The UK property market has reached a critical turning point in 2026. After months of uncertainty and declining prices, recent data from the Royal Institution of Chartered Surveyors (RICS) reveals early signs of stabilisation that could reshape investment strategies for both first-time buyers and seasoned property investors. Valuing Properties in Stabilising 2026 Markets: RICS Insights for First-Time Buyers and Investors has become essential knowledge as the market transitions from decline to potential recovery, with house prices showing their strongest improvement since late 2025.

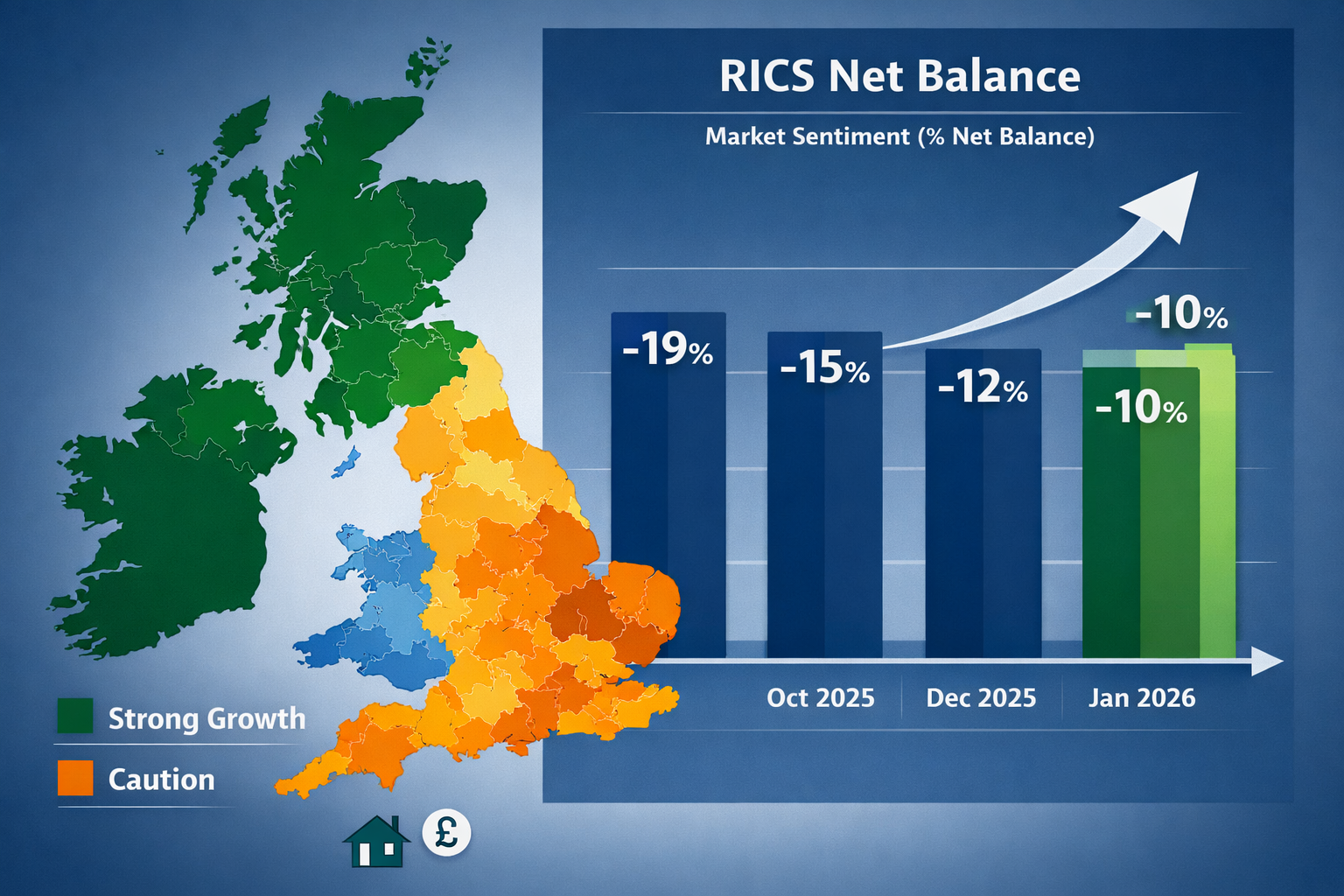

The net balance for house prices over the past three months improved dramatically to -10% in January 2026, up from -19% in October 2025[1]. This represents the most significant near-term development for property valuation, signaling a potential market turning point that savvy buyers and investors cannot afford to ignore. However, February data suggests renewed caution, making accurate valuation more critical than ever.

