1.8 million fixed-rate mortgages expire in 2026 — and every week of delay in a property transaction now carries a measurable financial cost. With the Bank of England base rate held at 3.75% yet lender SVRs averaging 7.13–7.15%, the gap between a smoothly completed deal and a stalled one can translate into thousands of pounds of unnecessary borrowing costs [1]. For buyers and sellers navigating this environment, party wall disputes have quietly emerged as one of the most common — and most avoidable — causes of transaction delay.

This article examines how UK Mortgage Rate Volatility 2026: Party Wall Risk Mitigation for Delayed Transactions intersects with lender timelines, offer expiry windows, and the legal framework of the Party Wall etc. Act 1996. Understanding this connection is no longer optional for anyone involved in a property purchase or renovation project this year.

Key Takeaways 📌

- SVR rates average 7.13–7.15% in 2026, meaning every month of delay on a mortgage rollover costs borrowers significantly more than necessary.

- Party wall disputes are a leading cause of transaction delays — and many are entirely preventable with early action.

- A party wall notice must be served at least two months before work begins, making early engagement critical in volatile rate environments.

- Mortgage offer validity windows (typically 3–6 months) can expire during protracted party wall negotiations, forcing borrowers to reapply at potentially worse rates.

- Proactive party wall surveys, schedules of condition, and early surveyor appointments are the most effective risk mitigation tools available in 2026.

The 2026 Mortgage Rate Landscape: Why Every Week Matters

Rate Volatility Is Reshaping Buyer Behaviour

Spring 2026 has delivered a mortgage market defined by uncertainty. The Bank of England held its base rate at 3.75% in April 2026, yet expert opinion remains sharply divided — some analysts forecast rate cuts later in the year, others predict further rises, and a third camp expects stability [1]. This ambiguity is pushing borrowers away from five-year fixed products and toward shorter two-year deals, which are pricing around 5.0% [6].

The practical consequence: buyers are more rate-sensitive than at any point in the past decade. A mortgage offer secured today at a competitive fixed rate carries an expiry date. If a transaction stalls — for any reason — that offer may lapse, forcing a reapplication at whatever rate the market offers at that future point.

💬 "Rate shock is real. Borrowers who entered the market expecting stability are now recalibrating every few weeks." — MPA Magazine, 2026 [6]

The Numbers Behind the Risk

| Mortgage Product | Average Rate (April 2026) | Lender Range |

|---|---|---|

| Standard Variable Rate (SVR) | 7.13–7.15% | 6.31% (Newcastle BS) to 8.38% (Aldermore) |

| Five-Year Fixed | 5.54% | Varies by LTV and lender |

| Two-Year Fixed | ~5.0% | Market-dependent |

| Bank of England Base Rate | 3.75% | N/A |

Source: HOA Mortgage Rate Forecast, April 2026 [1]

The spread between SVR and a five-year fixed deal represents a 1.59–1.61 percentage point saving for borrowers who remortgage successfully [1]. On a £300,000 mortgage, that differential equates to roughly £4,770 per year. Every month a transaction is delayed — and a mortgage offer edges closer to expiry — increases the probability of rolling onto an SVR, even temporarily.

Gross mortgage lending is forecast to reach £300 billion in 2026, a 4% increase, yet house purchase lending grows only 2% to £180 billion [3]. Transaction volumes are expected to fall 1% to 1.202 million — 10,000 fewer completions than 2025 [3]. The market is active but fragile, and delays are disproportionately costly in this environment.

For those preparing a property for sale, understanding how to prepare your property for market — including resolving any outstanding party wall matters — is a critical first step.

Understanding Party Wall Risk in Delayed Transactions

What Is a Party Wall, and Why Does It Cause Delays?

A party wall is a shared wall, boundary, or structure between two properties. Under the Party Wall etc. Act 1996, any building owner intending to carry out work affecting a party wall must serve formal notice on adjoining owners — typically two months before work begins for party wall works, or one month for excavation works.

When buyers discover mid-transaction that a property has unresolved party wall matters — or when a planned renovation triggers the Act — timelines can extend dramatically. Disputes between building owners and adjoining owners can take weeks to months to resolve, particularly if a party wall award needs to be formally agreed.

For anyone buying a property and planning immediate works, the advice is clear: don't forget the Party Wall Act when buying a house. Ignoring it is not a legal option — and the consequences of ignoring the Party Wall Act can include injunctions, forced demolition of completed work, and significant legal costs.

