{"cover":"Professional landscape format (1536×1024) hero image featuring bold text overlay 'Valuation Adjustments for New Build Premiums in 2026: Surveyor Strategies Amid 2-5% Market Growth' in extra large 70pt white sans-serif font with dark shadow and semi-transparent navy overlay box, positioned in upper third center. Background shows modern new build housing development with contemporary homes, construction crane in distance, and chartered surveyor in professional attire holding clipboard and tablet reviewing property details in foreground. Split composition showing new build homes on left and established resale properties on right for comparison. Color palette: deep navy blue, white, amber accents. High contrast, magazine cover quality, editorial style with architectural photography aesthetic, bright daylight, professional depth of field.","content":["Detailed landscape format (1536×1024) editorial image showing close-up of professional chartered surveyor's hands holding digital tablet displaying property valuation report with percentage calculations, premium adjustments, and comparative market analysis data. Screen shows split comparison of new build property at £368,500 versus resale property at £298,700 with 23.4% premium highlighted in amber. Background shows blurred new build property exterior with modern facade. Include visible elements: energy efficiency rating chart, warranty documentation, price-per-square-foot calculations on tablet screen. Professional business aesthetic with natural lighting, shallow depth of field focusing on tablet screen, modern color scheme of navy, white, and data visualization blues and greens.","Unique landscape format (1536×1024) infographic-style photograph showing surveyor conducting on-site inspection inside bright new build property interior. Wide-angle view capturing surveyor measuring room dimensions with laser measure, with visible modern fixtures including energy-efficient windows, underfloor heating controls, and contemporary kitchen appliances in background. Overlay transparent data boxes showing tangible value components: £8,000-£12,000 energy savings over 10 years, £15,000-£20,000 warranty value, £7,000-£10,000 maintenance savings. Professional inspection aesthetic with natural window light, clean modern interior, surveyor wearing business casual with high-visibility vest, clipboard and professional equipment visible, architectural photography style with clear details.","Distinctive landscape format (1536×1024) aerial drone photograph showing regional comparison of UK housing developments. Bird's eye view capturing three distinct sections: North East affordable new build semi-detached homes (£212,000 average), London compact new build flats (450-550 sq ft), and South East premium new build houses. Each section labeled with transparent overlay boxes showing regional premium percentages and price-per-square-foot calculations. Include visible street layouts, property sizes comparison, and color-coded regional zones in amber, navy, and teal. Professional real estate photography with clear daylight, high detail showing architectural differences between regions, cartographic style with data visualization elements, editorial quality suitable for property market analysis reports."]

The UK property market in 2026 presents chartered surveyors with a fascinating challenge: accurately valuing new build properties as 'hope value' discounts erode in recovering markets. With Valuation Adjustments for New Build Premiums in 2026: Surveyor Strategies Amid 2-5% Market Growth becoming increasingly critical, professionals must navigate a landscape where new builds command a national premium of 23.4% above resale prices, yet market forecasts predict modest growth of just 2-5% across most regions[1][2]. This creates a complex valuation environment where distinguishing genuine value from inflated pricing requires sophisticated analytical techniques and regional market knowledge.

As buyer demand upticks and mortgage rates stabilize, surveyors face scrutiny over whether substantial new build premiums remain justified. The gap between new build prices averaging £368,500 and resale properties at £298,700 demands careful examination of tangible value components versus speculative pricing[1]. Understanding these dynamics is essential for accurate mortgage valuations, investment assessments, and protecting client interests in 2026's evolving market.

Key Takeaways

✅ National new build premium stands at 23.4% above resale prices, with tangible value components justifying only 15-20% of this premium through energy savings, warranties, and lower maintenance costs[1]

✅ Regional variation is substantial, with London showing 15.3% price-per-square-foot premiums despite smaller unit sizes, while the North East offers the most accessible entry point at £212,000 average for semi-detached new builds[1]

✅ 2026 growth forecasts range from 2-5% across major institutions, with northern regions expected to outperform southern areas due to affordability pressures and tax changes affecting London and the South East[2][3]

✅ Stamp duty threshold changes from April 2025 now impact first-time buyers at £300,000+ and home movers at £125,000+, fundamentally altering true acquisition costs that surveyors must factor into valuations[2]

✅ Price-per-square-foot analysis reveals critical insights, particularly for flats where new builds average 450-550 sq ft compared to 550-700+ sq ft for resale conversions, making headline price comparisons misleading[1]

