}

The UK office market has entered a new era of polarisation. While West End prime rents have shattered records at £182.50 per square foot—with standalone transactions reaching an extraordinary £240 per square foot—secondary stock languishes with high incentives and stagnant real returns. Prime Office Valuations in 2026: Chartered Surveyor Tactics for BREEAM Excellent Assets vs Secondary Decline represents the critical challenge facing RICS-qualified professionals today: accurately valuing assets in a market where sustainability credentials, location quality, and amenity provision have become the primary drivers of capital appreciation.

The divergence is stark. An impressive 68% of London take-up over the past year has concentrated in new or comprehensively refurbished buildings[3], signalling an irreversible flight to quality. Meanwhile, secondary assets face structural headwinds as occupiers consolidate into smaller footprints within superior buildings. For chartered surveyors conducting valuations in 2026, understanding this bifurcation—and deploying appropriate methodologies for each asset class—has become essential to delivering credible, defensible opinions of value.

Key Takeaways

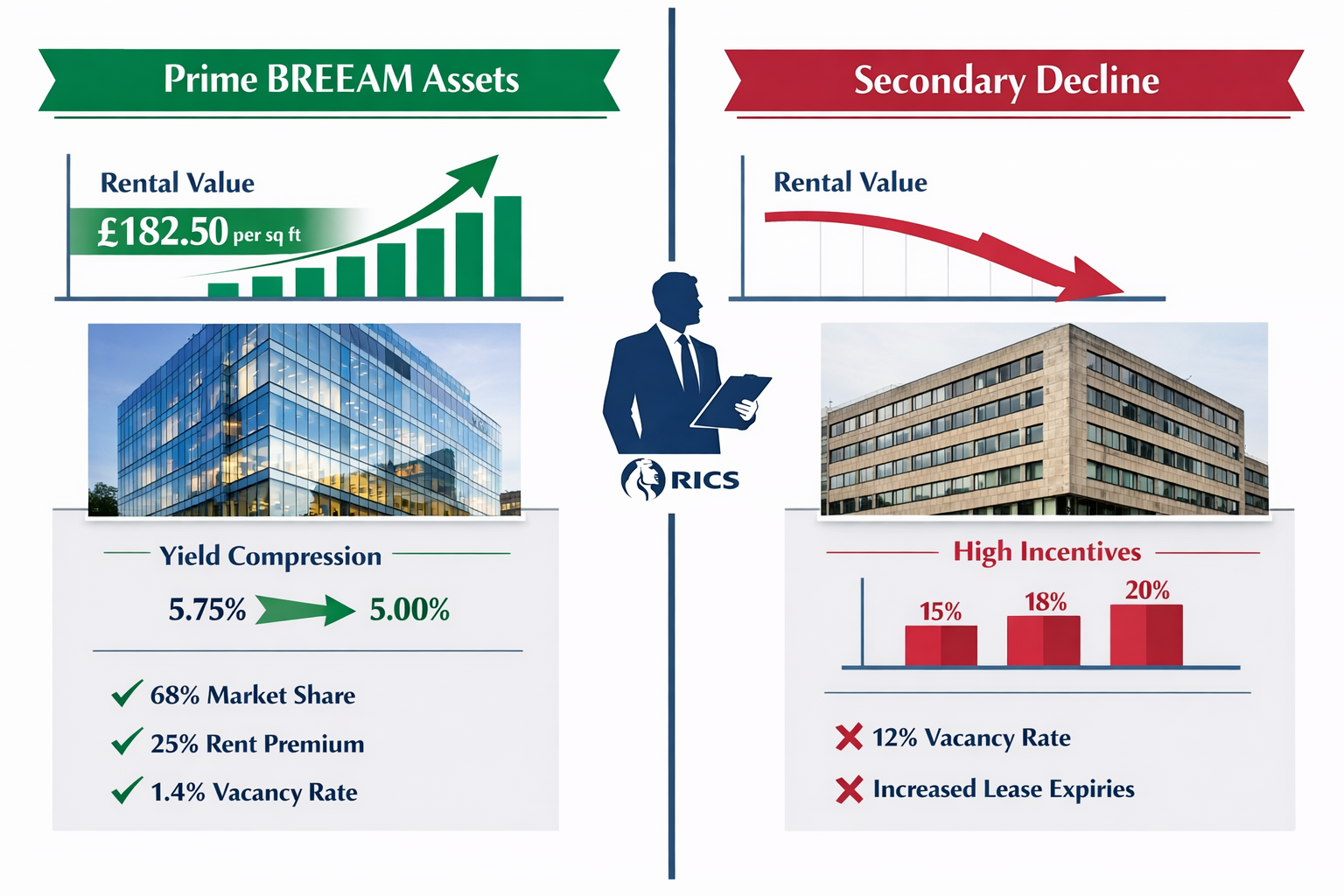

- BREEAM Excellent and Outstanding assets command 25% rental premiums over comparable non-certified stock, with prime yields compressing toward 5.00% as institutional capital targets ESG-compliant portfolios

