The London and South East property markets are experiencing a crisis of confidence. While national headlines celebrate stabilizing house prices across the UK in early 2026, chartered surveyors working in these high-cost regions face a starkly different reality. The latest RICS Q1 2026 data reveals that London and South East markets continue to lag behind the national recovery, with persistent affordability constraints creating unique valuation challenges that demand specialized surveyor strategies.

This comprehensive analysis examines the Surveyor Strategies for Navigating Affordability Crises in London and South East Markets: RICS Q1 2026 Data, providing property professionals with actionable insights to accurately assess properties in these constrained markets where apparent price stabilization masks deeper regional disparities.

Key Takeaways

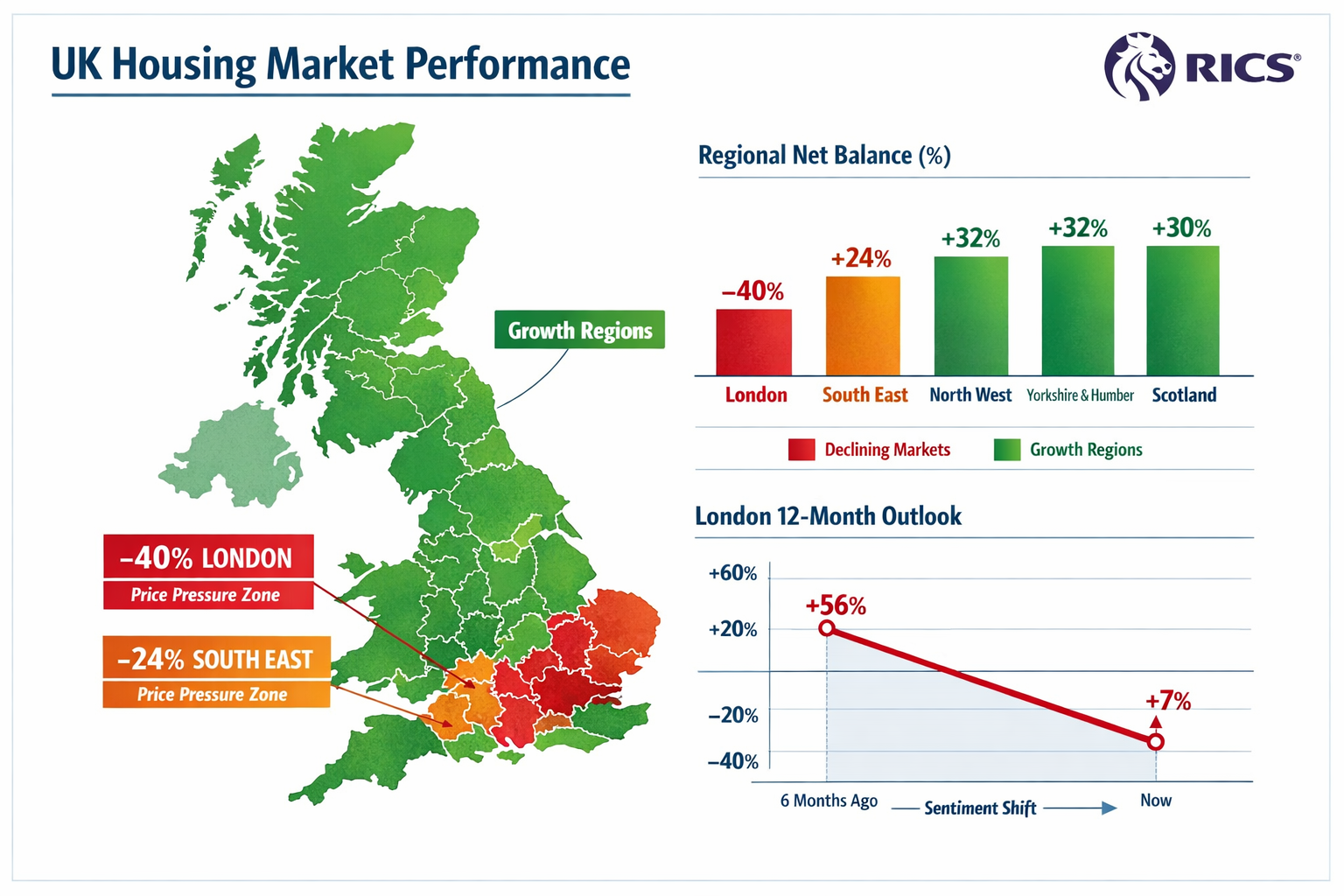

- London price expectations collapsed from +56% to +7% in just one month (January to February 2026), signaling a dramatic loss of confidence in the capital's property market recovery[3][4]

- Regional inequality intensifies: London reports -40% net balance for price expectations, South East at -24%, while northern regions experience rising prices, creating stark geographic divergence[3][4]

- Affordability pressures persist despite national stabilization: High-cost regions face continued downward price pressure while the national picture appears more optimistic[1]

- Rental market crisis deepens: Tenant demand fell to weakest levels since April 2020, while landlord supply remains constrained, creating affordability barriers across residential and commercial sectors[2]

- Surveyors require specialized valuation techniques to navigate these complex regional dynamics and provide accurate assessments in markets experiencing simultaneous stabilization and decline

Understanding the Regional Divide: RICS Q1 2026 Market Snapshot

The first quarter of 2026 has exposed a fundamental truth about the UK property market: national averages conceal critical regional realities. For chartered surveyors operating in London and the South East, understanding these geographic disparities is essential for accurate property valuation and client advisory services.

The London Confidence Collapse

The most striking revelation from the RICS Q1 2026 data concerns London's dramatic sentiment reversal. Price expectations for the capital over the next 12 months plummeted from +56% in January to just +7% in February—a 49-percentage-point collapse that represents one of the sharpest monthly declines on record[3][4].

