Twelve-month sales expectations jumped to a net balance of +35% in January 2026 — the strongest reading since December 2024 — yet near-term confidence sits at a cautious +4%. That gap tells chartered surveyors everything they need to know about the challenge ahead: the market is recovering, but it is doing so unevenly, and valuations must reflect that nuance with precision.

Chartered Surveyor Valuations in a Stabilizing Market: Adjusting for RICS January 2026 Optimism is not simply a matter of applying a blanket upward revision to comparable evidence. It requires a disciplined, regionally sensitive methodology that honours what the RICS January 2026 data actually says — and what it deliberately does not say.

Key Takeaways

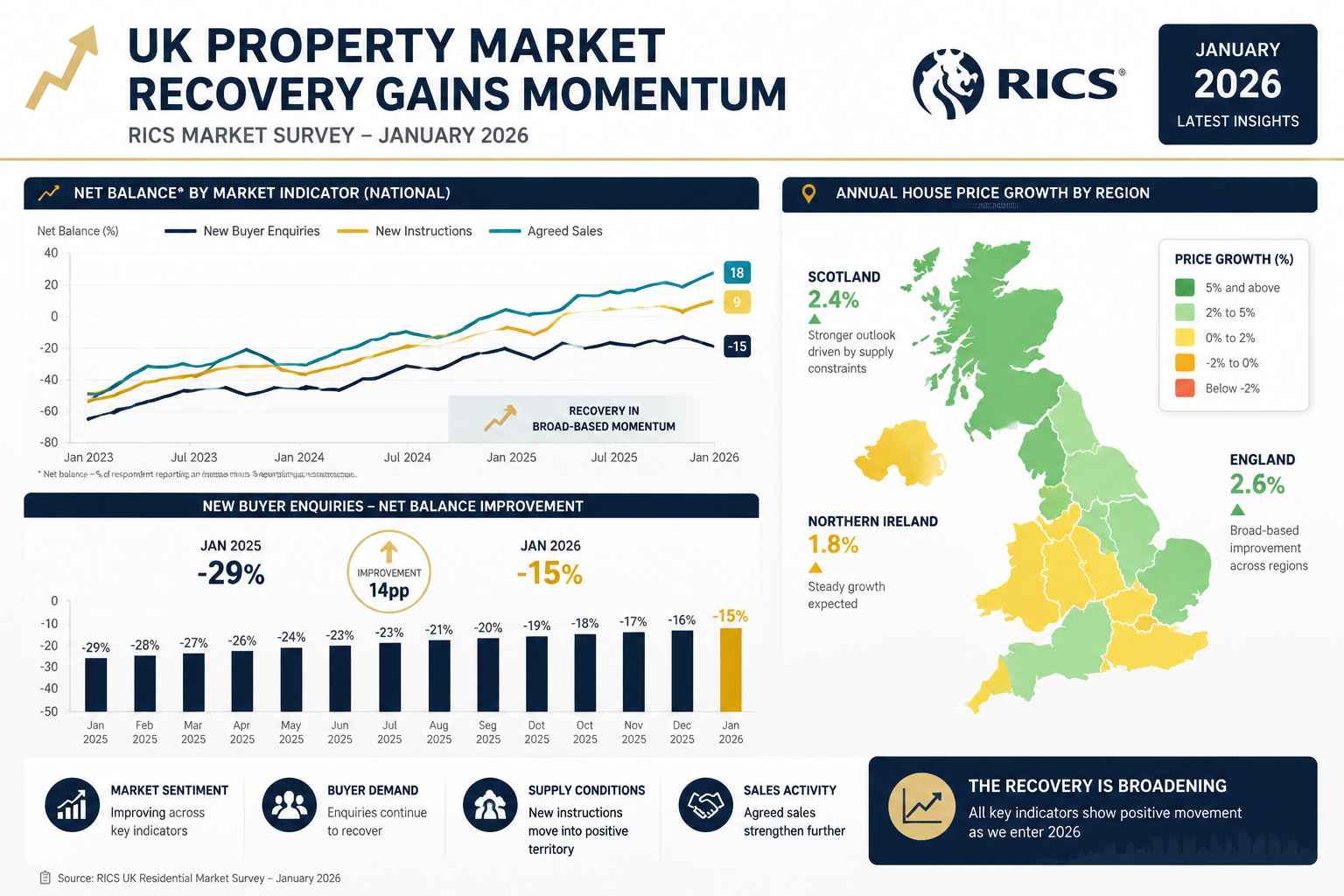

- Buyer enquiries improved to a net balance of -15% in January 2026, up from -29% in November 2025, signalling easing downward pressure on demand.

- House price net balance recovered to -10% from a low of -19% in October 2025, suggesting a potential turning point rather than a confirmed recovery.

- Regional divergence is significant: Scotland, Northern Ireland, and the North West outperform, while London, the South East, and East Anglia continue to lag.

- Comparable evidence windows should be compressed in a stabilizing market, with stronger weighting given to transactions aged 0-3 months.

- Time adjustments on older comparables should remain minimal — typically 0.0% to -0.1% per month — unless local evidence justifies a larger correction.

What the RICS January 2026 Data Actually Shows

The RICS UK Residential Survey for January 2026 paints a picture of cautious but genuine stabilization [1]. Three headline indicators deserve close attention from any practitioner involved in residential or commercial property valuation.

Buyer Enquiries

New buyer enquiries improved to a net balance of -15% in January 2026, up from -21% in December and -29% in November 2025 [1]. The figure is still negative — more surveyors reported falling enquiries than rising ones — but the trajectory is clearly improving. For valuation purposes, this matters because demand is a leading indicator. A sustained improvement in enquiries typically precedes price stabilization by one to two quarters.

House Prices

