The UK buy-to-let market is experiencing a dramatic transformation in 2026. While smaller landlords exit under mounting tax pressures, institutional investors are driving a remarkable resurgence—reshaping how properties are valued, surveyed, and financed. Valuing buy-to-let properties in 2026: surveyor strategies amid institutional landlord surge and tax pressures requires a sophisticated understanding of evolving valuation methodologies, regulatory compliance, and market dynamics that differ significantly from traditional residential assessments.

For chartered surveyors and property professionals, this shift presents both challenges and opportunities. New taxation thresholds affecting properties over £2 million, conservative rental income assessments, and the rise of Houses in Multiple Occupation (HMOs) demand specialized valuation approaches aligned with RICS standards. Understanding these strategies is essential for accurate appraisals in today's complex investment landscape.

Key Takeaways

- Four-tier valuation approach: Lenders now employ Desktop/AVM, drive-by, full internal, and commercial-style valuations depending on property type and risk profile[1]

- Tax threshold impact: 83% of offers on properties near £2 million now come in below this threshold to avoid higher taxation—a 19-point increase from 2025[2]

- Institutional dominance: Professional landlords and institutional investors are driving market resurgence while smaller landlords consolidate portfolios due to tax pressures[3]

- HMO valuation complexity: Properties with 6+ tenants require commercial-basis valuations driven by rental income rather than traditional property structure assessments[1]

- Regional strategy shift: Investment focus is moving northward to Manchester and Liverpool as southern markets reach affordability ceilings[3]

The 2026 Buy-to-Let Market Landscape

Institutional Landlords Reshape the Sector

The UK buy-to-let market is witnessing what industry experts describe as a "remarkable resurgence" driven primarily by institutional landlords and professional investors[4]. This represents a fundamental shift from the individual small landlord model that dominated for decades.

The private rented sector now comprises 4.7 million people, representing 19% of all English households[5]. While this figure has remained stable for over a decade, the composition of landlords has changed dramatically. Steeper tax bills and regulatory burdens are forcing smaller landlords to exit, shrinking rental supply and subsequently increasing rents for tenants[3].

Professional property management companies bring several advantages:

✅ Economies of scale in maintenance and compliance

✅ Access to institutional financing with favorable terms

✅ Professional survey and valuation protocols

✅ Long-term portfolio strategies rather than individual property focus

✅ Sophisticated risk management across diversified holdings

This professionalization affects how surveyors approach valuations. Institutional clients demand comprehensive building survey protocols that assess not just current value but long-term investment viability, regulatory compliance, and portfolio optimization potential.

