The property landscape across Northern England has shifted dramatically. While southern markets experience stagnation and uncertainty, chartered surveyors working across Yorkshire, the North East, and North West regions are witnessing something remarkable: consistent upward price trends that demand fresh valuation approaches. Northern England Property Valuations 2026: Surveyor Techniques for Upward Price Trends in Recovering Markets represents not just a regional phenomenon, but a fundamental recalibration of how professionals assess value in areas experiencing genuine economic recovery.

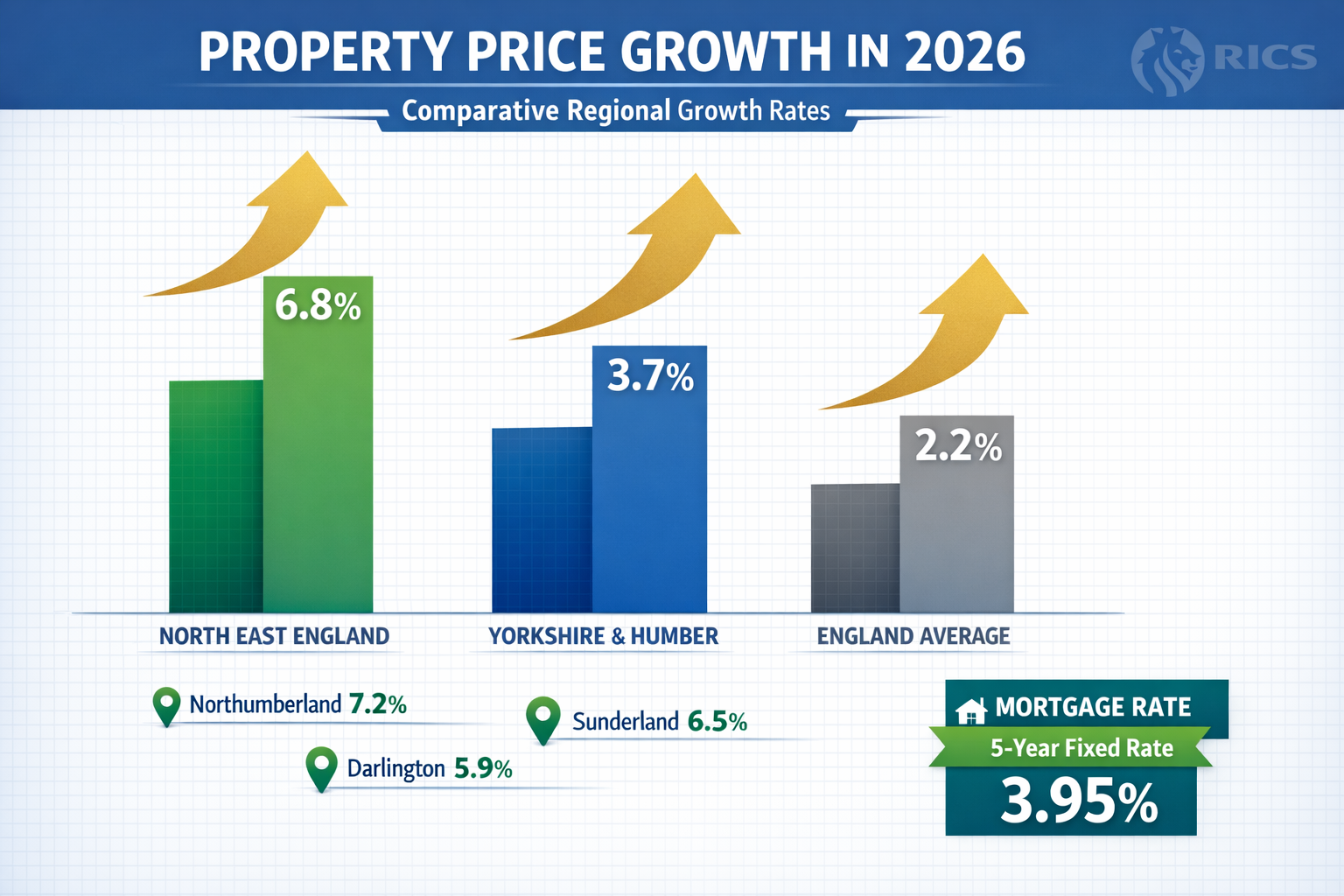

The North East recorded an impressive 6.8% annual price growth in 2026, with Yorkshire & Humber achieving 3.7%—both significantly outpacing England's overall 2.2% growth rate.[1] For RICS-qualified surveyors, these figures signal the need for specialized comparable analysis methods that account for rapid appreciation rather than the price adjustments more common in southern regions.

Key Takeaways

- Regional outperformance: Northern England markets are delivering 6.8% annual growth (North East) and 3.7% (Yorkshire & Humber), tripling the national average and requiring surveyors to adjust valuation methodologies for upward trends.[1]

- Transaction velocity indicates strength: Properties in leading Northern markets sell within two weeks on average, compared to extended listing periods in the South, signaling genuine buyer demand that supports higher valuations.[3]

- Affordability drives sustainable growth: Lower entry prices and improved mortgage rates (five-year fixed at 3.95%) create broader buyer participation, strengthening the foundation for continued appreciation through 2030.[1][4]

- Comparable analysis requires regional specificity: Standard southern valuation techniques fail to capture Northern market dynamics, necessitating specialized adjustment factors for regeneration impact, transaction speed, and controlled inventory levels.

- Long-term projections favor Northern investment: Five-year cumulative growth forecasts reach 27% for Yorkshire & Humber and 25% for the North East, outpacing the UK average of 22% and creating opportunities for strategic investors.[4]

Understanding the Northern England Property Recovery: Market Fundamentals Driving Valuation Changes

The recovery sweeping across Northern England represents more than cyclical market movement. Structural economic changes, infrastructure investment, and demographic shifts have created conditions where traditional valuation approaches—calibrated for stable or declining markets—no longer accurately reflect true property worth.

