The UK property market stands at a critical juncture in 2026. While expert forecasts suggest potential 4-5% national price growth, recent data paints a more complex picture that demands careful navigation by chartered surveyors. The RICS net balance for prices declined to -12% in February 2026, marking a concerning reversal after months of cautious optimism[5]. Against this backdrop of market uncertainty, new budget measures targeting properties valued above £2 million have introduced additional complications for Valuation Strategies for 4-5% National Price Growth in 2026: RICS Adjustments Post-Budget Tax Impacts on High-Value Properties.

For chartered surveyors and property professionals, recalibrating valuation methodologies has become essential. The gap between optimistic growth forecasts and current market realities requires sophisticated approaches that account for regional variations, tax implications, and evolving buyer sentiment. This comprehensive guide explores RICS-compliant tactics to navigate this stabilizing market effectively.

Key Takeaways

- Market sentiment remains cautious: RICS net balance dropped to -12% in February 2026, contradicting 4-5% growth forecasts and requiring conservative valuation approaches[5]

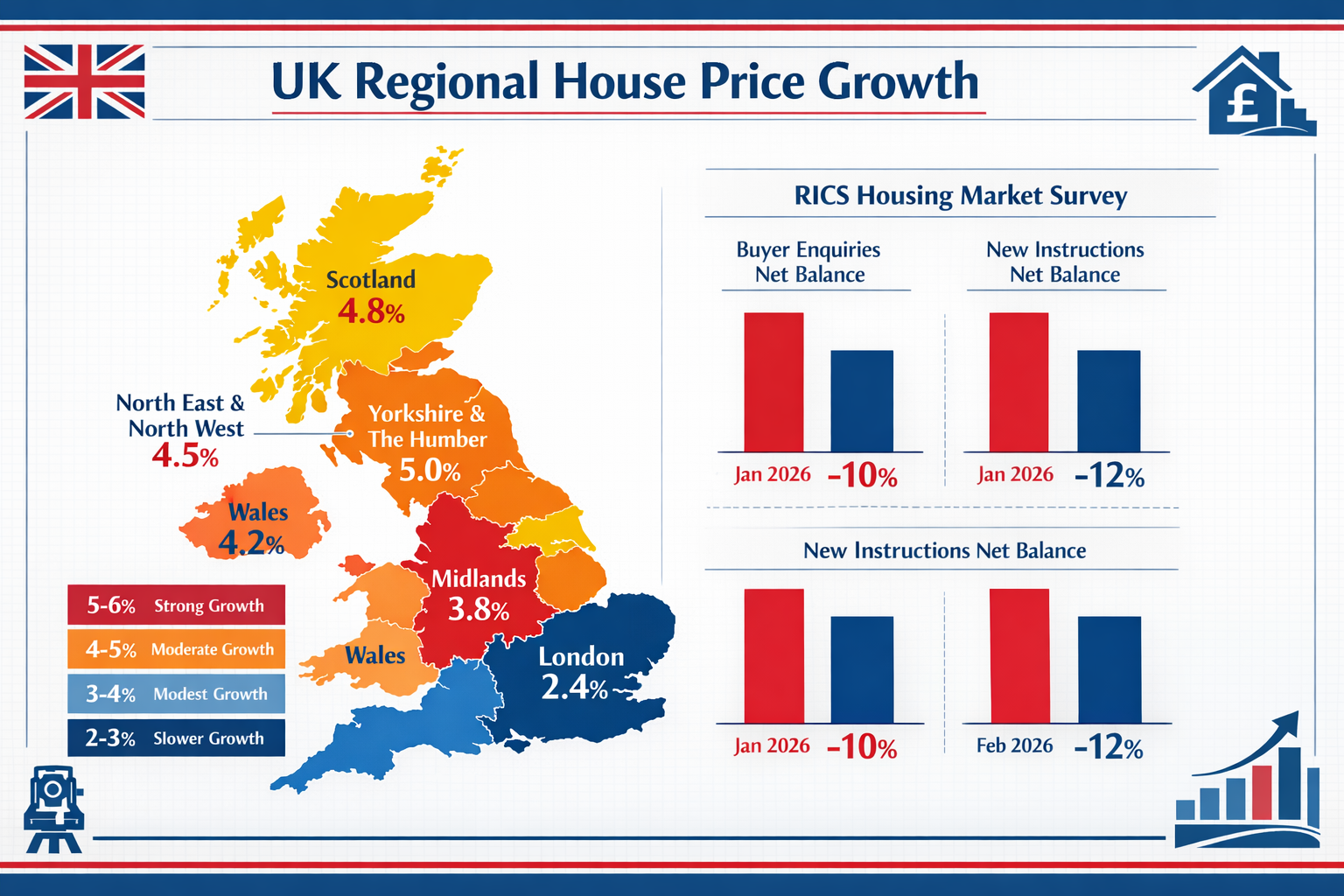

- Regional divergence is significant: London's 12-month price expectations fell sharply to +7%, while Scotland, Northern Ireland, and Northern England show stronger performance[2]

- Tax impacts on high-value properties: New budget measures affecting £2+ million properties demand specialized valuation adjustments and strategic planning

- RICS compliance is critical: Surveyors must adapt Red Book standards to reflect current market conditions while maintaining professional integrity

- Evidence-based valuations: Comparable sales analysis, market trend integration, and transparent methodology documentation are essential for defensible valuations

Understanding the Current UK Property Market Landscape in 2026

Current Market Indicators and Regional Variations

The UK residential property market in 2026 presents a fascinating paradox. While some analysts project 4-5% national price growth, the reality on the ground tells a different story. The Office for National Statistics recorded average UK house prices at £270,000, representing 2.4% growth in the 12 months to December 2025[3]. This modest appreciation falls significantly short of the more optimistic forecasts circulating in professional circles.

Recent RICS survey data reveals weakening momentum. The net balance for prices stood at -12% in February 2026, down from -10% in January, marking the first decline in four months[5]. This indicator measures the percentage of surveyors reporting price increases minus those reporting decreases, making it a reliable barometer of market sentiment.

Regional performance varies dramatically:

| Region | 12-Month Price Expectation | Market Characteristics |

|---|---|---|

| London | +7% | Sharp decline from +56% in January; luxury segment struggling |