Tax Pressures Driving Market Consolidation

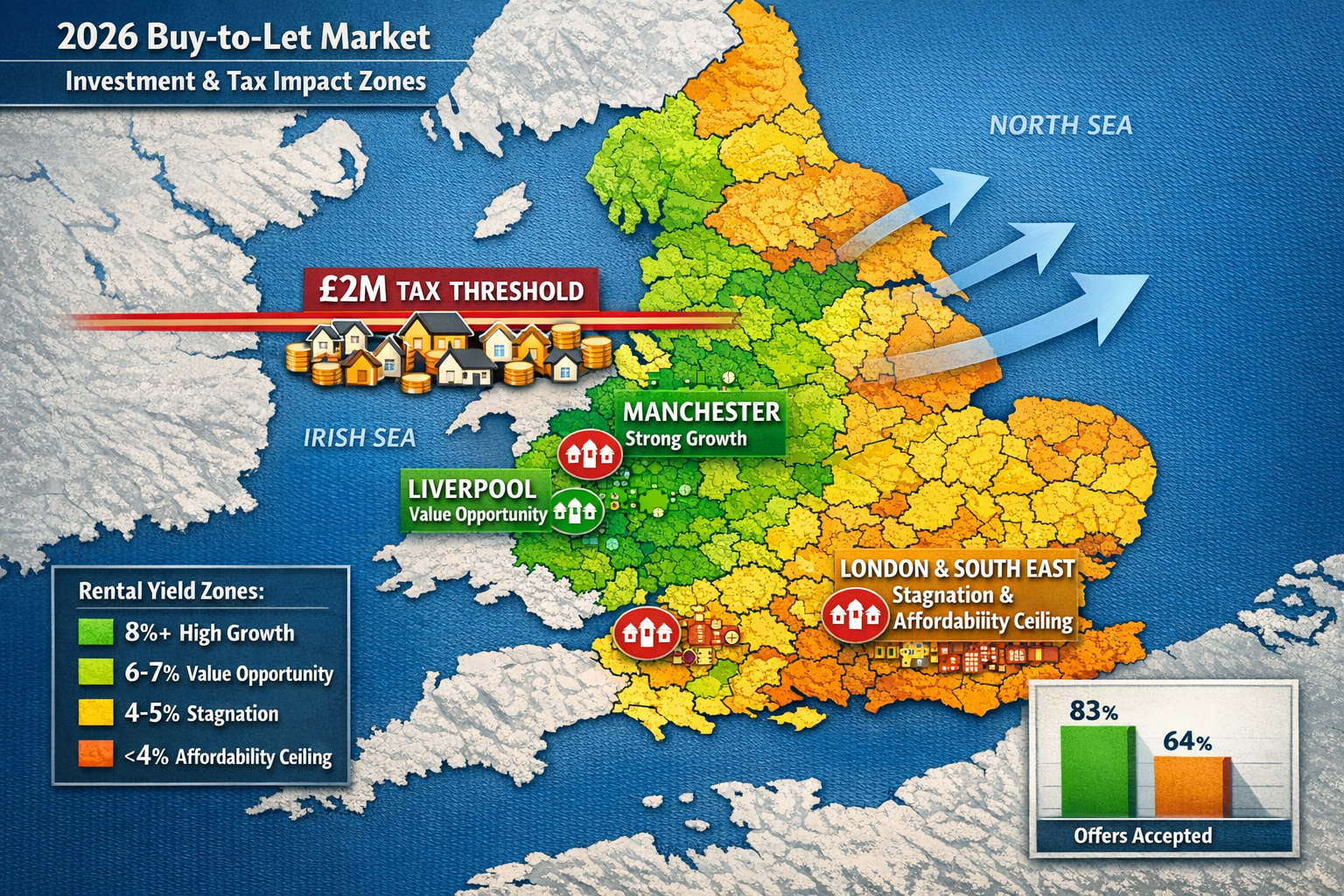

Tax policy changes are fundamentally altering buy-to-let investment calculations. The most significant development is new taxation on properties valued over £2 million, which is dramatically affecting high-value transactions.

Data from February 2026 reveals that 83% of offers on homes priced within 10% of £2 million came in below the threshold, compared to just 64% a year earlier—a significant 19 percentage point increase[2]. This behavioral shift demonstrates how taxation directly influences valuation negotiations and market pricing.

For surveyors, this creates a challenging dynamic:

- Downward valuation pressure near tax thresholds

- Increased scrutiny of comparable property analysis

- Conservative rental income projections to justify lower valuations

- Strategic timing of valuations relative to purchase negotiations

These pressures require surveyors to maintain strict RICS compliance while navigating client expectations and market realities. Understanding capital gains tax implications becomes essential for comprehensive valuation advice.

Demographic Shifts and Property Demand

Underlying market fundamentals continue to support buy-to-let investment despite tax headwinds. Single-person households have risen significantly to 33% of all households as of 2026, up from approximately 28% six years earlier[5]. This creates strong, sustained demand for one-bedroom properties and smaller units.

National property price growth is predicted at 4-5% for 2026, with average prices approaching the £300,000 mark[3]. This momentum builds on slower gains in preceding years and reflects pent-up demand meeting constrained supply.

Surveyor Strategies for Valuing Buy-to-Let Properties in 2026

Four-Tier Valuation Methodology Framework

Lenders employ four primary valuation approaches depending on risk level, property type, and loan-to-value ratios[1]. Understanding when each methodology applies is crucial for surveyors working in the buy-to-let sector.

| Valuation Type | Property Characteristics | Inspection Level | Typical Use Cases |

|---|---|---|---|

| Desktop/AVM | Standard properties, low LTV, established areas | None (data analysis only) | Remortgages, low-risk refinancing |

| Drive-By External | Mainstream properties, moderate LTV | External inspection only | Standard buy-to-let purchases |

| Full Internal Assessment | Higher value, unique features, higher LTV | Complete internal and external | New purchases, portfolio additions |

| Commercial-Style | Large HMOs, semi-commercial, 6+ tenants | Comprehensive income-based | Multi-unit investments, professional portfolios |

For most buy-to-let transactions, surveyors conduct either drive-by external inspections or full internal assessments. The selection depends on lender requirements, property characteristics, and perceived risk factors.

