensified through March[1].

Breaking Down the Key Metrics 📊

The survey's headline figures reveal interconnected weakness across multiple market dimensions:

| Metric | February 2026 | March 2026 | Trend Direction |

|---|---|---|---|

| New Buyer Enquiries | -26% | -39% | ⬇️ Sharply declining |

| Agreed Sales | -13% | -34% | ⬇️ Accelerating weakness |

| House Price Balance | -14% | -23% | ⬇️ Downward pressure |

| Short-term Price Expectations | -19% | -43% | ⬇️ Severely negative |

| 12-month Price Outlook | +33% | +2% | ⬇️ Near-stagnation |

This cascade effect—from initial enquiry weakness to collapsed price expectations—creates a challenging environment for accurate property valuation. When negotiating house prices down after survey, buyers now have substantial market data supporting downward adjustments.

The Mortgage Rate Connection

The March deterioration coincided with Iran-conflict-driven mortgage rate increases, which pushed average fixed-rate products higher and further dampened buyer confidence[2]. This external shock amplified existing affordability concerns, creating a dual pressure scenario where both demand and financing accessibility weakened simultaneously.

For chartered surveyors conducting annual tax valuations, this volatility introduces significant complexity in establishing market value at specific valuation dates.

Valuation Adjustment Techniques for Weak Buyer Enquiries

When buyer enquiries collapse to 31-month lows, traditional valuation methodologies face inherent limitations. The scarcity of recent comparable transactions and the lag between market sentiment shifts and completed sales data require surveyors to adopt enhanced analytical frameworks.

Time-Adjusted Comparable Analysis

The cornerstone of valuation adjustments during the February 2026 RICS Survey Slump involves recalibrating how comparables are weighted and adjusted:

1. Recency Weighting Enhancement ⏰

- Prioritize transactions completed within the most recent 8-week period

- Apply graduated discounting to comparables older than 12 weeks

- Incorporate pending sales data (under offer properties) as secondary evidence

- Document market velocity changes explicitly in valuation reports

2. Marketing Period Analysis

- Track average days on market for comparable properties

- Identify properties requiring price reductions to secure buyers

- Calculate the percentage of asking price achieved in recent sales

- Note properties withdrawn from market due to lack of interest

3. Enquiry-to-Offer Conversion Metrics

When buyer enquiries fall to -39%, the conversion funnel from initial interest to formal offers becomes critical evidence. Surveyors should:

- Request agent feedback on viewing-to-offer ratios

- Document the number of viewings required to secure offers

- Assess whether properties are achieving multiple offers or single-bidder scenarios

- Consider the negotiating leverage shift toward buyers

Market Conditions Adjustments

Professional valuation standards require explicit recognition of prevailing market conditions. During periods of weak demand, this means:

Downward Adjustments for:

- Properties in oversupplied market segments

- Homes requiring significant capital expenditure

- Properties with extended marketing periods

- Locations experiencing acute buyer enquiry weakness

Upward Adjustments for:

- Genuinely scarce property types with sustained demand

- Turnkey condition properties requiring no immediate investment

- Locations bucking regional trends (see regional divergence section)

For property development valuations, incorporating buyer enquiry weakness into residual land value calculations becomes essential to avoid overvaluation.

Regional Divergence: Valuation Adjustments Amid February 2026 RICS Survey Slump

One of the most striking features of the February-March 2026 data is the intensification of regional performance divergence. While national headlines focus on aggregate weakness, surveyors must apply location-specific adjustment techniques that reflect genuine local market dynamics.

