UK house prices fell in six of twelve months during 2023, yet certain London postcodes recorded double-digit annual growth in the same period — a contradiction that perfectly illustrates why 2026 Red Book Valuations in Volatile Markets: Practical Adjustments for UK Residential and Mixed‑Use Assets demands a more nuanced, evidence-led approach than ever before. When comparable evidence pulls in opposite directions and lenders tighten criteria mid-instruction, the valuer's judgement — anchored firmly in RICS Valuation – Global Standards (the Red Book) — becomes the critical variable between a defensible opinion and a negligence claim.

This guide is written for practitioners, asset managers, and sophisticated property owners who need to understand how Red Book methodology adapts to fragmented market conditions in 2026.

Key Takeaways 📌

- Market volatility does not suspend Red Book obligations — it intensifies the need for robust comparable analysis, transparent assumptions, and clear special assumptions.

- Regional divergence in 2026 means a single national narrative is misleading; valuers must weight local evidence heavily.

- Mixed-use assets carry compounded uncertainty because residential and commercial income streams can move in opposite directions simultaneously.

- Worked examples demonstrate how to apply adjustment factors, yield selection, and "material uncertainty" clauses practically.

- Independent professional valuations are more important than ever for tax, lending, pension, and litigation purposes in a volatile market.

Understanding the Red Book Framework in a Volatile 2026 Market

What the Red Book Actually Requires

The RICS Valuation – Global Standards, supplemented by the UK National Supplement, sets out a clear hierarchy of obligations. At its core, every Red Book valuation must:

- Define the basis of value — most commonly Market Value (MV) or Market Rent (MR)

- Identify the valuation date — critical when prices are moving rapidly

- Disclose assumptions and special assumptions transparently

- Provide sufficient comparable evidence — adjusted for time, condition, and location

- Consider whether a Material Uncertainty clause is warranted

💡 "The valuation date is not a formality — in a volatile market, a valuation can be materially different from one month to the next. Practitioners must resist pressure to 'back-date' or 'forward-date' their opinion."

In 2026, with interest rate expectations shifting, planning policy in flux following recent legislative changes, and buyer sentiment varying sharply by region, each of these obligations carries heightened practical weight.

When to Apply a Material Uncertainty Clause

VPS 3 of the Red Book permits — and sometimes requires — a Material Uncertainty declaration when market evidence is insufficient to provide a confident opinion. Triggers in the current environment include:

| Trigger | Example in 2026 Context |

|---|---|

| Thin transaction volume | Rural mixed-use estates with fewer than 3 comparables in 12 months |

| Rapidly changing lending criteria | Buy-to-let properties affected by stress-test changes |

| Regulatory uncertainty | Leasehold reform impact on long-leasehold flats |

| Post-event shock | Local economic disruption from major employer closure |

Applying this clause is not an admission of failure — it is a professional obligation that protects both the valuer and the client.

Practical Adjustments for UK Residential Assets in 2026

The Comparable Evidence Problem

The cornerstone of residential Red Book valuation is the sales comparison approach. In a volatile market, this creates a specific challenge: which comparables are truly comparable?

A transaction completed eight months ago in a different interest rate environment may be structurally misleading. Practitioners should apply a structured adjustment framework:

Step 1 — Time adjustment

Where the market has moved measurably since the comparable sale, apply a percentage adjustment. Use Land Registry House Price Index data at the local authority level, not national averages.

Example: A semi-detached in Berkshire sold for £480,000 in April 2025. Local indices show a 3.2% decline to the February 2026 valuation date. Adjusted comparable: £464,640.

Step 2 — Physical adjustment

Account for differences in floor area, condition, EPC rating, and garden size. EPC ratings now carry measurable price premiums or discounts — properties rated F or G can attract discounts of 5–15% versus equivalent C-rated stock in the same street.

Step 3 — Location micro-adjustment

Even within a single postcode, proximity to transport, school catchments, and noise exposure can justify ±8% adjustments. Document these with evidence, not assumption.