This isn't merely statistical noise. The data reflects genuine market anxiety among surveyors and property professionals who work daily in London's residential and commercial sectors. When professionals who understand market fundamentals lose confidence this rapidly, it signals deeper structural challenges beyond typical seasonal fluctuations.

South East and East Anglia: The Affordability Pressure Zone

London's challenges extend throughout its surrounding regions. The South East reports a net balance of -24% for near-term price expectations, while East Anglia registers -26%—both significantly more negative than the national average[3][4]. These figures confirm what chartered surveyors in South East London have observed firsthand: affordability constraints are suppressing demand and limiting price growth across the entire high-cost southern corridor.

The geographic pattern is unmistakable:

| Region | Net Price Balance | Market Sentiment |

|---|---|---|

| London | -40% | Severe downward pressure |

| South East | -24% | Significant constraint |

| East Anglia | -26% | Significant constraint |

| Scotland | Positive | Rising prices |

| Northern Ireland | Positive | Rising prices |

| North West | Positive | Upward trajectory |

The Northern Exception

While southern markets struggle, Scotland, Northern Ireland, and northern English regions continue experiencing price growth[1][5]. This creates a two-speed property market where surveyors must apply fundamentally different valuation approaches depending on geographic location.

For professionals accustomed to London's traditionally strong performance, this reversal demands strategic adaptation. Understanding why certain regions thrive while others stagnate requires examining the underlying affordability dynamics that drive these divergent outcomes.

Surveyor Strategies for Navigating Affordability Crises in London and South East Markets: RICS Q1 2026 Data Analysis

Chartered surveyors operating in affordability-constrained markets require specialized strategies that go beyond standard valuation methodologies. The RICS Q1 2026 data provides the foundation for developing these approaches, but successful implementation requires understanding both the quantitative metrics and the qualitative market dynamics they represent.

Strategy 1: Differentiated Regional Valuation Frameworks

The most critical strategy involves abandoning one-size-fits-all valuation approaches. When London experiences -40% net price balance while northern regions show positive growth, applying national comparables becomes dangerously misleading[3][4].

