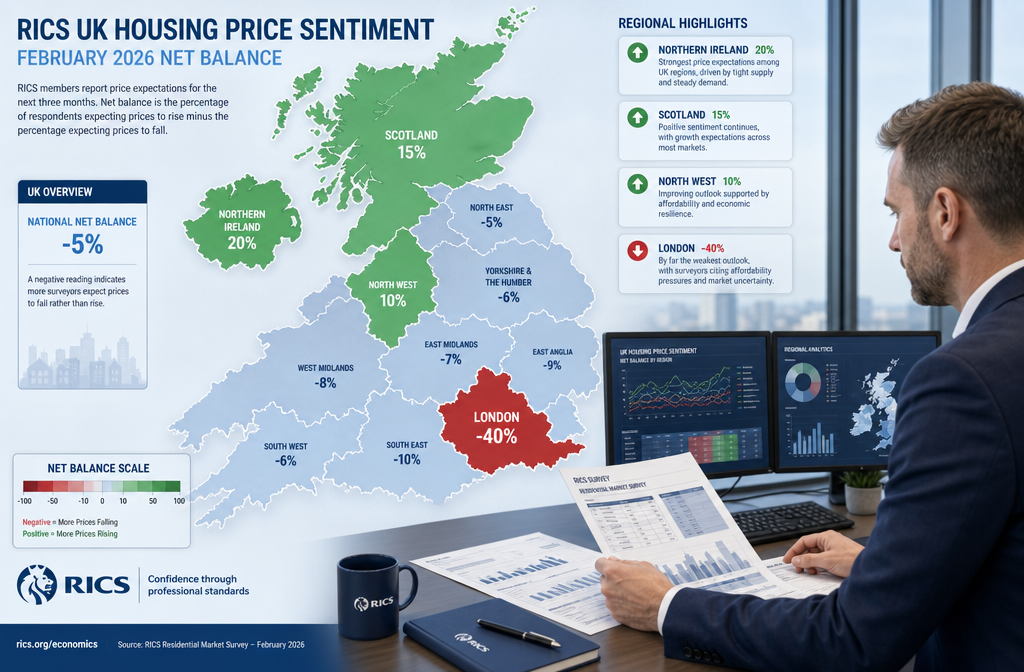

London's house price sentiment collapsed to a net balance of -40% in February 2026 — the steepest regional decline recorded in the RICS UK Residential Survey — while Northern Ireland, Scotland, and the North West reported rising prices in the same month [1]. That single data point captures the central challenge facing valuers across the UK right now: national headline figures have become almost meaningless when regional divergence is this extreme.

Achieving valuation resilience using RICS February 2026 survey data: countering geopolitical impacts on regional prices requires more than reading a headline net balance. It demands a granular, evidence-led approach that accounts for local demand signals, geopolitical headwinds, and the structural conditions unique to each market. This article explains what the February 2026 data actually shows, why geopolitical uncertainty is reshaping buyer behaviour, and how surveyors and property professionals can build defensible valuations in this environment.

Key Takeaways

- The RICS February 2026 survey recorded a headline house price balance of -12%, masking extreme regional divergence from -40% in London to positive readings in northern regions.

- New buyer enquiries fell sharply to a net balance of -26%, driven in part by geopolitical uncertainty including Middle East conflict escalation.

- Twelve-month price expectations remain positive at +33%, offering a longer-term anchor for valuation commentary despite short-term caution.

- Surveyors must move beyond national averages and apply precise, locality-specific adjustments supported by documented evidence.

- Enhanced defect documentation, explicit marketability commentary, and geopolitical risk acknowledgement are now essential components of a resilient valuation report.

What the RICS February 2026 Data Actually Shows

Headline Figures and What They Conceal

The RICS UK Residential Survey for February 2026 recorded a headline house price balance of -12%, suggesting a broadly flat to marginally negative national trend [1]. At face value, this is not alarming. But the headline figure conceals a market that is pulling in sharply different directions depending on geography.

New buyer enquiries fell to a net balance of -26% in February, down from -15% in January — a significant deterioration in demand momentum over just four weeks [1]. Agreed sales edged lower to -12%, and short-term price expectations weakened from -6% in January to -18% in February, reflecting growing caution among both buyers and agents [1].

