When purchasing a property in 2026, understanding the difference between leasehold and freehold tenure isn't just legal jargon—it directly impacts how much your property is worth today and what it will be valued at tomorrow. Leasehold vs Freehold Valuations: How Tenure, Ground Rent and Short Leases Really Affect Your Property Value represents one of the most significant yet misunderstood factors in the UK property market. Whether you're a first-time buyer, seasoned investor, or homeowner considering a sale, the tenure type can mean the difference between a property that appreciates steadily and one that loses value year after year.

Chartered valuation surveyors assess properties with short leases, escalating ground rents, and complex service charges very differently from freehold equivalents. These professionals apply specific valuation methodologies that account for lease length, marriage value, ground rent capitalization, and future liabilities—factors that can reduce a property's market value by 20-40% or more in extreme cases.

Key Takeaways

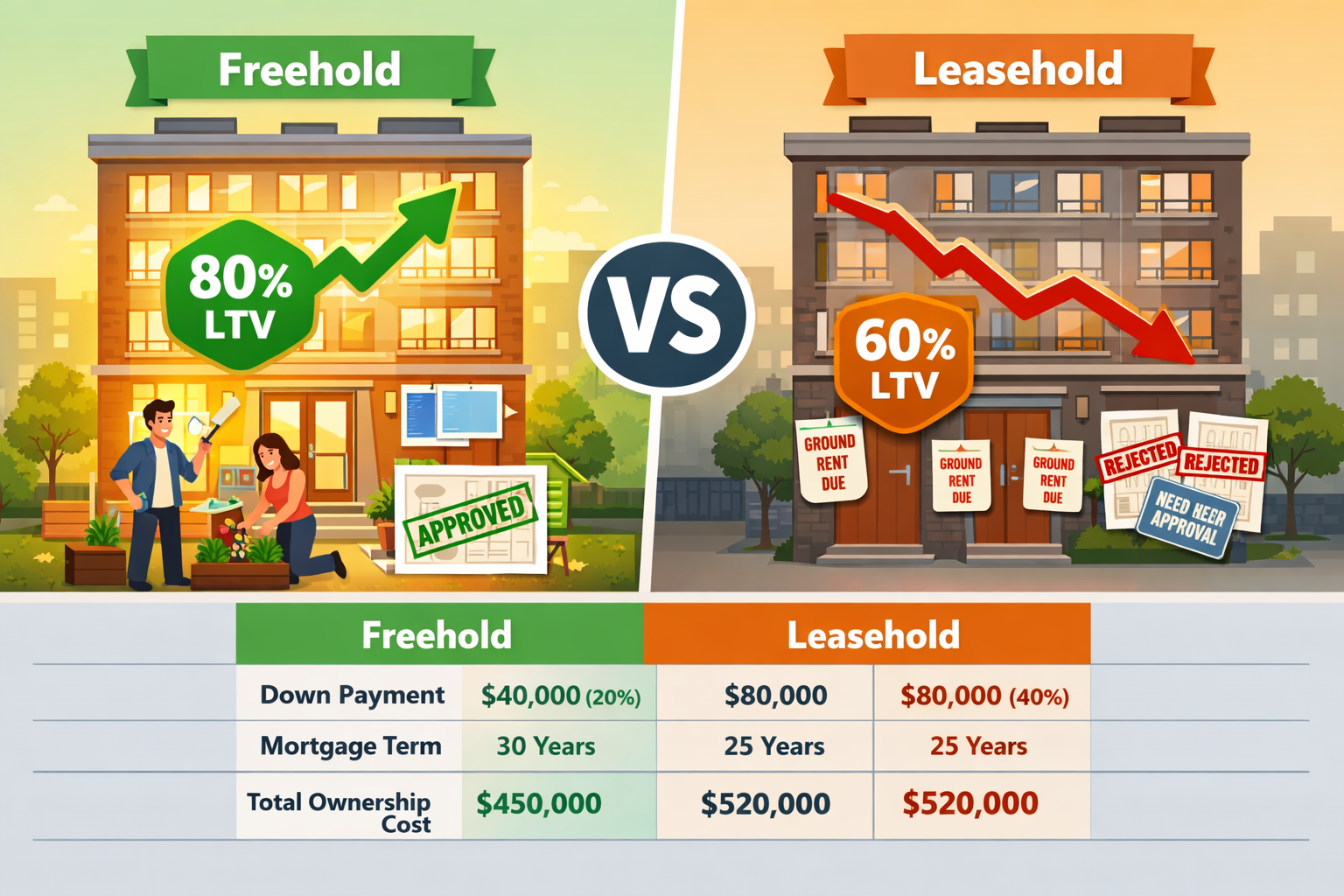

✅ Freehold properties dominate the market with approximately 70% of residential sales, offering superior liquidity, stronger appreciation potential, and better mortgage terms (80% LTV vs 60% for leaseholds)[1]

✅ Short leases dramatically reduce property value—properties with less than 80 years remaining face exponential value decline, with those under 60 years becoming nearly unmortgageable

✅ Ground rent and service charges create ongoing financial obligations that chartered surveyors capitalize into their valuations, directly reducing the property's market worth

✅ Mortgage lenders treat leasehold properties as higher risk, requiring larger deposits (40% vs 20% for freehold) and offering shorter mortgage terms (15-20 years vs 25 years)[1]

✅ The 2026 Leasehold Reform Act introduces significant changes including peppercorn ground rents on lease extensions, making professional valuation advice more critical than ever[4]

Understanding Freehold vs Leasehold: The Fundamental Difference

What Is Freehold Ownership?

Freehold ownership grants perpetual rights to both the property and the land it sits on. Freeholders enjoy complete autonomy over their asset, subject only to planning regulations and building codes. This ownership structure means:

- 🏡 Unlimited ownership duration with no expiry date

- 🔧 Full control over alterations without requiring third-party approval

- 💰 No ground rent or service charges to external landlords

- 📈 Benefit from land value appreciation over time