Desktop and AVM approaches utilize automated valuation models that analyze comparable sales data, local market trends, and property characteristics without physical inspection. While cost-effective, these methods lack the nuanced assessment that physical inspection provides—particularly important for identifying areas requiring further investigation.

Full internal assessments remain the gold standard for accurate buy-to-let valuations. These comprehensive inspections allow surveyors to identify structural issues, assess maintenance requirements, evaluate tenant appeal, and provide informed rental income projections. For investors, commissioning a thorough Level 3 full building survey before purchase provides critical due diligence beyond lender requirements.

Rental Income Assessment Protocols

Rental income assessment is more conservative in 2026, with valuers conducting comparable analysis of local properties and reviewing tenancy agreements closely[1]. Landlords should expect valuers to apply cautious assumptions, potentially reducing assessed rents below declared figures.

RICS-aligned rental assessment includes:

🔍 Comparable rental analysis: Reviewing similar properties within 0.5-mile radius

🔍 Tenancy agreement review: Verifying current rents and lease terms

🔍 Market trend analysis: Assessing rental growth or decline trajectories

🔍 Void period assumptions: Factoring realistic vacancy rates

🔍 Tenant quality assessment: Evaluating sustainability of current rental levels

Surveyors must distinguish between optimistic landlord projections and sustainable market rents. In areas experiencing rental growth, conservative assumptions protect lenders from overvaluation risk while potentially underestimating long-term investment returns.

For properties in locations like Putney, Hammersmith, or Clapham, local market knowledge becomes invaluable. Understanding micro-market dynamics, transport links, and neighborhood desirability directly influences rental income projections.

HMO Valuation Complexity and Size-Based Protocols

Houses in Multiple Occupation now offer the strongest rental yields of any property type[5]. Typically three bedrooms or more, HMOs with multiple tenants on separate agreements and inclusive billing generate strong, consistent income streams—though they require more stringent regulatory compliance and complex financing.

HMO valuations now follow size-based protocols[1]:

Properties with up to 6 tenants: Valued as standard houses with rent assessed per room. Surveyors calculate total rental income from individual room rates, apply appropriate yield calculations, and compare against similar HMO properties. The physical structure remains important, but income generation drives valuation.

Larger HMOs (6+ tenants): Use commercial-basis valuations driven entirely by rental income rather than property structure. These assessments resemble commercial valuations, focusing on:

- Net operating income (NOI) calculations

- Capitalization rates specific to HMO investments

- Regulatory compliance costs and licensing requirements

- Management intensity and operational expenses

- Tenant turnover and void period assumptions

The complexity of HMO valuations requires specialized expertise. Surveyors must understand licensing requirements, fire safety regulations, minimum room sizes, and amenity provisions. Failure to account for compliance costs can significantly overstate property value and investment returns.

Regional Investment Strategies and Valuation Adjustments for 2026

Geographic Valuation Variations

Regional investment strategy is shifting northward as investors diversify away from saturated southern markets[3]. This geographic rebalancing creates distinct valuation dynamics across UK regions.

Manchester is leading regional growth, offering strong rental yields combined with capital appreciation potential. The city's diverse economy, major regeneration projects, and expanding transport infrastructure support sustained property demand. Surveyors working in Manchester must account for rapid neighborhood transformation and emerging investment hotspots.

Liverpool offers strong property value relative to rental income, creating attractive entry points for portfolio expansion. Lower purchase prices combined with solid rental demand produce yields that significantly exceed southern markets. However, surveyors must carefully assess neighborhood quality, tenant demographics, and long-term sustainability.

London and the South East are forecast to see stable but flat growth, with prices reaching affordability ceilings for traditional buyers[3]. Prime markets experience stagnation due to tax impacts, though foreign capital continues to provide support. For surveyors, this requires:

- Conservative appreciation assumptions in valuation models

- Emphasis on rental yield over capital growth

- Careful assessment of properties near the £2 million threshold

- Recognition of micro-market variations within broader regions

Properties in areas like St Albans, Hemel Hempstead, and Buckinghamshire demonstrate how commuter belt locations maintain value through accessibility while avoiding central London price premiums.

Navigating the £2 Million Tax Threshold

The £2 million taxation threshold creates unique valuation challenges requiring strategic approaches. Surveyors must balance professional integrity with market realities when properties fall near this critical price point.

