RICS January 2026 survey data revealed that 43% of respondents expected house prices to rise over the following twelve months — a figure that stands in sharp contrast to the negative sentiment dominating short-term readings. That gap between near-term weakness and medium-term optimism defines the central challenge facing chartered surveyors in 2026: how to produce accurate, defensible valuations when the market is simultaneously declining in some regions and recovering in others.

Valuing stabilising house prices in 2026: chartered surveyor adjustments for national recovery and regional divides is not simply a technical exercise. It requires surveyors to reconcile conflicting data signals, apply rigorous methodology, and communicate uncertainty clearly to clients, lenders, and courts. This article examines the current market landscape, the regional fault lines shaping valuations, and the specific tools surveyors are deploying to maintain accuracy.

Key Takeaways

- The RICS House Price Balance fell to -34% in April 2026, yet 12-month price expectations remain strongly positive at +33%, creating a complex dual-signal environment for valuers.

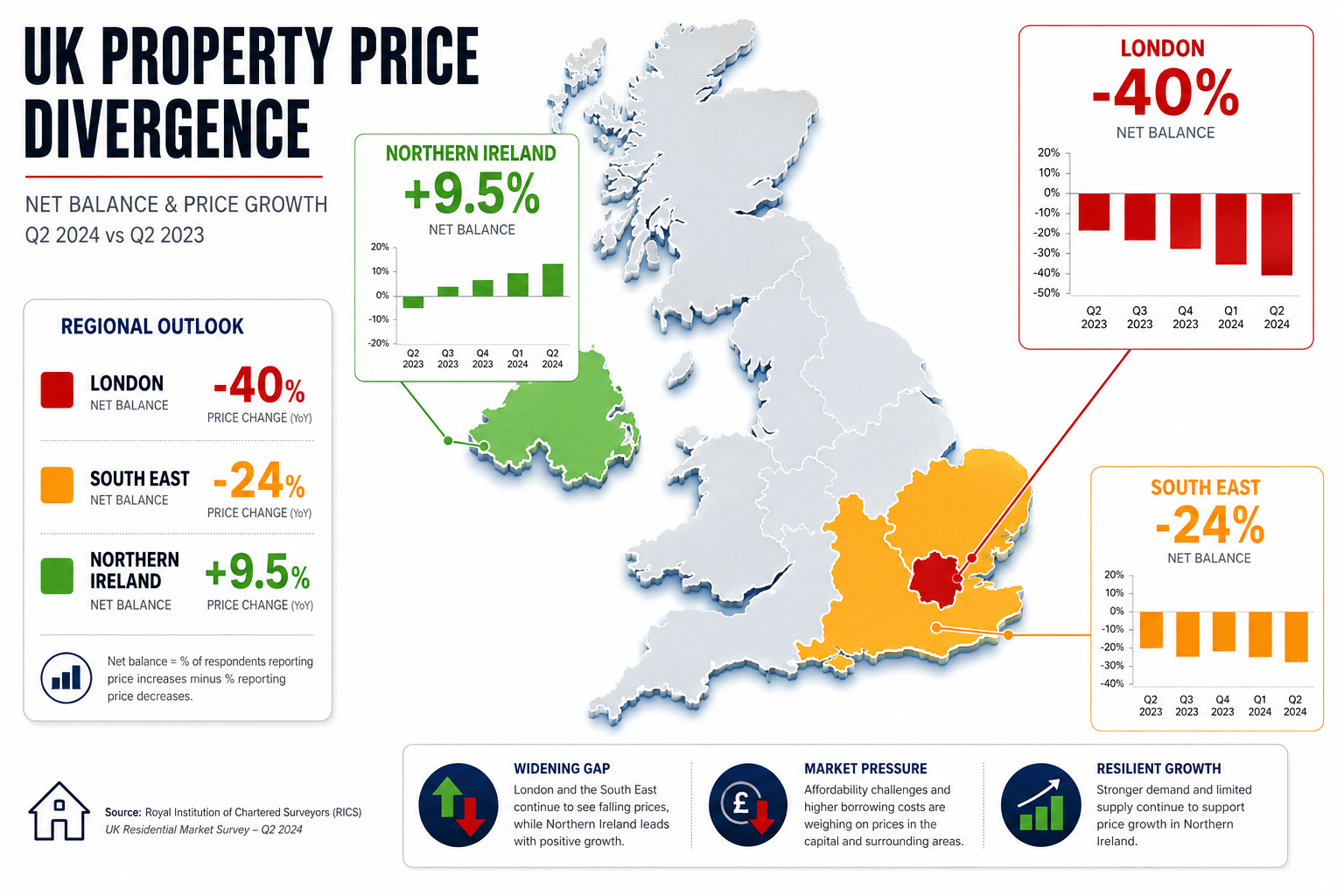

- London faces the sharpest downward pressure at -40% net balance, while Northern Ireland leads national growth at +9.5% annually, demanding region-specific valuation approaches.

- Surveyors are applying time adjustments of approximately 1.5-2% per month on London comparables to account for rapid monthly price declines.

- The updated RICS ESG standard, effective April 2026, now requires environmental and sustainability factors to be embedded in all formal appraisals.

- Automated valuation models require manual calibration in divergent markets; comparable evidence from the last three months is the current benchmark for accuracy.

Understanding the 2026 National Market Context

The headline numbers for 2026 tell a story of tension. The RICS House Price Balance dropped to -34% in April 2026, its weakest reading since November 2023, signalling that more surveyors are reporting falling prices than rising ones [1]. New buyer enquiries weakened further in February 2026, with a net balance sliding to -26%, down sharply from -15% in January [2]. These are not the conditions that suggest a straightforward recovery narrative.

Yet the same RICS data points in two directions at once. The 12-month price expectations balance sits at +33%, meaning a significant majority of market professionals anticipate prices will be higher a year from now [2]. Supply has not surged to destabilise the market either — new listings held a net balance of just +2% in February 2026, indicating broadly stable stock levels rather than a flood of distressed sellers [2].