London and South East: Acute Downward Pressure

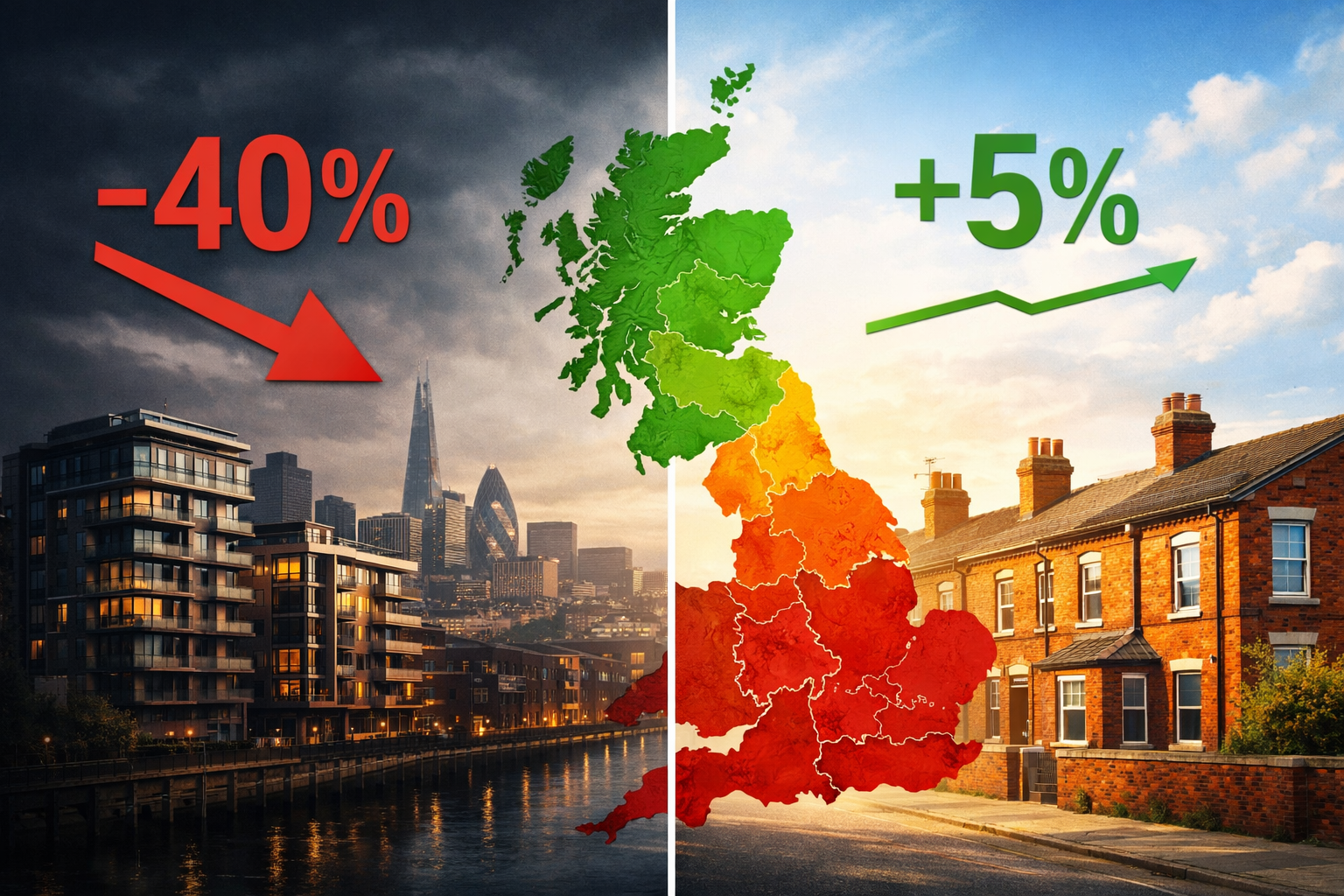

London recorded a devastating -40% net balance for house prices in February 2026, with 12-month expectations collapsing from +56% in January to just +7% by February[1]. This represents one of the sharpest sentiment reversals in recent survey history.

Valuation Implications for London:

- Apply conservative comparable selection favoring recent distressed sales

- Incorporate rental yield compression into investment property valuations

- Consider the impact of corporate relocation policies on prime central locations

- Document the "flight to affordability" affecting outer London boroughs

The South East followed a similar trajectory with -24% price balance, while East Anglia recorded -26%[1]. For chartered surveyors in Guildford and chartered surveyors in West London, these regional pressures demand explicit valuation commentary.