- Secondary office valuations require substantial depreciation adjustments reflecting high incentive packages (15-20%), limited tenant demand, and capital expenditure requirements for ESG retrofitting

- Regional prime markets (Birmingham, Manchester, Leeds) show sustained rental growth with forecasts projecting 30% increases by 2030, creating valuation opportunities beyond London's established centres

- Chartered surveyors must integrate sustainability metrics including EPC ratings, embodied carbon, and BREEAM/WELL certifications into comparable analysis and income capitalisation models

- Structural undersupply of Grade A stock (10.8m sq ft deficit projected through 2028) supports aggressive rental growth assumptions for prime valuations while secondary assets face obsolescence risk

Understanding the Prime vs Secondary Divide in 2026 Office Valuations

The contemporary office market operates on a two-tier system that fundamentally reshapes valuation approaches. Prime assets—characterised by BREEAM Excellent or Outstanding ratings, EPC A or B certifications, comprehensive amenity packages, and central locations—have become scarcity assets. Secondary stock, typically older buildings with inferior environmental performance and limited flexibility for hybrid working, faces structural obsolescence.

Defining Prime in 2026: The BREEAM Benchmark

BREEAM (Building Research Establishment Environmental Assessment Method) certification has evolved from a "nice-to-have" differentiator to a fundamental determinant of asset classification. In 2026, prime office valuations increasingly hinge on:

- ✅ BREEAM Excellent or Outstanding certification (minimum 70% score)

- ✅ EPC rating of A or B with demonstrable pathway to net-zero carbon

- ✅ Smart building technology including occupancy sensors, air quality monitoring, and energy management systems

- ✅ Wellness credentials such as WELL Building Standard certification

- ✅ Amenity-rich environments featuring end-of-trip facilities, collaboration zones, and F&B offerings

A new 'super-prime' category has emerged in Mayfair, St. James's, and select City core locations, commanding £200+ per square foot. These assets combine heritage architecture with cutting-edge sustainability retrofits, attracting blue-chip occupiers willing to pay significant premiums for brand-enhancing headquarters[4].

Secondary Stock: Valuation Challenges and Depreciation

Secondary offices—typically built pre-2000 without modern environmental systems—face multiple valuation headwinds:

| Valuation Factor | Impact on Secondary Assets |

|---|---|

| Rental Growth | Flat to negative in real terms; high incentives (15-20% of headline rent) erode effective income |

| Yield Premium | 150-250 basis points above prime (7.5-8.5% vs 5.25-5.75%) reflecting higher risk |

| Capital Expenditure | £50-150 per sq ft required for ESG compliance, reducing net asset value |

| Obsolescence Risk | Stranding potential as occupiers vacate for prime alternatives |

| Comparable Evidence | Limited transaction activity creating valuation uncertainty |

Chartered surveyors valuing secondary stock must apply substantial depreciation adjustments to account for physical deterioration, functional obsolescence, and economic obsolescence. The RICS Red Book requires explicit disclosure of assumptions regarding refurbishment costs and achievable rents post-improvement.

"The flight to quality is not a temporary trend—it's a structural shift driven by corporate ESG commitments and employee expectations. Secondary assets without credible repositioning plans face terminal decline." — Leading UK Property Economist

Prime Office Valuations in 2026: Chartered Surveyor Tactics for BREEAM Excellent Assets

Valuing BREEAM Excellent assets requires chartered surveyors to integrate environmental performance metrics into traditional income capitalisation and comparable analysis methodologies. The approach differs substantially from conventional office valuations.