Freehold properties comprised approximately 70% of residential sales as of 2025, indicating broader market liquidity and stronger investor demand[1]. This dominance reflects both buyer preference and lender confidence in perpetual asset value.

What Is Leasehold Ownership?

Leasehold ownership provides the right to occupy and use a property for a fixed term (typically 99-999 years), while the freeholder retains ownership of the land. Leaseholders face several constraints:

- ⏰ Fixed lease terms that diminish over time

- 💷 Ground rent obligations to the freeholder

- 🧾 Service charges for building maintenance and management

- 🚫 Restrictions on modifications requiring freeholder consent

- 📉 Declining asset value as lease term shortens

Leasehold properties lack land appreciation potential since leaseholders do not own the land; consequently, property value can remain stagnant with no benefit from land value appreciation over time[2]. For professional property valuations that account for these complexities, chartered surveyors apply specialized assessment techniques.

How Chartered Surveyors Value Leasehold Properties

The Lease Length Factor

Lease length represents the single most critical factor in leasehold valuations. Chartered surveyors apply different valuation approaches based on remaining term:

| Remaining Lease Term | Valuation Impact | Mortgage Availability | Market Liquidity |

|---|---|---|---|

| 80+ years | Minimal discount (0-5%) | Standard terms available | High |

| 70-80 years | Moderate discount (5-15%) | Limited lenders | Moderate |

| 60-70 years | Significant discount (15-25%) | Very limited | Low |

| Under 60 years | Severe discount (25-40%+) | Nearly unmortgageable | Very low |

Properties with less than 80 years remaining trigger the "marriage value" calculation—the additional value created when the lease is extended. This marriage value must be shared 50/50 between leaseholder and freeholder, effectively reducing the leaseholder's equity position.

Ground Rent Capitalization

Chartered surveyors capitalize ground rent into their valuations by treating it as an income stream that reduces the property's capital value. The calculation involves:

- Annual ground rent amount × Years' Purchase multiplier (typically 12-20 depending on review terms)

- Deduction from comparable freehold values

For example, a property with £500 annual ground rent using a 15 Years' Purchase multiplier would see a £7,500 reduction in valuation (£500 × 15 = £7,500). Properties with escalating ground rent clauses—particularly those doubling every 10-25 years—face exponentially higher deductions.