The net balance for house prices over the past three months stood at -10% in January 2026, recovering from a low of -19% in October 2025 [1]. This is not price growth; it is a slowing of price decline. Surveyors must be careful not to conflate stabilization with recovery when selecting and adjusting comparable evidence.

Sales Expectations

The divergence between near-term and twelve-month expectations is the most instructive data point of all. Near-term sales expectations eased to just +4%, while twelve-month expectations reached +35% [1]. This suggests that market participants believe conditions will improve materially over the year, but that the immediate pipeline remains constrained — likely by affordability pressures and residual mortgage rate uncertainty.

"The January 2026 RICS data does not signal a return to pre-2022 conditions. It signals that the floor may have been found — and that is a very different thing for a valuer to work with."

Regional Divergence and Its Impact on Valuation Methodology

One of the most consequential findings in the January 2026 survey is the scale of regional divergence [1]. Understanding this divergence is central to any credible approach to Chartered Surveyor Valuations in a Stabilizing Market: Adjusting for RICS January 2026 Optimism.

Where the Market Is Stronger

Price growth remains strongest in Scotland and Northern Ireland, with upward trends also reported in the North West and North of England [1]. In these markets, surveyors may find that:

- Comparable evidence from six months ago undervalues the current market

- Demand-side pressure from tenant enquiries (which edged higher in the three months to January 2026) is beginning to translate into purchase activity

- Upward time adjustments on older comparables may be justified, though they should be applied conservatively and documented carefully

Where the Market Continues to Lag

London, the South East, South West, and East Anglia continue to underperform the national average [1]. In these regions:

- National indices are likely to overstate local conditions

- Comparable evidence should be weighted heavily toward the most recent transactions

- Surveyors should be alert to the risk of over-optimism when interpreting the +35% twelve-month sales expectation figure at a local level

This regional picture reinforces a core principle: national sentiment data from RICS surveys should inform, but never replace, local comparable evidence [2].