Income Capitalisation with Sustainability Premiums

The income approach for prime, BREEAM-certified offices incorporates:

1. Enhanced Rental Growth Assumptions

West End prime rents are forecast to grow 5-8% annually through 2029[1], while City core prime shows 3.9% projected growth[2]. These aggressive assumptions reflect:

- Constrained development pipelines (only 15.6m sq ft under construction across London)

- Structural undersupply of 10.8m sq ft over five years[1]

- Occupier willingness to pay premiums for sustainability credentials

2. Sustainability Rent Premiums

BREEAM Excellent assets command 25% premiums over non-certified comparables[4]. Surveyors must evidence these premiums through:

- Direct comparable analysis of certified vs non-certified lettings

- Tenant covenant strength (blue-chip occupiers concentrate in prime)

- Lease terms (longer weighted average lease expiry in prime assets)

3. Yield Compression Forecasts

Prime London yields have stabilised at approximately 5.75%, with forecasts suggesting compression of at least 75 basis points over five years[2][4]. Regional prime yields range from 5.25-6.75%, with similar compression anticipated as institutional capital pursues ESG-compliant assets.

Comparable Analysis for BREEAM Assets

Identifying truly comparable evidence presents challenges in a market where sustainability credentials vary widely. Chartered surveyors should:

- Stratify comparables by BREEAM rating (Excellent vs Very Good vs Pass)

- Adjust for EPC differentials (A-rated vs B-rated vs C-rated)

- Account for amenity provision (quantify value of gyms, terraces, F&B)

- Consider smart building technology (IoT sensors, occupancy analytics)

For capital gains tax valuations and SIPP pension valuations, precise comparable adjustment is critical to withstand HMRC scrutiny.

Regional Prime Markets: Emerging Opportunities

Beyond London, regional prime markets present compelling valuation scenarios. Big 6 regional office rents have risen 32% over five years, with forecasts projecting a further 30% growth by end of 2030[4]. Key markets include:

- Birmingham: Prime rents holding at £56 per sq ft, among highest outside Oxbridge, driven by Grade A shortage

- Manchester: Strong occupier demand for ESG-aligned space supporting rental momentum

- Leeds: Benefiting from corporate relocations seeking cost-efficient prime alternatives to London

- Cambridge & Oxford: Science and technology sector demand sustaining premium valuations

Chartered surveyors in Hertfordshire, Buckinghamshire, and Berkshire are increasingly valuing regional prime assets as institutional investors diversify beyond London.

DCF Modelling for Long-Term Prime Holdings

Discounted cash flow (DCF) analysis provides robust valuation support for institutional-grade prime assets. The methodology requires:

Explicit Period Projections (Years 1-10):

- Annual rental growth at 3.9-5.8% based on location and specification

- Lease expiry schedule with renewal probability assumptions

- Capex requirements for ongoing ESG compliance (typically £5-10 per sq ft annually)

- Void periods and re-letting costs at lease breaks

Terminal Value Calculation:

- Exit capitalisation rate reflecting anticipated yield compression

- Residual rental growth assumption (typically 2.5-3.0% in perpetuity)

Discount Rate Selection:

- Risk-free rate plus prime office risk premium (typically 6.5-7.5% for London prime)

- Adjustment for asset-specific factors (tenant quality, lease length, location)

Valuation Tactics for Secondary Office Assets in Decline

Secondary office valuations demand a fundamentally different approach, acknowledging the structural challenges facing older, environmentally underperforming stock.

Depreciation and Obsolescence Adjustments

Chartered surveyors must quantify three forms of depreciation:

Physical Deterioration:

- Building fabric condition (roof, façade, M&E systems)

- Deferred maintenance liabilities

- Remaining economic life assessment

Functional Obsolescence:

- Floor plate inefficiency (inability to accommodate modern workspace layouts)

- Inadequate floor-to-ceiling heights (typically <2.6m in older stock)

- Insufficient power and data infrastructure for technology-intensive occupiers

Economic Obsolescence:

- EPC rating below B (limiting lettability to ESG-conscious occupiers)

- Location disadvantage relative to emerging prime nodes

- Lack of amenity provision expected by contemporary occupiers

The cost approach becomes increasingly relevant for secondary assets, where income potential may not support existing use value. Surveyors should calculate:

Depreciated Replacement Cost = (Land Value + Current Construction Cost) – Accumulated Depreciation

Refurbishment Viability Analysis

For secondary assets with repositioning potential, surveyors must assess refurbishment viability:

| Refurbishment Component | Typical Cost (£ per sq ft) | Value Impact |

|---|---|---|

| EPC Upgrade to B Rating | £30-50 | Enables lettability to corporate occupiers |

| BREEAM Retrofit to Very Good | £40-70 | 10-15% rental premium potential |

| Amenity Enhancement | £20-40 | Improved tenant retention and rent growth |

| Smart Building Technology | £15-25 | Operational cost savings and occupier appeal |

| Total Comprehensive Refurb | £105-185 | Potential reclassification to prime/super-prime |