| Scotland | +45% | Strong performance; affordability advantage |

| Northern Ireland | +38% | Consistent growth; first-time buyer activity |

| North of England | +35% | Moderate appreciation; steady demand |

| South East | +15% | Subdued growth; affordability constraints |

Understanding these regional disparities is crucial when developing Valuation Strategies for 4-5% National Price Growth in 2026: RICS Adjustments Post-Budget Tax Impacts on High-Value Properties. A comprehensive property valuation must account for local market conditions rather than relying solely on national averages.

The Reality Behind Growth Forecasts

The disconnect between projected 4-5% growth and actual market performance stems from several factors. Industry analysts describe the outlook as "modest movement" with expectations of low single-digit house price growth nationally for 2026[3]. This conservative assessment aligns more closely with observable market behavior.

Rightmove's March 2026 data showed annual asking price growth at -0.2% despite a seasonal 0.8% monthly uplift[3]. This negative annual figure underscores the challenging environment for sellers and the need for realistic pricing strategies.

"While surveyors expect +33% positive sentiment for 12-month price growth, this reflects moderate appreciation rather than the 4-5% growth some forecasts suggest." — RICS UK Residential Survey, February 2026[2]

For chartered surveyors conducting commercial valuations or residential assessments, these figures necessitate a recalibration of assumptions. Overly optimistic valuations risk professional liability and damage client relationships when properties fail to achieve expected prices.

Supply and Demand Dynamics

The fundamental supply-demand equation continues to influence market behavior. New buyer enquiries showed improvement in early 2026, with the RICS indicator rising to +10% in January before moderating[1]. However, this uptick in demand hasn't translated into proportional price increases due to several constraining factors:

Supply-side considerations:

- 📊 New listings remain constrained but gradually improving

- 🏗️ Construction activity limited by planning restrictions and material costs

- 💼 Investor activity subdued due to tax changes and regulatory burdens

- 🔄 Existing homeowners hesitant to sell in uncertain market conditions

Demand-side factors:

- 💰 Mortgage affordability challenges persist despite rate stabilization

- 👥 First-time buyers concentrated in more affordable regions

- 📉 Confidence remains fragile following economic uncertainty

- 🎯 Buyer selectivity increased; properties must be competitively priced

These dynamics create a market where Valuation Strategies for 4-5% National Price Growth in 2026: RICS Adjustments Post-Budget Tax Impacts on High-Value Properties must be grounded in evidence rather than optimistic assumptions. Professional surveyors need to demonstrate how their valuations account for these competing pressures.