The 2026 Leasehold Reform Act ensures that ground rent is reduced to a "peppercorn" (effectively zero) when extending leases[4], but existing ground rents on unexpired leases continue to affect valuations until extension.

Service Charge Assessment

Service charges represent ongoing liabilities that surveyors must assess when valuing leasehold properties. Key considerations include:

- 📊 Historical trends in annual service charge increases

- 🏢 Building condition and anticipated major works

- 🔍 Reserve fund adequacy for future repairs

- ⚖️ Management structure (freeholder-controlled vs resident-managed)

In many leasehold buildings, the ground landlord sets service charges unilaterally, often including their own management charges, creating less transparent and potentially higher ongoing costs[1]. Surveyors review service charge management documentation to assess future liability risk.

Properties with poorly maintained common areas, inadequate sinking funds, or upcoming major works (roof replacement, lift modernization, cladding remediation) may face significant valuation discounts of 10-30% depending on the anticipated costs.

Leasehold vs Freehold Valuations: Real-World Impact on Property Value

Price Appreciation Differences

Market data demonstrates substantial appreciation advantages for freehold properties. While specific to Dubai markets, the trend is consistent globally: freehold villa prices in prime communities increased by up to 15% year-on-year (2023-2025 period), substantially outpacing the 9% average growth across the wider residential market[1].

UK market analysis shows similar patterns, with freehold houses in desirable locations consistently outperforming leasehold flats in capital appreciation. The perpetual nature of freehold ownership allows properties to benefit from:

- 🌍 Land scarcity in urban areas

- 🏗️ Development potential and extension possibilities

- 🎯 Broader buyer appeal including investors and families

- 💪 Stronger negotiating position in sales

Mortgage and Financing Implications

Lending terms vary dramatically between freehold and leasehold properties, directly impacting affordability and market value:

Freehold advantages:

- 80% loan-to-value (LTV) ratio available for residents

- Mortgage tenures up to 25 years

- Lower interest rates reflecting reduced risk

- Down payment: £200,000 on a £1,000,000 property[1]

Leasehold constraints:

- 60% LTV ratio (or lower for short leases)

- Mortgage ceilings of 15-20 years typical

- Higher interest rates due to perceived depreciation risk

- Down payment: £400,000 on a £1,000,000 property[1]

This double down payment burden severely impacts cash flow and investment deployment capacity. For buyers requiring financing, the additional £200,000 equity requirement on a £1,000,000 leasehold purchase represents a significant barrier to entry.

When preparing your property for market, understanding these financing constraints helps set realistic price expectations.

Investment Returns: Rental Yield vs Capital Growth

Interestingly, leasehold properties can generate higher rental yields—averaging 15-20% annually compared to freehold counterparts—primarily due to lower initial investment requirements[2]. This creates different investment strategies:

Leasehold investment profile:

- ✅ Higher gross rental yields

- ✅ Lower entry costs

- ❌ Limited capital appreciation

- ❌ Declining asset value over time

- ⏱️ Best suited for short-term (5-10 year) investment horizons

Freehold investment profile:

- ✅ Strong capital appreciation potential

- ✅ Perpetual asset ownership

- ✅ Land value growth

- ❌ Lower initial yields

- 📅 Optimal for long-term wealth accumulation

Leasehold properties older than 30 years may stagnate or depreciate in value, making them generally more suited for shorter-term investment purposes rather than long-term wealth accumulation[2].