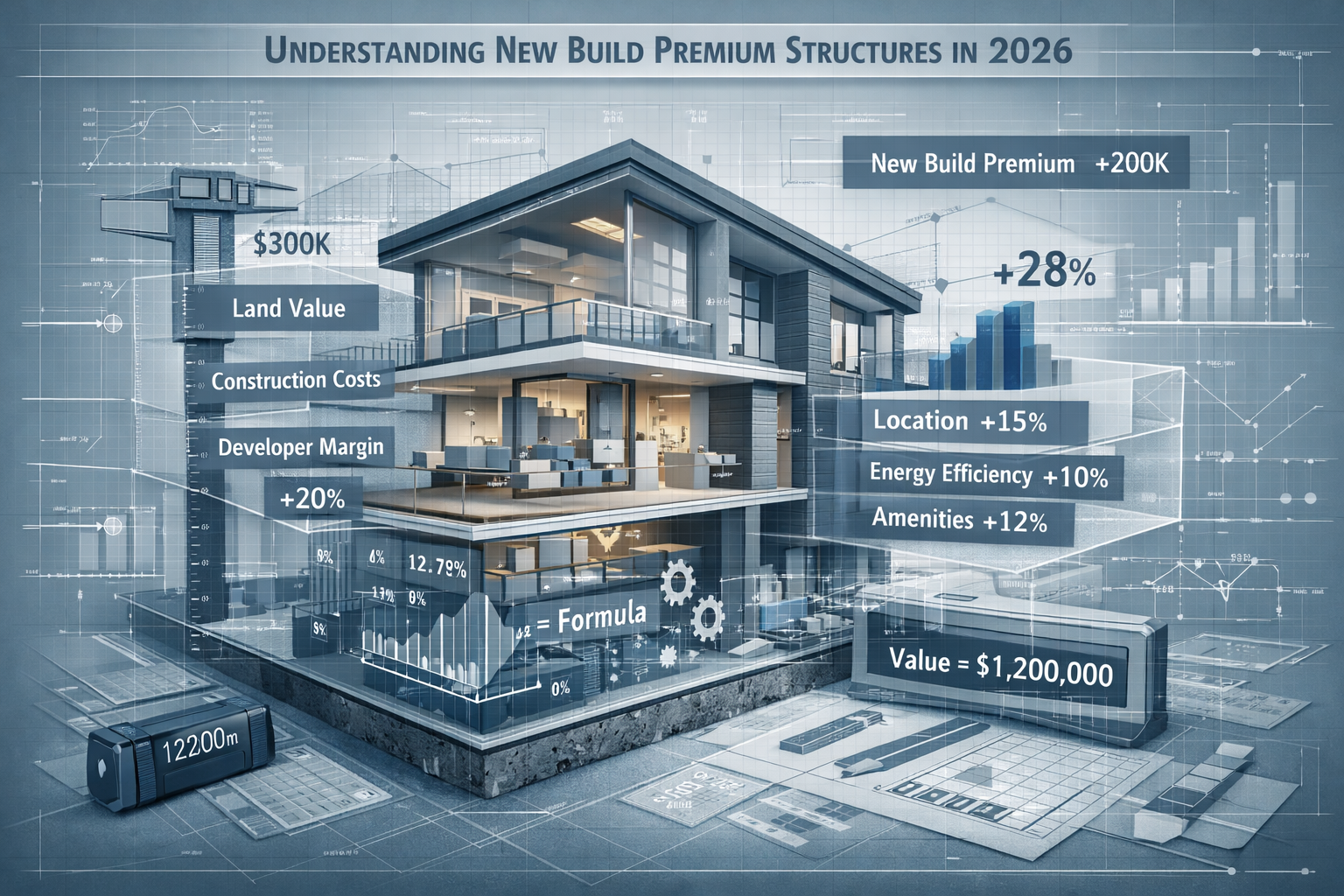

Understanding New Build Premium Structures in 2026

The Valuation Adjustments for New Build Premiums in 2026: Surveyor Strategies Amid 2-5% Market Growth framework begins with comprehending the underlying premium structure. As of September 2025 data from HM Land Registry, the national average new build premium of 23.4% represents a cumulative structure rather than annual growth[1]. Chartered surveyors must dissect this premium into justified and speculative components.

Tangible Value Components

Research demonstrates that 15-20% premiums can be justified through measurable value components[1]. Over a 10-year ownership period, new build properties deliver approximately £30,000-£50,000 in tangible benefits:

| Value Component | 10-Year Benefit | Annual Impact |

|---|---|---|

| Energy Efficiency Savings | £8,000-£12,000 | £800-£1,200 |

| NHBC/Developer Warranties | £15,000-£20,000 | £1,500-£2,000 |

| Reduced Maintenance Costs | £7,000-£10,000 | £700-£1,000 |

| Included Fixtures/Appliances | £5,000-£8,000 | £500-£800 |

When conducting property valuations, surveyors should document these tangible benefits explicitly. Properties carrying premiums exceeding 30% warrant careful scrutiny, particularly when assessed on a price-per-square-foot basis rather than headline prices alone.

The Price-Per-Square-Foot Reality

Price-per-square-foot analysis reveals hidden premiums that headline comparisons obscure. London provides the clearest example: new builds carry only a 4.7% headline price premium, yet command a 15.3% premium on a per-square-foot basis[1]. This discrepancy exists because new build flats typically measure 450-550 sq ft, substantially smaller than comparable resale converted flats at 550-700+ sq ft.

"Surveyors assessing value above 30% premiums should warrant careful scrutiny, particularly on a price-per-square-foot basis." – New Builds UK Market Analysis[1]

For professionals conducting building surveys, this metric provides more reliable valuation benchmarks than simple price comparisons. When evaluating whether a new build justifies its premium, calculating the effective cost per square foot against local resale comparables reveals the true market position.

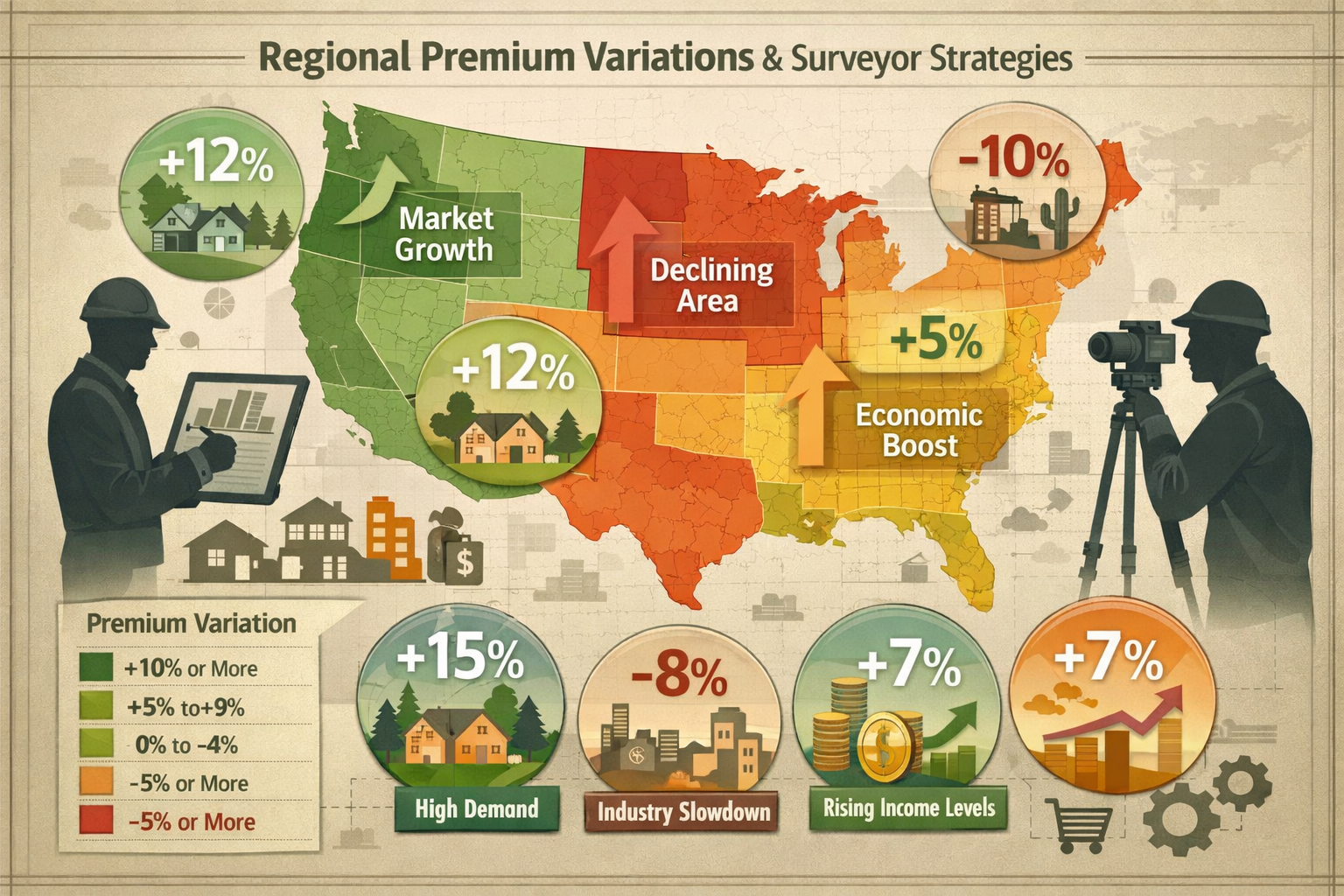

Regional Premium Variations and Surveyor Strategies

Valuation Adjustments for New Build Premiums in 2026: Surveyor Strategies Amid 2-5% Market Growth must account for substantial regional disparities. The UK market exhibits dramatic variation in both absolute premiums and percentage differentials across regions[1].

North East: Accessible Entry Points

The North East offers the lowest absolute premium at £65,600, with new build semi-detached homes averaging £212,000[1]. For surveyors working with first-time buyers, this region represents the most accessible entry point, requiring only a 5% deposit of £10,600. When conducting valuations in this region, professionals should emphasize:

- Affordability metrics relative to local wage levels

- Comparative rental yields for investment property assessments

- Future development pipeline affecting supply-demand dynamics

- Transport infrastructure improvements enhancing long-term value

The northern regions are expected to outperform southern areas in 2026, with more affordable locations in Scotland, Wales, and northern England seeing stronger price growth than London and the South East[4]. This creates opportunities for surveyors to identify value in markets where new build premiums remain modest yet growth potential is robust.

London and South East: Premium Compression

London faces divergent growth trajectories with Greater London forecast at 0-2% growth, prime central London at 0-1%, and prime outer London at 2%[3]. These modest projections reflect ongoing affordability pressures and recent tax reforms impacting the market.

For surveyors conducting commercial valuations or residential assessments in London, several factors require attention:

🏢 Flat premiums in the South East reach 28.2%, significantly higher than houses, reflecting improved specifications of purpose-built new blocks versus older converted stock[1]

📊 Unit size differentials create misleading headline comparisons, requiring price-per-square-foot normalization

🚇 Transport link proximity dramatically affects value retention in compact new build developments

💷 Stamp duty threshold changes from April 2025 fundamentally alter acquisition costs for properties above £300,000[2]

When assessing whether you need a survey on a new build, London buyers face particular challenges with space efficiency and long-term value retention that warrant professional scrutiny.

Property Type Variations

Detached properties command the highest new build prices at £498,200 (up 3.4% annually), followed by semi-detached at £332,100 (+3.8%), terraced at £298,400 (+3.4%), and flats/maisonettes at £287,600 (+2.6%)[1]. These growth rates inform surveyor expectations for 2026 valuations.

Interestingly, flats represent 32% of new build sales but carry notable regional variation in premiums[1]. Surveyors must adjust valuation approaches based on property type:

- Detached homes: Focus on land value components, garden space premiums, and privacy factors

- Semi-detached: Balance between space and affordability, emphasizing energy efficiency gains

- Terraced: Highlight urban location benefits and reduced maintenance compared to period terraces

- Flats: Scrutinize service charge projections, building quality, and long-term management structures

Market Growth Forecasts and Valuation Implications

The consensus 2026 house price growth ranges from 1.5%-4% across major forecasters, with Nationwide predicting 2-4%, Halifax 1-3%, Knight Frank 3%, Savills 2%, and Rightmove 2%[3]. The HomeOwners Alliance expects 2% growth driven by easing mortgage rates and steady wage growth[2].

Mortgage Rate Environment

Mortgage rates are expected to ease gradually through 2026, with the Bank of England's base rate projected to decline from current levels. This creates favorable conditions for buyer demand, particularly benefiting new build properties that attract first-time buyers using government schemes.

For surveyors conducting Right to Buy valuations or standard mortgage valuations, understanding rate trajectories helps assess whether current new build premiums remain sustainable. Properties priced at the upper end of local markets face greater vulnerability if rate reductions prove slower than anticipated.

Tax Changes Affecting Valuations

Stamp duty threshold changes implemented from April 1, 2025, now apply to first-time buyers at £300,000+ (previously £425,000) and home movers at £125,000+ (previously £250,000)[2]. This represents a significant cost increase that surveyors must factor into true acquisition costs.