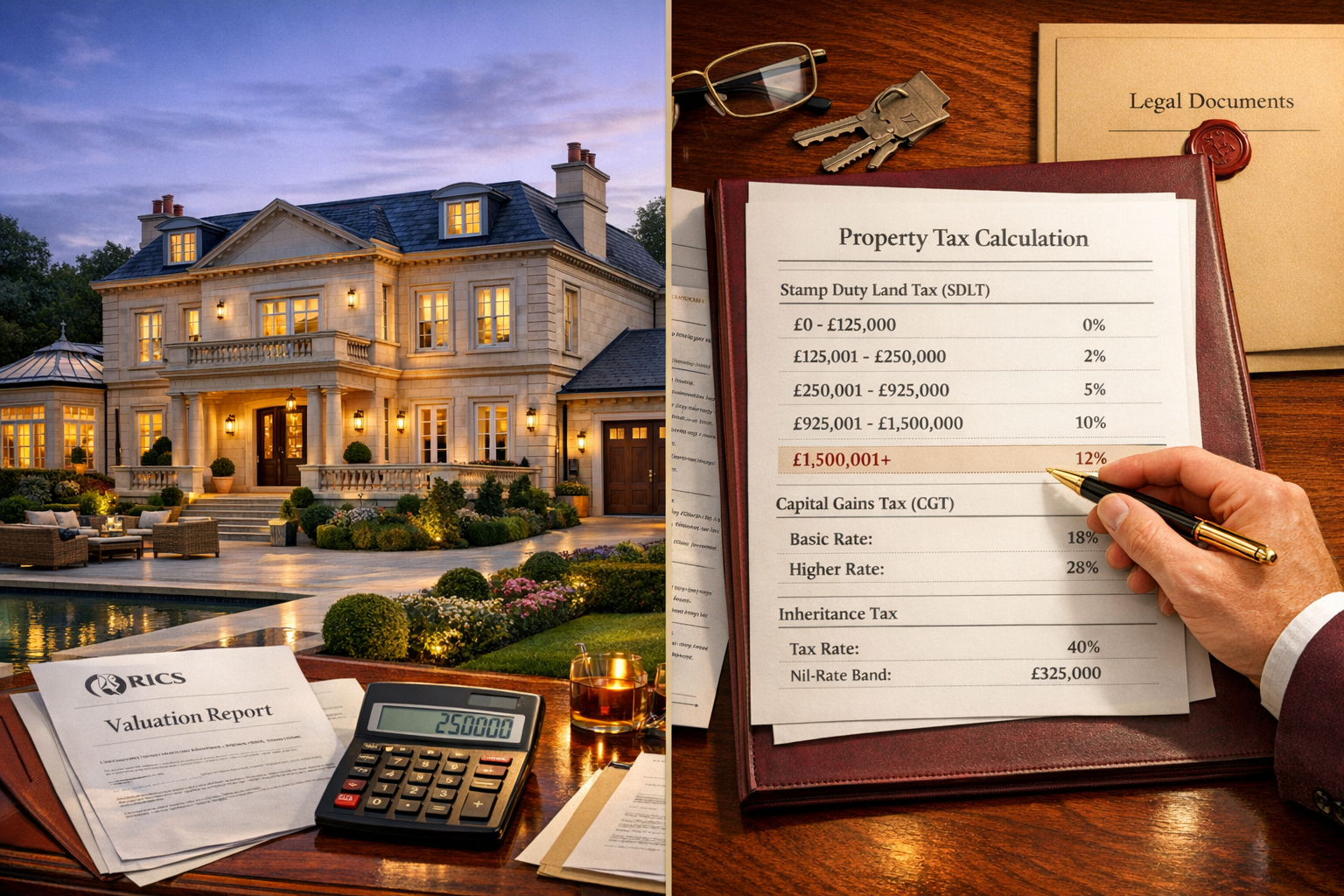

Post-Budget Tax Impacts on High-Value Properties

New Tax Measures Affecting £2+ Million Properties

The 2026 budget introduced significant changes affecting high-value residential properties, particularly those valued above £2 million. These measures have profound implications for valuation methodologies and require careful consideration when assessing premium properties.