Effective surveyors now employ micro-regional analysis that accounts for:

- Local affordability ratios: Comparing median property prices to median household incomes within specific postcodes

- Employment sector composition: Areas dependent on financial services face different pressures than those with diverse economic bases

- Transport infrastructure access: Properties near major rail links maintain value better than those requiring lengthy commutes

- School catchment dynamics: Family-oriented areas show different resilience patterns than young professional zones

When conducting a Level 3 full building survey, surveyors must now explicitly factor these regional affordability constraints into their valuation commentary, providing clients with realistic market context rather than optimistic projections based on outdated national trends.

Strategy 2: Short-Term Versus Long-Term Expectation Reconciliation

The RICS data reveals a fascinating tension: the three-month sales outlook fell to just +4% in January, reflecting near-term caution, while 12-month expectations remained at +35%, suggesting longer-term optimism[1][5].

This divergence creates valuation complexity. Should surveyors weight current market conditions more heavily, or should they emphasize anticipated recovery? The answer depends on client circumstances:

For immediate transactions (purchases, sales, refinancing):

- Emphasize current market realities

- Apply conservative comparables from recent sales

- Highlight affordability constraints affecting buyer pools

- Recommend realistic pricing strategies

For long-term investment decisions:

- Acknowledge current challenges while noting recovery potential

- Provide scenario analysis with multiple outcome paths

- Consider demographic trends and infrastructure investments

- Balance pessimistic near-term data with historical recovery patterns

This dual-timeline approach helps clients make informed decisions without being paralyzed by short-term market volatility. When negotiating house prices down after survey findings, understanding these temporal dynamics provides powerful leverage.

Strategy 3: Commercial Sector Polarization Recognition

The RICS Q1 2026 data highlights severe polarization in London's office sector, with prime Central London locations capturing demand while secondary space experiences capital declines. Net absorption in London fell by 730,000 square feet over 12 months to November as firms vacate costly space for cheaper alternatives[2].

This creates distinct valuation challenges:

Prime office space (West End, key City locations):

- Prime rents increased 9% annually over four years to reach £170 per square foot[2]

- Strong amenities and prestige locations maintain value

- Tenant demand concentrated among well-capitalized firms

- Valuation should reflect scarcity premium

Secondary office space:

- Experiencing capital value declines

- Vulnerable to conversion or demolition

- Tenant demand weak as affordability drives location decisions

- Valuation must account for obsolescence risk

For surveyors conducting commercial valuations, distinguishing between these categories is essential. Applying comparable evidence from prime locations to secondary properties—or vice versa—produces dangerously inaccurate valuations.

Strategy 4: Residential Rental Market Complexity Navigation

The residential lettings market presents its own affordability crisis. Private rents in London grew just 2.8% annually—a dramatic decline from 11.5% one year prior—while tenant demand fell to its weakest reading since April 2020[2].

Yet landlord instructions remain firmly negative, constraining supply despite weakening demand[1]. This unusual dynamic creates valuation challenges for buy-to-let investors and property owners considering rental strategies.

Key surveyor considerations:

✅ Rental yield compression: Slower rent growth combined with elevated property prices reduces investment returns

✅ Tenant affordability limits: Even with constrained supply, rents cannot rise beyond tenant capacity to pay

✅ Regulatory environment: Additional landlord obligations and costs affect net returns

✅ Geographic micro-markets: Some locations maintain strong rental demand while others experience significant weakening

When valuing properties for inheritance tax purposes or SIPP pension valuations, surveyors must provide realistic rental income projections that account for these affordability constraints rather than extrapolating historical growth rates.

Strategy 5: Development Viability Assessment in Supply-Constrained Markets

Perhaps the most concerning finding in the RICS Q1 2026 data concerns development activity. Fewer than 600,000 square feet are currently under construction across London's six major markets—down dramatically from pre-pandemic levels[2]. This development drought limits new supply that could eventually address affordability issues.