Additionally, property income tax rises by 2% from April 2027, increasing rates to 22%, 42%, and 47% across basic, higher, and additional bands[5]. This impacts investor yield calculations and secondary market valuations for new build properties marketed to buy-to-let purchasers.

When considering what to do if your home valuation is less than an offer, these tax considerations provide legitimate grounds for valuation adjustments below asking prices, particularly for properties where premiums exceed justified tangible benefits.

Surveyor Strategies for Accurate New Build Valuations

Valuation Adjustments for New Build Premiums in 2026: Surveyor Strategies Amid 2-5% Market Growth require systematic approaches that balance developer pricing against genuine market value. Professional surveyors should implement these evidence-based strategies:

1. Comparative Market Analysis with Normalization

Standard comparative market analysis must be normalized for size, specification, and location factors. Rather than comparing headline prices, surveyors should:

✓ Calculate price-per-square-foot for all comparables

✓ Adjust for energy efficiency ratings (EPC A-rated vs. lower ratings)

✓ Account for warranty coverage periods (10-year NHBC vs. older properties)

✓ Factor in included fixtures and appliances

✓ Consider parking provision and outdoor space

This systematic approach provides defensible valuations that withstand lender scrutiny and protect client interests.

2. Tangible Benefit Quantification

Document and quantify tangible benefits using standardized calculations. For energy efficiency, surveyors can reference EPC certificates showing projected annual savings. For warranties, assign present value to coverage using standard actuarial approaches.

When conducting insurance reinstatement cost valuations, new build specifications may justify higher rebuild costs due to modern construction standards, yet this differs from market value premiums.

3. Regional Growth Adjustment

Apply regional growth forecasts to assess whether current premiums remain sustainable. Properties in northern regions with 3-4% projected growth can justify higher premiums than London properties facing 0-2% growth[3][4].

Surveyors should maintain regional databases tracking:

- Historical premium trends over 3-5 year periods

- Absorption rates for new build developments

- Resale performance of recently completed developments

- Local wage growth and affordability ratios

4. Developer Incentive Adjustment

Many new builds include developer incentives that artificially inflate headline prices. Common incentives include:

- Stamp duty contributions (typically 3-5% of purchase price)

- Part-exchange schemes at inflated valuations

- Cash-back offers or upgrade packages

- Help to Buy equity loans

Surveyors must adjust valuations to reflect true market value rather than incentivized purchase prices. A property marketed at £350,000 with £15,000 in incentives has an effective market value closer to £335,000.

5. Future Marketability Assessment

Long-term marketability considerations affect present value. Surveyors should assess:

🏗️ Development saturation: Areas with excessive new build supply face future competition

📉 Resale performance: Track how similar developments perform in secondary markets

🏘️ Community maturity: Established neighborhoods vs. new developments lacking amenities

🚗 Infrastructure delivery: Promised transport links and facilities that may not materialize

Properties in oversupplied markets or dependent on undelivered infrastructure warrant valuation discounts despite current asking prices.

Practical Application: Case Study Approach

Consider a practical valuation scenario for a two-bedroom new build flat in the South East priced at £385,000. The surveyor's analysis proceeds systematically:

Step 1: Comparable Research

- Resale two-bedroom flats: £300,000-£320,000 (average £310,000)

- New build asking price premium: 24.2%

- National average premium: 23.4%[1]

Step 2: Size Normalization

- New build: 520 sq ft (£740/sq ft)

- Resale comparables: 650 sq ft average (£477/sq ft)

- True premium on per-square-foot basis: 55.1%

Step 3: Tangible Benefit Calculation

- Energy savings (EPC A vs. C): £900/year × 10 years = £9,000 present value

- Warranty coverage: £12,000 present value

- Included appliances/fixtures: £6,000

- Total tangible benefits: £27,000

Step 4: Justified Valuation

- Resale comparable base: £310,000

- Size adjustment (520 vs 650 sq ft): -£62,000

- Adjusted resale base: £248,000

- Plus tangible benefits: +£27,000

- Justified valuation: £275,000

Step 5: Valuation Recommendation

The surveyor reports a valuation of £275,000-£290,000, substantially below the £385,000 asking price. This protects the lender from over-exposure and provides the buyer with evidence for negotiating the house price down after survey.

This systematic approach demonstrates how Valuation Adjustments for New Build Premiums in 2026: Surveyor Strategies Amid 2-5% Market Growth protect all stakeholders while maintaining professional standards.