Regional Growth Patterns Outpacing National Trends

The data presents an unmistakable picture. The North East's 6.8% annual price growth doesn't just exceed the England average; it represents the strongest regional performance in the country.[1] Within this broader trend, specific markets demonstrate even more remarkable appreciation:

- Northumberland: Exceeding 7% annual growth

- Sunderland: Above 7% appreciation

- Darlington: Surpassing 7% year-on-year increases[1]

Yorkshire & Humber's 3.7% growth, while more modest, still significantly outperforms the 2.2% national figure and demonstrates consistency across diverse property types.[1] For chartered surveyors conducting independent property valuations, these regional variations demand location-specific comparable selection rather than relying on broader regional averages.

Transaction Velocity as a Valuation Indicator

One of the most telling metrics for surveyor analysis involves time on market. Properties in leading Northern and Scottish markets are selling in just over two weeks on average—a stark contrast to southern regions where listings frequently extend beyond six months.[3] This rapid transaction velocity indicates several factors critical to valuation:

✅ Motivated buyer demand reflecting genuine value recognition

✅ Reduced negotiation leverage for purchasers, supporting asking prices

✅ Limited requirement for price reductions compared to stagnant markets

✅ Strong local economic confidence driving purchasing decisions

When surveyors analyze comparable sales, transaction speed provides crucial context. A property selling within 14 days at asking price carries different valuation weight than one requiring multiple price reductions over six months—even if final sale prices appear similar.

Mortgage Rate Improvements Supporting Affordability

Financial accessibility fundamentally shapes property valuations. The decline of five-year fixed mortgage rates to 3.95% in early 2026—the first time below 4% since September 2022—has materially improved buyer purchasing power.[1] With expectations of further 0.25-0.50 percentage point cuts anticipated throughout the year, affordability continues strengthening.

For a typical £200,000 Northern England property, the difference between a 5% and 3.95% mortgage rate represents approximately £125 monthly savings on a 25-year term. This improved affordability translates directly into sustainable demand that supports current valuations and justifies optimistic future projections.