A Practical Framework for Regional Adjustment

| Region | Price Trend (Jan 2026) | Suggested Comparable Window | Time Adjustment Direction |

|---|---|---|---|

| Scotland / N. Ireland | Positive | 0-6 months | Neutral to slight positive |

| North West / North | Improving | 0-4 months | Neutral |

| Midlands / Wales | Broadly flat | 0-3 months | Neutral to slight negative |

| London / South East | Lagging | 0-3 months preferred | Slight negative on older data |

| South West / East Anglia | Lagging | 0-3 months preferred | Slight negative on older data |

For practitioners working in specific locations, understanding hyper-local conditions is essential. Those operating in areas such as St Albans or Putney will find that even within the broader South East underperformance trend, micro-market variations can be significant.

Adjusting Comparable Evidence in a Stabilizing Market

The technical challenge of Chartered Surveyor Valuations in a Stabilizing Market: Adjusting for RICS January 2026 Optimism lies in selecting and weighting comparable transactions appropriately when the market is neither clearly rising nor clearly falling.

Compressing the Evidence Window

In a stabilizing market, the evidence window for comparable transactions should be compressed [3]. The standard approach of accepting comparables up to twelve months old becomes problematic when conditions have shifted materially over that period. The recommended approach is:

- 0-3 months old: Use with minimal or no time adjustment. These transactions best reflect current market sentiment.

- 3-6 months old: Apply a small negative time adjustment, typically in the range of 0.0% to -0.1% per month, unless local evidence suggests the market has moved in a different direction [3].

- 6-12 months old: Treat with caution. These transactions may reflect a materially different market environment, particularly given that the house price net balance was at its lowest point (-19%) in October 2025 [1]. Significant adjustments or exclusion may be warranted.

- Over 12 months: Generally avoid unless no more recent evidence is available, and document the reasoning thoroughly.

Documenting Adjustments Transparently

RICS Red Book Global Standards require that any adjustments to comparable evidence are clearly reasoned and documented. In a stabilizing market, this is more important than ever. A valuation report that simply states "adjusted for market conditions" without quantifying or evidencing those adjustments will not withstand scrutiny — whether from a lender, a tribunal, or a client.

Key documentation best practices include:

- Stating the net balance figures from the most recent RICS survey as context

- Identifying whether the subject property falls within a stronger or weaker regional sub-market

- Quantifying time adjustments as a percentage per month with supporting rationale

- Cross-referencing at least three comparables where possible, noting any outliers

Understanding what factors are examined during a property valuation helps clients appreciate why this level of detail matters and why a chartered surveyor's judgment is irreplaceable.

The Risk of Anchoring to Optimism

The +35% twelve-month sales expectation is an encouraging figure, but it represents sentiment, not transacted evidence. Surveyors who anchor their valuations to forward-looking optimism rather than backward-looking comparable evidence risk producing figures that are not supportable under Red Book methodology. The appropriate response to improving sentiment is to:

- Monitor comparable evidence closely for signs that prices are beginning to move

- Narrow the evidence window to capture the most current transactions

- Avoid applying upward adjustments that are not yet supported by transacted data

This discipline is especially important for capital gains tax valuations and SIPP pension fund valuations, where the valuation date is fixed and the figure carries significant financial and legal consequences.

The Lettings Market: A Supporting Data Point for Residential Valuers

The lettings market data from January 2026 provides a useful secondary lens for residential valuers [1]. Tenant demand edged higher in the three months to January 2026, ending two consecutive quarters of flat or negative readings. However, landlord instructions remained negative, indicating that supply constraints persist.

For residential valuers, this matters in two ways:

Investment yield assessment: Properties with strong rental demand in supply-constrained areas may command a valuation premium relative to comparable owner-occupied stock, particularly where the landlord instruction trend suggests further supply tightening.

Demand signal: Rising tenant demand can be a leading indicator of future purchase activity, as renters who face escalating costs often convert to buyers when mortgage affordability improves. This supports the broader narrative of gradual recovery embedded in the +35% twelve-month sales expectation.

Valuers preparing reports for landlords or investors should also be aware of evolving property market legislation changes that may affect rental yields and investment valuations in 2026.

