The UK property market is experiencing a remarkable transformation in 2026. With the Bank of England holding base rates at 3.75% and mortgage products reaching their most affordable levels since 2022, the landscape for chartered valuations has fundamentally shifted. Understanding Chartered Valuations at 3.75% Base Rates: Adjusting for 4% House Price Growth and Buyer Confidence in Q2 2026 has become essential for property professionals, buyers, and investors navigating this evolving market. 🏡

The confluence of stabilized interest rates, projected 4% house price growth, and a remarkable 10% increase in property transactions compared to 2025 creates unprecedented opportunities—and challenges—for accurate property valuations. Chartered surveyors must now recalibrate their methodologies to reflect these dynamic market conditions while maintaining professional standards and accuracy.

Key Takeaways

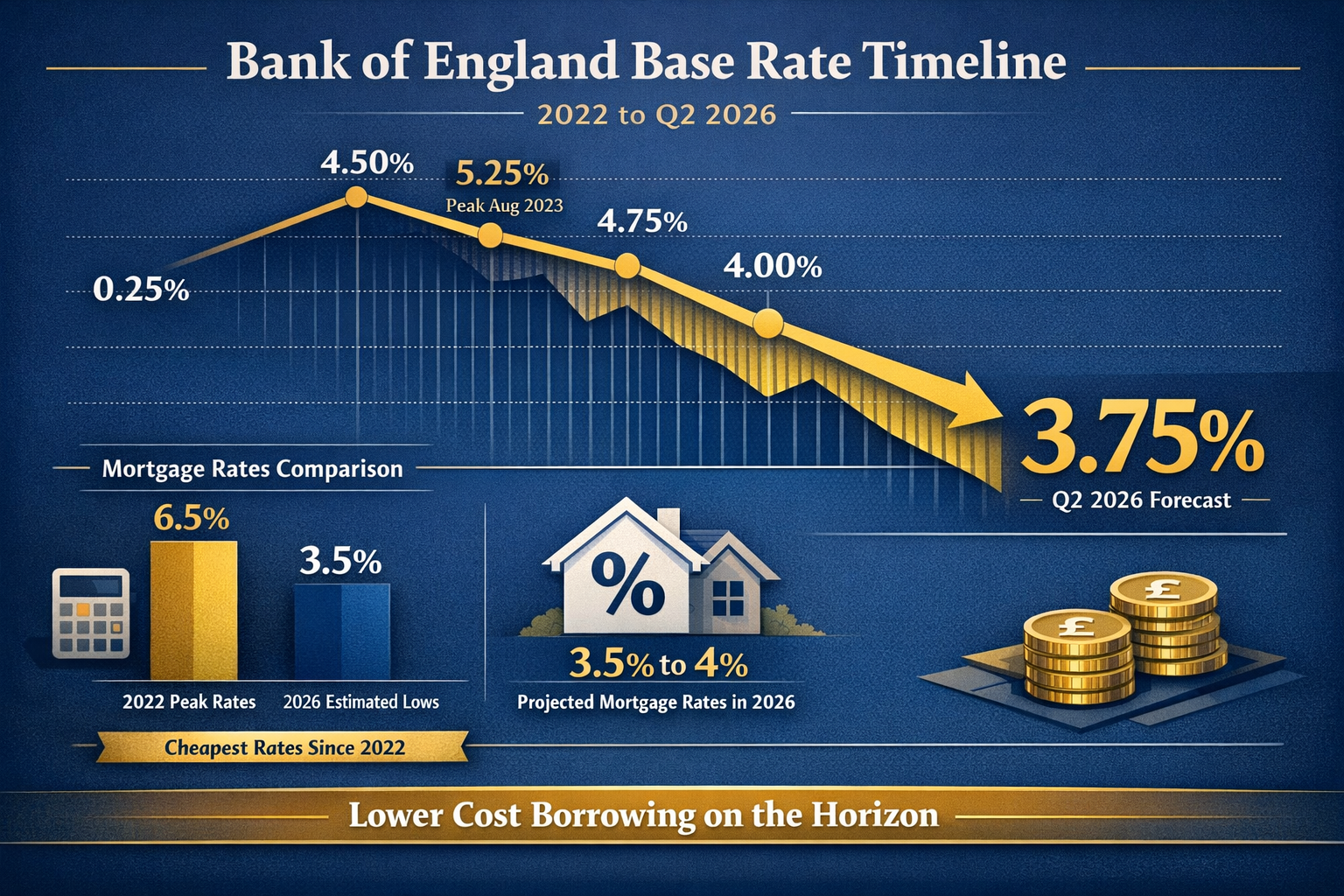

- Base rates held at 3.75% by the Bank of England in March 2026, creating the most affordable mortgage environment since 2022 [1][5]

- 4% house price growth projected for 2026, driven by improved buyer confidence and increased transaction volumes

- 10% transaction uplift from 2025 levels indicates renewed market momentum and buyer activity

- Valuation methodologies must adapt to reflect both stabilized borrowing costs and accelerating price appreciation

- Professional chartered surveyors play a critical role in ensuring accurate valuations that balance current rates with growth projections

Understanding the 3.75% Base Rate Environment

The Bank of England's March 2026 Decision

On March 19, 2026, the Bank of England's Monetary Policy Committee voted unanimously to maintain the base rate at 3.75% [1][5]. This decision reflects a careful balancing act between controlling inflation—which remains at 3% above the target 2% level—and supporting economic growth [3].