Key tax changes impacting high-value properties:

- Enhanced Stamp Duty Land Tax (SDLT): Additional surcharges on properties exceeding £2 million create transaction cost barriers

- Capital Gains Tax adjustments: Modified rates and allowances affect investment property valuations

- Inheritance Tax considerations: Changes to reliefs impact estate planning and property holding structures

- Annual Tax on Enveloped Dwellings (ATED): Increased rates for properties held in corporate structures

These tax modifications directly influence buyer behavior and market liquidity in the premium segment. Properties subject to higher tax burdens typically experience downward price pressure as buyers factor additional costs into their acquisition decisions.

For chartered surveyors, understanding these tax implications is essential when preparing annual tax valuations or advising clients on property transactions. The tax burden can represent a significant percentage of property value, particularly for properties just above key thresholds.

Valuation Adjustments for Tax-Affected Properties

When developing Valuation Strategies for 4-5% National Price Growth in 2026: RICS Adjustments Post-Budget Tax Impacts on High-Value Properties, surveyors must incorporate tax impacts into their analysis. This requires a nuanced approach that goes beyond simple comparable sales analysis.

Recommended adjustment methodology:

Step 1: Identify comparable sales — Select transactions of similar properties, adjusting for location, size, condition, and amenities. Ensure comparables reflect post-budget market conditions where possible.

Step 2: Calculate tax burden differential — Determine the incremental tax cost for the subject property compared to alternatives. Properties just above £2 million thresholds may face disproportionate impacts.

Step 3: Apply market-derived discount — Analyze transaction evidence to quantify how buyers discount prices to offset tax burdens. This typically ranges from 50-80% of the additional tax cost, depending on market conditions.

Step 4: Consider holding period — Longer-term investors may discount more heavily for ongoing tax obligations (like ATED), while owner-occupiers focus primarily on acquisition taxes.

Step 5: Document assumptions — Maintain clear records of tax calculations and market evidence supporting adjustment factors. RICS standards require transparent methodology.

Impact on Market Liquidity and Pricing

High-value properties have experienced reduced liquidity following the budget changes. London's sharp decline in 12-month price expectations from +56% to +7% between January and February 2026 reflects this cooling sentiment in the premium market[2].

Observable market impacts include:

- ⏱️ Extended marketing periods: Properties above £2 million taking 25-40% longer to sell

- 💵 Increased price negotiation: Buyers leveraging tax costs to negotiate discounts

- 📍 Threshold sensitivity: Properties priced just above £2 million facing particular resistance

- 🔄 Market segmentation: Growing divergence between sub-£2 million and premium segments

For surveyors conducting insurance reinstatement cost valuations or leasehold extension valuations, these tax impacts may have indirect effects. While reinstatement costs remain driven by construction expenses, market value components of leasehold valuations must reflect the changed tax environment.

Strategic Considerations for High-Value Property Owners

Property owners in the premium segment face important decisions regarding timing, pricing, and holding structures. Chartered surveyors providing advisory services should consider:

Pricing strategy recommendations:

- Position properties competitively within their market segment

- Consider pricing below key thresholds (£2 million) where feasible

- Account for buyer tax calculations in asking price determination

- Provide transparent tax impact analysis to potential buyers

Holding structure optimization:

- Review corporate ownership structures given ATED changes

- Evaluate trust arrangements for inheritance tax planning

- Consider timing of disposals relative to tax year boundaries

- Assess renovation and improvement strategies to maximize value

Professional surveyors working with exclusive properties must integrate these strategic considerations into their valuation advice, ensuring clients understand both the current market value and the tax-optimized approach to property ownership.

RICS-Compliant Valuation Strategies for Stabilizing Markets

Adapting Red Book Standards to Current Conditions

The RICS Valuation – Global Standards (Red Book) provides the framework for professional valuation practice. However, applying these standards in a market characterized by conflicting signals requires careful judgment and adaptation. Valuation Strategies for 4-5% National Price Growth in 2026: RICS Adjustments Post-Budget Tax Impacts on High-Value Properties must remain compliant while reflecting market realities.