Supply remained broadly stable. New vendor instructions came in at just +2%, meaning the number of properties being listed for sale held roughly steady [1]. This is important context: the demand weakness is not being matched by a flood of new stock, which limits the downside pressure on prices in most regions.

The Regional Picture: A Market Divided

The most striking feature of the February 2026 data is the regional divergence in price sentiment. Consider the contrast:

| Region | February 2026 Price Sentiment |

|---|---|

| London | -40% (net balance) |

| Yorkshire and the Humber | +3.9% annual growth |

| Northern Ireland | Positive (rising) |

| Scotland | Positive (rising) |

| North West | Positive (rising) |

London's reading of -40% is the steepest regional decline recorded in the survey [2]. Meanwhile, regions further north are experiencing genuine price growth, supported by stronger affordability ratios and less exposure to the international capital flows that make London particularly sensitive to geopolitical instability.

For anyone seeking to understand what house prices are doing in 2026, the answer depends entirely on which postcode is under consideration.

Rental Market Signals

The rental sector adds another layer of complexity. Tenant demand was broadly stable at +2% in the three months to February, but new landlord instructions remained deeply negative at -27% [1]. This ongoing supply constraint in the rental market has implications for valuation, particularly for buy-to-let assets and properties in areas where rental demand underpins capital values.

Geopolitical Uncertainty and Its Transmission Into UK Property Markets

How Global Events Reach Regional Prices

The RICS February 2026 survey explicitly cites the escalation of conflict in the Middle East as a factor dampening market momentum [1]. Understanding the transmission mechanism — how a geopolitical event thousands of miles away affects a semi-detached house in Surrey or a flat in Manchester — is essential for building a resilient valuation argument.

The pathway works broadly as follows:

- Risk aversion increases — investors and households become more cautious about large financial commitments.

- Mortgage market tightening — lenders reprice risk, and some product ranges are withdrawn or restricted.

- Consumer confidence falls — discretionary decisions, including property purchases, are deferred.

- Currency and capital flow shifts — international buyers, particularly active in prime London, reduce exposure to sterling-denominated assets.

- Regional demand responds unevenly — markets with lower international buyer participation (northern regions) are less directly affected.

This explains why London's -40% sentiment reading is so much worse than the national average. The capital's property market has a structural dependency on international capital and high-income professional demand that makes it acutely sensitive to global uncertainty [2].

Short-Term Caution vs Long-Term Confidence

One of the most useful features of the February 2026 data for valuation purposes is the gap between short-term and twelve-month price expectations.

Short-term price expectations fell to -18% in February 2026. Twelve-month expectations remained positive at +33%, down from +43% the previous month but still firmly in positive territory [1].

This divergence matters enormously for valuation methodology. A surveyor who anchors a valuation purely to current transaction evidence — which is thin and skewed by cautious buyers — risks producing a figure that understates longer-term market value. Conversely, ignoring short-term weakness entirely would produce an overly optimistic result that fails to reflect current marketability.

The professional answer is to acknowledge both signals explicitly in valuation commentary, weight comparable evidence carefully, and apply adjustments that are transparent and documented.

Valuation Resilience Using RICS February 2026 Survey Data: Countering Geopolitical Impacts on Regional Prices in Practice

Building a Defensible Valuation in a Divergent Market

Achieving valuation resilience using RICS February 2026 survey data: countering geopolitical impacts on regional prices requires a structured methodology. The following principles reflect current best practice guidance emerging from the profession in response to this data [3] [4].

1. Reject national averages as a primary reference point

The -12% headline balance is not a useful input for a specific property valuation. Surveyors must identify the relevant regional and sub-regional data, weight it appropriately, and document why national figures have been set aside or treated as secondary context.

2. Apply locality-specific comparable analysis

In a market where transaction volumes are subdued (agreed sales at -12%), the pool of recent comparables may be limited [1]. Surveyors should extend their comparable search period cautiously, apply time adjustments that reflect the February 2026 sentiment shift, and flag where comparable evidence is thin.