What this means for surveyors: The market is not in freefall. It is in a period of recalibration, where short-term demand weakness and affordability constraints are suppressing transaction prices, while underlying supply constraints and medium-term demand expectations support a recovery thesis. Producing a valuation in this environment requires surveyors to weigh both signals carefully rather than defaulting to either pessimism or optimism.

Buyer Demand and Transaction Volumes

Reduced buyer enquiries are feeding through to lower agreed sales volumes, which in turn limits the pool of comparable evidence available to valuers. When transaction volumes fall, the risk of relying on stale or unrepresentative comparables rises. Surveyors working in lower-turnover markets must be especially vigilant about the age and relevance of the evidence they use. Understanding what factors are examined during a property valuation helps clients appreciate why this process demands more scrutiny in a subdued market.

Regional Divergences Driving Chartered Surveyor Adjustments

The national average conceals a market that is, in practice, several distinct markets operating under very different conditions. Valuing stabilising house prices in 2026 requires chartered surveyors to apply regionally calibrated adjustments rather than a single national framework.

London and the South East

London recorded a net balance of -40% in February 2026, the most severe downward price pressure of any UK region [2]. The South East and East Anglia followed with net balances of -24% and -26% respectively [2]. These figures reflect a combination of affordability constraints, higher mortgage sensitivity among London buyers, and a correction from the elevated price levels reached during the post-pandemic period.

For surveyors operating in these markets, the practical implication is significant. Canterbury Surveyors' analysis of RICS February 2026 data recommends that valuers prioritise comparables from the last three months in rapidly changing markets such as London, and apply a downward time adjustment of approximately 1.5-2% per month, based on the -1.9% monthly price decline recorded in the capital [4].

"In a market declining at nearly 2% per month, a comparable sale from six months ago could overstate current market value by 10-12% if no time adjustment is applied."

This is not a theoretical concern. Lenders relying on overvalued security face real financial risk, and surveyors who fail to apply appropriate adjustments expose themselves to professional negligence claims. For buyers navigating these conditions, understanding how to negotiate a house price after a survey can be a valuable tool when valuations come in below asking price.

Chartered surveyors in London can access specialist local expertise through Prince Chartered Surveyors' London team, which covers the full range of residential and commercial valuation services across the capital.