Key Takeaways

✅ House prices have stabilised nationally with the net balance improving from -19% (October 2025) to -10% (January 2026), though February showed renewed short-term caution at -18%[1][2]

✅ Long-term outlook remains positive with +33% of RICS respondents expecting price growth over twelve months, despite short-term volatility[2]

✅ Regional variations are significant with Scotland and Northern Ireland showing strongest growth while London expectations dropped dramatically from +56% to +7%[2]

✅ Rental market continues strengthening with +20% expecting rental price increases and 12% rental income growth forecast through 2026[2][3]

✅ Professional RICS valuations are essential as markets stabilise, with modern methodologies like Discounted Cash Flow becoming increasingly important[4]

Understanding the 2026 Property Market Stabilisation

The Journey from Decline to Recovery

The UK residential property market has experienced a remarkable transformation over recent months. The improvement in price sentiment from -19% in October 2025 to -10% in January 2026 represents the fastest recovery rate in recent years[1]. This stabilisation follows a prolonged period of uncertainty driven by interest rate concerns, affordability pressures, and economic headwinds.

However, Valuing Properties in Stabilising 2026 Markets: RICS Insights for First-Time Buyers and Investors requires understanding that recovery is not linear. February 2026 data showed headline price expectations dropping to -18% for the next three months, down from -6% in January[2]. This volatility underscores why professional valuation expertise has never been more critical.

Key Market Indicators Shaping Valuations

Several fundamental indicators are influencing property valuations in 2026:

Buyer Enquiries: After improving significantly in January with a net balance of -15% (up from -21% in December), buyer enquiries declined again to -26% in February[2]. This fluctuation reflects ongoing uncertainty about interest rate trajectories and economic conditions.

Agreed Sales: Transaction volumes remain subdued with February's net balance at -12%, slightly weaker than January's -9%[2]. This indicates that while sentiment is improving, actual market activity continues to lag.

Regional Disparities: The market is experiencing significant geographical variation. Scotland and Northern Ireland demonstrate the strongest price growth, with upward trends also reported in the North West and North of England. Meanwhile, London, the South East, South West, and East Anglia continue to lag[1].

"The stabilisation we're seeing in 2026 represents a pivotal moment for property valuation. Markets are no longer in freefall, but neither have they returned to robust growth. This requires a nuanced approach to valuation that balances current weakness with medium-term optimism." – RICS Market Analysis

Valuing Properties in Stabilising 2026 Markets: Regional Considerations

Geographic Variations Demand Tailored Approaches

One of the most critical aspects of Valuing Properties in Stabilising 2026 Markets: RICS Insights for First-Time Buyers and Investors is recognizing that the UK property market is not monolithic. Regional performance varies dramatically, requiring location-specific valuation adjustments.

Strong Performance Regions

Scotland and Northern Ireland continue to lead the recovery, with positive price momentum sustained through early 2026[1]. Properties in these regions may warrant less conservative valuation adjustments, particularly for longer-term investment horizons.

Northern England and North West are showing resilient performance, benefiting from relative affordability and steady local economic conditions. First-time buyers in these regions may find more favorable entry points with lower downside risk.

Cautionary Markets

London has experienced the most dramatic reassessment, with twelve-month price expectations plummeting from +56% in January to just +7% in February[2]. This represents a major valuation concern for the capital, driven by:

- Affordability constraints reaching critical levels

- Potential for further interest rate impacts

- Economic uncertainty affecting high-value markets

- Exodus of workers maintaining hybrid arrangements

The South East, South West, and East Anglia face similar pressures, though less extreme than London. Properties in these regions require particularly conservative near-term valuation assumptions while maintaining awareness of longer-term growth potential.