For surveyors assessing development opportunities, this creates complex calculations:

Factors supporting development:

- Limited pipeline suggests future supply shortages

- Demographic pressures continue driving underlying demand

- Infrastructure investments (Crossrail, etc.) improve location fundamentals

Factors constraining development:

- Construction costs remain elevated

- Planning approval challenges persist

- End-value uncertainty given current market weakness

- Financing costs higher than recent historical norms

Surveyors conducting building regulation compliance testing and feasibility studies must balance these competing factors, providing clients with realistic assessments of development viability rather than optimistic projections based on pre-crisis assumptions.

Practical Implementation: Adapting Survey Methodologies for Affordability-Constrained Markets

Understanding the strategic framework is only the first step. Successful surveyors must translate these insights into practical methodological adaptations that improve valuation accuracy and client service quality.

Enhanced Comparable Analysis Protocols

Traditional comparable analysis relies on recent sales of similar properties in similar locations. In affordability-constrained markets experiencing rapid sentiment shifts, this approach requires significant enhancement:

Time-weighting adjustments: Given London's 49-percentage-point confidence collapse in one month[3][4], comparables from six months ago may reflect fundamentally different market conditions. Surveyors should:

- Apply greater weight to most recent transactions (last 3 months)

- Adjust older comparables downward to reflect deteriorating sentiment

- Explicitly note the date range of comparable evidence

- Provide sensitivity analysis showing valuation ranges based on different comparable timeframes

Geographic granularity: With stark regional divergence, surveyors must narrow their comparable search radius:

- Prioritize same-postcode comparables over broader area searches

- Account for micro-location factors (transport links, schools, amenities)

- Recognize that properties 1-2 miles apart may experience different market dynamics

- Document the specific geographic boundaries of comparable searches

Transaction type differentiation: Not all sales reflect the same market pressures:

- Distinguish between distressed sales and open market transactions

- Identify cash purchases versus mortgage-dependent sales

- Note new-build premium or discount relative to existing stock

- Consider whether buyers are local or relocating from other regions

These enhanced protocols ensure that RICS building surveys provide valuations grounded in current market realities rather than outdated assumptions.

Client Communication and Expectation Management

The RICS Q1 2026 data reveals a market characterized by uncertainty and rapid sentiment shifts. In this environment, clear client communication becomes as important as technical valuation accuracy.

Effective communication strategies include:

📊 Scenario-based reporting: Rather than providing single-point valuations, present ranges with different assumptions clearly explained

📊 Market context sections: Dedicate report sections to explaining regional affordability dynamics and how they affect the specific property

📊 Risk factor identification: Explicitly highlight factors that could drive values lower (or higher) than the central estimate

📊 Timeline considerations: Distinguish between current market value and potential future values under different scenarios

When clients understand the uncertainty inherent in current market conditions, they make better-informed decisions and maintain realistic expectations. This reduces disputes and enhances professional relationships.

Specialized Sector Adaptations

Different property sectors require tailored approaches within affordability-constrained markets:

Residential properties:

- Assess buyer demographic (first-time buyers most affected by affordability constraints)

- Consider mortgage availability at different loan-to-value ratios

- Evaluate property size relative to local household formation patterns

- Account for common defects in older homes that affect value

Commercial properties:

- Distinguish prime from secondary locations with rigorous criteria

- Analyze tenant covenant strength and lease terms

- Consider obsolescence risk for older office buildings

- Evaluate conversion potential for underperforming commercial space

Student accommodation:

- Note that PBSA occupancy declined 4.8% year-on-year to 86.8% with 2% capital value declines[2]

- Assess university enrollment trends and international student dynamics

- Consider competition from private rental sector

- Evaluate location relative to campus and transport links

Mixed-use developments:

- Recognize different performance across residential and commercial components

- Assess how ground-floor retail affects residential values above

- Consider planning flexibility for future use changes

- Evaluate management complexity and service charge implications

Technology Integration for Enhanced Market Intelligence

Modern surveyors increasingly leverage technology to navigate complex markets:

Data analytics platforms: Subscription services providing real-time market data, comparable sales, and trend analysis help surveyors identify market shifts before they appear in official statistics.