Step 4 — Tenure adjustment

Leasehold reform legislation continues to reshape the market for long-leasehold flats. For properties with fewer than 80 years unexpired, apply a specific diminution analysis. An independent property valuation is essential before any transaction or refinancing decision involving shorter leases.

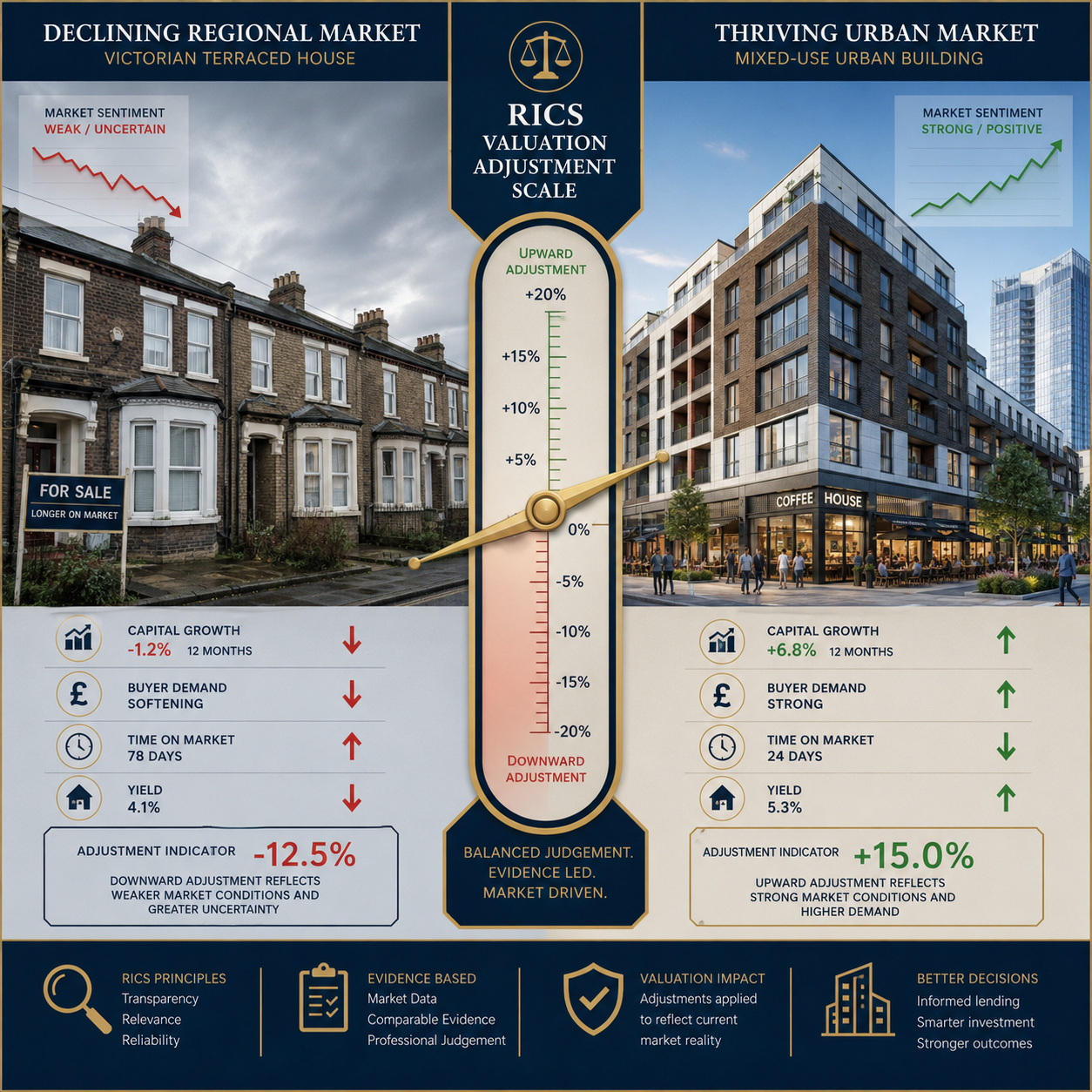

Regional Divergence: A Worked Example

Consider two residential instructions received in the same week in 2026:

Property A: Three-bedroom terraced house, Clapham, South London

- Strong buyer demand, constrained supply

- Three comparables within 0.3 miles, all within 4 months

- Minimal time adjustment required

- Valuation confidence: High

Property B: Four-bedroom detached, former mill town, North West England

- Buyer demand weak; two sales in the past 9 months, both at reduced prices

- Significant time adjustment needed; one comparable is a distressed sale

- Material Uncertainty clause likely warranted

- Valuation confidence: Moderate — with caveats

The chartered surveyors serving Clapham and similar high-demand urban areas will encounter very different evidence pools than colleagues operating in softer regional markets. Both must apply the same Red Book rigour — but the outputs, and the narrative within the report, will differ substantially.

Special Considerations: Capital Gains and Matrimonial Valuations

Two instruction types that generate particular complexity in volatile markets are Capital Gains Tax (CGT) valuations and matrimonial dispute valuations.

For CGT purposes, the valuation must reflect the market value at a specific historic date — sometimes years in the past. Reconstructing the market as it existed at that date, using period-correct comparables and lending conditions, requires careful archival research. Capital gains valuations must be prepared with particular attention to the evidential trail, since HMRC may scrutinise the opinion.

In matrimonial valuations, the court requires a current market value opinion. Where one party argues the market has moved significantly since separation, the valuer must address this directly — not ignore it.

Valuing Mixed‑Use Assets: Compounded Complexity in 2026

Why Mixed‑Use Is Harder Than Pure Residential or Commercial

A mixed-use asset — typically ground-floor retail or commercial with residential flats above — requires the valuer to apply two distinct methodologies simultaneously and then reconcile them into a single opinion of value.

The challenge in 2026 is that:

- Residential values are driven by mortgage availability, buyer confidence, and EPC performance

- Commercial values are driven by rental income, void risk, covenant strength, and yield expectations

- These two drivers are currently moving independently and sometimes in opposite directions

The Investment Method for Mixed‑Use: Step by Step

The investment method (income capitalisation) is the primary approach for mixed-use assets where income is the value driver.

Step 1 — Establish the passing rent

Identify the actual rent being received for each element. Separate the residential and commercial income streams.

Step 2 — Assess the Market Rent

Is the passing rent above or below the current market rent? A lease with a below-market rent on the commercial unit may have a reversionary value — but only if the covenant is strong enough to survive to the next review.

Step 3 — Select the capitalisation yield

This is where volatility bites hardest. Yield selection must reflect:

| Factor | Impact on Yield |

|---|---|

| Tenant covenant strength | Weak covenant → higher yield (lower value) |

| Lease length remaining | Short unexpired term → higher yield |

| Location quality | Prime pitch → lower yield |

| Void risk on commercial | High street retail → higher yield in 2026 |

| Residential demand | Strong demand → lower blended yield |

Example: A mixed-use building in Islington generates £28,000 per annum from a ground-floor café (3 years remaining on lease, strong covenant) and £24,000 per annum from two residential flats (assured shorthold tenancies, market rent).

- Commercial element: Capitalise at 6.5% → £28,000 ÷ 0.065 = £430,769

- Residential element: Capitalise at 4.75% → £24,000 ÷ 0.0475 = £505,263

- Gross valuation: £936,032 (subject to purchaser's costs deduction and any void/repair adjustments)

For commercial valuations of the non-residential element, practitioners must also consider whether the commercial use benefits from permitted development rights that could add residential conversion value — a factor increasingly relevant in 2026 as planning policy continues to evolve.

SIPP and Pension Fund Valuations of Mixed‑Use Assets

Mixed-use properties held within Self-Invested Personal Pensions (SIPPs) require a Red Book valuation at acquisition, disposal, and periodically during ownership. The volatile market of 2026 makes the triennial review particularly sensitive — a significant movement in yield or rental value between reviews can have direct implications for pension fund solvency calculations. SIPP pension valuations must be prepared strictly in accordance with HMRC requirements as well as Red Book standards.