Strategic valuation considerations include:

💡 Comparable selection bias: Properties just below £2 million may dominate recent sales data, creating downward pressure on valuations

💡 Negotiation leverage: Buyers increasingly use the threshold as justification for lower offers, regardless of true market value

💡 Timing sensitivity: Valuation dates relative to tax year boundaries affect strategic positioning

💡 Component separation: Potential to separate land value, chattels, or development potential from core property value

Surveyors must maintain RICS ethical standards while acknowledging these market dynamics. Transparent documentation of valuation methodology, comparable selection criteria, and adjustment rationale protects professional integrity while serving client interests.

For properties genuinely valued near £2 million, consider commissioning multiple valuation approaches to establish a defensible range. This might include both traditional comparable sales analysis and income capitalization methods, providing different perspectives on market value.

Institutional Portfolio Valuation Requirements

Institutional landlords demand valuation services that extend beyond individual property assessments. Portfolio-level analysis, risk diversification metrics, and strategic acquisition planning require sophisticated surveyor capabilities.

Institutional valuation protocols typically include:

📊 Portfolio composition analysis: Assessing geographic diversification, property type mix, and tenant demographic spread

📊 Regulatory compliance audits: Ensuring all properties meet licensing, safety, and energy efficiency standards

📊 Capital expenditure planning: Identifying maintenance requirements across multiple properties

📊 Yield optimization strategies: Recommending property disposals, acquisitions, or repositioning

📊 Risk-adjusted return calculations: Comparing portfolio performance against investment alternatives

These comprehensive services position surveyors as strategic advisors rather than transactional service providers. Understanding statutory considerations and environmental issues becomes essential for institutional-grade assessments.

RICS-Aligned Techniques for Accurate Buy-to-Let Appraisals

Comparable Sales Analysis Refinement

Traditional comparable sales analysis requires refinement for buy-to-let properties in 2026's complex market. Surveyors must apply sophisticated adjustment methodologies that account for investment-specific factors beyond standard residential considerations.

Enhanced comparable selection criteria:

- Investment purpose: Prioritize sales to investors over owner-occupiers

- Rental income verification: Confirm actual achieved rents, not asking prices

- Tenure considerations: Leasehold properties require ground rent and service charge adjustments

- Tenant status: Properties sold with sitting tenants may trade at discounts

- Recent transactions: Emphasize sales within 3-6 months given rapid market evolution

Adjustment factors specific to buy-to-let:

- Rental yield differential: Properties achieving above-market rents justify premium valuations

- Tenant quality: Long-term professional tenants reduce void risk and support higher values

- Condition and maintenance: Deferred maintenance requires significant value adjustments

- Regulatory compliance: Properties requiring licensing, fire safety upgrades, or EPC improvements need downward adjustments

- Management intensity: HMOs and multi-unit properties carry operational complexity costs

Surveyors should document all adjustments with clear rationale, supporting data, and sensitivity analysis. This transparency builds lender confidence and provides defensible valuation conclusions.

Income Capitalization Methodology

For larger HMOs and commercial-style buy-to-let properties, income capitalization methodology provides the most appropriate valuation approach. This technique values properties based on income-generating capacity rather than physical characteristics.

Core income capitalization formula:

Property Value = Net Operating Income ÷ Capitalization Rate

Net Operating Income (NOI) calculation:

- Gross potential rental income (all rooms at market rates)

- Less: Void allowance (typically 5-10% for HMOs)

- Less: Operating expenses (maintenance, management, utilities, insurance, licensing)

- Equals: Net Operating Income

Capitalization rate determination requires careful market analysis. Rates vary by:

- Property location: Prime areas command lower cap rates (higher values)

- Property condition: Well-maintained properties justify lower cap rates

- Tenant profile: Professional tenants reduce risk, lowering cap rates

- Management requirements: Higher management intensity increases cap rates

- Market conditions: Competitive investment markets compress cap rates

For 2026, typical HMO capitalization rates range from 5-8% depending on these factors. Surveyors must research recent investment property sales to establish appropriate rates for specific locations and property types.

Risk Assessment and Adjustment Factors

Comprehensive buy-to-let valuations incorporate risk-adjusted analysis that accounts for factors affecting investment performance and value sustainability.

Key risk categories:

🔴 Regulatory risk: Changes to licensing, safety standards, or tenant rights legislation

🔴 Market risk: Rental demand fluctuations, oversupply, or economic downturns

🔴 Property-specific risk: Structural issues, building pathology, or deferred maintenance

🔴 Tenant risk: Void periods, rent arrears, or property damage

🔴 Financial risk: Interest rate changes, refinancing challenges, or tax policy shifts

Surveyors should assign risk ratings (low, moderate, high) to each category and adjust valuations accordingly. High-risk properties may warrant 10-20% value reductions compared to low-risk equivalents, even with similar physical characteristics and current rental income.