"The combination of below-4% mortgage rates and Northern England's inherent affordability advantage creates a unique valuation environment where price growth can continue without overheating the market." — Regional Property Market Analysis, 2026[1]

Northern England Property Valuations 2026: RICS Surveyor Techniques for Comparable Analysis in Appreciating Markets

Traditional comparable sales analysis—the foundation of property valuation—requires significant adaptation when applied to Northern England Property Valuations 2026: Surveyor Techniques for Upward Price Trends in Recovering Markets. The methodologies that work effectively in stable or declining markets can systematically undervalue properties in regions experiencing genuine appreciation.

Selecting Appropriate Comparables in Fast-Moving Markets

The fundamental challenge surveyors face involves identifying truly comparable sales when market conditions change rapidly. A property sold six months ago in a market appreciating at 6.8% annually reflects a materially different valuation environment than current conditions.

Best practices for comparable selection in Northern markets include:

- Temporal proximity weighting: Prioritize sales within the most recent 3-month period, applying depreciation adjustments to older comparables based on documented regional growth rates

- Transaction speed filtering: Distinguish between properties selling quickly at asking price versus those requiring extended marketing and price reductions

- Regeneration proximity assessment: Account for infrastructure projects, transport improvements, and commercial development that may not yet be fully reflected in comparable sales

- Micro-market segmentation: Recognize that 7%+ growth in Northumberland may not apply uniformly across all neighborhoods within the region[1]

When conducting property valuations, chartered surveyors must document their comparable selection rationale with particular attention to market velocity and appreciation trends that distinguish Northern England from national patterns.

Adjustment Factors for Upward Price Trends

Standard valuation adjustments typically account for property-specific differences: size, condition, location amenities. In appreciating Northern markets, surveyors must additionally incorporate trend-based adjustments that reflect market momentum:

| Adjustment Category | Southern Stable Market | Northern Appreciating Market |

|---|---|---|

| Time adjustment | 0-1% quarterly | 1.5-1.7% quarterly (6.8% annual) |

| Condition premium | 5-10% for excellent | 8-15% for excellent (higher renovation demand) |

| Location desirability | Static multiplier | Dynamic multiplier reflecting regeneration |

| Transaction speed | Not typically considered | Premium for sub-14-day sales velocity |

The North East's 6.8% annual growth translates to approximately 1.7% quarterly appreciation.[1] A comparable sale from four months prior requires roughly a 2.3% upward adjustment purely for market movement—before considering property-specific factors.

Accounting for Controlled Inventory Dynamics

Unlike southern regions where 2026 began with the highest level of homes for sale in over eight years, Northern markets maintain controlled inventory levels.[1] Properties sitting unsold for more than six months remain modest in leading Northern and Scottish markets, limiting downward pressure on valuations.[3]

For surveyors, this inventory control has practical implications:

- Reduced distressed sale comparables: Fewer forced sales or motivated seller discounts that might artificially depress valuation benchmarks

- Seller pricing power: Limited inventory supports asking prices, reducing the discount between listing and sale prices

- Quality of comparables: Sales more likely to reflect genuine market value rather than circumstantial pricing

When assessing Level 2 or Level 3 survey requirements for valuation purposes, surveyors should consider how inventory constraints affect buyer due diligence urgency and negotiation dynamics.

Incorporating Regeneration and Infrastructure Impact

Northern England's property appreciation isn't occurring in a vacuum. Substantial regeneration investment, transport improvements, and commercial development create location-specific value drivers that generic valuation models fail to capture adequately.