Northern Resilience: Relative Strength Adjustments

In stark contrast, Northern Ireland, Scotland, and the North West of England continued reporting firmer price trends through February[1]. This divergence creates both opportunities and challenges:

Northern Market Characteristics:

- Stronger affordability fundamentals supporting sustained demand

- Less exposure to international buyer withdrawal

- More stable employment markets in specific sectors

- Lower absolute price levels maintaining first-time buyer accessibility

Valuation Approach Adjustments:

For properties in resilient northern markets, surveyors should:

- Avoid over-applying national negative sentiment to local conditions

- Maintain normal comparable timeframes (12-16 weeks) where transaction volumes support it

- Document specific local demand drivers (employment, infrastructure investment)

- Consider whether regional strength represents genuine sustainability or temporary lag

The South-to-North Valuation Gradient

The Valuation Adjustments Amid February 2026 RICS Survey Slump reveal a pronounced gradient effect, where adjustment severity should correlate with regional position:

| Region | Price Balance | Adjustment Approach |

|---|---|---|

| London | -40% | Aggressive downward adjustments, stress-test assumptions |

| South East | -24% | Moderate-to-strong downward adjustments, extended marketing periods |

| East Anglia | -26% | Moderate downward adjustments, buyer negotiation leverage |

| North West | Positive | Minimal adjustments, maintain standard methodology |

| Scotland | Positive | Standard approach, monitor for contagion effects |

For matrimonial valuations conducted during this period, regional divergence becomes particularly significant, as the timing and location of valuation can materially affect settlement outcomes.

Price Caution Strategies: Incorporating Forward-Looking Indicators

The collapse in 12-month price expectations from +43% in January to +2% in March[3] represents a fundamental shift from anticipated appreciation to expected stagnation. This forward-looking pessimism must inform current valuation decisions, particularly when dealing with home valuations less than offers.

Sentiment-Adjusted Valuation Framework

Professional surveyors must balance backward-looking transaction evidence with forward-looking market sentiment:

1. Expectation Discounting 💭

When short-term price expectations reach -43%, this signals widespread anticipation of value decline. Valuation adjustments should:

- Apply modest discounts (2-5%) to comparable evidence from rising market periods

- Increase the weight given to most recent transactions

- Explicitly state market direction assumptions in valuation reports

- Consider scenario analysis for high-value or complex properties

2. Transaction Volume Considerations

The collapse in agreed sales to -34% creates a liquidity discount scenario:

- Properties in illiquid markets trade at discounts to theoretical open-market value

- Extended marketing periods increase holding costs and seller motivation

- Reduced buyer competition eliminates bidding premium effects

- Consider "quick sale" versus "patient marketing" valuation scenarios

3. Mortgage Valuation Conservatism

Lenders increasingly demand conservative valuations during periods of market uncertainty. Surveyors conducting mortgage valuations should:

- Apply explicit risk adjustments for properties at upper price brackets

- Consider loan-to-value ratios in the context of potential near-term depreciation

- Document market velocity and liquidity constraints

- Provide clear commentary on market outlook and value sustainability

Evidence Hierarchy in Declining Markets

During the February 2026 RICS Survey Slump, the traditional evidence hierarchy requires recalibration:

Highest Weight:

- Completed sales within past 8 weeks in immediate locality

- Current asking prices for comparable properties (adjusted for negotiation)

- Properties under offer with known offer prices

- Recent price reductions on comparable properties

Moderate Weight:

5. Sales completed 8-16 weeks ago (with time adjustment)

6. Agent feedback on buyer behavior and negotiation patterns

7. Rental market evidence (yield approach for investment properties)

Lower Weight:

8. Sales completed more than 16 weeks ago

9. Asking prices without market feedback

10. Historical appreciation trends (now disrupted)

For chartered surveyors in Hammersmith, Fulham, and Ealing, this evidence hierarchy shift reflects the acute weakness in inner London markets.

Professional Standards and Documentation Requirements

The Valuation Adjustments Amid February 2026 RICS Survey Slump demand enhanced professional standards and documentation protocols. RICS valuation standards (Red Book) require surveyors to reflect market conditions accurately and provide sufficient reasoning for valuation conclusions.

