The UK mortgage market stands at a critical inflection point. With major lending institutions forecasting unprecedented volume increases and 1.8 million fixed-rate mortgages set to expire this year, chartered surveyors face a perfect storm of opportunity and operational challenge. Preparing Chartered Surveyors for 2026 Lending Volume Surge: Faster Valuations Amid Recovery Demand isn't just a strategic priority—it's an operational imperative that will separate thriving practices from those left struggling with backlogs and quality concerns.

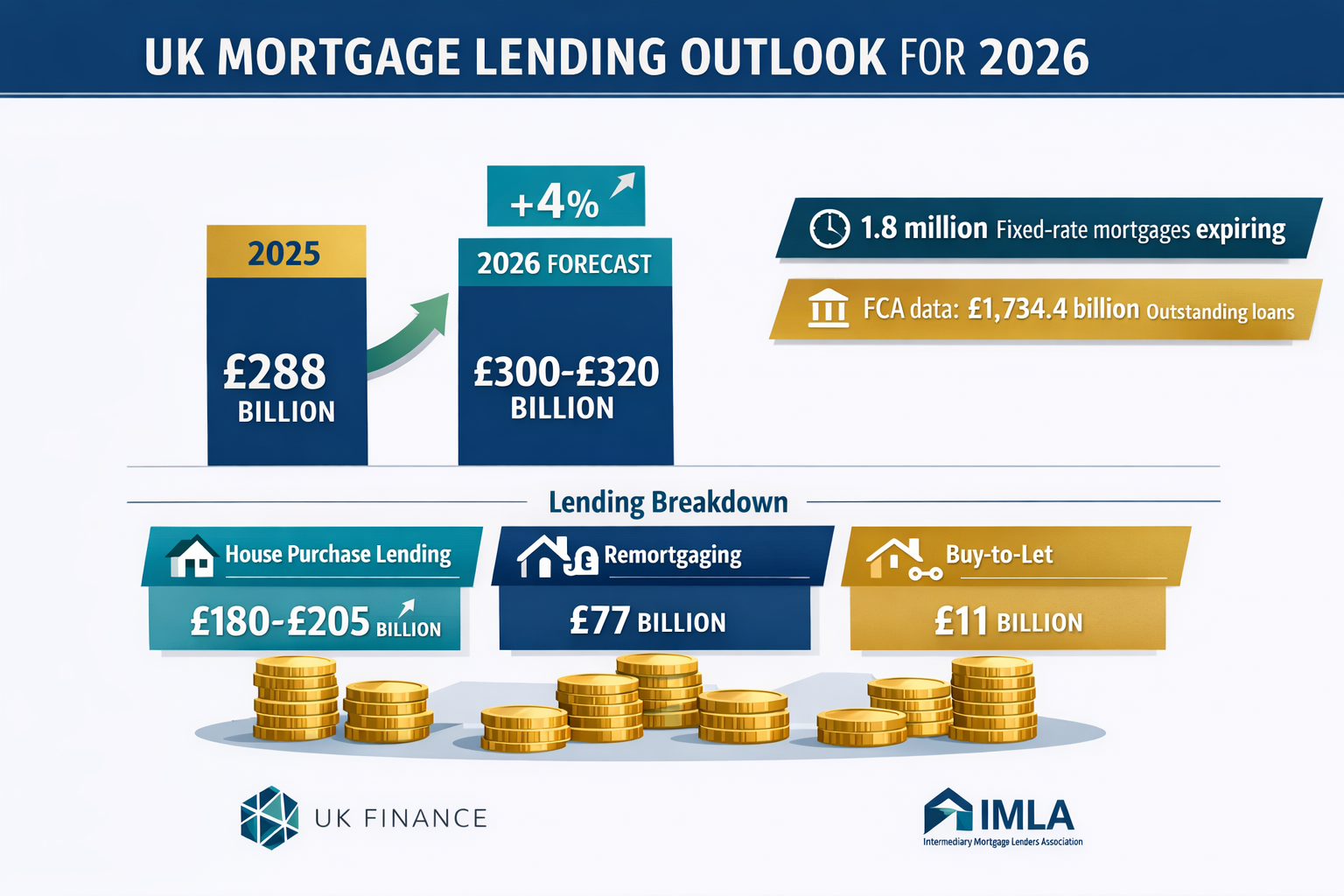

As UK Finance projects gross lending growth to £300 billion and the Intermediary Mortgage Lenders Association (IMLA) forecasts even more aggressive expansion to £320 billion[1][2], the surveying profession must rapidly evolve. Lenders demand faster turnaround times without compromising accuracy, borrowers expect seamless digital experiences, and regulatory bodies maintain stringent quality standards. The question isn't whether volume will surge—it's whether surveyors will be ready.

Key Takeaways

- 📈 Mortgage lending volumes are forecast to reach £300-£320 billion in 2026, representing 4-11% growth with house purchase lending between £180-£205 billion driving demand for property valuations[1][2]

- 🔄 1.8 million fixed-rate mortgages expire in 2026, creating a remortgaging surge projected at £77 billion (+10% growth) that will significantly increase valuation workload[1]

- ⚡ Technology adoption is essential for surveyors to meet faster turnaround expectations while maintaining RICS standards and quality assurance protocols

- 🎯 Regional demand patterns will vary significantly, with northern England showing stronger growth potential than southern markets, requiring strategic capacity planning[5]

- 💼 Workflow optimization and automation will differentiate successful surveying practices from those overwhelmed by volume increases and quality pressures

Understanding the 2026 Lending Volume Surge

The Numbers Behind the Recovery

The mortgage market recovery represents more than statistical optimism—it reflects fundamental shifts in lending conditions, regulatory frameworks, and consumer confidence. UK Finance's conservative forecast of £300 billion in gross lending for 2026 marks a 4% increase from 2025's approximately £288 billion[1]. However, IMLA's more bullish projection of £320 billion suggests the potential for double-digit growth if conditions align favorably[2].

House purchase lending forms the cornerstone of this expansion, with forecasts ranging from £180 billion (UK Finance) to £205 billion (IMLA)[1][2]. This represents the primary growth driver for new valuation instructions, as every mortgage application for property purchase requires a professional assessment.

The remortgaging sector tells an equally compelling story. With £77 billion projected for external remortgaging (a 10% increase) and £261 billion in internal product transfers, the refinancing wave creates substantial valuation demand[1]. Many lenders require updated valuations even for existing customers, particularly when loan-to-value ratios have changed significantly since the original mortgage.

Why Volumes Are Surging Now

Several converging factors explain the 2026 lending boom:

💰 Interest Rate Stabilization – After years of volatility, expectations for gradual rate reductions have improved affordability calculations and borrower confidence, making mortgage commitments more predictable.

📋 Regulatory Adjustments – Modifications to lending criteria and affordability assessments have expanded the pool of eligible borrowers without compromising prudent lending standards[2].

🏠 Fixed-Rate Expiries – The 1.8 million mortgages reaching their fixed-rate end dates create an unavoidable refinancing wave, regardless of broader market conditions[1].

📊 Market Confidence – RICS survey data from December 2025 shows confidence "decisively more" favorable, with expectations for sales and prices turning positive after extended uncertainty[7].

According to FCA data from March 2026, outstanding residential mortgage loans reached £1,734.4 billion—the highest stock since reporting began in 2007[4]. This massive portfolio requires ongoing management, valuations for equity release, and assessments for portfolio switches, adding to the overall demand picture.

For chartered surveyors, understanding these drivers helps anticipate not just volume increases but also the types of valuations most in demand. Purchase valuations require comprehensive on-site inspections, while remortgage valuations may leverage desktop reviews or automated valuation models (AVMs) for lower-risk properties. Strategic valuation services must accommodate this diversity.

Operational Challenges: Speed vs. Quality in Preparing Chartered Surveyors for 2026 Lending Volume Surge

The Turnaround Time Pressure

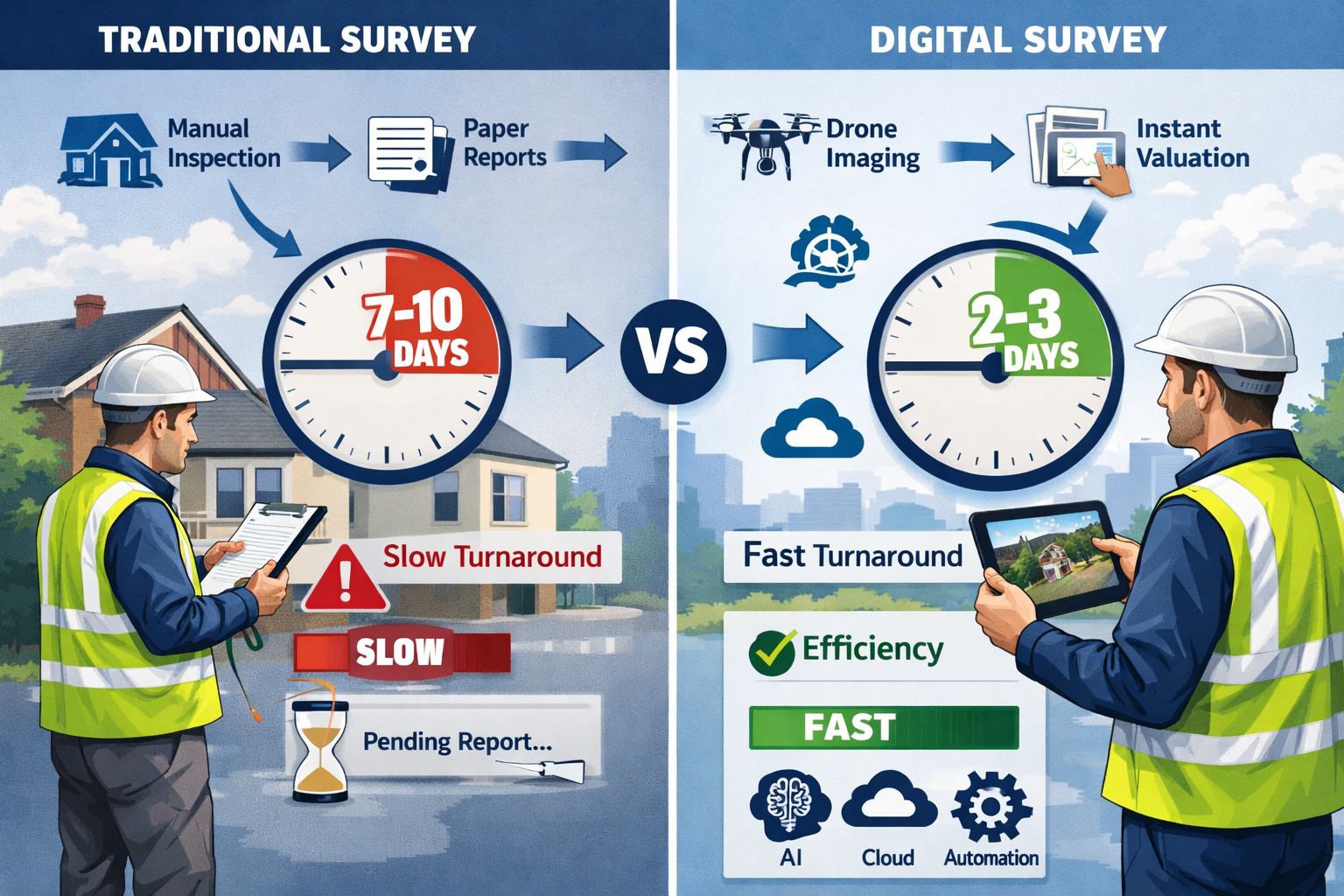

Lenders increasingly compete on speed-to-offer, compressing the entire mortgage application timeline. Where a 7-10 day valuation turnaround was once standard, many lenders now expect 48-72 hours for straightforward cases. This acceleration creates immediate operational challenges:

Resource Constraints – Most surveying practices operate with fixed capacity. A 10-20% volume increase cannot be absorbed without additional surveyors, expanded geographic coverage, or significant productivity improvements.

Geographic Imbalances – Regional variations in lending growth mean some areas face acute surveyor shortages while others have excess capacity. House price growth predictions show stronger performance in northern England compared to southern markets[5], potentially creating regional bottlenecks.

Quality Assurance Risks – Rushing valuations increases error probability, potentially exposing surveyors to professional liability and lenders to inaccurate security assessments.

Maintaining RICS Standards Under Volume Pressure

The Royal Institution of Chartered Surveyors (RICS) maintains rigorous professional standards that cannot be compromised regardless of volume pressures. Every valuation must:

- ✅ Comply with the RICS Valuation – Global Standards (Red Book)

- ✅ Include appropriate site inspections or clearly documented desktop methodology

- ✅ Utilize comparable evidence from appropriate timeframes and locations

- ✅ Document assumptions, limitations, and special assumptions transparently

- ✅ Undergo appropriate quality review before submission

These requirements create an inherent tension with speed demands. The solution isn't cutting corners—it's systematizing excellence through technology and process optimization.

The Buy-to-Let Dimension

While buy-to-let lending remains flat at approximately £11 billion for 2026[3], this sector presents unique valuation challenges. Institutional investors increasingly dominate this market, demanding sophisticated analysis beyond simple capital valuations:

- Rental yield assessments for investment performance metrics

- Portfolio valuations covering multiple properties simultaneously

- Market rent reviews for existing tenanted properties

- Development potential analysis for value-add strategies

Property value increases of 22.2% over five years and rental income growth of 12% sustain investor demand despite regulatory constraints[3]. Surveyors serving this market need specialized expertise in investment property valuation methodologies.

Our SIPP pension valuations service addresses the growing intersection between property investment and retirement planning, where accurate valuations are essential for compliance and tax purposes.

Technology Solutions for Faster Valuations Without Compromising Quality

Digital Workflow Transformation

Modern surveying practices must embrace comprehensive digital transformation across the entire valuation lifecycle:

📱 Mobile Inspection Technology – Tablets and smartphones equipped with specialized surveying apps enable real-time data capture, photo documentation with automatic metadata, and immediate report drafting during site visits. This eliminates double-handling and transcription errors.

☁️ Cloud-Based Report Systems – Centralized platforms allow multiple surveyors to access templates, comparable data, and quality assurance resources from any location, facilitating flexible working and rapid deployment to high-demand areas.

🤖 Automated Valuation Models (AVMs) – For lower-risk remortgaging cases, AVMs provide rapid desktop valuations using algorithmic analysis of comparable sales data, property characteristics, and market trends. While not suitable for all scenarios, AVMs can handle routine cases, freeing chartered surveyors for complex assessments requiring professional judgment.

🔗 Lender Portal Integration – Direct API connections between surveyor systems and lender platforms eliminate manual data entry, reduce turnaround times by hours or days, and minimize communication errors.

Data Integration and Comparable Evidence

Access to comprehensive, current market data represents a competitive advantage in fast-paced valuation environments. Modern systems integrate:

- Land Registry price paid data with automatic filtering by property type, location, and transaction date

- Rightmove and Zoopla listings for current market asking prices and time-on-market metrics

- Local authority planning data for development potential and constraints

- Energy Performance Certificate databases for sustainability assessments

- Flood risk and environmental data for risk evaluation

By automating data gathering and preliminary analysis, surveyors can focus their expertise on interpretation, adjustment, and professional judgment—the irreplaceable human elements of quality valuation.

Quality Assurance Through Technology

Technology doesn't just accelerate work—it can enhance quality when properly implemented:

Automated Consistency Checks – Software can flag unusual value conclusions, identify missing required information, and ensure calculations are mathematically correct before human review.

Peer Review Workflows – Digital systems facilitate structured peer review processes where senior surveyors can quickly review junior staff work, providing feedback and approval within hours rather than days.

Audit Trails – Complete documentation of data sources, methodology decisions, and review processes protects both surveyors and lenders while satisfying regulatory requirements.

Continuous Professional Development – Online training platforms and digital knowledge bases ensure all team members stay current with market conditions, regulatory changes, and best practices.

For practices offering specialized services like leasehold extension and enfranchisement valuations, technology enables efficient handling of complex calculations while maintaining the detailed documentation these cases require.

Strategic Capacity Planning for Preparing Chartered Surveyors for 2026 Lending Volume Surge: Faster Valuations Amid Recovery Demand

Workforce Development and Recruitment

Meeting the 2026 volume surge requires strategic human resource planning:

🎓 Accelerated Training Programs – Developing junior surveyors through structured mentorship and technology-assisted learning reduces the time from recruitment to productive capacity.

🤝 Strategic Partnerships – Forming networks with other surveying practices enables workload sharing during peak periods, geographic coverage expansion, and specialized expertise access.

💼 Flexible Staffing Models – Engaging experienced surveyors on flexible or contract bases provides surge capacity without permanent overhead increases.

🌍 Regional Expansion – Establishing presence in high-growth areas, particularly northern England where stronger house price growth is forecast[5], positions practices to capture emerging demand.

Our network of chartered surveyors across Essex, Hampshire, and East London demonstrates the value of strategic geographic positioning.

Service Differentiation and Specialization

Rather than competing solely on speed, successful practices differentiate through:

Specialized Property Types – Developing expertise in complex properties (listed buildings, non-standard construction, mixed-use) where generic AVMs fail and professional judgment commands premium fees.

Value-Added Services – Offering complementary services like right-to-buy valuations or annual tax valuations creates additional revenue streams and client relationships.

Institutional Client Focus – Developing capabilities for portfolio valuations, investment analysis, and sophisticated reporting meets the needs of buy-to-let investors and property funds.

Regulatory Compliance Expertise – Positioning as the go-to resource for complex regulatory scenarios (MEES compliance, stamp duty optimization, pension fund requirements) builds reputation and referral networks.

Managing Affordability Constraints

UK Finance notes that "affordability is now very tight" and will limit borrowing options for potential buyers[1]. This constraint affects valuation demand in several ways:

- Lower average loan sizes may reduce per-valuation fees while increasing volume

- Increased scrutiny of valuations by lenders concerned about security adequacy

- Greater focus on accurate market value rather than optimistic assessments

- Regional variations as affordability differs significantly across UK markets

RICS respondents identify financial constraints as the most significant obstacle to construction activity, with 70% citing this factor[6]. This may dampen new-build valuation demand while increasing focus on existing property transactions.

Regional Considerations and Market Variations

Geographic Demand Patterns

The 2026 lending surge won't distribute evenly across the UK. Understanding regional variations enables strategic resource allocation:

Northern England – Stronger house price growth predictions and improving affordability make this region a primary growth market. Practices with capacity in these areas will see disproportionate volume increases.

London and Southeast – Continued affordability challenges may moderate growth, but the sheer transaction volume and higher property values maintain strong demand for professional valuations in areas like Chelsea, Richmond, and Camden.

Regional Centers – Cities like Hemel Hempstead, Enfield, and Bexley offer balanced markets with steady demand and manageable competition.

Rural and Coastal Areas – Sussex and similar regions present specialized valuation challenges requiring local market knowledge and expertise in unique property types.

Property Type Considerations

Different property segments require varying valuation approaches:

| Property Type | Valuation Complexity | Technology Suitability | Turnaround Expectation |

|---|---|---|---|

| Standard Residential | Low-Medium | High (AVM suitable) | 24-48 hours |

| Period Properties | Medium-High | Medium | 5-7 days |

| Non-Standard Construction | High | Low | 7-10 days |

| Buy-to-Let Investment | Medium-High | Medium | 3-5 days |

| New Build | Medium | High | 2-3 days |

| Listed Buildings | Very High | Low | 10-14 days |

Strategic practices develop capabilities across multiple segments while maintaining excellence in their specializations.

Lender Relationships and Panel Management

Meeting Panel Requirements

Most mortgage lenders operate surveyor panels with specific requirements:

Professional Qualifications – RICS membership (typically MRICS or FRICS) with appropriate experience levels and professional indemnity insurance.

Geographic Coverage – Demonstrable local market knowledge and capacity to serve lender's operating areas within required timeframes.

Technology Integration – Capability to receive instructions and submit reports through lender portals with required data formats.

Quality Metrics – Track record of accurate valuations, low complaint rates, and compliance with lender-specific requirements.

Capacity Commitments – Ability to handle volume fluctuations and maintain service levels during peak periods.

Building Strategic Lender Partnerships

Beyond basic panel membership, leading practices develop strategic relationships through:

✨ Consistent Quality – Building reputation for accurate, well-documented valuations that withstand scrutiny and support lending decisions.

✨ Responsive Communication – Providing clear, timely updates on progress, challenges, and completion timelines.

✨ Flexibility – Accommodating urgent instructions and adapting to changing lender requirements.

✨ Value-Added Insights – Offering market intelligence and trend analysis that helps lenders understand portfolio risks and opportunities.

✨ Technology Collaboration – Working with lenders to optimize integration, streamline processes, and pilot new technologies.

These relationships create competitive advantages when lenders allocate increased volumes during the 2026 surge.

Financial Planning and Business Development

Investment Priorities

Preparing for the lending volume surge requires strategic investment:

Technology Infrastructure – Cloud platforms, mobile devices, software licenses, and integration development represent significant capital requirements but deliver rapid ROI through efficiency gains.

Human Capital – Recruitment, training, and retention programs ensure adequate capacity with appropriate skill levels.

Marketing and Business Development – Strengthening lender relationships, expanding geographic presence, and building brand recognition position practices for volume capture.

Quality Assurance Systems – Robust review processes, compliance monitoring, and professional development maintain standards under pressure.

Revenue Optimization

The volume surge creates opportunities for revenue growth beyond simple fee-for-service models:

- Tiered Pricing – Offering premium rates for expedited service or complex properties while maintaining competitive pricing for standard work

- Volume Agreements – Negotiating favorable terms with high-volume lenders in exchange for capacity commitments

- Bundled Services – Combining valuations with building surveys, snagging reports, or other complementary services

- Subscription Models – Offering ongoing valuation services for portfolio landlords or investment funds

Our approach to building surveys demonstrates how comprehensive service offerings create value beyond basic valuation requirements.

Risk Management

Volume increases amplify risks that require proactive management:

Professional Indemnity Insurance – Ensuring adequate coverage for increased volume and potential claim exposure.

Quality Control – Maintaining rigorous review processes despite time pressures to prevent errors and omissions.

Capacity Management – Avoiding over-commitment that could compromise quality or damage lender relationships.

Regulatory Compliance – Staying current with RICS standards, data protection requirements, and industry best practices.

Financial Stability – Managing cash flow, working capital, and profitability through volume fluctuations.

Conclusion: Positioning for Success in the 2026 Market

The 2026 lending volume surge represents a defining moment for chartered surveyors. With mortgage lending forecast between £300-£320 billion, 1.8 million fixed-rate mortgages expiring, and remortgaging volumes growing 10%, the demand for professional valuations will test the capacity and capabilities of every practice[1][2].

Preparing Chartered Surveyors for 2026 Lending Volume Surge: Faster Valuations Amid Recovery Demand requires a comprehensive strategy addressing technology adoption, workforce development, quality assurance, and strategic positioning. Success belongs to practices that:

🎯 Embrace technology without compromising professional standards or RICS compliance

🎯 Invest in people through training, recruitment, and retention strategies that build sustainable capacity

🎯 Differentiate services through specialization, quality, and value-added offerings beyond commodity valuations

🎯 Build strategic relationships with lenders, partners, and clients that create competitive advantages

🎯 Plan regionally with understanding of geographic demand patterns and market variations

The fundamentals remain unchanged: accurate valuations require professional judgment, local market knowledge, and rigorous methodology. Technology accelerates these processes but doesn't replace them. The practices that thrive in 2026 will be those that harness innovation to deliver faster valuations without sacrificing the quality and integrity that define the chartered surveying profession.

Next Steps

For Surveying Practices:

- Audit current technology capabilities and identify gaps

- Assess workforce capacity against projected volume increases

- Review lender panel memberships and strengthen strategic relationships

- Develop specialized service offerings for high-value market segments

- Implement quality assurance systems that scale with volume

For Lenders:

- Engage early with surveyor panels about capacity planning

- Invest in technology integration that streamlines instruction and reporting

- Consider strategic partnerships with high-capacity, quality-focused practices

- Balance speed requirements with quality standards and risk management

For Property Professionals:

- Partner with surveyors who demonstrate technology adoption and quality commitment

- Understand regional variations in valuation capacity and turnaround times

- Leverage specialized valuation services for complex transactions

The 2026 lending recovery creates opportunities for growth, innovation, and professional excellence. The time to prepare is now.

References

[1] Modest Growth Forecast Mortgage Lending In 2026 – https://www.ukfinance.org.uk/news-and-insight/press-release/modest-growth-forecast-mortgage-lending-in-2026

[2] Rise In Mortgage Lending Predicted Over Next Two Years – https://www.beaconfinancialtraining.co.uk/blog/rise-in-mortgage-lending-predicted-over-next-two-years/

[3] Buy To Let Valuation Surge 2026 Survey Strategies For Institutional Investors In A Recovering Market – https://nottinghillsurveyors.com/blog/buy-to-let-valuation-surge-2026-survey-strategies-for-institutional-investors-in-a-recovering-market

[4] Mortgage Lending Statistics – https://www.fca.org.uk/data/mortgage-lending-statistics

[5] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/

[6] Uk Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf

[7] Uk Residential Survey Dec 2025 Confidence Rebound – https://www.rics.org/news-insights/uk-residential-survey-dec-2025-confidence-rebound