Future-Proofing Valuation Practices

As the market evolves through 2026 and beyond, surveyors must adapt practices to emerging trends:

Technology Integration

Modern valuation practices increasingly incorporate:

- Automated valuation models (AVMs) as initial benchmarks

- Geographic information systems (GIS) for location analysis

- Energy performance databases for efficiency comparisons

- Planning portal integration for development pipeline assessment

However, technology complements rather than replaces professional judgment, particularly for new builds where unique factors require expert interpretation.

Sustainability Premiums

Environmental performance increasingly drives value, with EPC A-rated properties commanding measurable premiums. The 2026 market shows growing buyer preference for:

- Heat pump installations and renewable energy systems

- Superior insulation and airtightness standards

- Electric vehicle charging infrastructure

- Water efficiency measures

Surveyors should quantify these features' financial benefits when justifying new build premiums, referencing environmental issues in comprehensive assessments.

Regulatory Changes

Building Safety Act compliance affects new build valuations, particularly for buildings over 11 meters. Properties with robust fire safety systems, clear building control approval, and comprehensive warranties warrant premium valuations compared to those with compliance uncertainties.

When conducting valuations, surveyors should verify:

✓ Building Control completion certificates

✓ Fire safety documentation and evacuation plans

✓ Structural warranty coverage and terms

✓ Developer financial stability and track record

These factors affect both immediate marketability and long-term value retention.

Professional Development and Resources

Chartered surveyors seeking to enhance their expertise in Valuation Adjustments for New Build Premiums in 2026: Surveyor Strategies Amid 2-5% Market Growth should pursue:

📚 Continuing Professional Development (CPD): RICS offers specialized courses on new build valuation methodologies, market analysis techniques, and regulatory compliance.

🔍 Market Intelligence: Subscribe to regional property data services providing new build transaction evidence, absorption rates, and premium trend analysis.

🤝 Professional Networks: Engage with surveyor peer groups sharing insights on regional market conditions, lender requirements, and valuation challenges.

📊 Data Analytics: Develop proficiency in statistical analysis tools for comparative market analysis, regression modeling, and trend forecasting.

For those considering building surveyor roles in London or other regions, specialization in new build valuation provides competitive advantage in a growing market segment.

Conclusion

Valuation Adjustments for New Build Premiums in 2026: Surveyor Strategies Amid 2-5% Market Growth represent a critical competency for chartered surveyors navigating today's complex property market. With national new build premiums at 23.4% yet tangible benefits justifying only 15-20%, professional valuers must apply rigorous analytical frameworks to distinguish genuine value from speculative pricing[1].

The systematic strategies outlined—comparative market analysis with normalization, tangible benefit quantification, regional growth adjustment, developer incentive consideration, and future marketability assessment—provide surveyors with evidence-based approaches to protect client interests while maintaining professional standards.

As the 2026 market unfolds with projected 2-5% growth, regional variations, and evolving tax structures, surveyors who master these techniques will deliver superior value to clients, lenders, and the broader property market[2][3]. The erosion of 'hope value' discounts in recovering markets demands sophisticated valuation practices that balance developer pricing against genuine market fundamentals.

Actionable Next Steps

For surveyors seeking to implement these strategies:

- Develop regional databases tracking new build premiums, absorption rates, and resale performance in your operating areas

- Create standardized templates for tangible benefit quantification and comparative market analysis

- Establish lender relationships to understand valuation requirements and risk tolerance for new build properties

- Pursue specialized CPD in new build construction standards, energy efficiency assessment, and market forecasting

- Build developer networks to gain early insight into pipeline developments and market positioning strategies

The professionals who invest in these capabilities will lead the industry through 2026's evolving market conditions, delivering accurate valuations that serve all stakeholders effectively.

References

[1] New Build Prices Uk Regional Breakdown – https://www.new-builds.co.uk/blog/new-build-prices-uk-regional-breakdown

[2] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/

[3] The Property Market In 2026 Britains Top Experts On What You Can Expect And Its Good News All Round – https://www.countrylife.co.uk/property/the-property-market-in-2026-britains-top-experts-on-what-you-can-expect-and-its-good-news-all-round

[4] House Prices Set For A Gentle Rise In 2026 What It Means For You – https://custominsurancemortgagesolutions.co.uk/2026/01/29/house-prices-set-for-a-gentle-rise-in-2026-what-it-means-for-you/

[5] New Property Tax – https://hoa.org.uk/news/new-property-tax/