Valuation Adjustments by Region

| Region | Short-Term Outlook (3 months) | Medium-Term Outlook (12 months) | Valuation Approach |

|---|---|---|---|

| Scotland | Stable to Positive | Positive | Standard comparables with modest premium |

| Northern Ireland | Stable to Positive | Positive | Standard comparables with modest premium |

| North West England | Stable | Moderately Positive | Standard comparables |

| London | Cautious | Uncertain | Conservative adjustments, stress testing |

| South East | Cautious | Moderately Positive | Conservative near-term, balanced medium-term |

| South West | Cautious | Moderately Positive | Conservative near-term, balanced medium-term |

For comprehensive property valuations that account for regional variations, professional RICS chartered surveyors provide essential expertise.

RICS Valuation Methodologies for 2026 Markets

Moving Beyond Traditional Comparables

The stabilising market of 2026 demands more sophisticated valuation approaches. RICS has increasingly recommended adopting Discounted Cash Flow (DCF) methodology as a primary valuation method, moving beyond traditional backward-looking direct property comparables[4].

Why DCF Matters in Stabilising Markets

Traditional comparable sales methods rely heavily on recent transaction data. In rapidly changing markets, these comparables may not accurately reflect current or future value. DCF methodology offers several advantages:

🔍 Forward-Looking Analysis: Projects future cash flows rather than relying solely on historical data

📊 Risk Adjustment: Incorporates market uncertainty through discount rate adjustments

💰 Income Integration: Particularly valuable for buy-to-let properties where rental income is a key component

🎯 Scenario Planning: Allows testing multiple market outcome scenarios

The Three-Pillar Valuation Approach

Professional RICS valuations in 2026 should incorporate three complementary methodologies:

1. Comparable Sales Method (Adjusted)

Review recent sales of similar properties within the locality, but apply careful adjustments for:

- Time elapsed since sale (market conditions change rapidly)

- Property condition differences

- Location micro-variations

- Current market sentiment shifts

Understanding what factors are examined during property valuations helps buyers appreciate this complexity.

2. Income Capitalization Approach

Particularly relevant for investment properties, this method:

- Calculates net operating income

- Applies appropriate capitalization rates

- Adjusts for current rental market conditions

- Factors in the +20% expectation for rental price increases[2]

With rental income expected to climb 12% through 2026[3], this approach provides crucial insights for buy-to-let investors.

3. Cost Approach (Where Applicable)

For newer properties or unique situations:

- Estimates land value

- Adds current construction costs

- Subtracts depreciation

- Useful for properties with limited comparables

Professional Survey Requirements

Whether you're a first-time buyer or investor, obtaining a proper building survey is essential. The choice between different survey levels depends on property age, condition, and value. Many buyers benefit from understanding the differences in survey types and which they need.

For older properties or those with visible concerns, a Level 3 full building survey provides comprehensive analysis that can significantly impact final valuation.

Strategic Insights for First-Time Buyers in 2026

Timing Your Entry into a Stabilising Market

Valuing Properties in Stabilising 2026 Markets: RICS Insights for First-Time Buyers and Investors reveals a complex timing equation for first-time buyers. The data suggests 2026 presents both opportunities and risks:

Opportunity Factors:

- Prices have stabilised but not yet returned to strong growth

- Long-term expectations remain positive with +33% of respondents anticipating growth over twelve months[2]

- Five-year forecasts predict 22.2% average property value increase[3]

- Competition from buyers remains subdued with enquiries still in negative territory

Risk Factors:

- Short-term price expectations remain negative at -18% for the next three months[2]

- Interest rate uncertainty persists

- Economic conditions remain uncertain

- Regional variations mean some areas face greater downside risk

Valuation Strategies for First-Time Buyers

1. Obtain Independent Professional Valuations

Never rely solely on estate agent valuations or mortgage lender assessments. Getting an independent property valuation provides:

- Unbiased market assessment

- Identification of potential issues affecting value

- Negotiating leverage with sellers

- Confidence in your purchase decision

2. Build in Conservative Assumptions

Given the short-term caution in February data, first-time buyers should:

- Assume flat or modest price growth for the first 12-18 months

- Ensure affordability even if interest rates rise further

- Factor in potential maintenance costs revealed during surveys

- Avoid stretching budgets to maximum lending capacity

3. Focus on Fundamentals

In stabilising markets, properties with strong fundamentals outperform:

✅ Location: Proximity to transport, schools, amenities

✅ Condition: Well-maintained properties require less immediate capital

✅ Layout: Practical, adaptable spaces appeal to future buyers

✅ Energy Efficiency: Increasingly important for value and running costs

Understanding what questions to ask during building surveys helps identify these fundamental qualities.