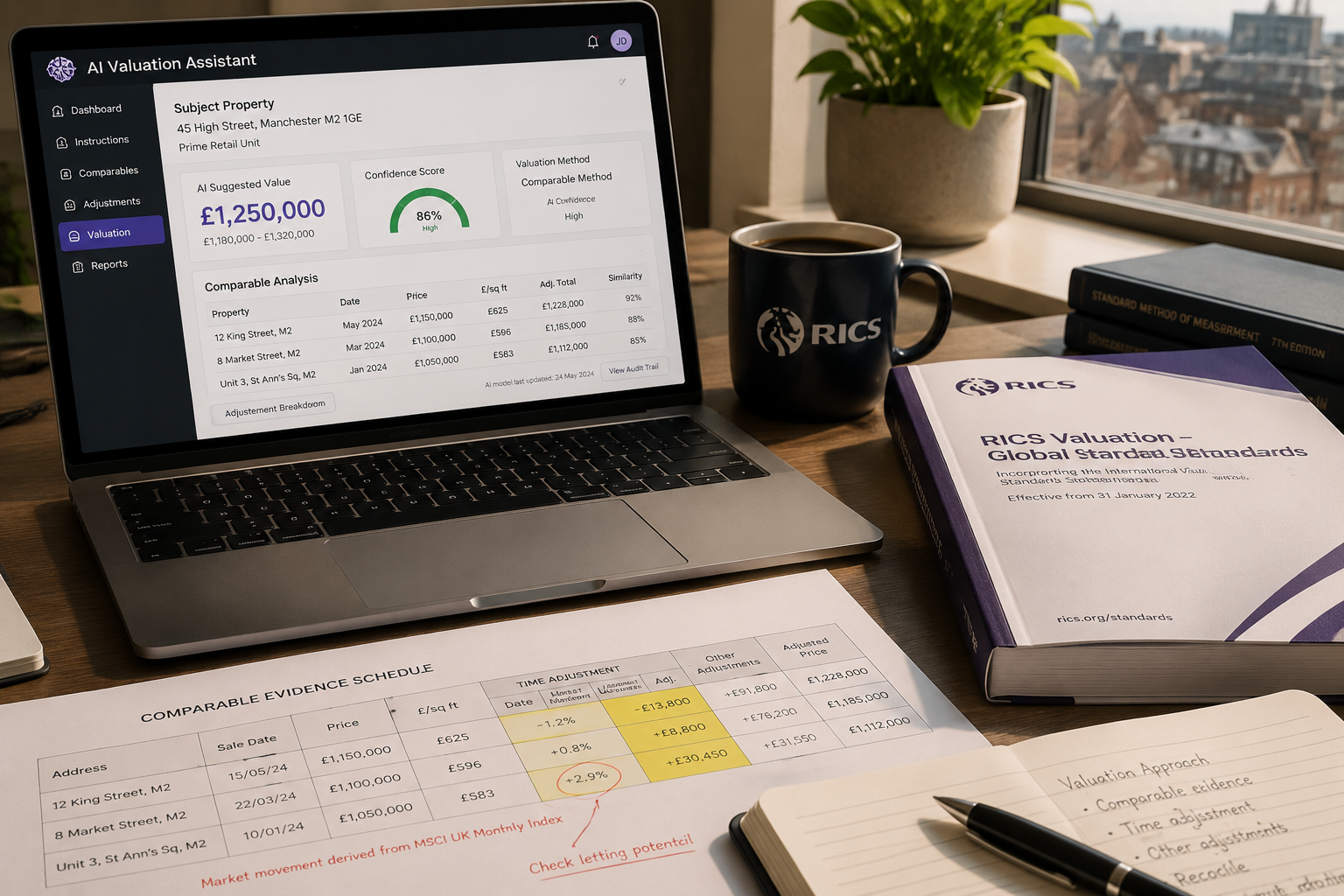

Technology and AI: The Emerging Tool in Valuation Practice

The RICS professional standard on the responsible use of artificial intelligence in surveying practice came into effect on 9 March 2026 [4]. This is a significant development for chartered surveyor valuations in a stabilizing market, because AI tools are increasingly being used to:

- Aggregate and filter comparable evidence at scale

- Identify regional sub-market trends from large transaction datasets

- Flag anomalies in comparable selection that a manual review might miss

However, the RICS standard is clear that AI is a tool to support professional judgment, not replace it [4]. In a market as nuanced as the current one — where a national net balance of -10% conceals wide regional variation — the interpretation of AI-generated outputs requires the same level of professional skill as any other aspect of the valuation process.