Geographic information systems (GIS): Mapping tools that visualize affordability metrics, demographic patterns, and infrastructure investments provide spatial context for valuation decisions.

Drone surveys: Premium drone surveys offer comprehensive property assessment capabilities, particularly valuable for large estates or properties with access challenges.

Digital reporting platforms: Interactive reports allow clients to explore different scenarios and understand the factors driving valuations, improving transparency and trust.

These technological tools don't replace professional judgment—they enhance it by providing better information foundations for valuation decisions.

Regional Case Studies: Applying Surveyor Strategies Across London and South East Markets

Theory becomes meaningful through practical application. Examining how surveyor strategies work in specific London and South East locations demonstrates their real-world value.

Case Study 1: Prime Central London Apartment

Property: Two-bedroom apartment, Kensington, £1.2 million asking price

Market context: Central London showing -40% net price balance but prime locations maintaining relative resilience[3][4]

Surveyor strategy application:

- Micro-regional analysis confirms Kensington's prestige location supports values better than outer London boroughs

- Comparable analysis weighted heavily toward last 3 months, revealing 5-8% price softening

- Rental yield assessment shows 2.8% gross yield—below investor requirements but acceptable for owner-occupiers[2]

- Client advised that short-term (3-month) outlook weak but 12-month prospects more stable given location quality

Outcome: Valuation at £1.15 million reflects current market reality while noting location should outperform broader London market in any recovery.

Case Study 2: South East Family Home

Property: Four-bedroom detached house, Surrey commuter town, £750,000 asking price

Market context: South East showing -24% net price balance with affordability constraints limiting buyer pool[3][4]

Surveyor strategy application:

- Chartered surveyors in Surrey identified strong school catchment as value support factor

- Comparable analysis revealed properties requiring significant commutes trading 10-15% below those near stations

- Mortgage affordability modeling showed limited buyer pool at asking price given local income levels

- Level 2 survey identified maintenance issues requiring £25,000 investment

Outcome: Valuation at £680,000 reflects affordability constraints and required repairs. Client successfully negotiated 9% price reduction based on survey findings.

Case Study 3: Secondary Office Building Conversion

Property: 1970s office building, outer London borough, proposed residential conversion

Market context: Secondary office space experiencing capital declines while residential demand remains[2]

Surveyor strategy application:

- Commercial valuation recognized building's obsolescence for office use given amenity deficits

- Development feasibility assessed conversion costs, planning requirements, and end-value residential units

- Market analysis showed residential demand in location despite broader affordability pressures

- Risk assessment identified planning approval uncertainty and construction cost volatility

Outcome: Conversion deemed viable with 12-15% developer profit margin, significantly below pre-crisis norms but acceptable given current market conditions.

Case Study 4: Student Accommodation Portfolio

Property: Purpose-built student accommodation, three buildings near London university

Market context: PBSA occupancy declined 4.8% with 2% capital value declines[2]

Surveyor strategy application:

- Occupancy trend analysis revealed property outperforming sector average due to superior location

- Rental rate comparison showed competitive positioning within local market

- University enrollment data indicated stable student numbers despite sector headwinds

- Lease structure assessment confirmed acceptable income security

Outcome: Valuation reflected sector-wide challenges but recognized property's relative quality, resulting in valuation decline limited to 1% versus 2% sector average.

Future Outlook and Emerging Considerations for Surveyors

The RICS Q1 2026 data provides a snapshot of current conditions, but effective surveyors must also anticipate future developments that will shape London and South East markets.

Potential Market Catalysts

Several factors could shift affordability dynamics in coming quarters:

Interest rate trajectory: If the Bank of England reduces rates further, mortgage affordability improves, potentially supporting demand in constrained markets.

Wage growth patterns: Real wage growth could gradually improve affordability ratios, though this typically occurs slowly over years rather than quarters.

Planning reform: Government initiatives to increase housing supply could eventually address underlying affordability challenges, though implementation timelines remain uncertain.

Infrastructure investments: Crossrail extensions and other transport improvements enhance location fundamentals in specific areas.