Northern England, Scotland, and Northern Ireland

At the opposite end of the spectrum, Northern Ireland led UK house price growth in 2026 with annual growth of +9.5% as of March 2026 [3]. Scotland also reported positive price trends, benefiting from relative affordability, strong local demand, and a different mortgage market profile compared to the South East [2].

For surveyors working in these markets, the challenge is different but equally demanding. Positive momentum can lead to optimistic comparable selection, and in a market where prices are rising, failing to apply upward time adjustments to older comparables will produce undervaluations. Lenders may be comfortable with conservative figures, but buyers and sellers both deserve accurate assessments.

| Region | RICS Net Balance (Feb 2026) | Annual Price Trend |

|---|---|---|

| London | -40% | Declining |

| South East | -24% | Declining |

| East Anglia | -26% | Declining |

| Northern Ireland | Positive | +9.5% annual growth |

| Scotland | Positive | Rising |

| National Average | Negative | Mixed |

Midlands and Northern England

The Midlands and Northern England occupy a middle ground, with conditions less extreme than London or Northern Ireland. These markets tend to show greater stability, which paradoxically can make valuation harder — there are fewer clear directional signals to guide adjustments. Surveyors in these regions benefit from using longer comparable windows (up to six months) while remaining alert to any acceleration in either direction.

Valuation Methodology: Chartered Surveyor Adjustments for National Recovery

Accurate appraisal in a divergent market demands a toolkit that goes beyond standard comparable analysis. The following approaches are central to how chartered surveyors are adapting their methodology in 2026.

Comparable Evidence Selection and Time Adjustments

The foundation of any residential valuation is comparable evidence — recent sales of similar properties in the same area. In a stable market, comparables from the past six to twelve months are generally reliable. In 2026, particularly in London and the South East, that window must be compressed.

RICS guidance and practitioner analysis both support using three-month comparables as the primary evidence base in rapidly moving markets [4]. Where only older comparables are available, time adjustments must be applied. In London, this means a downward adjustment of 1.5-2% per month for comparables older than three months [4]. In Northern Ireland, an upward adjustment reflecting the +9.5% annual growth rate would be appropriate — approximately 0.75-0.8% per month.

Key steps for comparable selection in 2026:

- Prioritise sales within the last three months wherever possible

- Document the basis for any time adjustment explicitly in the report

- Use at least three comparables; five or more is preferable in thin markets

- Weight comparables by similarity, recency, and transaction certainty (not just asking prices)

Automated Valuation Models: Calibration in a Divergent Market

Automated valuation models (AVMs) are widely used by lenders for initial screening, but their reliability degrades in markets with high regional divergence and low transaction volumes. AVMs trained on historical data from a more stable period will systematically overvalue London properties and potentially undervalue Northern Irish ones in 2026.

Chartered surveyors are increasingly asked to review or override AVM outputs, particularly for mortgage purposes. The correct approach is to treat the AVM figure as one data point rather than a conclusion, and to apply manual adjustments based on current comparable evidence and regional trend data. Where the AVM and the surveyor's assessment diverge by more than 5%, a full written explanation of the difference is considered best practice.

For clients who have received a valuation that differs from their expectations, the guide on what to do if your home valuation is less than an offer provides practical next steps.

Affordability Modelling and Stress Testing

Affordability constraints are a primary driver of the current demand weakness. Mortgage rates remain elevated relative to the pre-2022 baseline, and while some easing has occurred, the affordability ceiling for many buyers is materially lower than it was two years ago. Surveyors undertaking valuations for lending purposes are incorporating affordability stress tests into their analysis — assessing not just current market value but the sustainability of that value under different interest rate scenarios.

This is particularly relevant for insurance reinstatement cost valuations, where the rebuild cost must be assessed independently of market fluctuations, and for annual tax valuations where accurate current market values are required for compliance purposes.

The Updated RICS ESG Standard

A significant regulatory development shaping valuations in 2026 is the updated RICS ESG standard, which came into effect in April 2026. This standard mandates that valuers incorporate environmental, social, and governance factors into formal appraisals, with particular attention to sustainability-related expenditures [5].