3. Quantify geopolitical risk as a valuation input

Geopolitical uncertainty is not simply a narrative caveat — it has measurable effects on buyer demand, mortgage availability, and transaction timescales. Valuers are advised to incorporate global uncertainty explicitly into their valuation defence strategies and maintain enhanced documentation standards [3].

4. Differentiate between cyclical and structural price pressure

London's -40% sentiment reading contains both cyclical elements (short-term demand weakness) and structural elements (long-term affordability constraints, stamp duty impacts, international buyer caution). A resilient valuation distinguishes between these, because they have different implications for recovery timescales and value floors.

5. Address marketability explicitly

In markets characterised by reduced buyer demand, the time to sell a property increases. This affects value, particularly for properties with defects or unusual characteristics. Valuation commentary should explicitly address marketability, not just price [4].

Regional Adjustment Frameworks

For surveyors working across different regions, the February 2026 data supports a tiered adjustment framework:

London and South East:

- Apply downward sentiment adjustments reflecting -40% price balance

- Scrutinise comparable evidence for distress sales or motivated seller discounts

- Flag international buyer dependency as a risk factor in commentary

- Consider extended marketing period assumptions

Northern regions, Scotland, Northern Ireland:

- Positive price sentiment supports more stable comparable weighting

- Affordability ratios remain relatively favourable

- Rental supply constraints may support capital values in investment-grade stock

Midlands and transitional regions:

- Mixed signals require case-by-case analysis

- Weight local employment data and infrastructure investment alongside RICS sentiment figures

For properties in areas such as Surrey or West London, where price sensitivity to macroeconomic conditions is historically higher, the February 2026 data warrants particular care in comparable selection and commentary drafting.

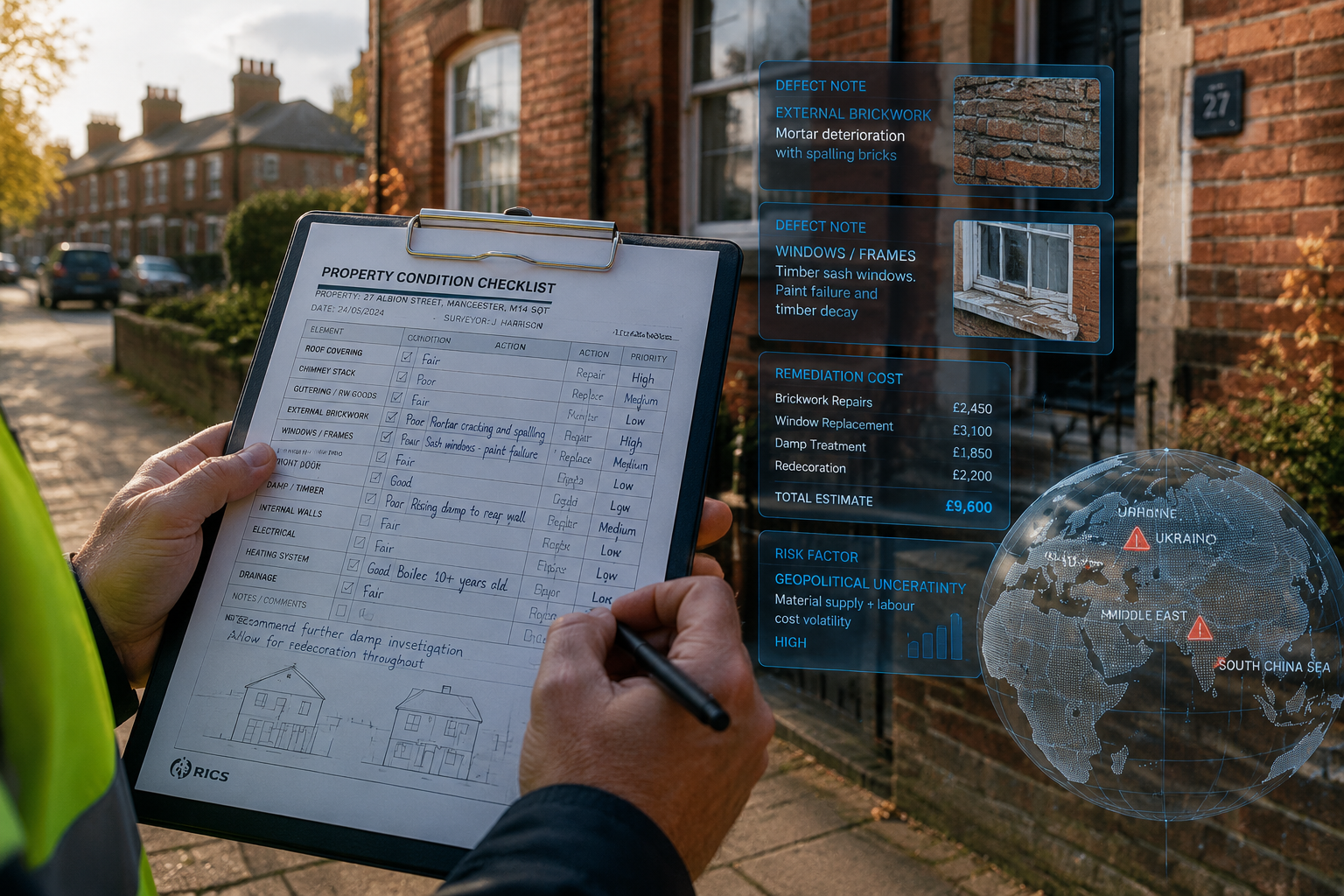

Enhanced Due Diligence and Defect Documentation

In a market where buyers are already cautious, defects carry greater weight. A property with unresolved structural issues or deferred maintenance faces a compounded marketability challenge when buyer enquiries are falling [4].

Surveyors should:

- Expand defect documentation beyond standard scope where market conditions amplify risk

- Quantify remediation costs with greater precision, using current contractor pricing rather than generic allowances

- Assess the impact on marketability explicitly, noting how identified defects interact with current demand conditions

For complex assessments, a Level 3 Full Building Survey provides the depth of investigation needed to support a fully defensible valuation in challenging market conditions. Understanding building materials and their condition is particularly important when quantifying remediation costs that feed into valuation adjustments.

Valuation Resilience Using RICS February 2026 Survey Data: Expert Witness and Dispute Considerations

The Rise of Valuation Disputes in Volatile Markets

Market volatility driven by geopolitical factors has contributed to an increase in valuation disputes [3]. When prices move sharply in one direction — or diverge dramatically between regions — the gap between what a buyer paid, what a lender valued, and what a property subsequently sells for can become legally significant.

Expert witnesses in valuation disputes arising from the February 2026 period face specific challenges:

- Thin comparable evidence due to subdued transaction volumes

- Rapid sentiment shifts between the valuation date and the dispute hearing

- Regional divergence that makes national market commentary potentially misleading

- Geopolitical factors that were identifiable but difficult to quantify at the time of valuation

The professional response is rigorous contemporaneous documentation. A valuation report written in February 2026 that acknowledges the RICS survey data, applies transparent regional adjustments, and explicitly flags geopolitical uncertainty as a risk factor is substantially more defensible than one that relies on bare comparable evidence [3].

Documentation Standards for Dispute Resilience

The following documentation standards are recommended for valuations prepared in the current environment:

| Documentation Element | Purpose |

|---|---|

| RICS survey data reference (February 2026) | Establishes awareness of market conditions at valuation date |

| Regional sentiment adjustment rationale | Justifies departure from national headline figures |

| Geopolitical risk acknowledgement | Demonstrates professional awareness of external factors |

| Comparable evidence with time adjustments | Supports the final figure with transparent methodology |

| Marketability commentary | Addresses buyer demand conditions explicitly |

| Defect remediation cost quantification | Links physical condition to value impact |

For properties where valuation is linked to lease extension or enfranchisement, the current market conditions add further complexity. Leasehold extension and enfranchisement valuations require particular care when market sentiment is shifting rapidly, as the assumptions embedded in statutory valuation formulae may not fully capture current conditions.

Understanding what to do if a home valuation comes in below an offer is also increasingly relevant in 2026, as the gap between agreed prices and formal valuations widens in pressure-sensitive markets.

Practical Steps for Property Professionals in 2026

For Surveyors and Valuers

- Download and retain the RICS February 2026 UK Residential Survey as a contemporaneous market reference for all valuations completed this month

- Build a regional adjustment log that tracks sentiment data by region, updated monthly as new RICS data is released

- Review comparable databases for evidence of distress pricing or extended marketing periods that may skew the pool

- Ensure valuation reports include explicit commentary on demand conditions, not just price comparables

- Engage with professional reasons why property owners hire surveyors to communicate the value of rigorous assessment in uncertain markets

For Buyers and Sellers

- Treat national house price headlines with scepticism — the February 2026 data shows a 80-percentage-point gap between London and the best-performing regions

- Commission a thorough survey before committing to a purchase in any market, but particularly in regions where price pressure is acute

- Understand that a valuation produced in February 2026 carries specific market context that may differ significantly from valuations produced six months earlier or later

- Seek advice from chartered surveyors in London or chartered surveyors in North London who are actively tracking local sentiment data

For Investors

- The rental supply constraint (-27% new landlord instructions) creates ongoing upward pressure on rents, supporting yield calculations for well-located investment stock

- Twelve-month price expectations at +33% suggest the current weakness may represent a buying opportunity in fundamentally strong locations

- Geopolitical uncertainty is a cyclical factor — structural undersupply of housing in the UK remains the dominant long-term driver of value

Conclusion

The RICS February 2026 UK Residential Survey delivers a clear message to property professionals: the UK housing market is not one market, and treating it as such in a valuation context is a professional risk. With London recording a -40% price sentiment balance while northern regions post growth, and with buyer enquiries falling sharply against a backdrop of geopolitical uncertainty, the February 2026 data demands a more sophisticated response than headline-reading allows.

Actionable next steps for valuers and property professionals:

- Integrate the February 2026 RICS data explicitly into all current valuation reports as a documented market reference point.

- Apply regional adjustments that reflect the specific sentiment data for the subject property's location, not national averages.

- Acknowledge geopolitical uncertainty as a named and quantified risk factor in valuation commentary, particularly for London and South East properties.

- Enhance defect documentation and remediation cost precision to reflect the amplified impact of physical condition on marketability in a low-demand environment.

- Monitor the twelve-month expectation data (+33%) as a counterbalance to short-term caution, ensuring valuations do not unduly penalise long-term value.

- Seek specialist support where valuation complexity is high — whether for leasehold, investment, or dispute-related instructions.

Valuation resilience using RICS February 2026 survey data: countering geopolitical impacts on regional prices is not a passive exercise. It requires active engagement with the data, transparent methodology, and the professional courage to depart from national averages when local evidence demands it.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026?utm_source=openai

[2] Valuation Adjustments In Regional Divergences RICS February 2026 Data For Surveyors In London Vs North – https://www.canterburysurveyors.com/blog/valuation-adjustments-in-regional-divergences-rics-february-2026-data-for-surveyors-in-london-vs-north/?utm_source=openai

[3] Geopolitical Uncertainty In RICS February 2026 Survey Expert Witness Preparation For Valuation Volatility Disputes – https://www.canterburysurveyors.com/blog/geopolitical-uncertainty-in-rics-february-2026-survey-expert-witness-preparation-for-valuation-volatility-disputes/?utm_source=openai

[4] Valuation Adjustments From February 2026 RICS Survey Countering Geopolitical Caution In Buyer Enquiries And Price Expectations – https://wimbledonsurveyors.com/valuation-adjustments-from-february-2026-rics-survey-countering-geopolitical-caution-in-buyer-enquiries-and-price-expectations/?utm_source=openai

[5] Valuation Divergence Post RICS February 2026 Expert Witness Strategies For Regional Disputes – https://www.canterburysurveyors.com/blog/valuation-divergence-post-rics-february-2026-expert-witness-strategies-for-regional-disputes/?utm_source=openai

[6] Valuation Challenges From RICS February 2026 Survey Expert Witness Strategies For 26 Buyer Enquiry Dip Disputes – https://wimbledonsurveyors.com/valuation-challenges-from-rics-february-2026-survey-expert-witness-strategies-for-26-buyer-enquiry-dip-disputes/?utm_source=openai