Enhanced Reporting Requirements 📝

Market Context Section:

Every valuation report during this period should include:

- Explicit reference to RICS survey data showing market weakness

- Regional-specific market commentary with supporting statistics

- Analysis of buyer enquiry trends and transaction volumes

- Forward-looking market outlook with scenario considerations

Assumption Transparency:

Clearly document assumptions regarding:

- Marketing period expectations (typically extended during weak demand)

- Buyer negotiation leverage and likely offer-to-asking ratios

- Market direction over the valuation's relevant time horizon

- Comparable adjustment rationale with specific percentage impacts

Uncertainty and Sensitivity:

For high-value or complex properties:

- Provide valuation ranges rather than single-point estimates

- Conduct sensitivity analysis on key assumptions

- Discuss factors that could cause material valuation variance

- Consider "market value" versus "forced sale value" scenarios

Risk Management for Surveyors

The combination of weak buyer enquiries and negative price expectations creates elevated professional liability exposure:

Mitigation Strategies:

- Conservative bias: When evidence is ambiguous, favor lower valuations

- Peer review: Implement internal review for valuations above threshold amounts

- Client communication: Ensure clients understand market uncertainty and valuation limitations

- Documentation rigor: Maintain detailed working papers supporting all adjustments

- Update protocols: Establish procedures for valuation updates if market conditions deteriorate further

Rental Market Considerations and Alternative Valuation Approaches

While sales markets experienced severe weakness, the February 2026 RICS survey showed tenant demand remained broadly stable at +2%, though landlord instructions stayed firmly negative at -27%[1]. This divergence creates opportunities for alternative valuation approaches.

Investment Property Valuation Adjustments

For buy-to-let and commercial residential properties:

Yield Compression Analysis:

- Rental growth expectations: 20% of surveyors anticipated rent increases over three months[1]

- Capital value uncertainty: Use yield-based valuations as cross-check

- Tenant demand stability: Provides downside protection versus owner-occupied comparables

- Supply constraints: Landlord exit continues supporting rental values

Dual Valuation Approach:

- Comparable sales method (primary): Adjusted for weak buyer enquiries

- Investment method (secondary): Rental income capitalized at appropriate yield

- Reconciliation: Where methods diverge significantly, investigate and document reasoning

This approach proves particularly valuable for chartered surveyors in Sussex, Oxfordshire, and Hertfordshire, where rental markets show relative resilience.

Practical Implementation: Case Study Approach

Consider a typical valuation scenario during the February 2026 slump:

Property: 3-bedroom semi-detached house, South East England

Client requirement: Mortgage valuation for purchase

Offer price: £450,000

Comparable evidence: Three sales at £440,000-£465,000 (completed 10-16 weeks ago)

Traditional Approach:

- Average comparables: £452,500

- Minor adjustments for condition/location: -£2,500

- Valuation: £450,000 ✅ Supports offer

Adjusted Approach (February 2026 Context):

- Average comparables: £452,500

- Time adjustment for market deterioration (-3%): -£13,575

- Buyer enquiry weakness adjustment (-2%): -£8,785

- Extended marketing period risk: -£5,000

- Valuation: £425,000 ⚠️ Below offer price

This £25,000 difference reflects the application of Valuation Adjustments Amid February 2026 RICS Survey Slump techniques, protecting both lender and borrower from overpayment in a declining market.

Strategic Recommendations for Surveyors and Property Professionals

Navigating the February 2026 market conditions requires strategic adaptation across multiple dimensions:

For Chartered Surveyors:

1. Continuous Market Intelligence 🔍

- Subscribe to weekly RICS survey updates

- Maintain relationships with local estate agents for real-time feedback

- Monitor mortgage rate movements and lending criteria changes

- Track regional divergence patterns for location-specific insights

2. Methodology Enhancement

- Develop standardized adjustment matrices for different market conditions

- Implement scenario analysis for valuations above £500,000

- Create template commentary addressing current market weakness

- Establish peer review protocols for challenging valuations

3. Client Education

- Proactively communicate market conditions to clients

- Explain valuation adjustments and their protective purpose

- Manage expectations regarding valuation outcomes

- Provide market outlook context beyond single-point valuations

For Property Buyers:

Negotiation Leverage:

The -26% buyer enquiry collapse creates substantial negotiation power:

- Request recent comparable evidence from sellers

- Highlight extended marketing periods and price reductions

- Commission independent valuations before finalizing offers

- Consider contingency clauses for further market deterioration

For Sellers and Agents:

Realistic Pricing:

- Accept that February-March 2026 represents a genuine market reset

- Price properties 5-10% below comparable evidence from Q4 2025

- Prepare for extended marketing periods (12-16 weeks versus 8-10 weeks)

- Consider rental options if sales market proves unworkable

Future Outlook and Monitoring Indicators

The shift in 12-month expectations from +43% to +2%[3] suggests surveyors should monitor several key indicators for signs of market stabilization or further deterioration:

Leading Indicators to Watch:

- 📈 Mortgage rate trends: Stabilization would support buyer confidence recovery

- 🏦 Lending criteria: Any tightening would compound demand weakness

- 💼 Employment data: Job market strength underpins housing demand

- 🌍 Geopolitical developments: Resolution of conflicts supporting rate normalization

- 📊 RICS monthly surveys: First positive buyer enquiry reading would signal turning point

Potential Scenarios:

Optimistic (30% probability):

- Mortgage rates stabilize by Q3 2026

- Buyer enquiries return to neutral by autumn

- Prices stabilize with modest regional variation

- Transaction volumes recover to long-term averages

Base Case (50% probability):

- Weak demand persists through H2 2026

- Prices decline 3-5% nationally, 7-10% in London/South East

- Transaction volumes remain 15-20% below historical norms

- Regional divergence continues with northern resilience

Pessimistic (20% probability):

- Further mortgage rate increases

- Buyer enquiries deteriorate beyond -40%

- Price declines accelerate to 8-12% nationally

- Transaction market approaches 2008-2009 levels of illiquidity

Conclusion

The Valuation Adjustments Amid February 2026 RICS Survey Slump: Techniques for Weak Buyer Enquiries and Price Caution represent a critical inflection point for UK property valuation practice. The collapse in buyer enquiries to -26% in February and -39% by March, combined with short-term price expectations reaching -43%, demands fundamental recalibration of valuation methodologies[1][3].

Chartered surveyors must move beyond mechanical application of historical comparable evidence, instead incorporating forward-looking market sentiment, regional divergence patterns, and liquidity constraints into their assessments. The techniques outlined—time-adjusted comparable analysis, sentiment-adjusted frameworks, enhanced documentation protocols, and scenario-based approaches—provide practical tools for maintaining valuation accuracy and professional credibility during market uncertainty.

Key Actionable Steps:

- Implement enhanced comparable adjustment matrices that explicitly account for market velocity changes and buyer enquiry weakness

- Adopt regional-specific valuation approaches recognizing the -40% London versus positive northern divergence

- Strengthen documentation and assumption transparency to manage professional liability and client expectations

- Monitor leading indicators continuously for signs of market stabilization or further deterioration

- Consider alternative valuation methods (investment approach) where rental markets show relative resilience

The February 2026 RICS survey data provides clear evidence that the UK housing market has entered a period of significant adjustment. Surveyors who adapt their methodologies proactively, maintain conservative professional judgment, and communicate market realities transparently will best serve their clients and protect their professional standing during this challenging period.

For property professionals seeking expert guidance through these market conditions, engaging experienced chartered surveyors in London and surrounding regions ensures valuations reflect current realities while maintaining professional standards and regulatory compliance.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Uk Rics Residential Market Survey Mar 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-mar-2026

[3] Uk Residential Market Survey March 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey-March-2026.pdf

[4] Valuation Divergence North Vs South Uk House Prices In 2026 And Surveyor Adjustment Techniques – https://nottinghillsurveyors.com/blog/valuation-divergence-north-vs-south-uk-house-prices-in-2026-and-surveyor-adjustment-techniques