Core Red Book principles for current market conditions:

VPS 3 – Valuation Reports: Enhanced disclosure requirements become critical when market conditions are uncertain. Valuers must clearly state assumptions about growth rates, market trends, and tax impacts. Where forecasts suggest 4-5% growth but current indicators show weakness, this divergence must be explicitly addressed.

VPS 4 – Bases of Value: Market value definitions require careful application. The concept of "willing buyer and willing seller" must reflect actual market behavior, not theoretical projections. In the current environment, willing buyers are demonstrably cautious, as evidenced by the -12% RICS net balance[5].

VPGA 10 – Matters that May Give Rise to Material Valuation Uncertainty: The gap between forecast growth and observable market behavior may constitute material uncertainty. Valuers should consider including appropriate caveats when conditions warrant.

Evidence-Based Comparable Sales Analysis

Robust comparable sales analysis forms the foundation of defensible valuations. In a market where growth forecasts diverge from reality, relying on objective transaction evidence becomes even more critical.

Best practices for comparable selection:

-

Recency weighting: Prioritize transactions from the past 3-6 months. In rapidly changing markets, older comparables may not reflect current conditions.

-

Adjustment transparency: Document all adjustments for differences in location, size, condition, and amenities. Use percentage adjustments supported by market evidence rather than arbitrary figures.

-

Tax impact consideration: When valuing properties affected by post-budget tax changes, select comparables that reflect similar tax positions. Pre-budget transactions may require adjustment.

-

Regional specificity: Given the significant regional variations in 2026 market performance, avoid over-reliance on national trends. A property in Scotland requires Scottish comparables, not London-based evidence.

-

Volume and quality: Use multiple comparables (minimum 3-5) to establish a range of values. Single comparable reliance creates vulnerability to anomalous transactions.

Comparable adjustment framework:

Base comparable price: £X

+ Location premium/discount: ±Y%

+ Size adjustment: ±Z per sq ft

+ Condition differential: ±A%

+ Amenity adjustments: ±B%

+ Tax impact adjustment: ±C%

= Adjusted comparable value: £Result

This systematic approach ensures consistency and provides clear documentation for clients and third parties reviewing the valuation.

Incorporating Market Trend Analysis

While comparable sales provide the primary evidence base, trend analysis offers important context. However, surveyors must distinguish between observable trends and speculative forecasts.

Reliable trend indicators for 2026:

- ✅ RICS net balance figures: Monthly data showing actual surveyor sentiment

- ✅ ONS house price index: Official statistics based on completed transactions

- ✅ Mortgage approval volumes: Leading indicator of future transaction activity

- ✅ Days on market trends: Observable changes in marketing periods

- ✅ Price reduction frequency: Percentage of listings requiring price cuts

Questionable trend sources:

- ❌ Unsubstantiated growth forecasts: Predictions not grounded in current data

- ❌ Marketing-driven projections: Estate agent optimism not supported by transactions

- ❌ Historical extrapolation: Assuming past performance predicts future results

- ❌ Selective regional data: Cherry-picking high-performing areas to suggest national trends

When preparing land value calculations or development appraisals, trend analysis becomes particularly important. Future value assumptions drive development viability, making conservative, evidence-based projections essential.

Addressing Valuation Uncertainty and Risk

The current market environment introduces significant uncertainty into valuation practice. Professional standards require acknowledgment and appropriate handling of this uncertainty.

Risk mitigation strategies:

Scenario analysis: Rather than providing a single point valuation, consider presenting a range based on different market scenarios:

- Conservative scenario: Continued market weakness, 0-2% growth

- Base case scenario: Modest recovery, 2-4% growth

- Optimistic scenario: Forecast achievement, 4-5% growth

Sensitivity testing: Demonstrate how changes in key assumptions affect valuation conclusions. This might include varying growth rates, tax impacts, or market liquidity assumptions.

Assumption documentation: Maintain detailed records of all assumptions, data sources, and analytical methods. This documentation protects against professional liability claims and demonstrates RICS compliance.

Client communication: Ensure clients understand the limitations of valuations in uncertain markets. Written reports should include appropriate caveats about market volatility and the potential for values to change.