The current rate environment represents a significant improvement from the peak rates experienced in 2023, when the base rate reached 5.25%. For property buyers and homeowners, this translates directly into more affordable mortgage products and increased purchasing power.

Key factors influencing the rate decision:

- Inflation concerns: CPI inflation stood at 3.2% in January 2026, partly driven by Middle East conflicts disrupting oil and gas supplies [3]

- Economic stability: The Committee prioritized maintaining stable conditions to support continued recovery

- Future outlook: The next MPC meeting scheduled for April 30, 2026, may bring further rate adjustments [3]

Impact on Mortgage Products and Affordability

The 3.75% base rate has created a mortgage market renaissance. Lenders are now offering their most competitive products since 2022, with fixed-rate deals becoming increasingly attractive to buyers who remember the uncertainty of recent years.

| Mortgage Type | Average Rate Q2 2026 | Comparison to 2023 Peak |

|---|---|---|

| 2-Year Fixed | 4.2% | -2.1% |

| 5-Year Fixed | 4.5% | -1.8% |

| Variable Rate | 4.0% | -1.9% |

| First-Time Buyer | 4.3% | -2.0% |

This affordability improvement has directly contributed to the 10% increase in property transactions, as more buyers can qualify for mortgages and afford higher-value properties.

Chartered Valuations at 3.75% Base Rates: Methodology Adjustments

Traditional Valuation Approaches in the Current Climate

Chartered surveyors must now recalibrate their valuation methodologies to account for the unique characteristics of the Q2 2026 market. The three primary valuation approaches—comparative, income, and cost—each require specific adjustments.

Comparative Method Adjustments:

The comparative method, which analyzes recent sales of similar properties, must now factor in the accelerated transaction velocity and rising prices. Properties that sold six months ago may no longer provide accurate benchmarks due to the 4% annual growth trajectory.

✅ Best practices include:

- Weighting recent sales (within 3 months) more heavily

- Applying time-adjustment factors of approximately 1% per quarter

- Considering location-specific growth variations

- Analyzing buyer demographics and motivation changes

Income Approach Considerations:

For investment properties, the income approach requires careful analysis of rental yields against mortgage costs. With borrowing costs stabilizing, rental properties become more attractive investments, potentially compressing yields.

Cost Approach Refinements:

Construction costs have moderated in 2026, but material price volatility requires surveyors to maintain current supplier pricing databases and adjust replacement cost calculations accordingly.

Integrating Market Momentum into Valuations

The 10% transaction increase from 2025 represents more than statistical noise—it signals fundamental market confidence restoration. Professional valuers must distinguish between:

- Sustainable price growth driven by improved affordability and genuine demand

- Speculative momentum that may not persist beyond short-term market enthusiasm

"The key to accurate valuations in Q2 2026 lies in understanding that we're not simply reverting to pre-2022 conditions. We're entering a new market phase characterized by informed buyers, stabilized rates, and realistic growth expectations." — RICS Valuation Standards

When conducting independent property valuations, chartered surveyors should incorporate:

- Forward-looking adjustments that account for the 4% annual growth trajectory

- Confidence indices reflecting buyer sentiment and transaction velocity

- Regional variations in how the 3.75% rate impacts different property markets

- Property-specific factors including condition, location, and unique features

Risk Assessment and Uncertainty Factors

Despite positive market indicators, professional valuers must acknowledge uncertainty factors:

- Inflation persistence: If inflation remains above 3%, further rate increases remain possible [3]

- Global economic conditions: International factors affecting UK economic stability

- Regional disparities: Not all areas experience uniform 4% growth

- Property type variations: Different segments respond differently to rate changes

Adjusting for 4% House Price Growth and Buyer Confidence

Analyzing the 4% Growth Projection

The projected 4% house price growth for 2026 represents a Goldilocks scenario—neither too hot to trigger affordability concerns nor too cold to discourage buyer activity. This moderate appreciation reflects several converging factors.

Growth drivers include:

- 💰 Improved mortgage affordability at 3.75% base rates

- 📈 Pent-up demand from buyers who delayed purchases during 2022-2024 uncertainty

- 🏘️ Supply constraints in desirable locations maintaining price support

- 💼 Economic confidence supporting employment and wage growth

Understanding house price trends requires analyzing both national averages and regional variations. London and the Southeast may experience different growth rates compared to Northern regions or rural areas.

Regional Variations in Growth Patterns

Not all regions benefit equally from the current market conditions. Chartered surveyors must apply location-specific adjustments:

High-Growth Areas (5-6% projected):

- Commuter belt locations with improved transport links

- Areas benefiting from remote work flexibility

- Regions with new development and infrastructure investment

Moderate-Growth Areas (3-4% projected):

- Established suburban markets

- Secondary cities with stable employment

- Areas with balanced supply and demand

Lower-Growth Areas (1-2% projected):

- Oversupplied new-build markets

- Regions with economic challenges

- Areas with declining population trends

Professional valuers in Hertfordshire, Hampshire, and Buckinghamshire must apply these regional considerations when preparing valuations.

Buyer Confidence Metrics and Transaction Analysis

The 10% increase in property transactions from 2025 provides tangible evidence of restored buyer confidence. This metric matters for valuations because transaction velocity directly impacts price discovery and market liquidity.

Confidence indicators include:

- Reduction in time-on-market for well-priced properties

- Decreased price negotiation margins

- Increased mortgage approval rates

- Growing first-time buyer participation

- Reduced fall-through rates on agreed sales

When buyers feel confident, they're more willing to pay asking prices or compete for desirable properties, supporting the 4% growth trajectory. Conversely, any confidence erosion could quickly dampen price appreciation.

Incorporating Survey Findings into Valuations

Professional building surveys reveal property conditions that significantly impact valuations. The relationship between survey findings and price adjustments remains critical, even in a growing market.

Survey impact considerations:

- Major defects may justify 5-15% valuation reductions regardless of market growth

- Minor issues might be absorbed by overall price appreciation

- Upgrade potential could support premium valuations in growth markets

- Energy efficiency increasingly affects both valuation and marketability

Understanding whether you need a Level 2 or Level 3 survey helps buyers make informed decisions that protect their investment in the current market.

Practical Applications for Property Professionals

For Chartered Surveyors and Valuers

Professional valuers must balance multiple considerations when preparing reports in Q2 2026:

Documentation requirements:

- Clear explanation of methodology adjustments for current market conditions

- Transparent disclosure of growth assumptions and rate environment impacts

- Comparable evidence from recent transactions with time adjustments

- Risk factors and uncertainty acknowledgments

Quality assurance measures:

- Peer review of valuations exceeding certain thresholds

- Regular calibration against actual transaction prices

- Continuous professional development on market conditions

- Adherence to RICS Red Book standards with appropriate adjustments

For Buyers and Sellers

Understanding Chartered Valuations at 3.75% Base Rates: Adjusting for 4% House Price Growth and Buyer Confidence in Q2 2026 empowers informed decision-making:

Buyer strategies:

- Obtain professional valuations before making offers

- Consider growth projections when assessing long-term value

- Factor in mortgage affordability at current rates

- Request detailed survey reports to identify issues

Seller approaches:

- Commission pre-sale valuations to set realistic asking prices

- Understand how recent comparable sales support pricing

- Address survey-identifiable issues before marketing

- Time sales to capitalize on current buyer confidence

For Lenders and Financial Institutions

Mortgage lenders rely on accurate valuations to manage lending risk. The current environment requires:

- Conservative loan-to-value ratios that account for potential rate increases

- Stress testing borrowers against potential 1-2% rate rises

- Regional risk assessment recognizing variable growth patterns

- Property type considerations affecting long-term value stability

For Investors and Portfolio Managers

Property investors must evaluate opportunities through the lens of current market conditions:

Investment analysis factors:

- Rental yield calculations at 3.75% borrowing costs

- Capital appreciation potential from 4% growth trajectory

- Portfolio diversification across regions and property types

- Exit strategy flexibility in changing rate environments

Challenges and Considerations for Q2 2026

Inflation and Future Rate Uncertainty

While the base rate holds at 3.75%, inflation at 3% remains above the Bank of England's 2% target [3]. This creates potential for future rate adjustments that could impact valuations.

Scenario planning considerations:

📊 If rates increase to 4.25-4.5%:

- Mortgage affordability deteriorates

- Price growth may slow to 1-2%

- Transaction volumes could decline

- Valuations require downward adjustments

📊 If rates decrease to 3.25-3.5%:

- Affordability improves further

- Price growth may accelerate to 5-6%

- Transaction volumes increase

- Valuations require upward adjustments

Supply and Demand Dynamics

The 4% growth projection assumes relatively balanced supply and demand. However, several factors could disrupt this equilibrium:

Supply constraints:

- Planning permission delays limiting new construction

- Existing homeowners reluctant to sell and lose low fixed-rate mortgages

- Land availability issues in high-demand areas

Demand fluctuations:

- Economic uncertainty affecting buyer confidence

- Changes to stamp duty or other property taxes

- Demographic shifts influencing housing preferences

Professional Standards and Liability

Chartered surveyors face increased scrutiny when valuations in rapidly changing markets later prove inaccurate. Professional indemnity considerations include:

- Clear documentation of assumptions and limitations

- Appropriate use of caveats regarding market uncertainty

- Regular revalidation of valuations in fast-moving markets

- Transparent communication with clients about confidence levels

Future Outlook and Market Predictions

Expectations for Late 2026 and Beyond

Market analysts anticipate the next MPC meeting on April 30, 2026, may provide signals about future rate direction [3]. Most economists predict:

- Gradual rate reductions to 3.25-3.5% by year-end if inflation moderates

- Sustained price growth of 3-5% annually through 2027

- Continued transaction growth as market confidence solidifies

- Regional divergence becoming more pronounced

Adapting Valuation Practices for Evolving Conditions

The property valuation profession must embrace flexibility and continuous adaptation:

Emerging best practices:

- Quarterly methodology reviews to incorporate market changes

- Enhanced data analytics and comparative market analysis tools

- Closer collaboration between surveyors, lenders, and estate agents

- Greater emphasis on forward-looking market indicators

Technology integration:

- Automated valuation models (AVMs) as supporting tools

- Geospatial analysis for location-specific adjustments

- Real-time transaction data integration

- Predictive modeling for growth trajectory analysis

Preparing for Different Market Scenarios

Prudent property professionals prepare for multiple potential outcomes:

Optimistic scenario (rates fall, growth accelerates):

- Valuations emphasize growth potential

- Investment opportunities increase

- Transaction volumes surge

Base case scenario (rates stable, 4% growth continues):

- Current methodologies remain appropriate

- Steady market conditions support planning

- Balanced risk-reward profiles

Pessimistic scenario (rates rise, growth stalls):

- Conservative valuation approaches essential

- Risk mitigation becomes priority

- Buyer caution returns

Conclusion

Chartered Valuations at 3.75% Base Rates: Adjusting for 4% House Price Growth and Buyer Confidence in Q2 2026 represents a critical inflection point for the UK property market. The combination of stabilized interest rates, moderate price growth, and restored buyer confidence creates an environment rich with opportunity—but also requiring careful professional judgment.

Chartered surveyors must balance traditional valuation methodologies with contemporary market realities, incorporating both the affordability benefits of 3.75% rates and the momentum indicated by 10% transaction growth. The projected 4% house price appreciation provides a reasonable baseline, but regional variations and property-specific factors demand individualized analysis.

Key Action Steps

For property professionals:

✅ Update valuation methodologies to reflect current market conditions

✅ Maintain continuous awareness of rate changes and economic indicators

✅ Document assumptions transparently and communicate uncertainties clearly

✅ Invest in professional development and market knowledge

For buyers and sellers:

✅ Obtain professional chartered surveyor valuations before major decisions

✅ Consider both current conditions and future market scenarios

✅ Factor in personal circumstances alongside market trends

✅ Work with qualified professionals who understand the 2026 market dynamics

For investors:

✅ Analyze opportunities through the lens of 3.75% borrowing costs

✅ Diversify across regions experiencing different growth rates

✅ Maintain flexibility to adapt to changing rate environments

✅ Focus on fundamentals rather than speculative momentum

The UK property market in Q2 2026 offers a window of opportunity created by the most favorable financing conditions since 2022, combined with realistic growth expectations and genuine buyer confidence. Success requires professional expertise, careful analysis, and adaptive strategies that acknowledge both opportunities and risks in this evolving landscape.

Whether you're a chartered surveyor preparing valuations, a buyer making the largest purchase of your life, or an investor building a property portfolio, understanding how 3.75% base rates, 4% growth projections, and restored market confidence interact will determine your success in this dynamic market environment. 🏠📈

References

[1] Bank Of England Holds Base Rate In March 2026 – https://www.spf.co.uk/insights/market-insights/bank-of-england-holds-base-rate-in-march-2026/

[2] Base Rate Held – https://www.moneysavingexpert.com/news/2026/03/base-rate-held/

[3] Bank Of England Base Rate – https://www.money.co.uk/mortgages/bank-of-england-base-rate

[4] March 2026 Base Rate Decision What It Means For Business Finance – https://bfs.ltd.uk/latest/march-2026-base-rate-decision-what-it-means-for-business-finance

[5] Current Interest Rate – https://www.bankofengland.co.uk/explainers/current-interest-rate