What Buyers Need to Know Before Instructing a Valuation

Critical Questions for Your Surveyor

Before commissioning a professional property valuation, buyers should prepare specific questions about leasehold properties:

- How many years remain on the lease? (Request exact calculation from the lease commencement date)

- What is the current ground rent, and does it escalate? (Review the exact escalation formula)

- What are the annual service charges, and what's the 5-year trend? (Request historical accounts)

- Are there any planned major works or Section 20 notices? (Check for upcoming capital expenditure)

- What is the marriage value calculation if extending? (Understand the total cost of lease extension)

- Does the freeholder have a track record of reasonable lease extensions? (Research their negotiation history)

- Are there any restrictions on subletting or alterations? (Review lease covenants)

Understanding Marriage Value

Marriage value represents the increase in property value created when a short lease is extended to add years. When a lease falls below 80 years, the leaseholder must share 50% of this marriage value with the freeholder.

Example calculation:

- Current value with 70-year lease: £300,000

- Value with 150-year extended lease: £400,000

- Marriage value: £100,000

- Leaseholder's share to freeholder: £50,000

- Plus freeholder's loss of ground rent capitalized: £15,000

- Total extension cost: £65,000+ (plus legal and valuation fees)

Savvy buyers factor this cost into their purchase negotiations. If a property is marketed at £300,000 with a 70-year lease, the "true cost" including extension is actually £365,000+—making it potentially less attractive than a £350,000 freehold equivalent.

Red Flags in Leasehold Valuations

Chartered surveyors watch for specific warning signs that should concern buyers:

🚩 Doubling ground rents – Clauses that double ground rent every 10-25 years can make properties virtually unsellable

🚩 High service charges with poor transparency – Annual charges exceeding £3,000-£5,000 without detailed accounts

🚩 Absent or inadequate reserve funds – Buildings without sinking funds for major repairs

🚩 Freeholder in financial difficulty – Risk of poor building maintenance and difficult lease negotiations

🚩 Onerous lease restrictions – Prohibitions on pets, subletting, or home businesses that limit market appeal

🚩 Building safety issues – Cladding, fire safety defects, or structural problems requiring remediation

If your home valuation comes in less than expected, these leasehold factors are often the culprit.

What Sellers Should Know When Pricing Leasehold Properties

Pre-Sale Lease Extension Strategy

Sellers with leases approaching 80 years face a strategic decision: extend before selling or sell with a short lease at a discount. The mathematics often favor extending before sale:

Extending before sale:

- Costs £40,000-£80,000 (typical range for 70-80 year leases)

- Increases property value by £60,000-£120,000

- Net benefit: £20,000-£40,000

- Attracts more buyers and mortgage lenders

- Faster sale completion

Selling with short lease:

- Reduced buyer pool (cash buyers only below 60 years)

- 20-40% price discount required

- Longer marketing period

- Buyers negotiate aggressively knowing extension costs

For property development projects or investment portfolios, lease extension timing becomes a critical value optimization strategy.

Transparent Documentation

Sellers should prepare comprehensive documentation for buyer due diligence:

- ✅ Complete lease deed with all supplemental deeds

- ✅ Last 3-5 years of service charge accounts

- ✅ Building insurance documentation

- ✅ Reserve fund statements

- ✅ Section 20 notices (major works consultations)

- ✅ Ground rent payment history

- ✅ Freeholder contact details and management company information

- ✅ Any correspondence about building issues

Transparency builds buyer confidence and supports the asking price during negotiations.

The 2026 Leasehold Reform Act: What's Changed

Peppercorn Ground Rent on Extensions

The landmark Leasehold and Freehold Reform Act 2024 (taking full effect in 2026) introduces several buyer-friendly provisions[4]:

Key reforms:

- 🎯 Ground rent reduced to "peppercorn" (£0) on all lease extensions

- 📏 Increased standard lease extension from 90 to 990 years for flats

- 💰 Removal of marriage value for leases above 80 years (proposed)

- 🏠 Right to buy freehold for more leaseholders

- 📋 Improved transparency on service charges and fees

These reforms significantly improve the economics of lease extensions, but only apply to new extensions—existing ground rents on unexpired leases continue until the leaseholder exercises their extension rights.