Regular revaluation: In rapidly changing markets, valuations can become outdated quickly. Recommend periodic revaluation for properties held for lending security, insurance, or financial reporting purposes.

Special Considerations for Different Valuation Purposes

Different valuation purposes require tailored approaches, particularly in the context of Valuation Strategies for 4-5% National Price Growth in 2026: RICS Adjustments Post-Budget Tax Impacts on High-Value Properties.

Mortgage lending valuations: Lenders require conservative valuations that protect against market downturns. In the current environment, applying the lower end of value ranges and avoiding optimistic growth assumptions aligns with prudent lending practice.

Probate and tax valuations: These require market value at a specific date, typically without regard to future growth. Current market weakness may benefit estates by reducing inheritance tax liabilities, making accurate reflection of current conditions essential.

Financial reporting valuations: Companies holding property assets must reflect fair value in accordance with accounting standards. The divergence between forecast and actual market performance may require impairment recognition for some properties.

Right to Buy valuations: These specialized assessments must reflect the specific statutory framework while incorporating current market conditions. Professional guidance on Right to Buy valuations ensures compliance with both RICS standards and legal requirements.

Practical Implementation: Tools and Techniques for 2026

Data Sources and Market Intelligence

Effective valuation in 2026 requires access to comprehensive, current market data. Chartered surveyors should develop a systematic approach to data collection and analysis.

Essential data sources:

- RICS monthly surveys: Primary source for surveyor sentiment and market trends[2]

- Land Registry data: Official transaction records providing comparable sales evidence

- ONS house price indices: National and regional price trend statistics[3]

- Mortgage lender reports: Halifax, Nationwide, and other lender indices

- Property portals: Rightmove, Zoopla for asking price trends and market inventory

- Local market intelligence: Direct knowledge from active market participation

Data integration techniques:

Create a systematic database of local comparables, updated monthly with new transactions. Track key metrics including:

- Average price per square foot by property type

- Days on market by price band

- Percentage of asking price achieved

- Volume of transactions by area

- New listing volumes and trends

This database becomes an invaluable resource for rapid, accurate valuations and supports the development of location-specific adjustment factors.

Technology and Valuation Software

Modern valuation practice increasingly relies on technology to enhance accuracy, efficiency, and compliance. Several tools can support Valuation Strategies for 4-5% National Price Growth in 2026: RICS Adjustments Post-Budget Tax Impacts on High-Value Properties.

Recommended technology solutions:

Automated Valuation Models (AVMs): While not suitable as standalone valuation tools for RICS purposes, AVMs provide useful cross-checks and help identify appropriate comparables. Use AVMs to validate rather than replace professional judgment.

Geographic Information Systems (GIS): Mapping tools help visualize comparable locations, identify micro-market boundaries, and analyze location-based value differentials.

Valuation report software: Standardized templates ensure consistency, completeness, and RICS compliance across all valuations. These systems also facilitate quality control and peer review.

Market data platforms: Subscription services providing comprehensive transaction data, planning information, and market analytics streamline research and improve accuracy.

Financial modeling tools: Spreadsheet-based models for discounted cash flow analysis, development appraisals, and investment valuations. These should include sensitivity analysis capabilities.

Quality Assurance and Peer Review

Given the challenging market conditions in 2026, robust quality assurance processes become essential for maintaining professional standards and managing risk.

Quality assurance framework:

-

Internal peer review: All valuations above specified thresholds (e.g., £1 million) should undergo review by a senior colleague before issuance.

-

Methodology consistency: Establish firm-wide standards for comparable selection, adjustment factors, and report formats to ensure consistency across valuers.

-

Assumption documentation: Maintain detailed working papers supporting all valuations, including comparable selection rationale, adjustment calculations, and market trend analysis.

-

Client feedback: Systematically collect feedback on valuation accuracy when properties subsequently transact, using this information to refine methodologies.

-

Continuing professional development: Ensure all valuers maintain current knowledge of market conditions, RICS standards, and relevant tax legislation through regular training.