4. Consider Regional Opportunities

First-time buyers with geographic flexibility should consider:

- Northern markets showing stronger resilience and affordability

- Scotland and Northern Ireland where price momentum remains positive

- Areas with strong rental demand if circumstances change

- Locations benefiting from improved transport links or regeneration

Millennial homebuyers are increasingly prioritizing these factors over traditional prestige locations.

Mortgage and Affordability Considerations

Valuation directly impacts mortgage availability. In 2026's stabilising market:

- Lenders remain cautious with loan-to-value ratios

- Professional valuations may come in below asking prices

- Larger deposits provide better rates and terms

- Fixed-rate products offer protection against further rate rises

Ensure any property valuation accounts for current lending criteria and conservative lender approaches.

Investment Property Valuation in the 2026 Market

The Buy-to-Let Opportunity

While first-time buyers face affordability challenges, Valuing Properties in Stabilising 2026 Markets: RICS Insights for First-Time Buyers and Investors reveals compelling opportunities for property investors in 2026.

The rental market fundamentals remain exceptionally strong:

📈 +20% of survey participants predict rental price increases over the next three months[2]

📉 Landlord instructions remain firmly negative at -27%, indicating continued supply constraints[2]

💷 Rental income expected to climb 12% through 2026, providing robust cash flow[3]

🏘️ 22.2% average property value increase forecast over five years, offering capital appreciation[3]

This combination of rental income growth and capital appreciation creates a dual-return investment profile that's particularly attractive in stabilising markets.

Valuation Approaches for Investment Properties

Investment property valuation requires additional considerations beyond residential owner-occupier properties:

Gross Rental Yield Analysis

Calculate the annual rental income as a percentage of property value:

Gross Rental Yield = (Annual Rental Income ÷ Property Value) × 100

In 2026, target yields vary by region:

- London: 3-5% (lower yields, higher capital growth potential)

- Regional cities: 5-7% (balanced yield and growth)

- Northern markets: 6-8%+ (higher yields, moderate growth)

Net Rental Yield Considerations

Account for all ownership costs:

- Mortgage interest

- Maintenance and repairs

- Insurance

- Management fees

- Void periods

- Regulatory compliance costs

With rental income rising 12% but property values also appreciating, net yields remain attractive despite higher interest rates.

Capital Growth Projections

The five-year forecast of 22.2% average property value increase[3] translates to approximately 4.1% annual compound growth. Combined with rental yields, total returns for buy-to-let investments could exceed 8-10% annually in well-selected properties.

Risk-Adjusted Valuation for Investors

Sophisticated investors in 2026 should apply risk-adjusted valuations:

Lower Risk (Premium Valuation):

- Properties in high-demand rental areas

- Good transport links and amenities

- Strong local employment markets

- Tenant demographics with stable income

- Properties requiring minimal maintenance

Higher Risk (Discounted Valuation):

- Areas with declining population or employment

- Properties requiring significant capital expenditure

- Locations with high void rates

- Regulatory challenges (e.g., leasehold issues)

- Properties in oversupplied rental markets

Professional commercial valuations expertise can be adapted for residential investment analysis.

Portfolio Diversification Strategies

Experienced investors are using 2026's stabilising market to rebalance portfolios:

🎯 Geographic Diversification: Spreading investments across regions with different growth profiles

🏘️ Property Type Mix: Combining houses, flats, and HMOs to balance yield and growth

💼 Tenant Demographic Spread: Mix of young professionals, families, and students reduces concentration risk

📊 Development Stage Variety: Combining established properties with development opportunities

Professional Valuation Services: When and Why to Use Them

The Value of Professional RICS Valuations

In stabilising 2026 markets, professional valuations provide critical advantages over informal estimates or automated valuation models (AVMs):

Accuracy in Volatile Markets

AVMs rely on historical data and algorithms that struggle in transitioning markets. Professional RICS surveyors:

- Apply current market knowledge and sentiment

- Adjust for recent market shifts not yet reflected in data

- Identify property-specific factors affecting value

- Provide defensible valuations for lending and legal purposes

Comprehensive Property Assessment

Professional valuations combine market analysis with physical inspection:

- Structural condition assessment

- Identification of defects affecting value

- Building regulation and planning compliance

- Energy efficiency and environmental factors

- Comparable properties with appropriate adjustments

Understanding building pathology helps surveyors identify issues that significantly impact value.