The residual valuation method determines maximum viable refurbishment expenditure:

Maximum Refurb Cost = (Post-Refurb GDV / Exit Yield) – Existing Value – Developer Profit

High Incentive Packages and Effective Rent

Secondary landlords typically offer incentive packages of 15-20% of headline rent to secure lettings, including:

- Rent-free periods (6-18 months)

- Fit-out contributions (£30-60 per sq ft)

- Break options (allowing early termination)

Chartered surveyors must calculate effective rent (ERV adjusted for incentives) rather than relying on headline figures:

Effective Rent = Headline Rent × (1 – Incentive Package %)

For example, a secondary office quoting £45 per sq ft headline with 18% incentives delivers effective rent of only £36.90 per sq ft—a critical distinction for income capitalisation valuations.

Yield Premiums and Risk Adjustment

Secondary assets trade at 150-250 basis points above prime yields[2][4], reflecting:

- Higher void risk (longer re-letting periods)

- Tenant covenant weakness (smaller, less-established occupiers)

- Capital expenditure uncertainty

- Obsolescence trajectory

Surveyors should evidence yield selection through:

- Recent secondary transaction comparables

- Investor return requirements for value-add strategies

- Risk-adjusted discount rates in DCF models

Chartered surveyors in North London, East London, and Essex frequently encounter secondary stock requiring careful yield calibration.

RICS Red Book Compliance and Reporting Standards

Regardless of asset quality, all valuations must comply with RICS Valuation – Global Standards (the "Red Book"). Key requirements include:

Basis of Value Selection

- Market Value: Most common for financial reporting, secured lending, and taxation

- Investment Value: For specific investor acquisition analysis

- Fair Value: IFRS-compliant basis for financial statements

Assumptions and Special Assumptions

BREEAM-related assumptions requiring explicit disclosure:

- Assumed continuation of environmental certification

- Assumed compliance with future ESG regulations (e.g., MEES minimum EPC B by 2030)

- Special assumption regarding completion of planned refurbishment works

Valuation Uncertainty

The Red Book mandates disclosure of material uncertainty where:

- Limited comparable evidence exists (common for super-prime and distressed secondary)

- Market conditions are rapidly changing

- Asset-specific factors create valuation complexity

Sustainability and ESG Reporting

RICS guidance increasingly requires:

- Explicit commentary on environmental performance (EPC, BREEAM, embodied carbon)

- Assessment of climate risk (physical and transition risks)

- Consideration of stranding risk for non-compliant assets

Professional surveyors should reference the Prince Chartered Surveyors approach to maintaining Red Book compliance while integrating sustainability metrics.

Regional Market Dynamics: Beyond London

While London dominates headlines, regional office markets present distinct valuation opportunities and challenges.

Birmingham: Grade A Scarcity

Birmingham's prime office market shows sustained rental pressure at £56 per sq ft[3], driven by acute shortage of ESG-aligned Grade A stock. Valuation considerations include:

- Limited development pipeline supporting rental growth assumptions

- Corporate relocations from London seeking cost-efficient prime space

- HS2 infrastructure investment enhancing connectivity and occupier appeal

Manchester: Northern Powerhouse Momentum

Manchester benefits from:

- Strong professional services and technology sector demand

- New prime developments commanding significant premiums

- Yield compression as institutional capital targets regional diversification

Cambridge & Oxford: Science and Technology Premiums

University cities command highest regional rents due to:

- Life sciences and technology sector concentration

- Severe planning constraints limiting supply

- Occupier willingness to pay premiums for talent attraction

Emerging Locations: Reading, Basingstoke, Milton Keynes

New prime developments in satellite locations demonstrate 25% premiums over previous peaks:

- Reading Station Hill at £56 per sq ft[4]

- Basingstoke PLANT at £38 per sq ft[4]

These examples evidence tenant appetite for sustainability credentials even in traditionally secondary locations.

Chartered surveyors in Oxfordshire, Hampshire, and Sussex should monitor these emerging prime nodes for comparable evidence.