Insurance Reinstatement: The Often-Overlooked Adjustment

Both residential and mixed-use Red Book instructions should prompt a parallel consideration: is the building insured for the correct reinstatement cost? This is a separate exercise from market valuation — reinstatement cost reflects the cost to rebuild, not the market value of the completed asset.

In 2026, construction inflation has remained elevated. Many buildings insured on pre-2022 figures are materially underinsured. An insurance reinstatement cost valuation should be commissioned alongside any Red Book exercise where the client also holds insurance responsibility.

Reporting Standards and Defensibility in 2026

What a Robust Red Book Report Must Contain

A valuation report that will withstand scrutiny — from a lender, HMRC, a court, or an RICS disciplinary panel — must include:

- ✅ Clear identification of the property, client, and intended use

- ✅ Explicit basis of value and valuation date

- ✅ List of assumptions (e.g., "vacant possession assumed", "no environmental contamination assumed")

- ✅ Comparable evidence schedule with adjustments shown and justified

- ✅ Yield selection rationale for income-producing assets

- ✅ Material Uncertainty clause where applicable, with explanation

- ✅ Valuer's RICS membership confirmation and any conflicts of interest disclosed

Avoiding Common Errors in Volatile Conditions

Practitioners under time pressure in a fast-moving market are vulnerable to specific errors:

- Over-reliance on automated valuation models (AVMs) — AVMs struggle in thin or volatile markets; they are a starting point, not a conclusion

- Ignoring lease events — rent reviews, break clauses, and lease expiries can dramatically alter value; missing them is indefensible

- Failing to re-inspect — a drive-by or desktop update is not a Red Book valuation

- Using national data for local conditions — the national house price index is irrelevant if the subject property is in a micro-market behaving differently

💡 "In a volatile market, the narrative within a Red Book report is as important as the number at the bottom of the page. Clients, lenders, and courts need to understand how the valuer reached their conclusion — not just what it is."

Preparing the Asset Before Valuation

Clients can take practical steps to support the valuation process and avoid unnecessary downward adjustments. Ensuring the property is well-presented, that all planning consents and building regulations certificates are available, and that any recent works are documented will help the valuer assess the asset accurately. Guidance on how to prepare your property before a professional inspection is a useful starting point for asset owners.

For mixed-use properties specifically, having lease documentation, rent schedules, service charge accounts, and any outstanding dilapidations claims organised before the valuer's inspection will materially improve the quality and speed of the final report.

Conclusion: Actionable Steps for Practitioners and Asset Owners in 2026

2026 Red Book Valuations in Volatile Markets: Practical Adjustments for UK Residential and Mixed‑Use Assets is not a theoretical challenge — it is a daily practical reality for every RICS-registered valuer working in the UK today. The market's regional fragmentation, shifting lending criteria, leasehold reform uncertainty, and construction cost inflation all demand a more rigorous, more transparent, and more thoroughly documented approach than was necessary in calmer conditions.

Immediate Action Steps ✅

- Review your comparable evidence protocols — establish a minimum standard for the age, proximity, and number of comparables required before issuing a report without a Material Uncertainty clause.

- Update your yield matrices — if your commercial yield benchmarks have not been reviewed since mid-2024, they are likely stale. Survey the market actively.

- Audit mixed-use instructions — ensure residential and commercial income streams are being valued separately before blending, and that yield selection for each element is individually justified.

- Brief clients on volatility — proactively explain to clients commissioning valuations for CGT, matrimonial, or lending purposes that a valuation is a point-in-time opinion, and that market conditions may require a refresh if the instruction is delayed.

- Commission reinstatement cost reviews — for any mixed-use or residential asset where the last insurance valuation is more than two years old, a fresh insurance reinstatement cost valuation is prudent.

- Engage RICS-qualified specialists — for complex mixed-use assets, leasehold properties, or any valuation likely to face challenge, the full range of professional valuation services from a chartered surveying practice provides both technical rigour and professional indemnity protection.

The Red Book exists precisely for moments like this — not as a bureaucratic constraint, but as a framework that protects clients, practitioners, and the integrity of the UK property market. In 2026, following it carefully is both a professional obligation and a commercial advantage.