For properties requiring significant work, understanding the consequences of failing to act on identified defects helps quantify risk-adjusted valuations.

Technology Integration in Valuation Practice

Modern surveying practice increasingly incorporates technology tools that enhance accuracy, efficiency, and client communication. For buy-to-let valuations in 2026, several technologies prove particularly valuable:

Automated Valuation Models (AVMs): While not replacing professional judgment, AVMs provide useful initial estimates and comparable property identification. Surveyors can use AVM outputs as starting points, then apply professional expertise to refine conclusions.

Geographic Information Systems (GIS): Mapping tools help visualize rental market dynamics, identify emerging investment areas, and analyze comparable property locations relative to transport links, amenities, and employment centers.

Digital inspection tools: Tablets and specialized software streamline data collection, photo documentation, and report generation. Cloud-based platforms enable real-time collaboration with institutional clients managing large portfolios.

Rental market databases: Subscription services providing comprehensive rental transaction data improve income assessment accuracy and support defensible rental projections.

Building Information Modeling (BIM): For larger HMOs and new-build buy-to-let developments, BIM integration allows surveyors to assess construction quality, identify potential defects, and estimate lifecycle costs with greater precision.

Technology should enhance rather than replace professional surveying expertise. The most effective approach combines data-driven analysis with on-site inspection, local market knowledge, and experienced professional judgment.

Conclusion

Valuing buy-to-let properties in 2026 requires sophisticated strategies that address institutional landlord demands, navigate complex tax pressures, and apply RICS-aligned methodologies across diverse property types. The market's transformation from individual small landlords to professional institutional investors fundamentally changes valuation requirements and expectations.

Key strategic imperatives for surveyors include:

✅ Master the four-tier valuation framework and understand when each approach applies

✅ Apply conservative rental income assessments that reflect sustainable market rates

✅ Develop HMO valuation expertise using appropriate size-based protocols

✅ Navigate the £2 million tax threshold with professional integrity and transparent methodology

✅ Provide portfolio-level analysis that serves institutional client strategic objectives

✅ Integrate technology tools while maintaining professional judgment primacy

The buy-to-let sector's continued evolution demands ongoing professional development, market research, and methodological refinement. Surveyors who invest in specialized expertise, maintain RICS compliance, and adapt to changing market dynamics will position themselves as essential advisors in this growing investment sector.

For property investors, engaging qualified surveyors who understand these complexities provides critical due diligence that protects capital, optimizes returns, and ensures regulatory compliance. Whether acquiring a single HMO or building an institutional portfolio, professional valuation services deliver insights that justify their cost many times over.

Next Steps for Property Professionals

📌 For surveyors: Pursue specialized training in buy-to-let valuation methodologies, HMO assessment protocols, and institutional portfolio analysis

📌 For investors: Commission comprehensive building surveys before acquisition and maintain regular condition surveys for portfolio properties

📌 For lenders: Ensure valuation instructions clearly specify property type, intended use, and risk factors requiring assessment

📌 For all stakeholders: Stay informed about tax policy changes, regulatory developments, and market trends affecting buy-to-let valuations

The 2026 buy-to-let market presents significant opportunities for those equipped with appropriate expertise, strategic insight, and professional standards. By applying the surveyor strategies outlined in this analysis, property professionals can navigate complexity, mitigate risk, and capitalize on the institutional landlord surge reshaping UK rental markets.

References

[1] Buy To Let Mortgage Valuations 2026 – https://www.property118.com/buy-to-let-mortgage-valuations-2026/

[2] Post Budget 2026 Valuation Challenges Surveyor Strategies For High Value Properties Over 2 Million – https://nottinghillsurveyors.com/blog/post-budget-2026-valuation-challenges-surveyor-strategies-for-high-value-properties-over-2-million

[3] The 2026 Property Reset Market Forecasts Budget Impacts Investor Focus – https://surveyingcorp.com/2025/12/the-2026-property-reset-market-forecasts-budget-impacts-investor-focus/

[4] Surveying The 2026 Buy To Let Boom Building Survey Protocols For Institutional Landlord Investments – https://nottinghillsurveyors.com/blog/surveying-the-2026-buy-to-let-boom-building-survey-protocols-for-institutional-landlord-investments

[5] 2026size Property Investors – https://www.buyassociationgroup.com/en-gb/news/2026size-property-investors/