Technology and Data in Modern Office Valuation

Contemporary office valuations increasingly leverage technology and data analytics:

PropTech Integration

- Automated valuation models (AVMs) providing initial value ranges

- Geospatial analysis assessing location quality and accessibility

- Energy performance databases benchmarking sustainability metrics

- Occupancy analytics from smart building sensors informing demand assumptions

ESG Data Platforms

Platforms providing:

- BREEAM and WELL certification databases

- EPC register analysis and benchmarking

- Carbon emissions tracking (operational and embodied)

- Climate risk assessment tools (flood, heat, transition risks)

Market Intelligence

Real-time data sources including:

- CoStar, EGi, and PropertyData for transaction comparables

- MSCI and IPD for yield and return benchmarks

- Occupier requirement databases tracking demand trends

Future-Proofing Valuations: 2026-2030 Outlook

Looking ahead, several trends will shape Prime Office Valuations in 2026: Chartered Surveyor Tactics for BREEAM Excellent Assets vs Secondary Decline:

Regulatory Tightening

- MEES regulations requiring minimum EPC B for commercial lettings by 2030

- Building Safety Act implications for older office stock

- Embodied carbon regulations potentially mandating whole-life carbon assessments

Yield Compression Continuation

Forecasts project 75+ basis point yield compression for prime assets through 2030[2][4], driven by:

- Institutional capital allocation to ESG-compliant real estate

- Pension fund demand for long-term income with inflation protection

- Limited development pipeline constraining supply

Secondary Stock Bifurcation

Secondary assets will diverge into:

- Repositionable stock with viable refurbishment economics

- Terminal decline assets facing conversion to alternative uses or demolition

Hybrid Working Stabilisation

Post-pandemic office utilisation has stabilised at 60-70% of pre-2020 levels, with implications:

- Continued demand for quality over quantity (smaller footprints in better buildings)

- Amenity provision becoming essential rather than optional

- Flexibility requirements (shorter leases, break options) affecting valuation assumptions

Conclusion

Prime Office Valuations in 2026: Chartered Surveyor Tactics for BREEAM Excellent Assets vs Secondary Decline encapsulates the fundamental challenge facing RICS professionals in today's polarised market. The divergence between prime, ESG-compliant assets commanding record rents and yield compression, and secondary stock facing structural obsolescence, demands sophisticated, differentiated valuation approaches.

Chartered surveyors must:

✅ Integrate sustainability metrics (BREEAM, EPC, embodied carbon) as primary value drivers rather than peripheral considerations

✅ Apply aggressive rental growth assumptions (3.9-8% annually) for prime assets supported by structural undersupply and occupier demand

✅ Quantify substantial depreciation for secondary stock reflecting physical deterioration, functional obsolescence, and economic obsolescence

✅ Evidence yield selection through stratified comparable analysis distinguishing prime, super-prime, and secondary transactions

✅ Assess refurbishment viability using residual valuation methodology to determine repositioning economics

✅ Maintain Red Book compliance while incorporating emerging ESG reporting requirements

The market outlook through 2030 strongly favours prime, BREEAM Excellent assets, with forecasts projecting 30% rental growth in regional markets[4] and continued yield compression of 75+ basis points[2]. Secondary assets without credible repositioning strategies face terminal decline as occupiers consolidate into superior buildings.

Actionable Next Steps

For Asset Owners:

- Commission BREEAM assessments to quantify certification potential

- Develop ESG improvement roadmaps with capital expenditure forecasts

- Engage chartered surveyors for refurbishment viability analysis

For Investors:

- Target prime, BREEAM Excellent assets in supply-constrained markets

- Underwrite aggressive rental growth for best-in-class stock

- Apply appropriate yield compression assumptions in DCF models

For Occupiers:

- Prioritise sustainability credentials in location decisions

- Anticipate continued rental growth for prime space

- Consider longer lease commitments in prime buildings to lock in relative value

For Chartered Surveyors:

- Enhance technical knowledge of BREEAM, WELL, and environmental standards

- Develop robust comparable databases stratified by sustainability credentials

- Integrate climate risk assessment into valuation reporting

The office market of 2026 rewards quality, sustainability, and location. Chartered surveyors who master the distinct tactics required for Prime Office Valuations in 2026: Chartered Surveyor Tactics for BREEAM Excellent Assets vs Secondary Decline will deliver the credible, defensible opinions of value that clients, lenders, and investors demand in this bifurcated market.

References

[1] London Office Pricing Forecast – https://adaptworkspace.com/news/london-office-pricing-forecast

[2] London Office Market – https://langhamestate.com/industry-community/london-office-market/

[3] The Cost Of Uk Office Space – https://www.oktra.co.uk/insights/the-cost-of-uk-office-space/

[4] The Shifting Landscape Of Uk Offices – https://www.jll.com/en-uk/insights/the-shifting-landscape-of-uk-offices