The property valuation landscape is experiencing a significant shift in 2026. With mortgage rates dropping to their lowest levels since September 2022, chartered surveyors and property professionals face a critical challenge: recalibrating valuation methodologies to accurately reflect improved market affordability. As 30-year fixed rates fall to between 5.81% and 6.04% APR[1][3], understanding valuation adjustments for 2026 mortgage rate cuts becomes essential for accurate property assessments.

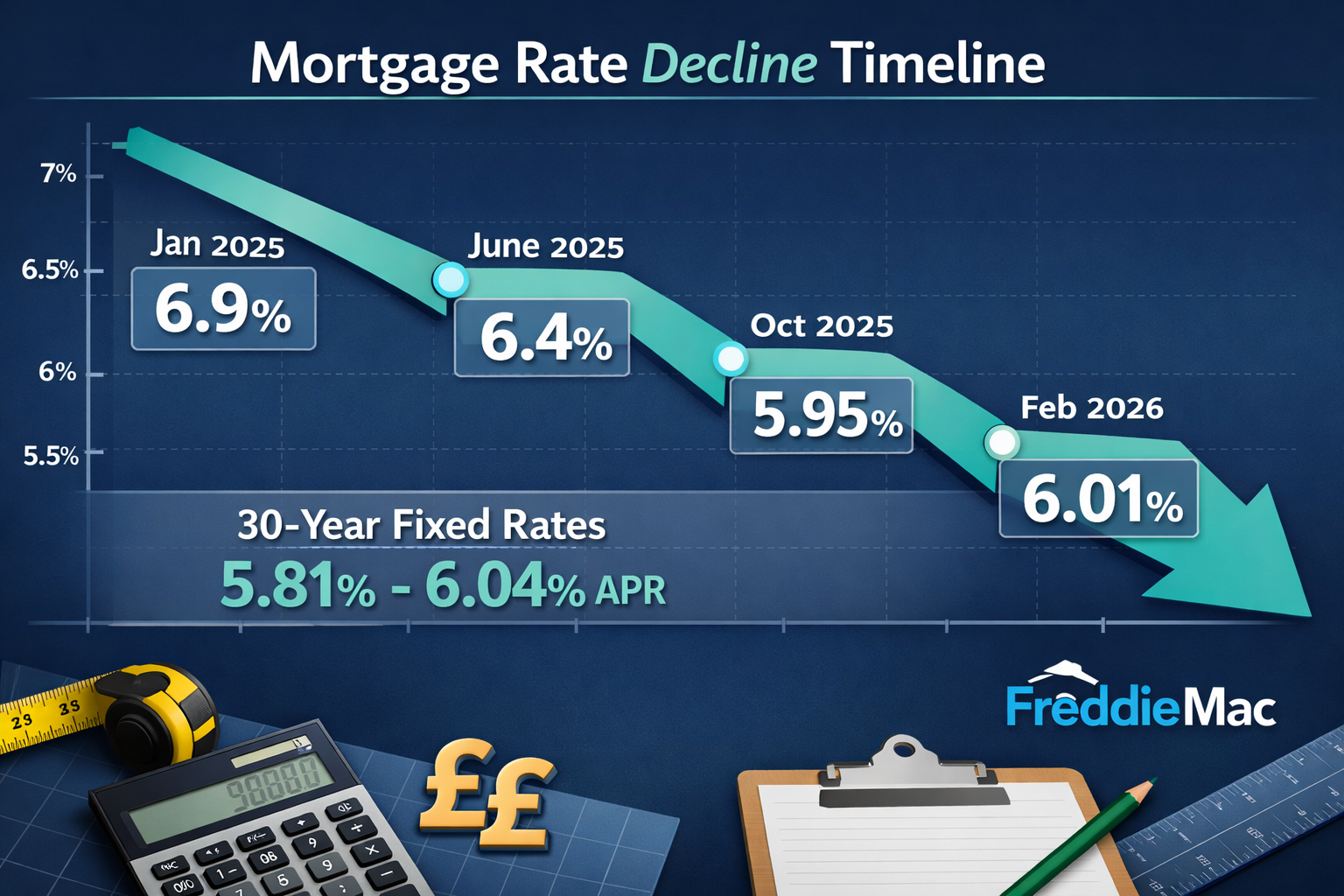

This transformation isn't merely about adjusting numbers on a spreadsheet. The decline of more than a full percentage point from early 2025 levels—when rates hovered around 6.9%[5]—has fundamentally altered buyer purchasing power and market dynamics. For property professionals, this means revisiting comparable evidence strategies, reassessing buyer pool calculations, and implementing new methodological frameworks.