Chartered surveyors must evaluate:

🏗️ Proximity to regeneration zones: Properties within 1km of major development projects often experience appreciation exceeding regional averages

🚆 Transport connectivity improvements: New rail links, station upgrades, and improved commuter routes materially affect residential desirability

🏢 Commercial investment indicators: Office development, retail improvements, and employment growth signal sustainable demand

📊 Planning pipeline analysis: Approved but not yet commenced projects represent future value drivers

For example, properties in Sunderland benefiting from waterfront regeneration and improved Newcastle connectivity demonstrate appreciation patterns distinct from the broader North East market—despite both exceeding 7% annual growth.[1]

Case Studies: Investor-Focused Valuation Approaches for Northern England Growth Markets

Understanding Northern England Property Valuations 2026: Surveyor Techniques for Upward Price Trends in Recovering Markets requires examining specific investment scenarios where valuation methodology directly impacts acquisition decisions and return projections.

Case Study 1: Yorkshire Buy-to-Let Portfolio Expansion

Scenario: A property investor seeks to expand their buy-to-let portfolio, comparing opportunities in Leeds (Yorkshire & Humber) versus similar investments in the South East.

Valuation considerations:

- Yorkshire & Humber demonstrates 3.7% annual growth versus stagnant southern markets[1]

- Five-year cumulative growth projection: approximately 27% for Yorkshire & Humber versus 22% UK average[4]

- Rental yields remain stronger due to lower entry prices relative to rental demand

- Transaction costs reduced by faster sales velocity (under 14 days average)[3]

Surveyor approach: When valuing comparable properties for investment purposes, chartered surveyors must project not just current market value but sustainable appreciation potential. A £150,000 Leeds property appreciating at 3.7% annually reaches approximately £180,000 within five years, while a £300,000 southern property growing at 2% reaches only £330,000—the Northern investment delivers superior percentage returns despite lower absolute price points.

For investors considering capital gains implications, the Northern England appreciation trajectory creates more favorable tax planning opportunities over medium-term holding periods.

Case Study 2: Northumberland Residential Development Site

Scenario: A developer evaluates a residential development site in Northumberland, where annual growth exceeds 7%.[1]

Valuation complexity:

- Existing use value versus development potential in rapidly appreciating market

- Planning timeline considerations when market grows 1.7% quarterly

- Comparable land sales becoming outdated within 3-month periods

- Infrastructure improvements affecting site desirability during development phase

Surveyor approach: Traditional residual valuation methods assume relatively stable end values. In Northumberland's 7%+ growth environment, surveyors must incorporate appreciation during the development timeline. A 24-month development cycle could see end values increase 14%+ from initial valuation, materially affecting land value calculations and development viability assessments.

This requires sensitivity analysis showing valuation ranges under different appreciation scenarios—conservative (4%), moderate (7%), and optimistic (10%)—to provide developers with risk-adjusted decision frameworks.

Case Study 3: Wigan First-Time Buyer Acquisition

Scenario: A first-time buyer seeks property in Wigan, identified by Zoopla as a top-performing location with 2-4% forecast annual growth and resilient market conditions.[3]

Valuation considerations:

- Affordability advantage: Northern property prices remain considerably below southern equivalents[3]

- Mortgage rate improvement to 3.95% enhances purchasing power[1]

- Rapid transaction velocity (14-day average) reduces negotiation leverage[3]

- Limited price reduction requirements compared to southern markets

Surveyor approach: For mortgage valuation purposes, chartered surveyors must balance conservative lending risk assessment with recognition of genuine market strength. A property selling at asking price within 14 days in a market demonstrating consistent appreciation represents lower risk than a property requiring multiple price reductions in a stagnant market—even if the latter has lower absolute price.

Understanding these property market legislation changes and their impact on valuation standards helps surveyors provide accurate assessments that reflect true market conditions rather than outdated assumptions based on southern market dynamics.

Case Study 4: Multi-Regional Investment Portfolio Rebalancing

Scenario: An institutional investor reviews their UK residential portfolio allocation, currently weighted toward London and South East holdings.

