The UK data centre sector is experiencing unprecedented growth in 2026, creating both extraordinary opportunities and complex challenges for chartered surveyors. As artificial intelligence workloads drive demand for high-density computing facilities, the traditional approaches to property valuation are being tested like never before. Data Centre Boom and Valuation Challenges: Chartered Surveyor Strategies for High-Density UK Sites in 2026 represents a critical intersection of technology infrastructure, real estate expertise, and financial assessment that requires sophisticated understanding of both physical assets and digital infrastructure.

The UK data centre market reached £17.24 billion in 2026 and is projected to surge to £31.99 billion by 2031, representing a compound annual growth rate of 13.17% [1]. This explosive expansion, fueled by hyperscaler cloud services and AI computing demands, has transformed data centres from niche industrial properties into premium investment assets requiring specialized valuation expertise.

Key Takeaways

- 💰 Market expansion: The UK data centre market is projected to grow from £17.24 billion in 2026 to £31.99 billion by 2031, with London alone targeting 5.16 gigawatts of capacity

- 🏗️ Mega campus dominance: Facilities exceeding 40 MW are advancing at 27.60% CAGR, fundamentally changing valuation approaches and creating consolidation pressure on medium-sized assets

- ⚡ Power-centric valuation: Traditional square footage metrics are being replaced by power capacity (MW) and rack density (kW) as primary value drivers

- 🔧 RICS compliance challenges: Chartered surveyors must integrate specialized technical assessments of cooling systems, electrical infrastructure, and AI-readiness into standard valuation frameworks

- 📍 Geographic stratification: East London's Royal Docks and established hubs like Slough show divergent investment profiles requiring location-specific valuation strategies

Understanding the Data Centre Boom and Market Dynamics in 2026

The Scale of UK Data Centre Growth

The transformation of the UK data centre landscape represents one of the most significant shifts in commercial property markets this decade. London's data centre market alone reached 2.77 gigawatts in 2026 and is forecast to expand to 5.16 gigawatts by 2031, growing at a 13.21% CAGR [2]. This capacity expansion reflects not just incremental growth but a fundamental restructuring of digital infrastructure.

The UK government has set ambitious targets, aiming for 6 GW of AI-capable data centre capacity by 2030, alongside a 20% increase in total sites during this period [3]. These targets underscore the strategic importance of data infrastructure to national economic competitiveness and create a favorable regulatory environment for investment.

The Mega Campus Revolution

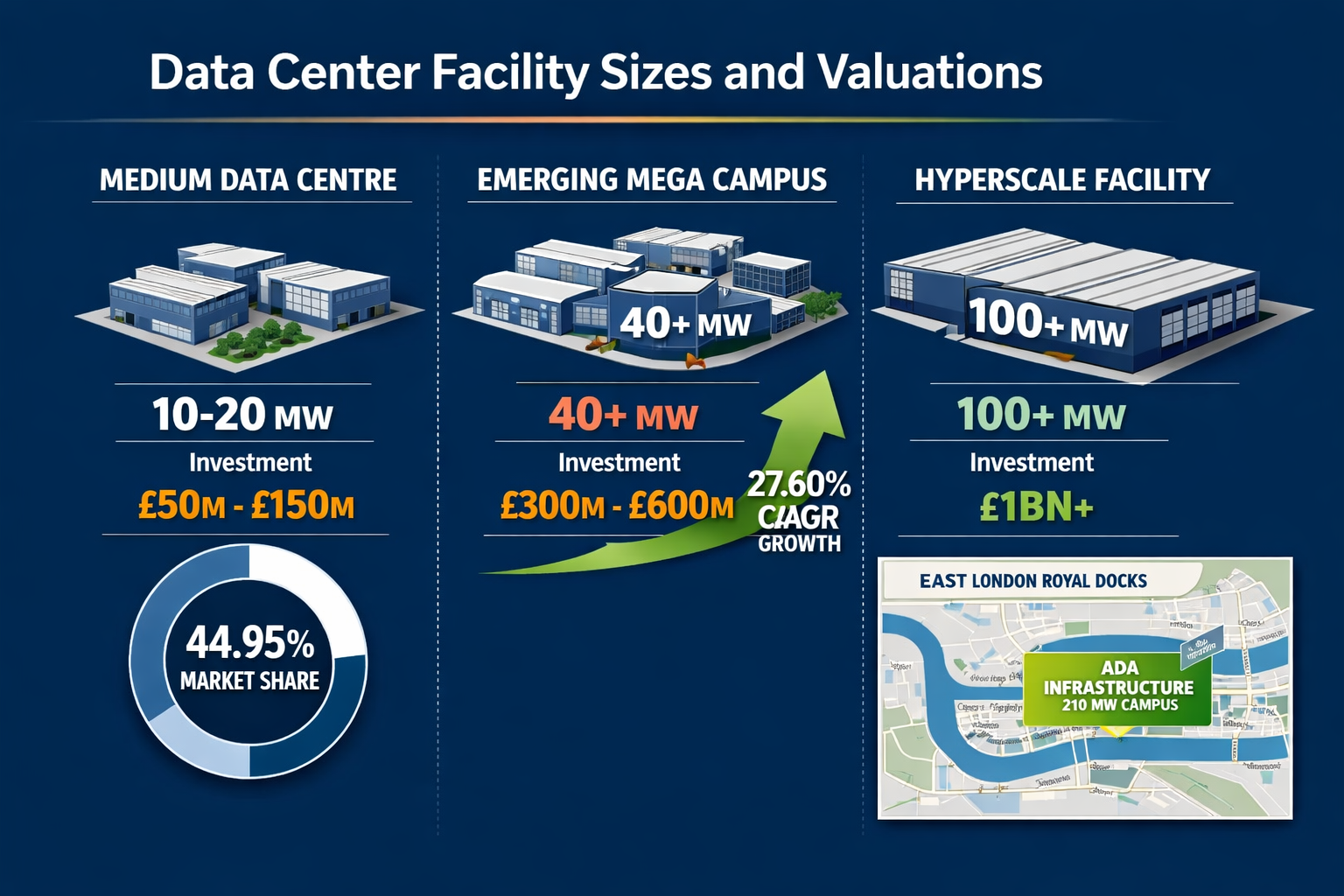

Perhaps the most significant structural change affecting valuations is the shift toward mega campuses. While facilities between 10-20 MW led capacity in 2025 with 44.95% market share, momentum has decisively shifted toward mega campuses exceeding 40 MW, which are projected to advance at 27.60% CAGR between 2026-2031 [2].

This consolidation trend creates profound implications for chartered surveyors. Mega campus investors bundle multiple data halls into single planning envelopes, reducing per-megawatt capital expenditure and shortening time-to-revenue. The London data centre market for mega facilities is forecast to double, lifting their revenue contribution above one-third of total by decade's end [2].

Operators of medium-sized assets now face critical decisions: invest substantial capital to upgrade to 30 kW racks and AI-ready infrastructure, or risk declining occupancy as hyperscale workloads bypass their facilities. This pressure is driving mergers, asset sales, and creating valuation complexities for chartered surveyors across Hertfordshire and surrounding regions.

Geographic Hotspots and Investment Patterns

East London's Royal Docks district is rapidly emerging as a new powerhouse for data centre development. Ada Infrastructure's 210 MW campus has become the bellwether for the region, receiving planning approval that integrated community skills hubs and river-water cooling systems. East London's share of the London data centre market is projected to climb from single digits to mid-teens over the next five years [2].

Traditional hubs continue to dominate, however. Equinix, Digital Realty, and NTT collectively hold over 45% of installed megawatts in London through their interconnected campuses [2]. Digital Realty's July 2024 Slough acquisition advanced its metro footprint to 14 facilities, while NTT's May 2025 land purchase for LON2 positions London as its EMEA flagship.

For surveyors working across Central London, Islington, and South East London, understanding these geographic investment patterns is essential for accurate comparable analysis.

Hyperscaler Dominance and AI Workloads

Within London's colocation market, hyperscale-focused formats held 41.60% in 2025 and are advancing at 23.90% CAGR [2]. More significantly, hyperscalers' self-built campuses are projected to outstrip every other archetype at 14.55% CAGR, reflecting surging AI inference and sovereign-cloud workloads [2].

AI and GPU-driven high-density compute requirements are contributing +4.8% to CAGR forecasts, with particular concentration in London's financial district and wider metropolitan area. Hyperscaler cloud expansion demand contributes +5.2% to CAGR forecasts, primarily in Slough and Docklands [2].

"The shift from traditional colocation to hyperscale and AI-optimized facilities represents a fundamental change in how we assess data centre value. Power density per rack has become as important as total square footage."

Data Centre Boom and Valuation Challenges: Technical Assessment Requirements

Power Capacity as the Primary Value Driver

Traditional commercial property valuation relies heavily on square footage, location, and construction quality. Data centres upend this framework by making electrical capacity the primary value determinant. A facility with modest floor space but robust electrical infrastructure and cooling capacity commands premium valuations compared to larger buildings with limited power delivery.

Chartered surveyors must now assess:

- Total power capacity (measured in megawatts)

- Available vs. committed capacity (critical for revenue projections)

- Power Usage Effectiveness (PUE) ratios (efficiency metric affecting operating costs)

- Rack density capabilities (kW per rack, with 30+ kW increasingly standard for AI workloads)

- Redundancy levels (N, N+1, 2N configurations affecting reliability and value)

For professional valuation services, integrating these technical specifications into RICS-compliant reports requires collaboration with electrical engineers and data centre specialists.

Cooling Infrastructure Assessment

Modern high-density data centres generate extraordinary heat loads. A single AI-optimized rack can produce thermal output equivalent to several residential properties. Cooling infrastructure has evolved from simple air conditioning to sophisticated systems including:

- Direct liquid cooling (DLC) for GPU clusters

- Rear-door heat exchangers for high-density racks

- Free cooling utilizing ambient air temperatures

- River-water cooling systems (as deployed at Ada Infrastructure's Royal Docks campus)

- Adiabatic cooling and evaporative systems

Surveyors must evaluate not just the presence of cooling systems but their scalability, efficiency, and alignment with tenant requirements. A facility designed for traditional 5-8 kW racks faces expensive retrofitting to accommodate 30+ kW AI workloads, directly impacting valuation.

Grid Connectivity and Power Resilience

The UK's electrical grid faces capacity constraints in key data centre markets. Grid connection availability has become a critical valuation factor, with some sites experiencing multi-year delays for power upgrades.

Assessment criteria include:

- Existing grid connection capacity and available headroom

- Substation proximity and upgrade pathways

- Backup power systems (diesel generators, battery storage, fuel cells)

- Renewable energy integration (on-site solar, power purchase agreements)

- Planning permissions for power infrastructure expansion

Properties with secured grid capacity or existing high-voltage connections command significant premiums. Conversely, sites requiring extensive utility upgrades face valuation discounts reflecting both capital costs and time delays.

Structural and Environmental Considerations

High-density computing creates unique structural demands. Floor loading requirements for data centres exceed typical commercial specifications, with some facilities requiring 2,000+ kg per square meter capacity for dense equipment installations.

Premium drone surveys can efficiently assess roof conditions for solar installations and cooling equipment, while structural engineering evaluations verify load-bearing capacity for planned equipment densities.

Environmental factors affecting valuation include:

- Flood risk (critical for low-lying sites like Docklands)

- Seismic considerations (though less significant in UK than other markets)

- Noise pollution from cooling systems (affecting planning compliance)

- Water availability for cooling systems

- Proximity to fiber routes and network interconnection points

RICS-Compliant Valuation Methodologies for Data Centre Boom Sites

Adapting Traditional Approaches to High-Density Assets

Chartered surveyors must adapt established RICS valuation methodologies to accommodate data centre-specific characteristics while maintaining professional standards and defensibility.

Comparable Method Adaptations

The comparable method remains foundational but requires significant modification:

Power-normalized comparables: Rather than price per square foot, surveyors increasingly use price per megawatt or price per rack metrics. A recent East London transaction might be analyzed as "£2.8 million per MW of IT load capacity" rather than traditional square footage pricing.

Stratification by facility type: Mega campuses (40+ MW), enterprise facilities (10-20 MW), and edge computing sites represent distinct sub-markets requiring separate comparable pools.

Geographic micro-markets: Proximity to fiber routes, grid capacity, and planning environments create significant value variations even within single boroughs. Sites near Watford or Hemel Hempstead may show different value dynamics than central London locations.

Lease structure analysis: Data centre leases often include complex power pricing, cross-connect fees, and service level agreements that significantly impact value beyond base rent.

Investment Method Refinements

The investment method requires careful analysis of:

Tenant covenant strength: Hyperscalers like AWS, Microsoft, and Google represent different risk profiles than smaller colocation tenants. Multi-tenant facilities require portfolio analysis of tenant mix and concentration risk.

Yield compression factors: Prime data centre assets in established markets have experienced yield compression, with some institutional-grade facilities trading below 4% net initial yields. Understanding market yield expectations across different facility types is essential.

Capex requirements: Future capital expenditure for cooling upgrades, power infrastructure, and technology refresh must be factored into net income projections. Facilities unable to support 30 kW racks face significant upgrade costs or revenue limitations.

Revenue growth assumptions: While traditional commercial properties might assume modest rental growth, data centre facilities serving AI workloads may justify higher growth assumptions based on capacity scarcity and demand fundamentals.

Depreciated Replacement Cost (DRC) Method

For specialized facilities with limited comparable transactions, the DRC method provides a robust framework:

Land value assessment: Evaluate based on alternative use value, grid capacity, and planning permissions for data centre development.

Building replacement cost: Calculate modern equivalent asset costs, including:

- Raised floor systems rated for equipment loads

- Redundant electrical distribution

- Cooling infrastructure sized for target rack densities

- Security systems and access controls

- Fire suppression systems (often sophisticated gas-based systems)

Specialist equipment: Assess replacement cost of:

- Uninterruptible power supply (UPS) systems

- Backup generators and fuel storage

- Cooling equipment (chillers, CRACs, heat exchangers)

- Network interconnection infrastructure

Depreciation factors: Apply depreciation for:

- Physical deterioration of building and equipment

- Functional obsolescence (inability to support modern rack densities)

- Economic obsolescence (market oversupply or technological shifts)

Optimization adjustments: Account for modern design efficiencies that would differ from the existing facility.

Specialized Valuation Scenarios

Development Site Valuation

Undeveloped sites with data centre potential require assessment of:

- Residual land value based on completed facility value minus development costs

- Grid capacity availability and connection costs

- Planning probability and timeline assumptions

- Development risk premium appropriate to market conditions

Sites in emerging markets like East London's Royal Docks command different risk premiums than established Slough locations.

Portfolio Valuations

For SIPP pension valuations or inheritance tax valuations involving data centre portfolios, surveyors must consider:

- Portfolio premium for geographic diversification

- Operational synergies between facilities

- Tenant concentration across the portfolio

- Staged disposal scenarios versus whole portfolio sale

Leasehold Interest Valuations

Data centre leasehold interests present unique challenges:

- Power allocation rights within multi-tenant facilities

- Expansion options and right-of-first-refusal clauses

- Service level agreement value and performance guarantees

- Interconnection rights and cross-connect revenue sharing

Due Diligence and Technical Verification

Robust valuation requires verification beyond financial analysis:

Technical due diligence partnerships: Engage specialist data centre consultants to verify:

- Electrical infrastructure capacity and condition

- Cooling system performance and efficiency

- Network connectivity and fiber routes

- Building management systems and monitoring

Operational review: Analyze historical PUE, uptime statistics, and maintenance records.

Planning and compliance verification: Confirm:

- Planning permissions for current and future capacity

- Environmental permits for cooling water discharge

- Noise compliance certificates

- Building regulations compliance for electrical and fire systems

Lease documentation review: Scrutinize service level agreements, power pricing structures, and tenant rights.

For chartered surveyors across Essex, Guildford, and other growth markets, establishing relationships with technical specialists is essential for credible valuations.

Risk Factors and Market Challenges in 2026

Grid Capacity Constraints

The UK's electrical grid faces significant capacity constraints in key data centre markets. Some sites experience multi-year delays for power upgrades, creating valuation uncertainty. Properties with secured grid capacity command premiums, while those dependent on future upgrades face discounts reflecting both capital costs and revenue delays.

The government's 6 GW AI-capable capacity target by 2030 [3] requires substantial grid investment. Surveyors must assess whether individual sites benefit from planned infrastructure upgrades or face competitive disadvantages.

Technological Obsolescence Risk

Data centre technology evolves rapidly. Facilities designed for traditional workloads face obsolescence as AI and high-density computing dominate demand. Medium-sized assets unable to retrofit to 30 kW racks risk declining occupancy [2], directly impacting valuations.

Surveyors must evaluate:

- Upgrade pathway feasibility and costs

- Remaining economic life of current configurations

- Competitive positioning against newer facilities

Regulatory and Environmental Pressures

Data centres face increasing scrutiny regarding:

- Energy consumption and carbon emissions

- Water usage for cooling systems

- Noise pollution from mechanical equipment

- Planning restrictions in residential areas

Properties with renewable energy integration, efficient cooling systems, and strong community relationships command premiums. Those facing regulatory challenges or environmental opposition experience valuation pressure.

Market Concentration and Competition

The dominance of Equinix, Digital Realty, and NTT with over 45% market share [2] creates competitive dynamics affecting smaller operators. Independent facilities may face challenges attracting hyperscale tenants who prefer established operators with proven reliability.

Conversely, specialist facilities serving niche markets (edge computing, sovereign data requirements) may command premiums despite smaller scale.

Financial Market Sensitivity

Data centre valuations reflect broader financial market conditions:

- Interest rate movements affect yield expectations and debt costs

- Infrastructure investment appetite drives transaction volumes

- Currency fluctuations impact international investor demand

- Economic growth forecasts influence demand projections

The projected growth from £17.24 billion in 2026 to £31.99 billion by 2031 [1] assumes continued economic expansion and technology adoption. Recession scenarios would pressure these forecasts and valuations.

Strategic Considerations for Chartered Surveyors

Building Specialist Expertise

Data centre valuation requires continuous professional development:

- Technical training in electrical systems, cooling technologies, and network infrastructure

- Market intelligence on transaction activity, lease structures, and yield trends

- Regulatory awareness of planning policies, environmental requirements, and grid development

- Relationship building with technical consultants, operators, and institutional investors

Professional organizations like RICS offer specialized courses, while industry conferences provide networking and market insight.

Developing Robust Valuation Frameworks

Establishing standardized internal frameworks ensures consistency and defensibility:

- Comparable databases tracking transactions with power capacity, rack density, and location attributes

- Financial models incorporating data centre-specific revenue streams and cost structures

- Risk assessment matrices for technological, regulatory, and market factors

- Quality assurance processes for technical verification and assumption validation

Client Communication and Education

Many property investors lack data centre expertise. Effective surveyors:

- Explain technical concepts in accessible language

- Quantify risk factors with scenario analysis and sensitivity testing

- Provide market context beyond individual property assessment

- Recommend specialist advisors for technical, legal, and operational due diligence

For clients seeking independent property valuations, clear communication builds confidence and supports informed decision-making.

Geographic Market Specialization

Given the concentration of data centre activity in specific markets, surveyors benefit from geographic specialization:

- London submarkets: Understanding differences between Docklands, Slough, and emerging East London locations

- Regional hubs: Expertise in Manchester, Birmingham, or Edinburgh markets

- Edge computing: Knowledge of distributed facilities in secondary cities

Firms with presence across South West London, Bromley, and other key areas can leverage local market intelligence.

Ethical and Professional Standards

Data centre valuations involve significant financial stakes and complex technical assessments. Maintaining RICS professional standards requires:

- Independence from commercial pressures

- Competence through appropriate expertise or specialist consultation

- Transparency regarding assumptions, limitations, and uncertainties

- Objectivity in analysis and conclusions

When assignments exceed individual expertise, ethical practice requires engaging appropriate specialists or declining the instruction.

Future Outlook and Emerging Trends

AI-Driven Demand Evolution

Artificial intelligence workloads are fundamentally reshaping data centre requirements. The +4.8% contribution to CAGR from AI and GPU-driven demand [2] reflects current trends, but continued AI advancement could accelerate requirements further.

Surveyors must monitor:

- Rack density evolution beyond current 30 kW standards

- Cooling technology advancement enabling higher densities

- Specialized AI facilities optimized for training versus inference workloads

Sustainability Integration

Environmental, social, and governance (ESG) factors increasingly influence valuations:

- Renewable energy integration and power purchase agreements

- Water efficiency in cooling systems

- Circular economy approaches to equipment lifecycle

- Community benefits like skills training and local employment

Facilities demonstrating strong ESG credentials may command premium valuations from institutional investors with sustainability mandates.

Edge Computing Proliferation

While mega campuses dominate growth projections, edge computing facilities serving latency-sensitive applications represent a distinct market segment:

- Smaller footprints (typically under 5 MW)

- Distributed locations closer to end users

- Different tenant profiles and lease structures

- Unique valuation considerations balancing scale limitations with strategic locations

Modular and Prefabricated Solutions

Innovative construction approaches may accelerate deployment:

- Modular data centres reducing construction timelines

- Prefabricated components improving quality and efficiency

- Scalable designs enabling phased capacity expansion

These approaches affect development risk assessments and residual land valuations.

Quantum Computing Implications

While still emerging, quantum computing may eventually impact data centre requirements:

- Specialized environmental controls (extreme cooling requirements)

- Hybrid facilities combining classical and quantum computing

- Uncertain timeline for commercial deployment

Surveyors should monitor technological developments while recognizing current valuation impacts remain minimal.

Conclusion

Data Centre Boom and Valuation Challenges: Chartered Surveyor Strategies for High-Density UK Sites in 2026 represents a critical professional frontier. The UK market's projected growth from £17.24 billion in 2026 to £31.99 billion by 2031 [1] creates extraordinary opportunities for surveyors who develop specialized expertise in this complex asset class.

The shift toward mega campuses exceeding 40 MW, advancing at 27.60% CAGR [2], fundamentally changes valuation approaches. Traditional square footage metrics give way to power capacity, rack density, and cooling efficiency as primary value drivers. Chartered surveyors must integrate technical assessments of electrical infrastructure, cooling systems, and AI-readiness into RICS-compliant valuation frameworks.

Geographic dynamics add further complexity. East London's Royal Docks emergence as a data centre powerhouse, alongside established hubs in Slough and Docklands, creates distinct submarkets requiring specialized knowledge. The dominance of Equinix, Digital Realty, and NTT with over 45% market share [2] shapes competitive dynamics and transaction comparables.

Success in this market requires:

✅ Continuous professional development in data centre technology and market dynamics

✅ Robust valuation frameworks incorporating power capacity, cooling infrastructure, and grid connectivity

✅ Technical partnerships with electrical engineers and data centre specialists

✅ Geographic market intelligence across key investment locations

✅ Client education translating complex technical factors into clear valuation rationale

For chartered surveyors willing to invest in specialized expertise, the data centre boom offers significant professional opportunities. Those who master the technical complexities while maintaining RICS professional standards will position themselves as essential advisors in one of the UK's fastest-growing property sectors.

Actionable Next Steps

For property professionals seeking to capitalize on data centre valuation opportunities:

- Assess current capability gaps in technical knowledge, market intelligence, and valuation methodologies

- Pursue specialized training through RICS courses, industry conferences, and technical partnerships

- Build comparable databases tracking data centre transactions with power capacity and technical specifications

- Develop technical networks with electrical engineers, cooling specialists, and data centre operators

- Monitor market developments including grid capacity projects, planning approvals, and hyperscaler expansion plans

- Engage with institutional investors to understand evolving requirements and valuation expectations

The convergence of artificial intelligence growth, digital infrastructure investment, and property expertise creates a unique moment for chartered surveyors. Those who embrace the complexity and develop robust, RICS-compliant approaches to data centre valuation will establish themselves as leaders in this dynamic market.

References

[1] Uk Data Centre Manufacturing Growth 2026 – https://thegrowthhub.me/uk-data-centre-manufacturing-growth-2026/

[2] London Data Center Market – https://www.mordorintelligence.com/industry-reports/london-data-center-market

[3] 2026 Data Centre Trends – https://www.onnecgroup.com/2025/12/04/2026-data-centre-trends/