Approximately 85% of all properties set to fall within the new High-Value Council Tax Surcharge (HVCTS) are located in London and the South East — a statistic that places chartered surveyors operating in these regions at the sharp end of one of the most consequential property tax reforms in a generation [4]. For owners of homes valued at £2 million or more, the stakes are considerable. For the surveyors tasked with producing defensible, RICS-compliant Red Book valuations, the technical demands have never been greater.

This article examines how chartered surveyor valuations under new high-value home taxes 2026 are being shaped by the HVCTS, what adjustment methods apply specifically to London and South East markets, and how sensitivity analysis can help surveyors and property owners navigate band thresholds with precision.

Key Takeaways

- The HVCTS imposes annual surcharges of £2,500 to £7,500 on residential properties valued at £2 million or more, with valuations based on 2026 market values conducted by the Valuation Office Agency.

- Approximately 85% of affected properties are in London and the South East, making regional adjustment methodology critically important.

- Chartered surveyors must apply rigorous comparable selection, time adjustments, and sensitivity analysis — especially for properties near band thresholds.

- The VOA uses a comparable sales method; independent RICS Red Book valuations can be used to challenge VOA assessments through the formal appeals process.

- A government consultation launched in May 2026 means the final framework is still subject to change, and surveyors should monitor developments closely.

Understanding the HVCTS: What Chartered Surveyors Need to Know

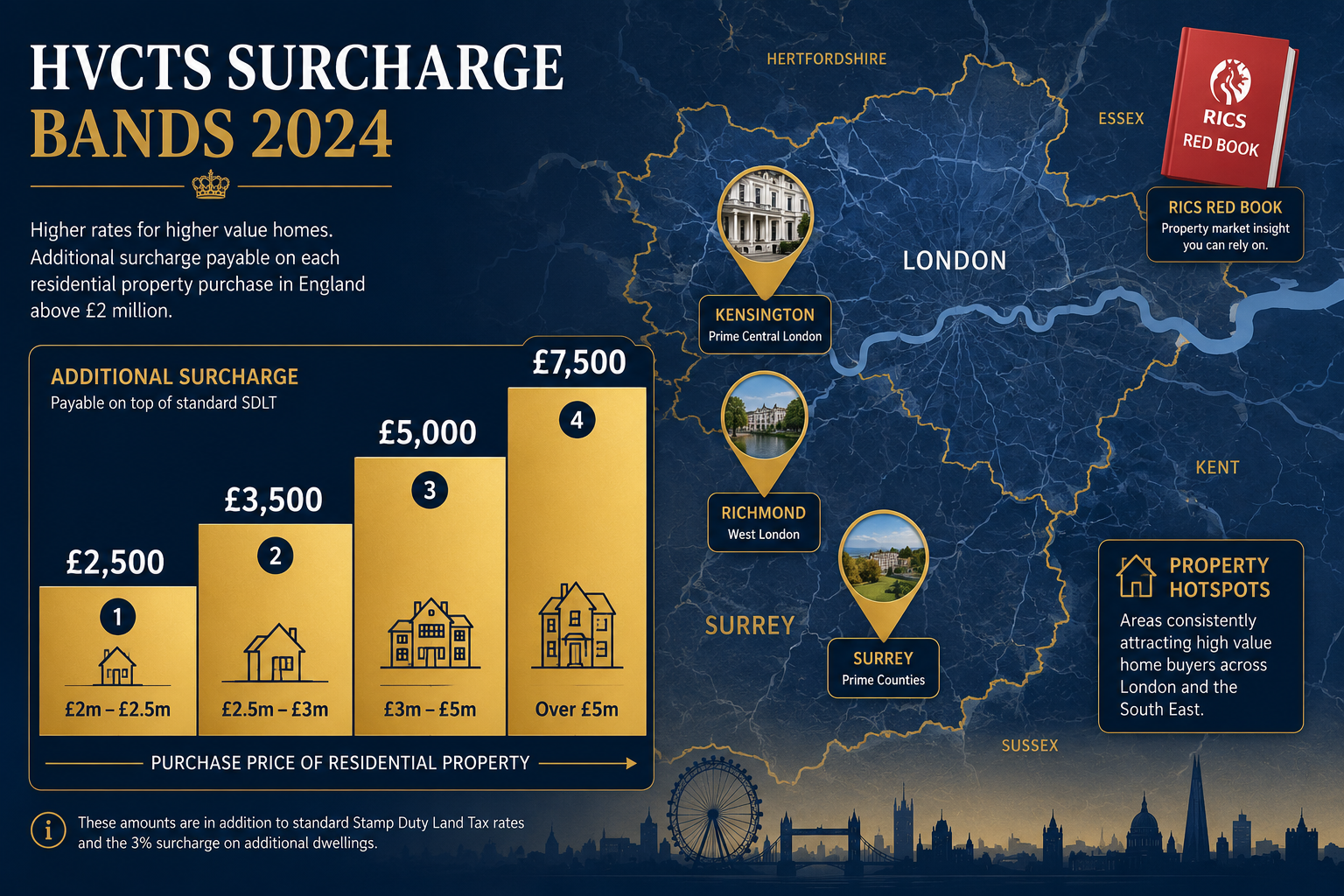

The High-Value Council Tax Surcharge was announced in November 2025 and represents a new annual levy on residential properties in England valued at £2 million or above [1]. It sits alongside existing council tax and is scheduled to commence in April 2028. The Valuation Office Agency (VOA) will conduct targeted valuations throughout 2026 to identify properties that cross the threshold, with those valuations anchored to 2026 market values and subject to reassessment every five years [2].

The surcharge operates across four bands:

| Valuation Band | Annual Surcharge |

|---|---|

| £2,000,000 to £2,499,999 | £2,500 |

| £2,500,000 to £2,999,999 | £3,500 |

| £3,000,000 to £4,999,999 | £5,000 |

| £5,000,000 and above | £7,500 |

For context, a property sitting at £2.05 million faces a £2,500 annual charge. A property assessed at £2.55 million faces £3,500. The financial difference between bands is meaningful, but the difference between being just inside or just outside the £2 million threshold is the most consequential distinction of all.

On 19 May 2026, the government launched an eight-week public consultation inviting feedback from property owners, surveyors, and industry bodies on the surcharge's design, deferral mechanisms, billing procedures, appeals process, and enforcement [5]. The outcome of this consultation may refine the final framework, which is an important caveat for any valuation work undertaken now.

For chartered surveyors, the practical implication is clear: clients whose properties are near any of the four band thresholds will require valuations that are not only accurate but also robustly documented and capable of withstanding scrutiny at appeal.

How the VOA Valuation Method Works — and Where Surveyors Can Add Value

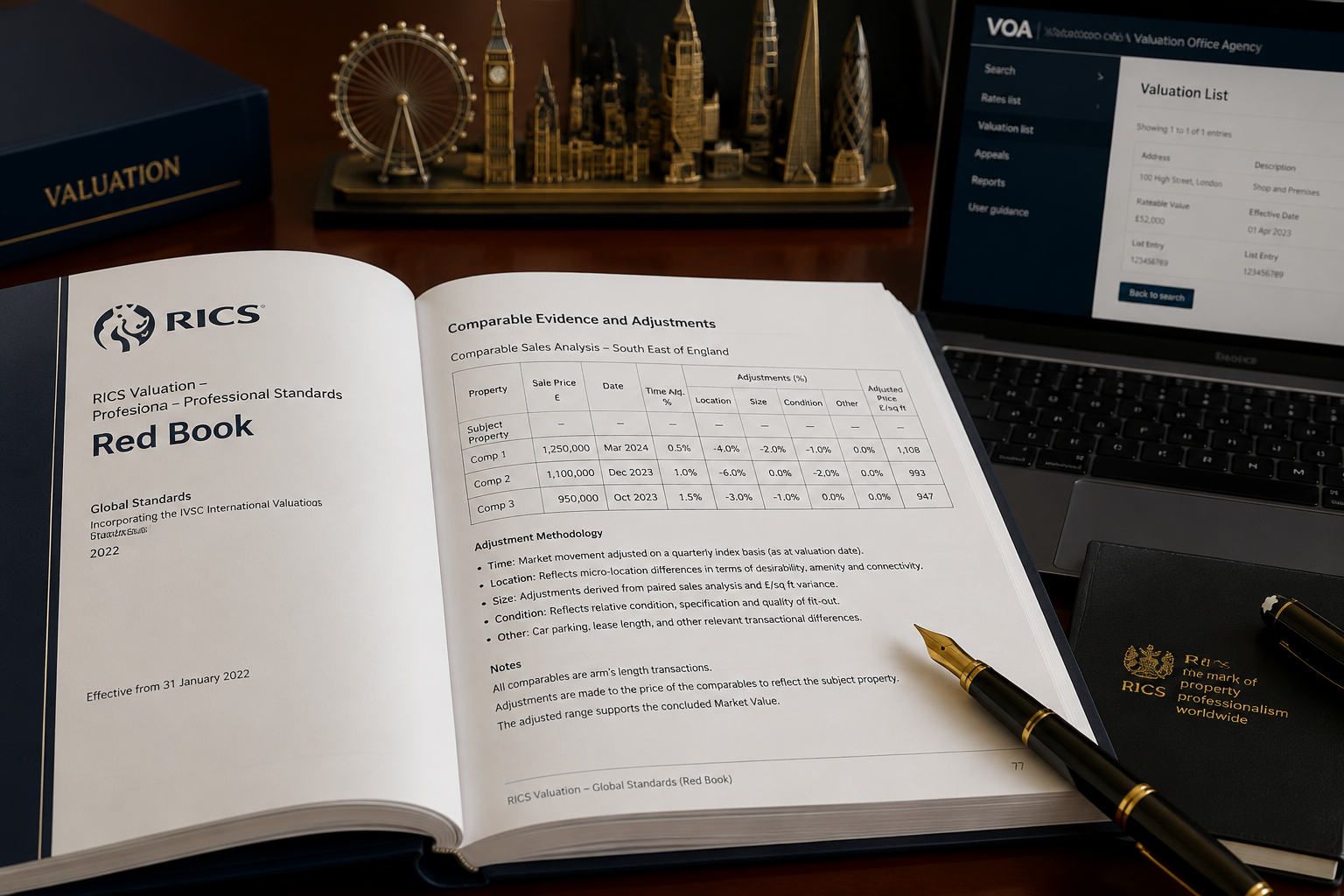

The VOA will employ the comparable sales method as its primary valuation approach [6]. This involves analysing recent sales of similar properties and making adjustments for differences in size, condition, location, tenure, and other material factors. The method is well-established in RICS practice, but its application to the high-value London and South East market introduces significant complexity.

The Comparable Sales Method in High-Value Markets

In mainstream residential markets, comparables are relatively abundant. In the £2 million-plus segment of London and the South East, the pool of truly comparable transactions is often thin. A five-bedroom detached house in a prime Surrey village may have only two or three recent sales that come close to matching its specification. Each comparable must then be adjusted for differences — and those adjustments, if poorly justified, become the weakest point in any valuation.

The VOA's approach will inevitably involve some degree of generalisation given the volume of properties to be assessed. This is precisely where independent chartered surveyors specialising in valuations can add significant value: by producing a more granular, property-specific analysis that either supports or challenges the VOA's figure.

Red Book Compliance and HVCTS Valuations

RICS Red Book Global Standards govern the production of formal valuations in the UK. For HVCTS purposes, any independent valuation submitted as part of an appeal or pre-emptive challenge should comply fully with Red Book requirements. This means:

- A clearly stated basis of value (market value as defined by RICS)

- A defined valuation date (2026 market conditions)

- Full disclosure of assumptions and special assumptions

- Documented comparable evidence with explicit adjustment reasoning

- A signed valuation certificate

Surveyors producing inheritance tax valuations will recognise this framework — the HVCTS context demands the same level of rigour, applied to a living market rather than a date-of-death snapshot.

Adjustment Methods for London and South East High-Value Properties

The regional concentration of HVCTS-affected properties makes London and South East adjustment methodology the defining professional challenge of 2026 for many chartered surveyors [7]. The following adjustment categories are the most material.

1. Location Adjustments Within Sub-Markets

London is not one market. Kensington and Chelsea, Richmond upon Thames, and the City of London fringes each carry distinct value drivers. Within the South East, prime Surrey villages, Berkshire commuter towns, and coastal Sussex locations behave differently from one another.

Surveyors must apply micro-location adjustments that reflect:

- Proximity to transport links: Crossrail catchment areas continue to command premiums in West London boroughs.

- School catchment quality: In areas like Ealing and Hammersmith, school catchment boundaries can shift values by 5-10% within a single street.

- Planning restrictions and conservation area status: Properties in conservation areas may carry both a premium (character, scarcity) and a discount (restriction on alterations).

For surveyors working across South East London and South West London, maintaining a live database of sub-market comparable evidence is no longer optional — it is a professional necessity under HVCTS conditions.

2. Time Adjustments in a Flat-Growth Environment

The high-value London market has experienced subdued price growth since 2022. With foreign investor activity returning selectively and domestic buyer sentiment cautious, the £2 million-plus segment has seen limited transactional volume and, in some sub-markets, modest price softening [8].

This creates a specific adjustment challenge: stale comparables. A sale from twelve months ago may not accurately reflect current market conditions. Surveyors should:

- Apply a time adjustment factor based on index data (RICS House Price Survey, Land Registry HPI) for the specific sub-market

- Clearly document the basis for any time adjustment in the valuation report

- Consider whether a comparable from a different but more active sub-market is preferable to a closer but older comparable

"In a flat or softening market, the direction of time adjustments matters as much as their magnitude. A surveyor who applies an upward time adjustment without evidential basis risks producing a valuation that overstates market value — and potentially places a client in a higher HVCTS band unnecessarily."

3. Physical and Condition Adjustments

High-value properties in London and the South East often have significant physical complexity: basement extensions, loft conversions, listed building constraints, and heritage features. Each of these requires a considered adjustment.

Key adjustment categories include:

- Gross Internal Area (GIA) adjustments: Price per square foot analysis must account for the diminishing marginal value of additional floor space above certain thresholds.

- Condition and specification: A recently refurbished property commands a premium over one requiring significant capital expenditure. Surveyors should quantify this adjustment explicitly.

- Basement and below-ground space: Sub-ground accommodation is typically valued at a discount to above-ground space, reflecting natural light limitations and construction risk.

- Listed building status: Grade I and Grade II listed properties carry both scarcity premiums and compliance cost discounts. Net adjustment direction depends on buyer demand in the specific sub-market.

4. Tenure and Legal Adjustments

In London particularly, leasehold properties with short unexpired lease terms require significant downward adjustment. A property with 75 years remaining on its lease is materially less valuable than an equivalent freehold — and the adjustment quantum must be supported by lease extension cost modelling, not assumption.

Similarly, properties subject to restrictive covenants, overage agreements, or shared ownership structures require legal adjustments that should be documented with reference to solicitor advice or specialist legal valuation input.

Sensitivity Analysis: Navigating Band Thresholds

For properties near the £2 million, £2.5 million, £3 million, or £5 million thresholds, sensitivity analysis is not a supplementary exercise — it is central to the valuation's usefulness to the client [8].

A Practical Sensitivity Analysis Example

Consider a detached property in a prime Surrey location. The surveyor's central estimate of market value is £2.48 million. The property sits just below the £2.5 million band threshold. A sensitivity analysis might look like this:

| Scenario | Adjustment Applied | Indicated Value | HVCTS Band | Annual Charge |

|---|---|---|---|---|

| Downside (-3%) | Condition discount | £2,405,600 | Band 1 | £2,500 |

| Central estimate | No adjustment | £2,480,000 | Band 1 | £2,500 |

| Upside (+2%) | Location premium | £2,529,600 | Band 2 | £3,500 |

| Upside (+5%) | Specification premium | £2,604,000 | Band 2 | £3,500 |

In this example, a 2% upward adjustment pushes the property into Band 2, increasing the annual surcharge by £1,000. Over five years (the reassessment period), that represents a £5,000 difference in cumulative tax liability. The surveyor's adjustment decisions carry direct financial consequences for the client.

Best practice for threshold properties:

- Present a central estimate with a clearly stated range (e.g., £2.40 million to £2.55 million)

- Identify which adjustments are most sensitive to the final figure

- Document the evidential basis for each adjustment with specific comparable references

- Advise the client on the appeals process if the VOA assessment differs materially

If a VOA assessment appears to overstate value, property owners should be aware that understanding what to do when a home valuation differs from expectations is an important first step — and that a formal Red Book valuation from a RICS-regulated surveyor provides the strongest foundation for an appeal.

Regional Considerations: Key London and South East Markets

London Boroughs

Prime Central London (PCL) — covering areas such as Kensington, Chelsea, Westminster, and Islington — has the highest concentration of HVCTS-affected properties in the country. Surveyors working in Islington and surrounding boroughs must navigate a market where transaction volumes at the £2 million-plus level have been constrained by stamp duty land tax (SDLT) at higher rates, combined with the prospect of the HVCTS adding to holding costs.

Foreign investor activity — historically a significant driver of PCL values — has returned selectively in 2026, with buyers from the Middle East and Southeast Asia active in certain segments. However, the HVCTS adds to the total cost of ownership calculation for non-resident investors, and surveyors should factor potential demand-side softening into their market commentary.

Surrey and Berkshire

Surrey and Berkshire represent the largest concentration of HVCTS-affected properties outside London. The Surrey and Berkshire markets are characterised by large detached family homes, equestrian properties, and country houses — all of which present specific valuation challenges around land value apportionment, outbuilding valuation, and rural amenity premiums.

For properties in this segment, the comparable evidence base is often national rather than purely local. Surveyors must exercise careful judgement in selecting and adjusting comparables from different geographic sub-markets.

Sussex and the Wider South East

Coastal and rural Sussex, along with parts of Essex and Hertfordshire, contain a smaller but growing number of HVCTS-affected properties, particularly as buyers have sought larger homes outside London since 2020. Surveyors in Sussex and Essex should be alert to the specific valuation challenges of converted rural buildings, properties with significant land, and homes with unusual construction types.

The Appeals Process and the Surveyor's Role

The government's consultation launched in May 2026 includes specific questions about the design of the appeals mechanism [5]. While the final process is not yet confirmed, it is expected to follow a similar structure to existing council tax banding appeals — with an initial challenge to the VOA, followed by escalation to an independent tribunal if unresolved.

Chartered surveyors will play a central role in the appeals process by:

- Producing formal Red Book valuations that provide an independent market value opinion

- Preparing comparable evidence schedules that support the client's position

- Acting as expert witnesses in tribunal proceedings where required

The expert witness report services offered by specialist surveying firms will be in increasing demand as HVCTS assessments are issued and challenged from 2026 onwards.

Conclusion

The introduction of the High-Value Council Tax Surcharge represents a structural shift in the cost of owning high-value residential property in England — and the burden falls disproportionately on London and the South East. For chartered surveyors, this creates both a professional challenge and a significant opportunity to demonstrate the value of rigorous, evidence-based valuation practice.

Actionable next steps for surveyors and property owners:

- Build and maintain a live comparable database for your specific sub-markets, updated at least quarterly to reflect current transaction evidence.

- Apply sensitivity analysis as standard practice for any property within 10% of an HVCTS band threshold — document the range and the key adjustment drivers.

- Ensure full Red Book compliance on all HVCTS-related valuations, including explicit statement of assumptions, valuation date, and comparable adjustment methodology.

- Monitor the consultation outcome — the eight-week consultation that began in May 2026 may result in changes to band thresholds, deferral mechanisms, or the appeals process.

- Advise clients proactively — property owners near the £2 million threshold in particular should commission an independent valuation before the VOA assessment is issued, not after.

- Engage with the appeals process early if a VOA assessment appears to overstate value — a well-prepared Red Book valuation is the most effective tool available.

The surveyors who invest in technical precision, regional market intelligence, and clear client communication in 2026 will be best positioned to serve their clients through what promises to be a complex and consequential period for the high-value property market.

References

[1] High Value Council Tax Surcharge – https://www.gov.uk/government/publications/high-value-council-tax-surcharge?utm_source=openai

[2] High Value Council Tax Surcharge – https://www.gov.uk/government/news/high-value-council-tax-surcharge?utm_source=openai

[3] Budget 2025 Sees Mansion Tax Announced – https://www.evelyn.com/press-centre/all-press-releases/budget-2025-sees-mansion-tax-announced/?utm_source=openai

[4] UK Mansion Tax 2026 Bands Dates Who Pays – https://valuq.co.uk/insights/uk-mansion-tax-2026-bands-dates-who-pays?utm_source=openai

[5] Fairer Taxes For High Value Homes – https://www.gov.uk/government/news/fairer-taxes-for-high-value-homes?utm_source=openai

[6] High Value Council Tax Surcharge – https://www.gov.uk/government/consultations/high-value-council-tax-surcharge/high-value-council-tax-surcharge?utm_source=openai

[7] Valuation Adjustments In Regional Divergences RICS February 2026 Data For Surveyors In London Vs North – https://www.canterburysurveyors.com/blog/valuation-adjustments-in-regional-divergences-rics-february-2026-data-for-surveyors-in-london-vs-north/?utm_source=openai

[8] Valuation Adjustments For High Value Properties Over 2m Navigating 2026 Budget Tax Changes And Market Stability – https://princesurveyors.co.uk/blog/valuation-adjustments-for-high-value-properties-over-2m-navigating-2026-budget-tax-changes-and-market-stability/?utm_source=openai

[9] High Value Council Tax Surcharge – https://www.gov.uk/government/publications/high-value-council-tax-surcharge/high-value-council-tax-surcharge?utm_source=openai