Valuation Implications Post-Reform

Chartered surveyors must now account for:

- Reduced extension costs making short leases less problematic

- Increased buyer confidence in leasehold properties

- Potential compression of the discount between freehold and leasehold values

- Transition period uncertainty as reforms are implemented

However, service charges, building quality, and management standards remain critical valuation factors unaffected by the reforms.

Investor Considerations: When Leasehold Makes Sense

Despite the challenges, leasehold properties can offer compelling investment opportunities in specific circumstances:

High-Yield Short-Term Strategies

Investors seeking cash flow over capital appreciation may find leasehold properties attractive:

- 🏙️ Prime city center locations with strong rental demand

- 🎓 Student accommodation near universities

- 💼 Corporate lets for business travelers

- 📅 5-10 year investment horizons before lease becomes problematic

The 15-20% annual rental returns[2] can exceed freehold alternatives, particularly when purchasing at a discount due to lease length.

Value-Add Lease Extension Plays

Sophisticated investors purchase properties with 60-75 year leases at significant discounts, immediately extend the lease, and either:

- 🔄 Resell at freehold-equivalent values (capturing the discount)

- 🏠 Hold for improved rental yields on a secure long lease

This strategy requires:

- ✅ Access to extension capital (£40,000-£100,000+)

- ✅ Understanding of marriage value calculations

- ✅ Relationship with cooperative freeholders

- ✅ Professional surveyor and legal support

Conclusion: Making Informed Decisions on Leasehold vs Freehold Valuations

Understanding Leasehold vs Freehold Valuations: How Tenure, Ground Rent and Short Leases Really Affect Your Property Value empowers buyers, sellers, and investors to make financially sound decisions in 2026's complex property market. The tenure type fundamentally shapes mortgage availability, ongoing costs, capital appreciation potential, and ultimate resale value.

Freehold properties offer superior long-term wealth accumulation, stronger appreciation, better financing terms, and complete autonomy—explaining their 70% market dominance[1] and premium pricing. Leasehold properties can provide higher initial yields and lower entry costs, but require careful assessment of lease length, ground rent structures, service charge trajectories, and extension costs.

Action Steps for Property Stakeholders

For buyers:

- Instruct a chartered surveyor to assess lease terms and calculate total ownership costs

- Factor lease extension costs into your maximum purchase price

- Verify mortgage availability before making offers on properties with less than 80 years remaining

- Review service charge accounts and building maintenance standards

- Consider the 2026 reforms when evaluating short leases

For sellers:

- Obtain a professional valuation accounting for all lease factors

- Consider extending leases below 85 years before marketing

- Prepare comprehensive documentation for buyer due diligence

- Price realistically based on comparable leasehold sales, not freehold equivalents

- Highlight any favorable lease terms or recent building improvements

For investors:

- Match property tenure to your investment horizon (short-term: leasehold possible; long-term: freehold preferred)

- Calculate total returns including both yield and anticipated capital appreciation

- Assess lease extension opportunities for value-add strategies

- Diversify across tenure types to balance cash flow and growth

- Monitor regulatory changes affecting leasehold valuations

The expertise of chartered valuation surveyors becomes invaluable when navigating these complexities. Professional assessment ensures you understand exactly how tenure, ground rent, service charges, and lease length affect the property's true market value—protecting you from overpaying or underpricing in today's sophisticated property market.

Whether you're purchasing your first home, selling an investment property, or building a portfolio, recognizing how leasehold and freehold valuations differ represents essential knowledge for successful property ownership in 2026 and beyond.

References

[1] Freehold Vs Leasehold – https://www.ritukant.com/freehold-vs-leasehold/

[2] Exploring Freehold Vs Leasehold Uno Properties Insights – https://unoproperties.co/article/exploring-freehold-vs-leasehold-uno-properties-insights/

[3] Freehold Vs Leasehold Property Understand The Legal Differences – https://hello.pricelabs.co/freehold-vs-leasehold-property-understand-the-legal-differences/

[4] The Leasehold Freehold Reform Act What 2026 Buyers Need To Know – https://www.gorvinsresidential.com/the-leasehold-freehold-reform-act-what-2026-buyers-need-to-know/