Surveyors should:

- Document which AI tools were used and how outputs were verified

- Ensure that AI-generated comparable selections are reviewed against local knowledge

- Never present AI outputs as the basis for a valuation without independent professional verification

This aligns with the Prince Chartered Surveyors approach to combining technology with rigorous professional standards.

Practical Guidance for Clients Commissioning Valuations in 2026

For property owners, buyers, and investors commissioning valuations in the current environment, understanding how a chartered surveyor is working with the RICS January 2026 data is genuinely useful. Here is what to expect from a well-conducted valuation in a stabilizing market:

- A narrower comparable window: Expect the surveyor to focus on transactions from the past three months, with older evidence used sparingly and with explicit adjustment.

- Regional context: The report should acknowledge whether the subject property sits in a stronger or weaker regional sub-market and reflect that in the evidence selection.

- Conservative time adjustments: Upward adjustments should not be applied unless supported by transacted evidence, not just survey sentiment.

- Clear documentation: Every adjustment should be quantified and reasoned, not simply asserted.

- A distinction between current value and future value: The surveyor's job is to assess Market Value as at the valuation date — not to project what the property might be worth in twelve months if the +35% sales expectation materialises.

If a valuation figure comes back lower than expected, it is worth understanding what to do if your home valuation is less than an offer before taking any further steps.

For those considering a full structural assessment alongside their valuation, a Level 3 full building survey provides the most comprehensive picture of a property's condition — information that is directly relevant to any valuation adjustment for physical defects.

Conclusion

The RICS January 2026 survey data offers genuine grounds for cautious optimism. Buyer enquiries are improving month on month, house price declines are moderating, and twelve-month sales expectations have reached their highest point in over a year. But Chartered Surveyor Valuations in a Stabilizing Market: Adjusting for RICS January 2026 Optimism demands that practitioners treat this data as context, not instruction.

The core discipline remains unchanged: select the most relevant comparable evidence, apply transparent and proportionate adjustments, and produce a figure that reflects the market as it is — not as participants hope it will be.

Actionable next steps for practitioners and clients:

- Review comparable evidence windows and compress them to 0-3 months where possible in lagging regions

- Cross-reference national RICS sentiment data against local transaction evidence before applying any time adjustments

- Document all adjustments with explicit reference to regional sub-market conditions

- Engage with the new RICS AI professional standard to understand how technology can support — but not substitute — valuation judgment

- Commission valuations from RICS-regulated chartered surveyors who demonstrate clear methodology and regional knowledge, particularly for tax, pension, or litigation purposes

The market is stabilizing. Valuations should reflect that stabilization with precision, not enthusiasm.

References

[1] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution?utm_source=openai

[2] Valuation Strategies For Regional Price Flatness In Spring 2026 Rics Data For Divergent UK Markets – https://nottinghillsurveyors.com/blog/valuation-strategies-for-regional-price-flatness-in-spring-2026-rics-data-for-divergent-uk-markets?utm_source=openai

[3] Valuing Stabilised National Prices In Early 2026 Rics Techniques From January Survey Insights – https://kingstonsurveyors.com/valuing-stabilised-national-prices-in-early-2026-rics-techniques-from-january-survey-insights/?utm_source=openai

[4] What Surveyors Think AI – https://ww3.rics.org/uk/en/modus/technology-and-data/surveying-tools/what-surveyors-think-ai.html?utm_source=openai