Case Study: Applying Strategies to a £2.5 Million London Property

To illustrate practical application of these principles, consider a hypothetical valuation scenario:

Property details:

- Location: Prime Central London

- Type: Four-bedroom townhouse

- Size: 2,200 square feet

- Condition: Excellent, recently renovated

- Purpose: Mortgage lending valuation

Market context:

- London 12-month expectations: +7% (down from +56%)[2]

- Subject to enhanced SDLT and potential ATED

- Marketing period for similar properties: 4-6 months

- Recent price reductions common in this segment

Valuation approach:

Step 1: Identify five comparable sales from past six months, ranging from £2.2-£2.7 million. Adjust for differences in size, condition, and exact location.

Step 2: Analyze asking prices versus achieved prices. Recent comparables showing average 8% reduction from initial asking price, indicating buyer negotiating power.

Step 3: Apply tax impact adjustment. Properties just above £2 million showing additional 3-5% discount as buyers factor in enhanced tax burden.

Step 4: Consider market trend. Given negative RICS net balance and declining London sentiment, apply conservative approach within comparable range.

Step 5: Determine value range: £2.35-£2.50 million. For mortgage lending purposes, adopt conservative figure of £2.40 million, providing lender with appropriate security margin.

Report disclosure: Clearly state assumptions about market conditions, tax impacts, and the divergence between some growth forecasts and current observable trends. Include appropriate caveats about market uncertainty.

This systematic approach demonstrates how Valuation Strategies for 4-5% National Price Growth in 2026: RICS Adjustments Post-Budget Tax Impacts on High-Value Properties can be applied in practice while maintaining RICS compliance and professional standards.

Conclusion

The UK property market in 2026 presents significant challenges for chartered surveyors and valuation professionals. While some forecasts suggest 4-5% national price growth, the reality reflected in RICS data tells a more cautious story. The net balance of -12% in February 2026, combined with annual growth of just 2.4%, demonstrates the gap between optimistic projections and market reality[3][5].

Valuation Strategies for 4-5% National Price Growth in 2026: RICS Adjustments Post-Budget Tax Impacts on High-Value Properties must be grounded in evidence rather than speculation. The post-budget tax changes affecting properties above £2 million have created additional complexity, particularly in London and the South East where premium properties face extended marketing periods and increased price negotiation.

Successful navigation of this environment requires:

✅ Rigorous application of RICS Red Book standards with enhanced disclosure of assumptions and market uncertainties

✅ Evidence-based comparable sales analysis that prioritizes recent transactions and accounts for tax impacts

✅ Regional specificity recognizing the significant performance variations between London (+7% expectations) and stronger regions like Scotland (+45%)[2]

✅ Conservative professional judgment that protects clients and maintains professional credibility in uncertain conditions

✅ Transparent methodology documentation supporting all valuation conclusions with clear audit trails

Actionable Next Steps

For chartered surveyors and property professionals:

-

Review current valuation methodologies to ensure they reflect 2026 market conditions rather than outdated assumptions about growth rates.

-

Enhance data collection systems to maintain comprehensive, current comparable sales databases with particular attention to post-budget transactions.

-

Implement quality assurance processes including peer review for high-value and complex valuations.

-

Update client communication to ensure realistic expectations about property values, marketing periods, and tax implications.

-

Invest in continuing professional development to maintain current knowledge of RICS standards, tax legislation, and market trends.

-

Consider specialist advice for complex scenarios, particularly involving high-value properties, development sites, or unusual tax situations.

The stabilizing market of 2026 demands professionalism, rigor, and evidence-based practice. By applying these principles, chartered surveyors can provide valuable guidance to clients while maintaining the highest standards of professional practice. Whether conducting commercial valuations, annual tax assessments, or specialized property appraisals, the strategies outlined in this guide provide a framework for navigating the challenges and opportunities of the 2026 property market.

The divergence between forecast and reality serves as a reminder that professional valuation is both art and science, requiring judgment, experience, and unwavering commitment to evidence-based practice. As market conditions continue to evolve throughout 2026, these principles will remain essential for delivering valuations that serve clients effectively while upholding the reputation and standards of the chartered surveying profession.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[3] Uk Residential Property Market Update Spring 2026 – https://www.vailwilliams.com/uk-residential-property-market-update-spring-2026/

[5] tradingeconomics – https://tradingeconomics.com/united-kingdom/rics-house-price-balance/news/532749