Key Takeaways

✅ Mortgage rates have declined significantly to 5.81%-6.04% APR as of February 2026, the lowest since September 2022, requiring surveyors to recalibrate valuation methodologies[1][3]

✅ Expanded buyer pools mean approximately 1.42 million additional households can now afford homeownership with each 25-basis-point rate reduction[2]

✅ Comparable evidence must be time-adjusted to account for the rapidly changing interest rate environment and its impact on transaction prices

✅ Expert forecasts predict stability with rates remaining around 6% throughout 2026 and 2027, allowing for more consistent valuation frameworks[5]

✅ Refinancing opportunities are creating secondary market effects that influence property values and assessment methodologies[3]

Understanding the 2026 Mortgage Rate Environment

Current Rate Landscape and Trajectory

The mortgage rate environment in 2026 represents a dramatic shift from the previous year's elevated levels. As of February 19, 2026, Freddie Mac reported the 30-year fixed rate at 6.01%, down eight basis points from the previous week[1]. This decline continues a trend that has seen rates fall consistently throughout early 2026.

The reduction from approximately 6.9% in early 2025 to current levels below 6.1% represents more than a statistical change—it's a fundamental market transformation. For property valuations, this shift creates both opportunities and challenges:

- Increased buyer affordability expands the potential purchaser pool

- Refinancing activity creates upward pressure on comparable sales

- Market velocity accelerates as previously priced-out buyers enter the market

- Comparable evidence dating becomes more critical with rapidly changing conditions

According to Fannie Mae's February 2026 Housing Forecast, rates are predicted to remain at approximately 6% for most of 2026 and 2027[5]. This stabilization provides surveyors with a more predictable framework for forward-looking valuations, though the transition period requires careful adjustment methodologies.

Economic Drivers Behind Rate Reductions

Understanding the economic forces driving these rate cuts helps surveyors anticipate future movements and adjust property valuation methodologies accordingly. Several key factors are at play:

Federal Reserve Policy: Analysts expect at least one Federal Reserve rate cut during the first half of 2026, though stronger-than-expected labor numbers may limit multiple cuts[5]. This monetary policy stance directly influences mortgage rate trajectories.

Inflation Trends: Moderating inflation has created space for rate reductions without triggering economic overheating concerns.

Market Competition: Lender competition for market share in a recovering housing market has compressed margins, contributing to lower consumer-facing rates.

The National Association of Realtors (NAR) forecasts mortgage rates will decline from the mid-6% range of 2025 to possibly 6% in 2026[7], aligning with current observations and providing validation for valuation adjustments based on these trends.

Valuation Adjustments for 2026 Mortgage Rate Cuts: Methodology Frameworks

Recalibrating Comparable Evidence

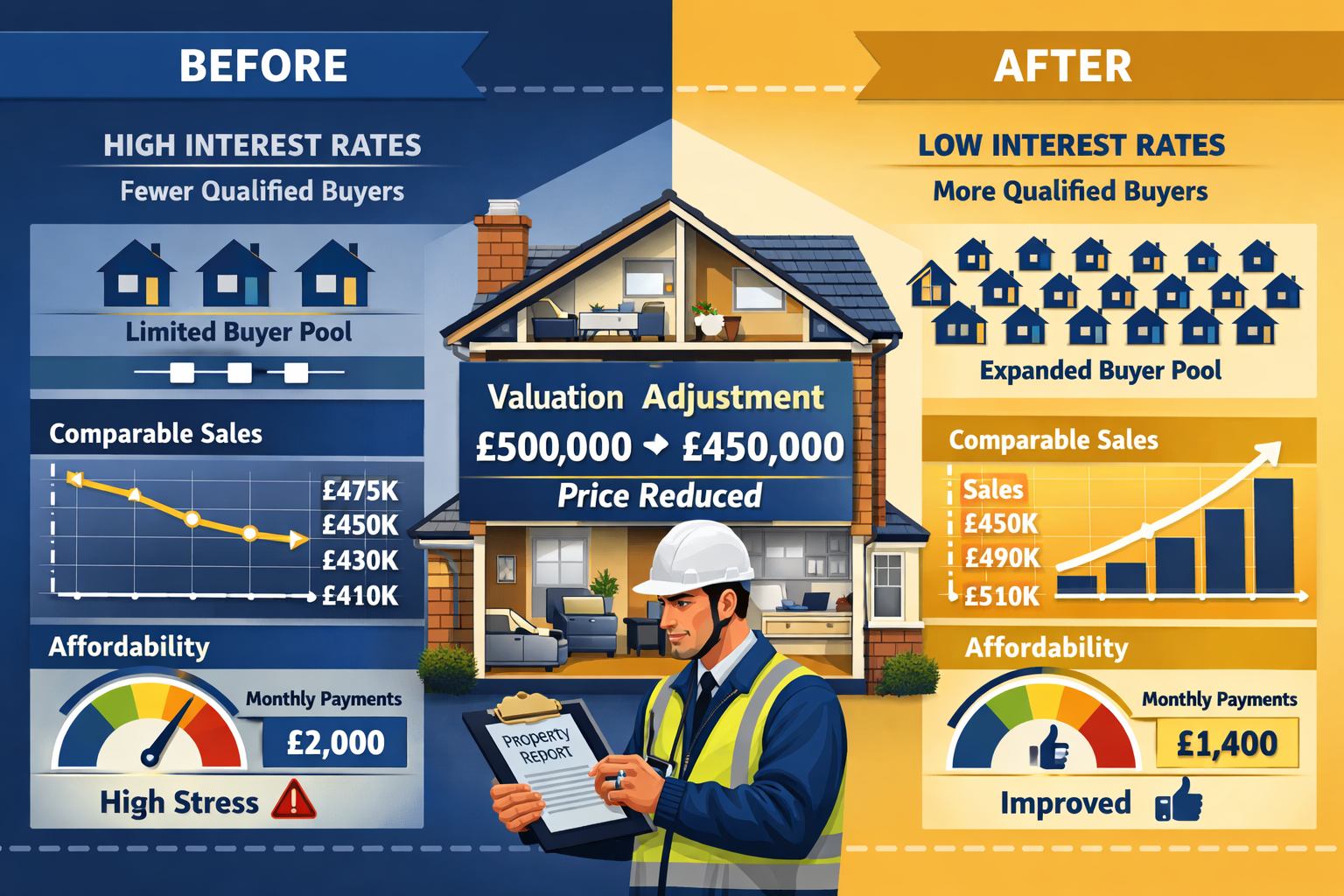

The cornerstone of property valuation—comparable sales analysis—requires significant recalibration when interest rates shift dramatically. Traditional approaches that simply adjust for time and physical characteristics no longer suffice in the current environment.

Time Adjustment Protocols must now incorporate interest rate differentials. A comparable sale from six months ago occurred in a fundamentally different financing environment. Consider this framework:

| Sale Date | Prevailing Rate | Current Rate | Required Adjustment Factor |

|---|---|---|---|

| August 2025 | 6.7% | 6.0% | +3.5% to +5.0% |

| November 2025 | 6.4% | 6.0% | +2.0% to +3.0% |

| January 2026 | 6.2% | 6.0% | +1.0% to +1.5% |

These adjustment factors reflect the enhanced affordability and expanded buyer pool created by rate reductions. The specific percentage applied depends on local market conditions, property type, and price point.

Buyer Pool Expansion Analysis

One of the most significant impacts of falling interest rates is the expansion of qualified buyers. Research indicates that at current 6% mortgage rates with a median new home price of £413,595, approximately 88.2 million households are priced out of the market[2]. However, a 25-basis-point rate cut from 6.25% to 6% would price approximately 1.42 million additional households into the market[2].

For surveyors conducting valuations, this expansion translates to:

📊 Increased demand pressure in entry-level and mid-market segments

📊 Compressed days on market as buyer competition intensifies

📊 Upward price momentum in previously stagnant markets

📊 Regional variation based on local affordability thresholds

When assessing property development opportunities, understanding these buyer pool dynamics becomes critical for accurate feasibility studies and development appraisals.

Discount Rate Adjustments for Income-Producing Properties

For commercial and investment properties valued using income capitalization approaches, falling mortgage rates necessitate corresponding adjustments to discount rates and capitalization rates.

Traditional Relationship: Capitalization rates typically maintain a spread over mortgage rates to account for risk and return expectations. As mortgage rates fall, cap rates generally follow, though with a lag and compression.

2026 Adjustment Framework:

- Review historical spread between mortgage rates and cap rates in your market

- Analyze recent investment sales to identify emerging cap rate trends

- Consider the risk-free rate environment and investor return expectations

- Apply graduated adjustments rather than immediate full recalibration

For capital gains tax valuations and investment property assessments, these discount rate adjustments can significantly impact present value calculations and therefore assessed values.

Impact on Different Property Sectors and Valuation Approaches

Residential Property Valuations

The residential sector experiences the most direct impact from mortgage rate cuts. Owner-occupied properties benefit immediately from improved affordability, while investment properties see secondary effects through rental market dynamics.

Key Valuation Considerations for Residential Properties:

🏠 First-time buyer segments experience disproportionate value increases as marginal buyers enter the market

🏠 Move-up markets see accelerated activity as existing homeowners refinance and access equity

🏠 Luxury segments show more muted responses, as cash buyers and less rate-sensitive purchasers dominate

🏠 Regional variations depend on local employment conditions and housing supply constraints

When preparing property valuations for different purposes, surveyors must consider whether the valuation reflects current market conditions or requires adjustment for anticipated rate movements.

Commercial and Investment Property Assessments

Commercial property valuations require more nuanced adjustments. The relationship between mortgage rates and commercial property values operates through multiple channels:

Direct Financing Impact: Lower rates reduce debt service costs, improving cash-on-cash returns and making acquisitions more attractive.

Indirect Economic Effects: Rate cuts often signal economic concerns, which may negatively impact tenant demand and rental growth expectations.

Cap Rate Compression: Investment yield requirements typically decline as financing costs fall, though market-specific factors create variation.

For leasehold extension and enfranchisement valuations, the deferment rate—a critical component—requires particular attention as the broader interest rate environment shifts.

Development and Land Valuations

Development appraisals are highly sensitive to interest rate changes due to the time value of money calculations inherent in residual valuation methodologies.

Residual Land Value Adjustments:

- Finance costs during construction decrease with lower rates

- Developer's profit expectations may adjust based on risk-free rate changes

- Exit values increase due to improved end-user affordability

- Development period assumptions may shorten due to improved market velocity

The combined effect typically produces significant upward pressure on development land values, particularly for residential-led schemes. Surveyors must carefully model these interactions to avoid overvaluation in markets where supply may respond to improved economics.

Comparable Evidence Strategies in a Declining Rate Environment

Selecting and Adjusting Comparable Transactions

The selection of appropriate comparable evidence becomes more complex when interest rates are falling rapidly. Traditional six-month or twelve-month lookback periods may span dramatically different financing environments.

Best Practice Framework for 2026:

1. Prioritize Recent Transactions: Weight comparables from the past 60-90 days more heavily than older sales, even if they're less physically similar.

2. Apply Rate-Based Time Adjustments: Use the methodology outlined earlier to adjust older comparables for the changed financing environment.

3. Segment by Buyer Type: Distinguish between cash transactions (less rate-sensitive) and financed purchases when analyzing comparable evidence.

4. Monitor Market Velocity: Track days on market trends as a leading indicator of rate-driven demand changes.

5. Document Assumptions Clearly: Given the transitional nature of the current market, transparent documentation of adjustment rationale is essential.

For professionals seeking guidance on property market legislation changes that may interact with these valuation adjustments, staying informed on regulatory developments remains crucial.

Regional Market Variations

Not all markets respond identically to mortgage rate cuts. Regional variations in housing supply, employment conditions, and existing affordability levels create differentiated impacts.

High-Constraint Markets (limited supply, strong employment):

- More pronounced value increases

- Faster absorption of rate-driven demand

- Greater upward pressure on comparable evidence

Balanced Markets (moderate supply, stable employment):

- Moderate value adjustments

- Steady improvement in market velocity

- Gradual comparable evidence appreciation

Oversupplied Markets (excess inventory, weaker employment):

- Muted value responses

- Rate cuts primarily reduce time on market rather than increase prices

- Comparable evidence shows stability rather than growth

Understanding these regional dynamics helps surveyors apply appropriate adjustment factors when working across different geographic markets or when preparing properties for market in specific locations.

Forward-Looking Valuation Considerations

With expert consensus suggesting rates will remain around 6% throughout 2026 and 2027[5], surveyors can adopt more stable forward-looking assumptions than during the volatile 2024-2025 period.

Scenario Planning Approaches:

📈 Base Case (75% probability): Rates stabilize at 5.75%-6.25% through 2027

📈 Optimistic Case (15% probability): Further cuts to 5.25%-5.75% if economic conditions weaken

📈 Pessimistic Case (10% probability): Rates rise back to 6.5%-7.0% if inflation resurges

For most valuation purposes, the base case provides the appropriate foundation, with sensitivity analysis exploring the range of outcomes for significant decisions like property investment strategies.

Practical Implementation for Surveyors and Valuers

Updating Valuation Models and Templates

Professional practice requires systematic updates to valuation models, templates, and assumption sets to reflect the 2026 rate environment.

Critical Updates Checklist:

✔️ Discount rate assumptions for DCF models (reduce by 50-75 basis points from 2025 levels)

✔️ Capitalization rate databases (review and update based on recent investment sales)

✔️ Comparable adjustment factors (implement rate-differential time adjustments)

✔️ Affordability calculations (update using current 6.0% rate assumptions)

✔️ Finance cost assumptions (for development appraisals, reduce from 7-8% to 6-7%)

✔️ Market commentary templates (incorporate discussion of rate environment impacts)

These updates ensure consistency across valuation assignments and provide defensible methodologies for client discussions and potential challenges.

Client Communication and Expectation Management

The changing rate environment creates both opportunities and challenges for client relationships. Clear communication about how rate cuts impact valuations prevents misunderstandings and manages expectations.

Key Discussion Points:

💡 Timing considerations: Values are rising due to rate cuts, but the pace and magnitude vary by property type and location

💡 Comparable evidence limitations: Recent transactions may not fully reflect current conditions in fast-moving markets

💡 Refinancing implications: For existing owners, explaining how rate cuts create refinancing opportunities adds value

💡 Future outlook: Sharing expert forecasts about rate stability helps clients make informed decisions

💡 Valuation purpose alignment: Different valuation purposes may require different treatment of rate environment factors

For clients navigating complex situations like estate settlements, explaining how current market conditions affect property values becomes particularly important.

Professional Standards and Compliance

RICS Red Book and other professional standards require valuers to reflect current market conditions accurately. The 2026 rate environment creates specific compliance considerations.

Red Book Compliance in Changing Markets:

Market Conditions Commentary: VPS 3 requires adequate description of market conditions, which must now address the rate environment and its impacts.

Assumptions and Special Assumptions: When valuing in transitional markets, clearly state assumptions about rate stability and market trajectory.

Comparable Evidence: Ensure comparables are appropriately adjusted and that any limitations are disclosed.

Valuation Uncertainty: Consider whether current market conditions warrant an explicit uncertainty statement.

Departure from Standards: In exceptional cases where standard approaches don't adequately capture rate-driven value changes, document any departures clearly.

Maintaining rigorous professional standards while adapting to changing market conditions protects both clients and professional reputation.

Refinancing Wave and Secondary Market Effects

Impact of Refinancing Activity on Property Values

The decline in mortgage rates to 5.81%-6.04% has triggered significant refinancing activity. Experts suggest refinancing could make sense if current rates are 0.5-0.75 percentage points lower than an existing mortgage rate[3].

This refinancing wave creates several secondary effects relevant to property valuations:

Increased Equity Access: Homeowners refinancing can access accumulated equity, potentially funding improvements that increase property values.

Reduced Financial Stress: Lower monthly payments improve household financial stability, reducing distressed sale inventory.

Market Confidence: Active refinancing signals market health and confidence, supporting price stability.

Renovation Activity: Equity withdrawal often funds property renovations, improving local housing stock quality.

For surveyors, understanding these dynamics helps explain market trends that might otherwise appear anomalous in comparable evidence analysis.

Cash-Out Refinancing and Home Improvement Impacts

When homeowners refinance at lower rates while extracting equity, property values can experience upward pressure through two mechanisms:

- Direct improvements funded by cash-out proceeds

- Neighborhood effects as multiple properties undergo enhancement

Valuers should monitor local building permit activity and renovation trends as indicators of this dynamic, particularly in established neighborhoods where refinancing activity concentrates among long-term owners with substantial equity positions.

Expert Forecasts and Long-Term Valuation Planning

Industry Predictions for Rate Trajectory

Understanding expert forecasts helps surveyors develop appropriate long-term valuation assumptions and advise clients on market timing.

Consensus View for 2026-2027:

- Rates stabilize around 6.0% for 30-year fixed mortgages[5][7]

- Limited further declines expected absent economic deterioration

- Federal Reserve likely to implement modest cuts but not aggressive easing[5]

- Market expects gradual normalization rather than return to ultra-low rates

This consensus supports valuation approaches that assume relative stability rather than continued dramatic rate declines.

Preparing for Potential Rate Volatility

While the base case assumes stability, prudent valuation practice requires considering alternative scenarios:

Upside Risk (rates rise): Inflation resurgence could push rates back toward 7%, reversing recent value gains.

Downside Risk (rates fall further): Economic weakness could drive rates below 5.5%, accelerating value appreciation.

For significant valuation assignments—particularly development feasibility studies or long-term investment decisions—sensitivity analysis exploring these scenarios provides valuable decision-making context.

Integration with Broader Market Analysis

Valuation adjustments for 2026 mortgage rate cuts don't occur in isolation. Successful valuation practice integrates rate considerations with:

- Supply and demand fundamentals in local markets

- Employment and income trends affecting buyer capacity

- Planning and regulatory changes impacting development activity

- Demographic shifts influencing housing preferences

- Economic conditions beyond interest rates alone

This holistic approach ensures valuations reflect the full complexity of market dynamics rather than over-emphasizing a single factor, even one as significant as mortgage rates.

Conclusion

The valuation adjustments required for 2026 mortgage rate cuts represent both a challenge and an opportunity for property professionals. With rates declining to 5.81%-6.04% APR—the lowest since September 2022—surveyors must recalibrate methodologies to accurately reflect improved affordability and expanded buyer pools[1][3].

The evidence is clear: each 25-basis-point rate reduction prices approximately 1.42 million additional households into the market[2], fundamentally altering demand dynamics and comparable evidence. Professional valuers who systematically adjust their approaches—updating discount rates, recalibrating comparable evidence with rate-differential time adjustments, and clearly communicating assumptions—will provide the most accurate and defensible valuations in this evolving environment.

Actionable Next Steps

For property professionals navigating valuation adjustments for 2026 mortgage rate cuts:

1. Update Your Models: Review and adjust discount rates, cap rates, and comparable adjustment factors to reflect current market conditions.

2. Enhance Documentation: Clearly explain rate environment impacts in valuation reports and client communications.

3. Monitor Market Data: Track days on market, transaction volumes, and investment sales to identify emerging trends.

4. Segment Your Analysis: Recognize that different property types, price points, and regions respond differently to rate changes.

5. Maintain Professional Standards: Ensure all adjustments comply with RICS Red Book and other applicable professional standards.

6. Seek Expert Guidance: For complex assignments or unfamiliar property types, consider consulting with specialists who can provide professional valuation services tailored to current market conditions.

The stabilization of rates around 6% throughout 2026 and 2027[5] provides a more predictable framework than recent years, but the transition period requires careful methodology adjustments and clear professional judgment. By implementing the frameworks outlined in this article, surveyors can deliver accurate, defensible valuations that serve their clients' needs while maintaining the highest professional standards.

References

[1] Mortgage Rates Today February 25 2026 – https://themortgagereports.com/mortgage-rates-now/mortgage-rates-today-february-25-2026

[2] Pricing In One Point Four Two Million Households – https://www.nahb.org/news-and-economics/housing-economics-plus/special-studies/special-studies-pages/pricing-in-one-point-four-two-million-households

[3] Mortgage Rates Today Friday February 27 2026 – https://www.nerdwallet.com/mortgages/news/mortgage-rates-today-friday-february-27-2026

[4] Times Mortgage Interest Rates Could Fall March 2026 – https://www.cbsnews.com/news/times-mortgage-interest-rates-could-fall-march-2026/

[5] Mortgage Rates February 25 2026 – https://www.bankrate.com/mortgages/analysis/mortgage-rates-february-25-2026/

[6] Current Refi Mortgage Rates 02 26 2026 – https://fortune.com/article/current-refi-mortgage-rates-02-26-2026/

[7] Mortgage Rates Forecast For 2026 Experts Predict Whether Rates Will Keep Dropping – https://www.firstcbt.bank/blog/post/mortgage-rates-forecast-for-2026-experts-predict-whether-rates-will-keep-dropping