In practice, this means surveyors must now assess:

- Energy Performance Certificate (EPC) ratings and the likely cost of upgrades to meet future regulatory requirements

- Flood risk and climate resilience as factors affecting long-term value

- Social factors such as proximity to amenities and community infrastructure

- Governance considerations for leasehold and shared ownership properties

Properties with poor EPC ratings face a growing value discount as buyers and lenders price in the cost of future retrofitting. Conversely, properties with strong sustainability credentials may command a premium that was not captured in pre-2026 valuation frameworks. Surveyors who fail to account for these factors risk producing reports that are non-compliant with current RICS standards.

Choosing the Right Survey Level

The complexity of the current market reinforces the importance of commissioning the right type of survey. Buyers uncertain about which level of inspection is appropriate can consult the complete guide to choosing between a Level 2 and Level 3 property survey, which sets out the key differences and when each is appropriate. In a market where price reductions after survey are increasingly common, understanding average price reductions following a survey helps buyers set realistic expectations.

Communicating Uncertainty and Market Conditions in Valuation Reports

One of the most important — and sometimes underused — tools available to surveyors is the market conditions caveat. RICS Red Book guidance permits and in some cases requires surveyors to include explicit statements about market uncertainty when conditions are exceptional. In 2026, with a -34% national price balance and significant regional divergence, the threshold for including such caveats is clearly met [1].

A well-drafted market conditions statement should:

- Describe the current state of the local market with reference to specific data (RICS surveys, Land Registry data, local agent intelligence)

- Explain the basis for comparable selection and any time adjustments applied

- Note the degree of uncertainty in the valuation and the range within which the true market value might fall

- State any assumptions about future market conditions that underpin the figure

This transparency protects the surveyor professionally and gives clients, lenders, and other users of the report the information they need to make informed decisions.

Conclusion

Valuing stabilising house prices in 2026: chartered surveyor adjustments for national recovery and regional divides demands a more sophisticated and regionally nuanced approach than has been required in more stable market periods. The combination of short-term price weakness nationally, extreme divergence between London and Northern Ireland, the introduction of mandatory ESG factors, and the limitations of automated valuation models in thin markets creates a genuinely complex professional environment.

Actionable next steps for property professionals and buyers in 2026:

- Instruct a qualified chartered surveyor with specific experience in your target region — national averages are misleading in a market this fragmented.

- Request transparency on comparable selection — ask your surveyor to explain which comparables were used, how old they are, and whether time adjustments were applied.

- Factor ESG costs into your offer price — properties with poor EPC ratings carry a real cost burden that should be reflected in negotiations.

- Treat AVM figures as a starting point, not a conclusion — particularly in London, where automated models are most likely to overstate current values.

- Monitor the 12-month expectations data — the +33% positive balance suggests recovery is anticipated; buyers who can transact now may benefit from entering before sentiment fully shifts.

For those seeking specialist valuation support across London and the South East, Prince Chartered Surveyors' locations page provides access to regional expertise across a wide range of property types and valuation purposes.

References

[1] Rics House Price Balance – https://tradingeconomics.com/united-kingdom/rics-house-price-balance?utm_source=openai

[2] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026?utm_source=openai

[3] Uk House Price Growth Region 2026 – https://usurv.ai/insights/uk-house-price-growth-region-2026/?utm_source=openai

[4] Valuation Adjustments In Regional Divergences Rics February 2026 Data For Surveyors In London Vs North – https://www.canterburysurveyors.com/blog/valuation-adjustments-in-regional-divergences-rics-february-2026-data-for-surveyors-in-london-vs-north/?utm_source=openai

[5] Valuation Adjustments For Stabilising Prices Rics Techniques For Accurate Appraisals In Early 2026 Recovery – https://kingstonsurveyors.com/valuation-adjustments-for-stabilising-prices-rics-techniques-for-accurate-appraisals-in-early-2026-recovery/?utm_source=openai

[6] Valuation Impacts Of Stabilising House Prices Rics Techniques From January 2026 Survey Data – https://princesurveyors.co.uk/blog/valuation-impacts-of-stabilising-house-prices-rics-techniques-from-january-2026-survey-data/?utm_source=openai