Strategic valuation analysis:

| Region | Current Allocation | 5-Year Growth Projection | Recommended Allocation |

|---|---|---|---|

| London/South East | 65% | 18-20% | 45% |

| Yorkshire & Humber | 10% | 27% | 25% |

| North East | 5% | 25% | 15% |

| Other regions | 20% | 22% average | 15% |

Surveyor approach: Portfolio-level valuation requires assessing not just individual property values but regional risk-adjusted return profiles. Yorkshire & Humber's projected 27% five-year growth and the North East's 25% projection significantly outpace the UK average of 22%.[4]

For institutional investors, chartered surveyors must provide comparative regional analysis demonstrating how Northern England's superior affordability, controlled inventory, and infrastructure investment create more favorable risk-return profiles than traditionally favored southern markets.

Advanced Surveyor Techniques: Data Analytics and Market Intelligence for Northern England Valuations

Modern property valuation extends beyond traditional comparable analysis. Chartered surveyors working in Northern England's appreciating markets increasingly rely on data analytics, predictive modeling, and comprehensive market intelligence to provide accurate valuations that reflect both current conditions and sustainable future trends.

Leveraging Transaction Data Analytics

The rapid transaction velocity in Northern markets—properties selling within 14 days on average—generates substantial data that sophisticated surveyors can analyze for valuation insights:[3]

Key metrics to track:

- Listing-to-sale price ratios: Percentage achieved relative to asking price

- Days on market distribution: Identifying outliers that may indicate overpricing or property-specific issues

- Seasonal variation patterns: Understanding how Northern markets respond to traditional seasonal cycles

- Buyer demographic trends: First-time buyers, investors, relocators from southern regions

By maintaining proprietary databases of regional transactions, surveying firms can identify micro-trends before they appear in published indices, providing clients with more timely and accurate valuations.

Incorporating Economic Indicators Beyond Property Data

Property values don't exist in isolation. Northern England's appreciation reflects broader economic strengthening that surveyors must monitor:

📈 Employment growth rates in key Northern cities

💼 Commercial investment levels indicating business confidence

🎓 University enrollment trends affecting rental demand in cities like Leeds, Manchester, Newcastle

🏭 Manufacturing and logistics sector expansion driving employment-based housing demand

🚄 HS2 and Northern Powerhouse infrastructure progress affecting connectivity and desirability

For example, when valuing properties in areas benefiting from Northern Powerhouse Rail improvements, surveyors should reference transport infrastructure impact studies showing typical property appreciation of 10-25% within 1km of new stations—above baseline regional growth rates.

Predictive Modeling for Long-Term Valuations

Traditional valuations provide point-in-time assessments. Investors and developers increasingly require forward-looking valuations that project sustainable appreciation trajectories.

Yorkshire & Humber's projected 27% cumulative growth through 2030 and the North East's 25% projection provide baseline assumptions.[4] However, sophisticated surveyor analysis segments these projections by:

- Property type: Terraced houses versus apartments versus detached homes

- Price bracket: Entry-level versus mid-market versus premium properties

- Location tier: City center versus suburban versus rural/commuter

- Tenure type: Freehold versus leasehold considerations

This granular approach recognizes that not all Northern England properties will appreciate uniformly, even within high-growth regions. Entry-level properties in regeneration areas may exceed 30% five-year growth, while premium rural properties might achieve 18-20%—both outperforming national averages but requiring different valuation approaches.

Risk Assessment in Appreciating Markets

Rapid appreciation creates valuation risks that chartered surveyors must address transparently:

⚠️ Sustainability concerns: Can 6.8% annual growth continue, or does it represent catch-up appreciation that will moderate?

⚠️ Economic sensitivity: How would Northern markets respond to recession or employment shocks?

⚠️ Mortgage rate dependency: What happens if rates rise back above 5%?

⚠️ Supply response: Could increased construction moderate appreciation?

Professional valuations should include sensitivity analysis showing value ranges under different scenarios. For the North East's 6.8% growth, this might include:[1]

- Conservative scenario: Growth moderates to 3-4% annually (still above national average)

- Base case scenario: Continued 5-6% growth reflecting sustained economic improvement

- Optimistic scenario: Acceleration to 8-10% as southern buyers increasingly relocate

This approach provides clients with realistic expectations while acknowledging the genuine strength of Northern England's property recovery.