Common Scenarios Where Party Wall Issues Delay Transactions 🏠

1. Loft conversions on semi-detached or terraced properties

Loft conversions almost always affect party walls. If a seller has completed a loft conversion without serving proper notice, a buyer's surveyor may flag this as a legal defect. Resolving it — even retrospectively — takes time. Learn more about whether loft conversions require party wall agreements.

2. Basement excavations near shared boundaries

Excavation within 3–6 metres of an adjoining structure triggers the Act. These works are common in London and South East England, where buyers frequently plan basement extensions.

3. Structural alterations to shared walls

Removing chimney breasts, installing steel beams, or cutting into party walls all require formal notice and, where neighbours dissent, a surveyor-agreed party wall award.

4. Disputes inherited from previous owners

A property may have unresolved party wall disputes from previous works. These can surface during conveyancing searches and halt a transaction unexpectedly.

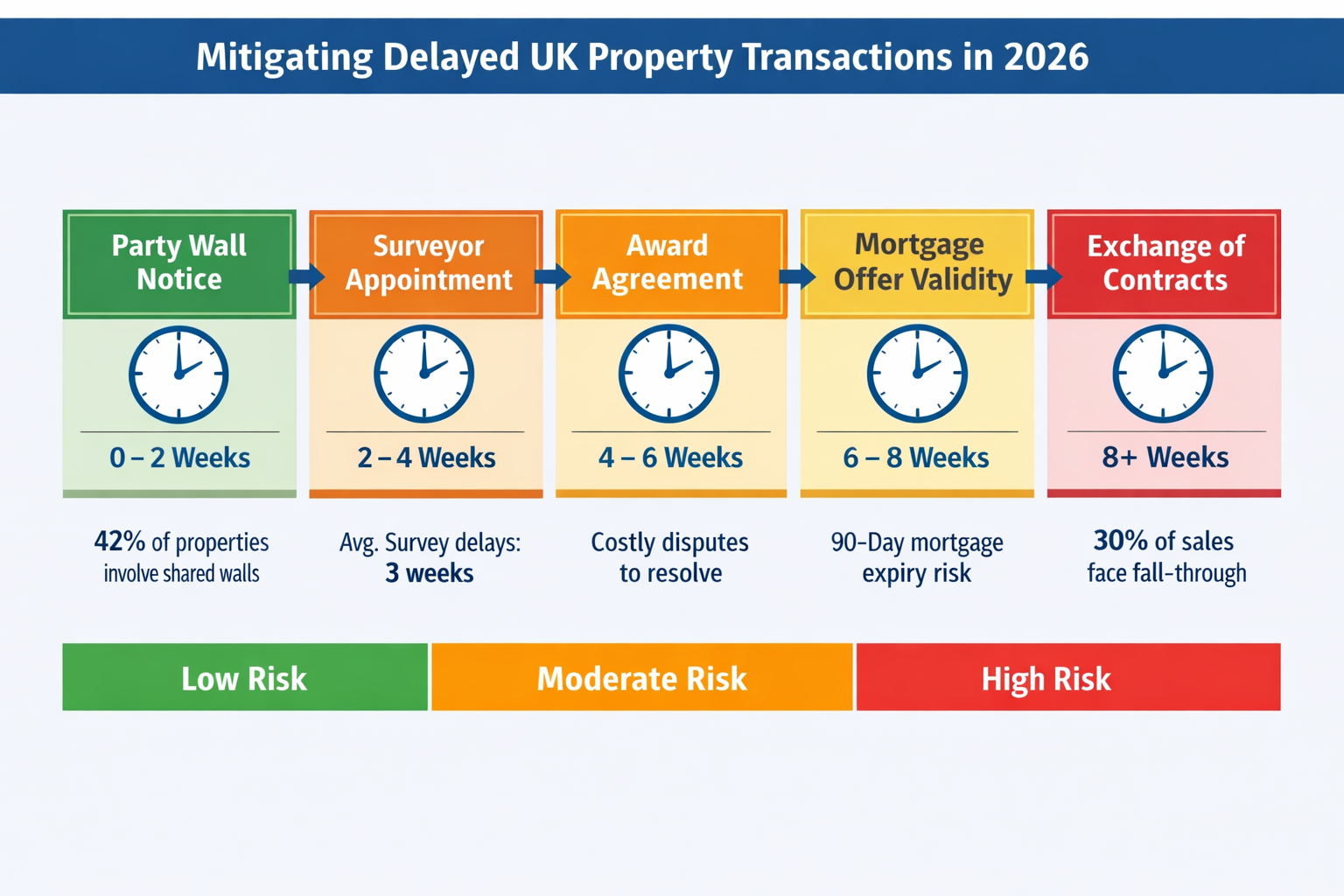

The Timeline Problem: Party Wall Notices vs. Mortgage Offer Expiry

Here is where UK Mortgage Rate Volatility 2026: Party Wall Risk Mitigation for Delayed Transactions becomes acutely relevant. Consider this typical scenario:

- Buyer receives mortgage offer: Week 1

- Conveyancer discovers unresolved party wall matter: Week 4

- Party wall notice served on neighbour: Week 5

- Neighbour dissents; surveyors appointed: Week 7

- Party wall award agreed: Week 14–18

- Mortgage offer expires (standard 3-month window): Week 13

The buyer is now forced to reapply for a mortgage — potentially at a higher rate — or request an extension from the lender, which is not guaranteed. In a volatile rate environment where two-year fixed deals are climbing and SVRs average over 7%, this is a genuinely costly outcome [2].

UK Mortgage Rate Volatility 2026: Party Wall Risk Mitigation for Delayed Transactions — Practical Strategies

Strategy 1: Commission a Party Wall Schedule of Condition Early

A party wall schedule of condition is a detailed photographic and written record of the adjoining property's condition before any works begin. Commissioning this early in the transaction process serves two purposes:

- It demonstrates good faith to adjoining owners, reducing the likelihood of disputes.

- It protects all parties from spurious damage claims after works are completed, which can otherwise trigger lengthy and expensive post-completion disputes.

In a 2026 market where transaction volumes are already under pressure [3], a schedule of condition is a low-cost tool that can prevent high-cost delays.

Strategy 2: Serve Party Wall Notices Before Exchange