Regulatory Compliance

For certain transactions, professional RICS valuations are mandatory or highly advisable:

- Inheritance tax valuations

- SIPP pension valuations

- Right to buy valuations

- Matrimonial settlements

- Probate and estate administration

When to Commission Professional Valuations

For First-Time Buyers

Professional valuations are recommended when:

✅ Purchasing older properties (pre-1900) with potential hidden defects

✅ Buying properties significantly above or below market average

✅ Negotiating price reductions based on survey findings

✅ Purchasing in rapidly changing local markets

✅ Seeking mortgage lending at high loan-to-value ratios

For Property Investors

Investors should obtain professional valuations:

✅ Before purchasing investment properties to confirm yield calculations

✅ When refinancing to release equity for further investments

✅ For portfolio revaluations to assess performance

✅ When considering property development or significant renovations

✅ For tax planning and compliance purposes

Choosing the Right Surveyor

Not all surveyors offer the same expertise. When selecting a professional for Valuing Properties in Stabilising 2026 Markets: RICS Insights for First-Time Buyers and Investors, consider:

🎓 RICS Accreditation: Ensures professional standards and indemnity insurance

📍 Local Market Knowledge: Familiarity with regional trends and comparable properties

🏗️ Relevant Specialization: Experience with your property type (period properties, new builds, commercial conversions)

📊 Valuation Methodology: Understanding of modern approaches including DCF analysis

💬 Communication: Clear reporting and willingness to explain findings

For properties requiring detailed analysis, explore exclusive properties with comprehensive survey services.

Practical Valuation Checklist for 2026

Pre-Purchase Due Diligence

Before committing to any property purchase in 2026's stabilising market, complete this comprehensive checklist:

Market Research Phase

- Review RICS monthly market surveys for latest sentiment data

- Research specific local area price trends over past 12-24 months

- Identify comparable sales within past 6 months (adjust for market changes)

- Assess local rental market if considering investment potential

- Evaluate regional economic indicators and employment trends

Property-Specific Analysis

- Commission appropriate survey level (Level 2 or Level 3)

- Obtain professional RICS valuation independent of lender

- Review Energy Performance Certificate and improvement costs

- Check planning history and any restrictions

- Investigate local development plans affecting future value

- Assess transport links and infrastructure improvements

Financial Modeling

- Calculate maximum affordable purchase price (conservative assumptions)

- Model multiple interest rate scenarios (current, +1%, +2%)

- Factor in all transaction costs (stamp duty, surveys, legal fees)

- Budget for immediate repairs/improvements identified in survey

- For investors: model rental yields under various occupancy scenarios

- For investors: calculate break-even points and cash flow projections

Risk Assessment

- Identify property-specific risks (structural, legal, environmental)

- Assess market-timing risks given current stabilisation phase

- Evaluate personal circumstances (job security, family changes)

- Consider exit strategy and potential resale timeline

- Review insurance requirements and costs

Negotiation Strategy Based on Valuation

Professional valuations provide powerful negotiation leverage:

If valuation comes in below asking price:

- Present professional valuation report to seller

- Request price reduction to valuation level

- Negotiate seller contribution to identified repairs

- Consider walking away if seller unwilling to negotiate

If valuation confirms asking price:

- Proceed with confidence in fair market value

- Focus negotiations on other terms (completion date, inclusions)

- Build contingency for short-term market volatility

If valuation exceeds asking price:

- Rare in 2026's cautious market but possible in high-demand areas

- Proceed quickly to secure property

- Ensure financing is secure before exchange

- Consider whether asking price reflects true market or if valuation is optimistic

Future-Proofing Your Property Investment

Long-Term Value Considerations

The five-year forecast of 22.2% average property value increase[3] makes 2026 an attractive entry point for long-term investors. However, future-proofing requires attention to emerging value drivers:

Energy Efficiency and Sustainability

Properties with poor energy performance face increasing valuation penalties:

- EPC ratings below C may face rental restrictions

- Energy costs significantly impact affordability

- Retrofit costs can be substantial (£10,000-£50,000+)

- Green mortgages offer preferential rates for efficient properties

Consider EPC requirements and building surveys when evaluating properties.