Regulatory Compliance and Professional Standards for Northern England Valuations

RICS (Royal Institution of Chartered Surveyors) standards apply uniformly across all UK regions, but their application in Northern England Property Valuations 2026: Surveyor Techniques for Upward Price Trends in Recovering Markets requires careful attention to regional market dynamics and transparent methodology disclosure.

RICS Red Book Compliance in Appreciating Markets

The RICS Valuation – Global Standards (Red Book) mandates specific requirements that take on particular importance in rapidly appreciating markets:

Market value definition: "The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion."

In Northern markets where properties sell within 14 days, "proper marketing" timelines differ from southern regions requiring extended listing periods.[3] Surveyors must document that rapid sales reflect genuine market conditions rather than inadequate marketing or distressed circumstances.

Assumptions and special assumptions: When valuing properties in regeneration areas or locations benefiting from planned infrastructure, surveyors must clearly state assumptions about:

- Completion timelines for nearby development projects

- Planning permission likelihood for development sites

- Infrastructure delivery schedules affecting connectivity

- Economic growth sustainability in the region

These assumptions should reference credible sources—government infrastructure plans, published regeneration strategies, employment forecasts—rather than speculative projections.

Disclosure Requirements for Methodology Variations

When applying Northern England-specific valuation techniques that differ from standard approaches, RICS standards require clear disclosure:

✓ Comparable selection criteria: Explaining temporal weighting toward recent sales

✓ Adjustment methodology: Documenting how quarterly appreciation factors are calculated

✓ Regional data sources: Identifying market intelligence beyond standard indices

✓ Limitations and uncertainties: Acknowledging where insufficient comparable data exists

This transparency ensures that valuation users—whether lenders, investors, or individual buyers—understand both the methodology and its limitations.

Mortgage Lending Valuations: Balancing Accuracy and Prudence

For mortgage purposes, surveyors face the challenge of providing accurate valuations that reflect genuine Northern England appreciation while maintaining appropriate lending prudence. With five-year fixed rates at 3.95% and further cuts anticipated, lenders increasingly recognize Northern markets as lower-risk than previously assumed.[1]

However, mortgage valuations should still incorporate:

- Conservative comparable selection: Favoring completed sales over pending transactions

- Moderate appreciation assumptions: Using documented regional growth rates rather than optimistic projections

- Property-specific risk factors: Condition issues, location concerns, or market segment weaknesses

- Exit strategy considerations: Ensuring properties would remain saleable if market conditions change

The goal is valuations that support sustainable lending while recognizing the genuine strength of Northern England's property recovery—avoiding both excessive conservatism that undervalues properties and optimistic overvaluation that creates lending risk.

Future Outlook: Sustaining Valuation Accuracy Through 2030

The five-year projections showing Yorkshire & Humber achieving approximately 27% cumulative growth and the North East reaching 25%—both significantly outpacing the UK average of 22%—create both opportunities and challenges for chartered surveyors.[4]

Monitoring Leading Indicators for Continued Growth

Surveyors must track indicators that signal whether Northern England's appreciation will continue, moderate, or potentially reverse:

Positive indicators supporting continued growth:

- Mortgage rate reductions continuing as forecast (additional 0.25-0.50 percentage points)[1]

- Employment growth in key Northern cities exceeding national averages

- Infrastructure investment proceeding on schedule

- Net migration into Northern regions from southern England

- Commercial property investment indicating business confidence

Warning indicators suggesting moderation:

- Inventory levels rising significantly above current controlled levels

- Transaction velocity slowing from sub-14-day averages[3]

- Mortgage approval rates declining in Northern regions

- Major employer redundancies or business relocations

- Government infrastructure spending reductions

By systematically monitoring these indicators, surveyors can adjust valuation methodologies proactively rather than relying on lagging price indices.

Adapting to Market Maturation

As Northern England markets mature and appreciation potentially moderates from current 6.8% levels toward more sustainable long-term rates, valuation techniques must evolve accordingly:[1]

Early appreciation phase (current): Emphasis on transaction velocity, regeneration impact, comparative regional analysis

Maturation phase (2027-2028): Transition toward more traditional comparable analysis with moderate growth adjustments

Equilibrium phase (2029-2030): Standard valuation techniques with Northern England established as premium market

This evolution requires surveyors to remain flexible, continuously updating methodologies to reflect current market conditions rather than applying outdated approaches designed for different market phases.

Professional Development for Regional Specialization

The distinct characteristics of Northern England Property Valuations 2026: Surveyor Techniques for Upward Price Trends in Recovering Markets suggest value in regional specialization. Chartered surveyors focusing on Northern markets should pursue:

- Local market immersion: Regular site visits, attendance at regional property events, relationships with local agents

- Data analytics capabilities: Investment in technology for transaction analysis and predictive modeling

- Infrastructure knowledge: Understanding of Northern Powerhouse, HS2, and regional regeneration initiatives

- Economic literacy: Familiarity with regional employment trends, demographic shifts, and business investment patterns

This specialization enables more accurate valuations than generic approaches applied uniformly across diverse UK markets.

Conclusion

Northern England Property Valuations 2026: Surveyor Techniques for Upward Price Trends in Recovering Markets represents a fundamental shift in UK property dynamics. The North East's impressive 6.8% annual growth and Yorkshire & Humber's 3.7% appreciation—both significantly outpacing the national 2.2% average—demand specialized surveyor approaches that recognize regional distinctiveness rather than applying outdated assumptions based on southern market conditions.[1]

The evidence is compelling: properties selling within two weeks, mortgage rates below 4% for the first time since 2022, controlled inventory levels limiting downward pressure, and five-year projections showing 25-27% cumulative growth.[1][3][4] These aren't temporary anomalies but structural changes driven by affordability advantages, infrastructure investment, and economic regeneration.

For chartered surveyors, the implications are clear:

✅ Temporal weighting toward recent comparables becomes essential in markets appreciating 1.7% quarterly

✅ Transaction velocity analysis provides crucial context for valuation accuracy

✅ Regeneration proximity assessment captures value drivers absent from standard models

✅ Regional economic monitoring enables proactive methodology adjustments

✅ Transparent disclosure of Northern-specific techniques maintains RICS compliance

Actionable Next Steps

For property investors: Commission valuations from chartered surveyors with demonstrated Northern England expertise and request detailed comparable analysis showing regional appreciation trends. Consider portfolio rebalancing toward Yorkshire & Humber and North East markets offering superior five-year growth projections.

For homebuyers: Understand that rapid transaction velocity (14-day averages) reduces negotiation leverage—obtain professional property valuations before making offers to ensure fair pricing in competitive markets.

For developers: Incorporate quarterly appreciation factors into residual valuations for sites in high-growth areas like Northumberland, Sunderland, and Darlington where annual growth exceeds 7%.[1]

For surveyors: Invest in regional data analytics capabilities, maintain current knowledge of infrastructure projects and regeneration initiatives, and develop transparent methodologies for upward trend adjustments that comply with RICS standards while reflecting genuine market conditions.

The Northern England property recovery isn't speculation—it's documented reality supported by transaction data, mortgage improvements, and economic fundamentals. Valuation techniques must evolve to match this new reality, ensuring accuracy for all market participants navigating these dynamic and opportunity-rich markets.

References

[1] Regional Property Market Update Spring 2026 North East Yorkshire And The Humber – https://www.stevegooch.co.uk/blog-box-view/1454924560/1772628358/regional-property-market-update-spring-2026-north-east-yorkshire-and-the-humber?from_page=%2Fnews&post_width=contained

[2] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/

[3] Why Northern England And Scotland Are Set To Lead Uk House Price Growth In 2026 – https://www.belvoir.co.uk/guides/news/why-northern-england-and-scotland-are-set-to-lead-uk-house-price-growth-in-2026/

[4] Uk Price Forecasts – https://investropa.com/blogs/news/uk-price-forecasts