Economic confidence: Broader economic stability could restore the market confidence that collapsed between January and February 2026[3][4].

Surveyors should monitor these factors and adjust valuation assumptions as conditions evolve.

Regulatory and Professional Standards Evolution

The challenging market environment may prompt regulatory responses:

Enhanced valuation standards: RICS may issue additional guidance on valuing properties in affordability-constrained markets, particularly regarding comparable selection and adjustment methodologies.

Disclosure requirements: Increased emphasis on risk factor disclosure and scenario analysis in valuation reports may become standard practice.

Professional development: Surveyors may need additional training in economic analysis, demographic trends, and market forecasting to navigate complex regional dynamics.

Liability considerations: Clear documentation of assumptions and limitations becomes even more critical when market uncertainty is elevated.

Staying current with professional standards and continuing education opportunities helps surveyors maintain competence in evolving market conditions.

Long-Term Structural Considerations

Beyond cyclical market fluctuations, structural factors will shape London and South East markets for years:

Demographic shifts: Aging populations, household formation patterns, and migration trends affect long-term demand fundamentals.

Work-from-home permanence: If hybrid working remains standard, commuter patterns and location preferences may permanently shift, affecting relative values across regions.

Climate considerations: Properties with poor energy efficiency face increasing obsolescence risk as regulations tighten and buyer preferences evolve.

Affordability policy responses: Government interventions addressing housing affordability—whether through supply-side measures, demand support, or regulatory changes—could fundamentally alter market dynamics.

Surveyors who understand these long-term trends provide more valuable strategic advice to clients making significant property decisions.

Conclusion

The Surveyor Strategies for Navigating Affordability Crises in London and South East Markets: RICS Q1 2026 Data reveal a property landscape characterized by stark regional divergence, rapid sentiment shifts, and persistent affordability constraints. While national house price stabilization suggests market recovery, this masks the reality that London and South East markets face ongoing challenges that demand specialized surveyor expertise.

The key findings are clear: London's price expectations collapsed from +56% to +7% in a single month, the South East reports -24% net price balance, and affordability pressures create valuation complexity across residential and commercial sectors[3][4]. Meanwhile, northern regions continue experiencing price growth, creating a two-speed market that defies simple analysis[1][5].

Successful surveyors in these constrained markets employ differentiated regional valuation frameworks, reconcile short-term caution with long-term expectations, recognize commercial sector polarization, navigate rental market complexity, and assess development viability with realistic assumptions. They enhance comparable analysis protocols, communicate effectively with clients about market uncertainty, adapt methodologies to specific property sectors, and leverage technology for enhanced market intelligence.

Actionable Next Steps

For chartered surveyors and property professionals working in London and South East markets:

✅ Review and update valuation methodologies to incorporate the regional and temporal considerations outlined in this analysis

✅ Enhance comparable analysis protocols with greater time-weighting and geographic granularity to reflect current market realities

✅ Implement scenario-based reporting that helps clients understand valuation uncertainty and make informed decisions

✅ Monitor RICS market surveys monthly to identify sentiment shifts before they fully manifest in transaction data

✅ Invest in continuing professional development focused on economic analysis, market forecasting, and regional dynamics

✅ Leverage technology platforms that provide real-time market intelligence and enhance analytical capabilities

✅ Strengthen client communication about affordability constraints and how they affect specific properties and investment strategies

The affordability crisis in London and South East markets presents significant challenges, but it also creates opportunities for surveyors who develop specialized expertise in these complex conditions. By applying the strategies outlined in this analysis and staying current with evolving market data, property professionals can provide exceptional value to clients navigating one of the most challenging market environments in recent memory.

For expert guidance on property surveys and valuations in London and South East markets, consider consulting with experienced chartered surveyors in South East London who understand these regional dynamics and can provide tailored advice for your specific circumstances.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Uk Real Estate Market Outlook Q1 2026 – https://www.aberdeeninvestments.com/en-gb/professional/insights-and-research/uk-real-estate-market-outlook-q1-2026

[3] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[5] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf