The property market across the United Kingdom tells two distinctly different stories in 2026. While much of the nation experiences stabilisation and cautious recovery, Northern Ireland has emerged as an unexpected powerhouse, demonstrating remarkable price leadership that challenges conventional valuation methodologies. The phenomenon of Valuation Accuracy in Northern Ireland's 2026 Price Leadership: RICS Adjustments Outpacing National Stabilisation represents more than statistical curiosity—it signals a fundamental shift requiring chartered surveyors to refine their approaches, defend optimistic assessments with robust evidence, and navigate unprecedented regional divergence.

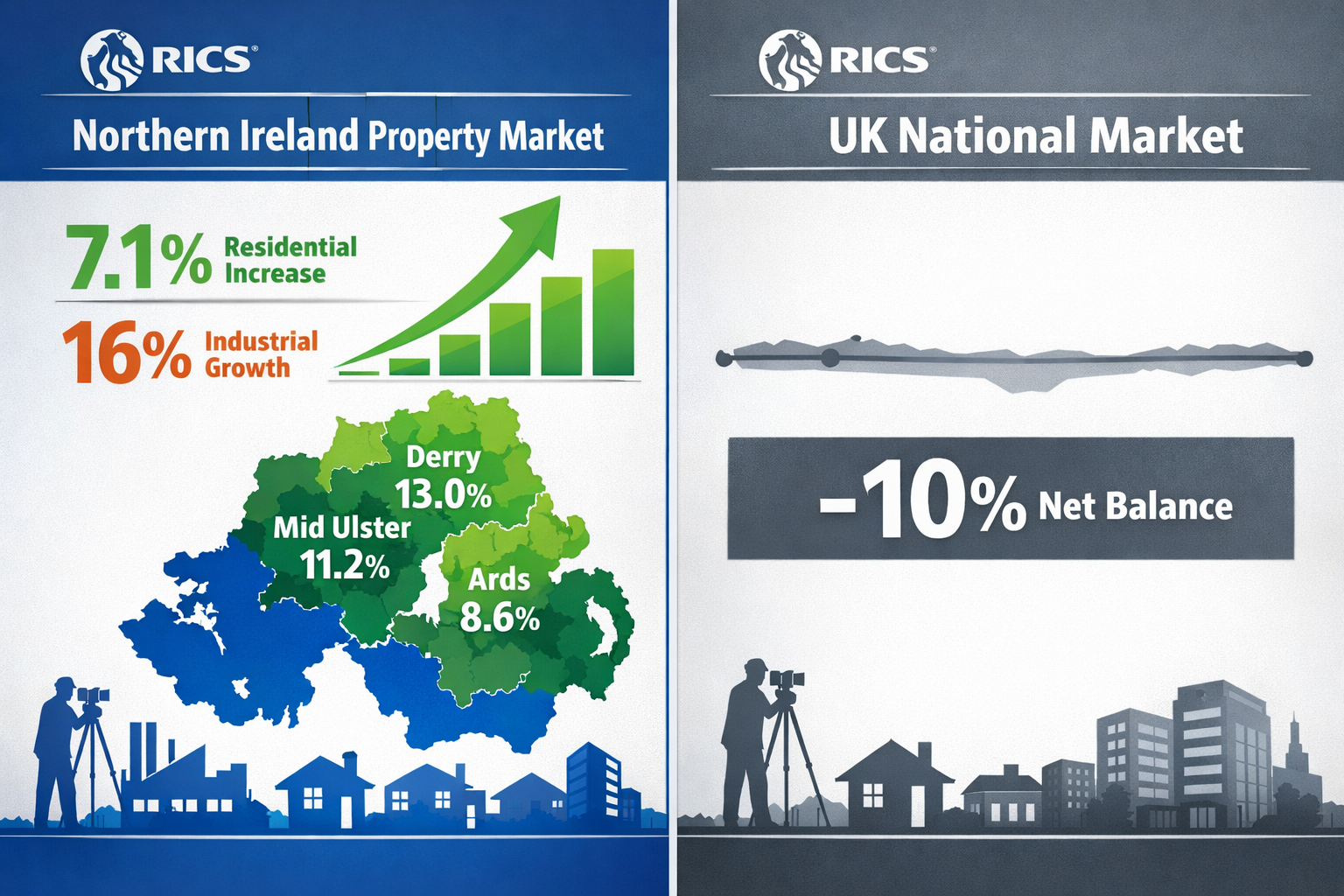

As the Land Property Services published its draft valuation list for Reval 2026, the numbers revealed a striking reality: overall non-domestic valuations increased by 15% across Northern Ireland's property sectors, while residential values climbed 7.1% year-on-year.[1][2] These figures stand in sharp contrast to the broader UK market, where the national house price net balance improved to just -10% in early 2026, up from -19% in October 2025.[5] For property professionals, this divergence creates both opportunity and challenge—particularly when defending valuations that appear optimistic against national benchmarks but accurately reflect local market conditions.

Key Takeaways

🔑 Northern Ireland leads UK regional growth with residential values increasing 7.1% year-on-year and non-domestic valuations rising 15% overall, significantly outpacing national stabilisation trends.

📊 Sectoral divergence demands precision: Industrial and warehousing properties experienced the strongest growth at 16%, while office and retail sectors showed more moderate 9% increases, requiring sector-specific valuation approaches.

🗺️ Regional concentration within Northern Ireland: Derry City and Strabane led with 13.0% growth, followed by Mid Ulster at 11.2%, demonstrating that even within high-performing regions, location-specific analysis remains critical.

⚖️ RICS methodology adjustments essential: Approximately 67% of properties saw valuations at or below the 15% average, indicating significant individual variance that demands robust comparable evidence and quality-based differentiation.

💼 Mortgage market support strengthens valuations: Five-year fixed rates at 3.95% and 7,158 mortgage product options provide fundamental support for optimistic assessments when properly documented.

Understanding Northern Ireland's 2026 Market Position

The Regional Performance Gap

Northern Ireland's property market performance in 2026 represents a remarkable departure from historical patterns. Traditionally viewed as following rather than leading UK property trends, the region now stands among the strongest performers nationally. RICS identified Scotland and Northern Ireland in January 2026 as demonstrating the strongest price growth across the UK, contrasting sharply with London and the South East, which continue to lag behind.[3]

This shift reflects multiple converging factors:

- Post-pandemic economic rebalancing favouring regions with lower initial property values

- Strong rental demand with net +28% of RICS respondents expecting rental price increases in the near term, up from +16% previously[2]

- Limited modern supply in key sectors, particularly industrial and warehousing properties

- Improved mortgage accessibility with product choice reaching levels not seen since October 2007[2]

For chartered surveyors conducting property valuations, these macroeconomic factors provide essential context when defending assessments that may appear aggressive when compared against national benchmarks but accurately reflect local market dynamics.

Sectoral Performance Breakdown

The Valuation Accuracy in Northern Ireland's 2026 Price Leadership becomes particularly evident when examining individual property sectors. The Reval 2026 draft valuation list reveals significant sectoral variation:[1]

| Property Sector | Valuation Increase | Key Drivers |

|---|---|---|

| Industrial & Warehousing | 16% | Strong demand, limited modern supply, e-commerce growth |

| Residential | 7.1% (year-on-year) | Mortgage accessibility, rental demand, regional concentration |

| Office (Overall) | 9% | Grade A Belfast properties leading, quality-based divergence |

| Retail | 9% | Belfast strength, high street variance, independent retailers stable |

| Hospitality | Wide variance | Post-pandemic recovery asymmetry, expansion-driven increases |

This sectoral breakdown demonstrates why blanket valuation approaches fail in the current Northern Ireland market. A Grade A office in Belfast's central business district operates in a fundamentally different valuation environment than a provincial retail unit, despite both experiencing nominal increases in the Reval 2026 process.

Geographic Concentration Within Northern Ireland

Even within Northern Ireland's strong overall performance, geographic concentration creates valuation complexity. Regional price growth disparity shows:[2]

- Derry City and Strabane: 13.0% growth (leading region)

- Mid Ulster: 11.2% growth

- Ards and North Down: 8.6% growth

- Other regions: Varying performance below these leaders

This geographic variance means that surveyors cannot simply apply Northern Ireland's headline figures to individual properties. Understanding how to negotiate house prices requires granular knowledge of sub-regional market conditions, infrastructure developments, and local economic factors driving specific area performance.

RICS Adjustments and Valuation Methodology for Northern Ireland's 2026 Price Leadership

The Comparable Evidence Challenge

The core challenge in achieving Valuation Accuracy in Northern Ireland's 2026 Price Leadership lies in selecting and adjusting comparable evidence. With approximately 67% of Northern Ireland properties receiving valuations at or below the 15% average increase,[1] individual property assessment demands sophisticated analysis beyond simple market averages.

RICS-qualified surveyors must navigate several methodological complexities:

Temporal adjustments: The Reval 2026 valuations use April 2024 as the rental evidence baseline,[1] requiring careful consideration of market movements between the valuation date and current assessment dates. Given the 7.1% year-on-year residential growth rate,[2] temporal adjustments can significantly impact final valuations.

Quality stratification: The 9% increase in office values masks substantial divergence, with Grade A Belfast offices experiencing stronger growth than secondary provincial properties.[1] Surveyors must carefully stratify comparables by quality grade, location, and specification rather than relying on sectoral averages.

Sector-specific factors: The 16% increase in industrial and warehousing valuations[1] reflects specific supply-demand dynamics in that sector. Applying these growth rates to other property types would produce inaccurate assessments. Each sector requires dedicated comparable analysis with sector-appropriate adjustments.

Micro-location premiums: With Derry City and Strabane showing 13.0% growth while other regions lag,[2] micro-location adjustments become critical. Properties in high-performing localities may justify valuations significantly above regional averages when supported by appropriate comparable evidence.

Defending Optimistic Assessments

When conducting independent property valuations, surveyors frequently encounter scepticism regarding Northern Ireland's strong performance relative to national trends. Defending optimistic assessments requires systematic evidence presentation:

1. Establish Regional Context

Begin by documenting Northern Ireland's position as a RICS-identified strong performer alongside Scotland,[3] distinguishing the region from underperforming areas like London and the South East. This contextual framing prevents inappropriate comparisons with national stabilisation trends.

2. Present Sectoral Evidence

Provide detailed sectoral performance data from Reval 2026,[1] demonstrating that the subject property's valuation aligns with documented sectoral trends rather than representing an outlier assessment. For industrial properties, the 16% sectoral increase provides strong support for valuations that might otherwise appear aggressive.

3. Document Comparable Transactions

Assemble a robust set of comparable transactions from the April 2024 baseline period forward, with detailed adjustments for:

- Location quality and accessibility

- Property condition and specification

- Lease terms and tenant covenant strength

- Market timing between comparable and subject property

4. Incorporate Mortgage Market Data

Reference the 3.95% five-year fixed mortgage rates and 7,158 available mortgage products[2] as fundamental support for residential valuations. This mortgage accessibility directly impacts buyer demand and sustainable price levels, providing objective market evidence beyond comparable transactions alone.

5. Address Variance Explicitly

Acknowledge that 67% of properties received at or below average increases,[1] then explain specifically why the subject property justifies above-average valuation based on quality, location, or sector-specific factors. This transparency strengthens credibility rather than undermining the assessment.

Quality-Based Valuation Differentiation

The RICS Adjustments Outpacing National Stabilisation in Northern Ireland demand particular attention to quality-based differentiation. The 9% average increase in office values[1] encompasses a wide range of individual outcomes:

Grade A Belfast offices experienced the strongest growth, driven by:

- Limited new supply in prime locations

- Corporate occupier demand for modern specifications

- ESG compliance and energy efficiency premiums

- Hybrid working accommodation with enhanced amenities

Secondary provincial offices showed more modest increases, reflecting:

- Reduced demand for older, less efficient buildings

- Hybrid working reducing space requirements

- Competition from newer business park developments

- Higher vacancy rates in some locations

Surveyors must therefore apply quality-specific adjustments when using comparables across different property grades. A simple percentage adjustment proves insufficient; detailed analysis of specification differences, location quality, and market positioning becomes essential for accurate assessment.

Rental Evidence and Net Annual Value Calculations

The Reval 2026 process bases valuations on rental evidence from April 2024,[1] creating specific methodological requirements for surveyors working with these valuations. Understanding Net Annual Value (NAV) calculations and their relationship to market rents provides essential context:

NAV represents the estimated annual rental value a property might reasonably be expected to achieve if let on the open market. For many independent high street retailers, NAVs remained unchanged in Reval 2026,[1] despite overall retail sector increases of 9%. This variance reflects:

- Declining footfall in some high street locations

- Shift toward online retail reducing physical space demand

- Contrast with stronger performance in Belfast retail core

- Individual property circumstances overriding sectoral trends

When conducting valuations for inheritance tax purposes or capital gains calculations, surveyors must carefully distinguish between NAV-based rating valuations and market value assessments, while recognising that both should reflect similar underlying rental evidence when properly calibrated.

Strategic Approaches for Surveyors in Northern Ireland's Divergent Market

Developing Robust Comparable Databases

Achieving consistent Valuation Accuracy in Northern Ireland's 2026 Price Leadership requires surveyors to maintain comprehensive comparable databases that capture the region's market complexity. Unlike more stable markets where recent comparables provide reliable guidance, Northern Ireland's rapid growth and sectoral divergence demand more sophisticated data management:

Geographic segmentation: Maintain separate comparable sets for each of Northern Ireland's local government districts, with particular attention to high-growth areas like Derry City and Strabane (13.0% growth) and Mid Ulster (11.2% growth).[2] This segmentation enables precise location adjustments rather than relying on regional averages.

Temporal tracking: Record not just transaction prices but transaction dates, enabling accurate temporal adjustments. With year-on-year growth of 7.1% in residential properties,[2] a comparable from 12 months prior requires significant adjustment to reflect current market conditions.

Quality coding: Implement systematic quality grading for all comparables, distinguishing between Grade A, Grade B, and secondary properties. The divergent performance between Grade A Belfast offices and provincial properties[1] demonstrates why quality coding proves essential for accurate adjustments.

Sectoral specialisation: Develop deep expertise in specific sectors rather than attempting comprehensive coverage. The 16% industrial growth versus 9% office and retail growth[1] shows that sectoral specialists can provide more accurate valuations than generalists applying broad market trends.

Communicating Regional Outperformance to Clients

When valuations reflect Northern Ireland's strong performance, clients—particularly those familiar with national stabilisation narratives—may question assessments that appear optimistic. Effective communication strategies include:

Visual comparison presentations: Create charts showing Northern Ireland's performance versus national trends, using RICS data[3] to demonstrate the region's position as a documented strong performer rather than an anomaly.

Sectoral context: Explain how the subject property's sector performed within Reval 2026,[1] providing objective third-party validation for growth assumptions. Clients more readily accept valuations aligned with published governmental revaluation data.

Mortgage market fundamentals: Reference the 3.95% five-year fixed rates and 7,158 mortgage products[2] as concrete evidence supporting residential valuations. These tangible market indicators provide reassurance that valuations reflect sustainable buyer demand rather than speculative pricing.

Rental demand indicators: Cite the +28% net balance of RICS respondents expecting rental increases[2] as fundamental support for both residential and commercial valuations. Strong rental markets underpin capital values across property sectors.

Handling Valuation Challenges and Appeals

The significant variance in individual property outcomes within Reval 2026—with 67% receiving at or below average increases[1]—inevitably generates valuation challenges and appeals. Surveyors must prepare systematic responses:

Document methodology comprehensively: Maintain detailed working papers showing comparable selection, adjustment factors, and reasoning. When conducting RICS building surveys, this documentation proves essential if valuations face subsequent challenge.

Prepare alternative valuation scenarios: Develop sensitivity analyses showing how valuations change under different assumptions. This demonstrates that the preferred valuation represents a reasoned judgment within a defensible range rather than an arbitrary figure.

Engage with rating authorities: For non-domestic properties affected by Reval 2026, understand the Land Property Services appeal process and timelines. The draft valuation list publication triggers specific appeal windows that clients must observe.

Maintain professional indemnity coverage: Ensure professional indemnity insurance adequately covers work in Northern Ireland's rapidly appreciating market, where valuation quantum increases proportionally with property values.

Sector-Specific Valuation Strategies

The RICS Adjustments Outpacing National Stabilisation require tailored approaches for different property sectors:

Industrial and Warehousing (16% Growth)

The strongest-performing sector in Reval 2026[1] demands particular attention to:

-

Supply constraints: Limited modern industrial stock drives premium valuations for well-specified properties. Surveyors should document supply limitations in specific locations to justify above-average assessments.

-

E-commerce impact: Properties with good access to transport networks and urban populations command premiums reflecting their suitability for last-mile logistics. Location-specific factors outweigh general sectoral trends.

-

Specification quality: Modern industrial units with enhanced eaves heights, loading facilities, and yard space significantly outperform older stock. Quality-based adjustments prove more significant than in other sectors.

Office Properties (9% Growth with Quality Divergence)

Office valuations require careful quality stratification:

-

Grade A Belfast core: These properties justify valuations at the upper end of the 9% average increase,[1] supported by limited supply and corporate occupier demand. Comparables should draw exclusively from similar quality properties.

-

Provincial secondary offices: More conservative valuations reflecting reduced demand for older buildings. Surveyors should acknowledge hybrid working impacts while recognising that quality properties maintain value better than market averages suggest.

-

ESG and efficiency premiums: Modern, energy-efficient offices command increasing premiums as occupiers prioritise ESG compliance. These premiums deserve explicit quantification in valuation reports.

Retail Properties (9% Growth with Geographic Variance)

Retail valuations demand geographic precision:

-

Belfast retail core: Stronger performance justifies valuations toward the upper end of sectoral increases, particularly for prime pitch locations with strong footfall.

-

Independent high street retailers: Many saw no NAV change in Reval 2026,[1] reflecting challenging trading conditions. Surveyors should carefully assess individual circumstances rather than applying sectoral averages.

-

Out-of-town retail: Performance varies significantly based on catchment, accessibility, and tenant mix. Location-specific analysis proves more valuable than sectoral trends.

Residential Properties (7.1% Year-on-Year Growth)

Residential valuations benefit from:

-

Mortgage market support: The 3.95% five-year fixed rates and 7,158 product options[2] provide objective market support for valuations that might otherwise appear optimistic.

-

Regional concentration: Properties in Derry City and Strabane (13.0% growth), Mid Ulster (11.2%), and Ards and North Down (8.6%)[2] justify valuations significantly above Northern Ireland averages when supported by local comparable evidence.

-

Rental demand fundamentals: The +28% net balance expecting rental increases[2] supports both investment property valuations and owner-occupied assessments by demonstrating underlying market strength.

Integrating Reval 2026 Data into Valuation Practice

The Land Property Services Reval 2026 draft valuation list[1] provides surveyors with valuable market intelligence that extends beyond rating purposes:

Benchmark validation: Compare subject property valuations against Reval 2026 outcomes for similar properties. Significant divergence requires explanation and additional supporting evidence.

Sectoral trend confirmation: Use published sectoral increases (16% industrial, 9% office and retail)[1] to validate that individual valuations align with documented market trends rather than representing outlier assessments.

Geographic pattern analysis: The Reval 2026 data reveals geographic patterns within Northern Ireland that may not be evident from transaction data alone. This intelligence informs location adjustments and comparable selection.

Quality differentiation evidence: The wide variance in individual outcomes—with 67% at or below average increases[1]—provides objective evidence supporting quality-based valuation differentiation. This variance legitimises above-average valuations for superior properties when properly documented.

Future-Proofing Valuation Approaches

While Northern Ireland demonstrates strong performance in 2026, surveyors must also consider sustainability and potential market shifts:

Monitor national recovery progression: The national house price net balance improved to -10% in early 2026 from -19% in October 2025.[5] If national recovery accelerates, Northern Ireland's relative outperformance may moderate. Valuations should reflect current conditions while acknowledging potential convergence.

Track mortgage market evolution: The 3.95% five-year fixed rates[2] represent historically attractive financing. Any significant rate increases would impact sustainable price levels, particularly for residential properties where mortgage accessibility drives demand.

Assess rental market sustainability: The +28% net balance expecting rental increases[2] supports current valuations but requires ongoing monitoring. Rental market weakening would undermine fundamental support for both residential and commercial property values.

Consider supply response: Strong valuations incentivise new development. Increased supply in industrial (currently showing 16% growth)[1] or other sectors could moderate future growth rates. Surveyors should monitor planning approvals and development pipelines in their specialised sectors.

Conclusion

The phenomenon of Valuation Accuracy in Northern Ireland's 2026 Price Leadership: RICS Adjustments Outpacing National Stabilisation represents both opportunity and challenge for property professionals. With residential values increasing 7.1% year-on-year, non-domestic valuations rising 15% overall, and industrial properties experiencing 16% growth,[1][2] Northern Ireland has emerged as a clear regional leader while much of the UK experiences stabilisation rather than growth.

For chartered surveyors, this divergence demands methodological precision and robust evidence presentation. The wide variance in individual property outcomes—with 67% receiving at or below average increases[1]—demonstrates that headline figures provide only initial context. Accurate valuation requires:

✅ Sector-specific analysis recognising that industrial (16%), office (9%), and retail (9%) properties operate in distinct market conditions

✅ Geographic precision acknowledging that Derry City and Strabane (13.0% growth), Mid Ulster (11.2%), and other regions show concentrated strength

✅ Quality-based differentiation particularly for office properties where Grade A Belfast assets significantly outperform secondary provincial properties

✅ Robust comparable evidence with detailed adjustments for location, quality, timing, and sector-specific factors

✅ Mortgage market fundamentals including 3.95% five-year fixed rates and 7,158 product options supporting residential valuations

The strategic imperative for surveyors working in Northern Ireland's market centres on defending optimistic assessments with systematic evidence while maintaining professional scepticism about individual property circumstances. Not every property participates equally in regional growth, and quality analysis distinguishes accurate valuations from simplistic application of market averages.

Actionable Next Steps

For surveyors conducting valuations in Northern Ireland:

- Develop comprehensive comparable databases with geographic, sectoral, and quality segmentation reflecting the market's complexity

- Engage with Reval 2026 data as validation and market intelligence beyond its rating purposes

- Prepare systematic defence documentation for valuations that appear optimistic against national trends but accurately reflect local conditions

- Specialise in specific sectors where the divergence between industrial (16%), office (9%), and other property types demands deep expertise

- Monitor mortgage market conditions and rental demand indicators that provide fundamental support for current valuation levels

For property owners and investors:

- Obtain professional valuations from RICS-qualified surveyors with specific Northern Ireland market expertise

- Understand regional variance within Northern Ireland, recognising that location-specific factors significantly impact individual property values

- Consider timing carefully given Northern Ireland's strong current performance and potential for future convergence with national trends

- Review existing valuations for inheritance tax, capital gains, or pension purposes to ensure they reflect 2026 market conditions

Northern Ireland's 2026 price leadership demonstrates that regional property markets increasingly diverge from national trends, requiring surveyors to maintain sophisticated analytical capabilities and resist oversimplified valuation approaches. Those who master the complexity will deliver accurate assessments that serve clients effectively while maintaining professional standards in a rapidly evolving market environment.

References

[1] Land Property Services Publishes Draft Valuation List Reval 2026 – https://www.finance-ni.gov.uk/news/land-property-services-publishes-draft-valuation-list-reval-2026

[2] Article – https://www.alexanderjacob.co.uk/blog/article.html?id=1772635696

[3] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[5] Regional Valuation Divergences In 2026 Recovery Rics Tactics For North South Price Shifts In Building Surveys – https://nottinghillsurveyors.com/blog/regional-valuation-divergences-in-2026-recovery-rics-tactics-for-north-south-price-shifts-in-building-surveys