Adaptability and Future Use

Properties that accommodate changing lifestyles maintain value better:

- Home office space (hybrid working continues)

- Flexible room configurations

- Outdoor space (gardens, balconies, terraces)

- Good natural light and ventilation

- Adequate storage

Technology and Connectivity

Modern buyers and tenants expect:

- High-speed broadband infrastructure

- Electric vehicle charging capability

- Smart home compatibility

- Adequate electrical capacity for modern appliances

Community and Amenities

Long-term value increasingly depends on:

- Walkable neighborhoods with local services

- Green spaces and recreational facilities

- Good schools (even for non-families, affects resale)

- Cultural and social amenities

- Community cohesion and safety

Monitoring Your Investment

After purchase, regular valuation monitoring helps optimize returns:

Annual Reviews:

- Track local market trends against national data

- Monitor RICS surveys for sentiment shifts

- Review rental market if investment property

- Assess property condition and maintenance needs

Trigger Point Revaluations:

- Significant local market movements (±10%)

- Completion of major renovations or improvements

- Changes in local infrastructure or amenities

- Refinancing or equity release opportunities

- Tax planning or estate administration needs

Conclusion: Navigating Property Valuation in 2026's Stabilising Market

Valuing Properties in Stabilising 2026 Markets: RICS Insights for First-Time Buyers and Investors requires a sophisticated understanding of both current market dynamics and longer-term trends. The data presents a nuanced picture: short-term caution is warranted with February's renewed price pessimism, yet medium and long-term fundamentals remain encouraging with positive twelve-month expectations and strong five-year growth forecasts.

Key Strategic Recommendations

For First-Time Buyers:

🏠 Act with informed confidence – The stabilisation phase offers opportunities for those who conduct thorough due diligence

📊 Invest in professional valuations – Independent RICS assessments provide negotiating power and purchase confidence

🎯 Focus on fundamentals – Location, condition, and adaptability matter more than timing the market perfectly

💷 Maintain financial prudence – Conservative affordability assumptions protect against continued uncertainty

For Property Investors:

📈 Capitalize on rental market strength – With 12% rental income growth forecast and supply constraints, buy-to-let fundamentals are robust

🗺️ Embrace regional diversification – Geographic spread reduces risk from localized market weakness

🔍 Apply rigorous valuation methodology – DCF analysis and comprehensive yield calculations ensure sound investment decisions

⏰ Take a long-term perspective – Five-year growth forecasts of 22.2% reward patient capital

Immediate Action Steps

-

Review current RICS monthly surveys to understand the latest market sentiment in your target area

-

Engage RICS chartered surveyors for professional valuations on any properties under serious consideration

-

Conduct comprehensive financial modeling with conservative assumptions for interest rates and price movements

-

Assess regional opportunities beyond traditional high-value areas where stabilisation is more advanced

-

Build a professional advisory team including surveyors, mortgage brokers, and solicitors with 2026 market expertise

-

Monitor market indicators monthly to identify when stabilisation transitions to growth in your target areas

The 2026 property market represents a pivotal moment. Those who approach property valuation with professional rigor, regional awareness, and balanced optimism will position themselves to benefit from the recovery ahead. Whether you're a first-time buyer seeking your first home or an investor building a portfolio, the insights from RICS data provide a roadmap for navigating these stabilising markets with confidence.

The key is not to wait for perfect market conditions—which rarely materialize—but to make informed decisions based on professional valuations, sound fundamentals, and realistic expectations. The stabilisation we're witnessing in 2026 may well be remembered as the optimal entry point for a new generation of property owners and investors.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Buy To Let Valuation Surge 2026 Survey Strategies For Institutional Investors In A Recovering Market – https://nottinghillsurveyors.com/blog/buy-to-let-valuation-surge-2026-survey-strategies-for-institutional-investors-in-a-recovering-market

[4] Independent Review Of Real Estate Investment Valuations By Rics – https://www.altusgroup.com/insights/independent-review-of-real-estate-investment-valuations-by-rics/