The most effective risk mitigation strategy is also the simplest: serve party wall notices before exchanging contracts. This is counterintuitive for many buyers, who assume notice should follow completion. However, serving notice early means the statutory two-month period runs concurrently with conveyancing, rather than after it.

This approach requires buyers to commit to a property before exchange — but given that 5 common misconceptions about party wall agreements frequently cause buyers to underestimate the timeline, early action is always preferable.

Strategy 3: Appoint a Specialist Party Wall Surveyor Immediately

When a neighbour dissents to a party wall notice, both parties are entitled to appoint surveyors — or agree on a single agreed surveyor. Delays in appointing surveyors are the single largest cause of extended party wall timelines.

A specialist party wall surveyor will:

- ✅ Prepare and serve notices correctly (errors restart the clock)

- ✅ Negotiate with the adjoining owner's surveyor efficiently

- ✅ Draft a party wall award that protects both parties

- ✅ Coordinate with structural engineers where required

Understanding how engineers interact with party wall processes is particularly important for complex structural works, where engineering sign-off and party wall awards must align.

Strategy 4: Request Extended Mortgage Offer Validity

Not all lenders will agree, but many will extend a mortgage offer by 1–3 months when presented with a documented reason — such as an ongoing party wall process. The key is to communicate proactively, before the offer expires, not after. Mortgage brokers operating in the 2026 market are increasingly familiar with this request, given the volume of transactions affected by rate volatility and legal delays [2].

Strategy 5: Build Rate Protection Into Financial Planning

With 1.8 million fixed-rate mortgages expiring in 2026 [3], borrowers should model their finances against a range of rate scenarios. If a transaction delays and a reapplication becomes necessary:

- SVR exposure: Even a 30-day SVR period at 7.13–7.15% on a £400,000 mortgage costs approximately £950–£960 in additional interest compared to a 5.54% fixed rate.

- Product transfer options: Many lenders allow internal product transfers without a full reapplication, which can protect borrowers from the worst of market volatility [3].

- Rate lock agreements: Some lenders offer rate lock periods of up to 6 months, providing a buffer against market movements during extended transactions.

Strategy 6: Use Party Wall Drawings to Accelerate Agreement

Professionally prepared party wall drawings give adjoining owners and their surveyors a clear, unambiguous picture of proposed works. Disputes frequently arise not from genuine objection to works, but from confusion about their scope. High-quality drawings reduce that ambiguity and accelerate agreement — directly compressing the timeline risk that threatens mortgage offer validity.

The Broader Context: Geopolitical Risk, Market Sentiment, and Transaction Certainty

Mortgage rate volatility in 2026 is not purely a domestic phenomenon. Geopolitical uncertainty — including Middle East conflict concerns — is feeding market instability and influencing swap rates, which in turn affect fixed mortgage pricing [6]. Building surveyors are already adjusting valuations to account for interest rate volatility and geopolitical risk [7], and lenders are pricing that uncertainty into their products.

For property buyers, this external volatility reinforces the importance of controlling what can be controlled. Party wall compliance, early notice service, and proactive surveyor engagement are all within a buyer's control. Swap rate movements and Bank of England decisions are not.

Transaction volumes are forecast to fall to 1.202 million in 2026 — 10,000 fewer than 2025 [3]. In a contracting market, chains are more fragile, and a single delayed transaction can collapse multiple linked sales. Party wall risk mitigation is therefore not just about protecting one buyer's mortgage rate — it protects the entire chain.

For those working with chartered surveyors in London or across the South East, engaging professionals early in the process is the most reliable way to compress transaction timelines and protect against rate exposure.

Quick Reference: Party Wall Risk Mitigation Checklist for 2026 Transactions ✅

| Action | Timing | Priority |

|---|---|---|

| Identify whether Party Wall Act applies | Before making offer | 🔴 Critical |

| Commission schedule of condition | At offer acceptance | 🔴 Critical |

| Serve party wall notice | Before exchange | 🔴 Critical |

| Appoint specialist surveyor | Immediately on dissent | 🔴 Critical |

| Request mortgage offer extension if needed | 4+ weeks before expiry | 🟠 High |

| Obtain party wall drawings | Before notice served | 🟠 High |

| Model rate scenarios for delay periods | At mortgage application | 🟡 Medium |

| Communicate with lender proactively | Throughout process | 🟡 Medium |

Conclusion: Certainty Is the Currency of the 2026 Property Market

UK Mortgage Rate Volatility 2026: Party Wall Risk Mitigation for Delayed Transactions is not an abstract concern — it is a practical, financial reality for tens of thousands of buyers and sellers this year. With SVRs averaging over 7%, fixed-rate savings of 1.6 percentage points available to those who complete on time, and 1.8 million mortgage deals expiring across the year, the cost of delay has never been higher [1][3].

Party wall matters are among the most common — and most preventable — causes of transaction delay. The strategies outlined above are not complex or expensive. They require early action, professional engagement, and clear communication.

Actionable next steps:

- Determine immediately whether the Party Wall etc. Act 1996 applies to any planned works on the property being purchased or sold.

- Engage a specialist party wall surveyor before exchange of contracts — not after.

- Commission a schedule of condition to protect all parties and reduce dispute risk.

- Communicate proactively with your mortgage lender about any potential delays, and explore offer extension options before the deadline.

- Model your finances against a range of rate scenarios, including a period of SVR exposure, so that any delay is a managed inconvenience rather than a financial shock.

In a market defined by volatility, certainty is the most valuable asset a buyer or seller can create — and party wall risk mitigation is one of the most direct routes to achieving it.

References

[1] Mortgage Rate Forecast – https://hoa.org.uk/advice/guides-for-homeowners/for-owners/mortgage-rate-forecast/

[2] UK Mortgage Market Faces Renewed Volatility As Rates Climb In Spring 2026 – https://www.bradleys-estate-agents.co.uk/articles/uk-mortgage-market-faces-renewed-volatility-as-rates-climb-in-spring-2026

[3] Modest Growth Forecast Mortgage Lending In 2026 – https://www.ukfinance.org.uk/news-and-insight/press-release/modest-growth-forecast-mortgage-lending-in-2026

[6] Rate Shock Pushes Borrowers Towards Two-Year Fixes – https://www.mpamag.com/uk/mortgage-industry/market-trends/rate-shock-pushes-borrowers-towards-two-year-fixes/571067

[7] Macroeconomic Uncertainty And Spring 2026 Valuations How Building Surveyors Adjust For Interest Rate Volatility And Geopolitical Risk – https://nottinghillsurveyors.com/blog/macroeconomic-uncertainty-and-spring-2026-valuations-how-building-surveyors-adjust-for-interest-rate-volatility-and-geopolitical-risk