A 68% probability of at least one flood exceeding six feet striking the Jersey City area before 2050 is not a distant warning — it is an active planning constraint shaping every development decision being made in 2026 [4]. Pair that with Miami-Dade County's position as one of the most flood-exposed metropolitan areas on the planet, and the stakes for accurate surveying become impossible to overstate. Surveying Jersey City and Miami's 2026 Boom: Coastal Flood Risk Mapping and Elevation Certifications sits at the intersection of booming real estate markets and accelerating sea-level rise, demanding that developers, lenders, insurers, and homeowners treat flood data not as a compliance checkbox but as a core investment variable.

Key Takeaways

- Both Jersey City and Miami face quantifiable, near-term flood risk that directly affects property values, insurance premiums, and construction compliance in 2026.

- Elevation certificates (ECs) are mandatory for new construction and substantial improvements in both markets, and they directly determine National Flood Insurance Program (NFIP) premium rates.

- LiDAR-based surveying is now the standard for producing FEMA-compliant elevation data, offering centimeter-level accuracy that traditional methods cannot match.

- New Jersey's Coastal Vulnerability Index (CVI) and Miami-Dade's Flood Zone Maps are distinct but complementary tools that inform resilience planning at the parcel level.

- Proactive flood risk mapping can reduce insurance costs, unlock financing, and strengthen a property's long-term asset value in both ULI-ranked coastal markets.

Why Coastal Flood Risk Mapping Matters in 2026's Hottest Markets

Both Jersey City and Miami consistently rank among the Urban Land Institute's top-tier markets for real estate investment and development activity. That ranking comes with a hidden cost: both cities sit on low-lying coastal terrain where the gap between current ground elevation and projected flood levels is narrowing each year.

What is coastal flood risk mapping?

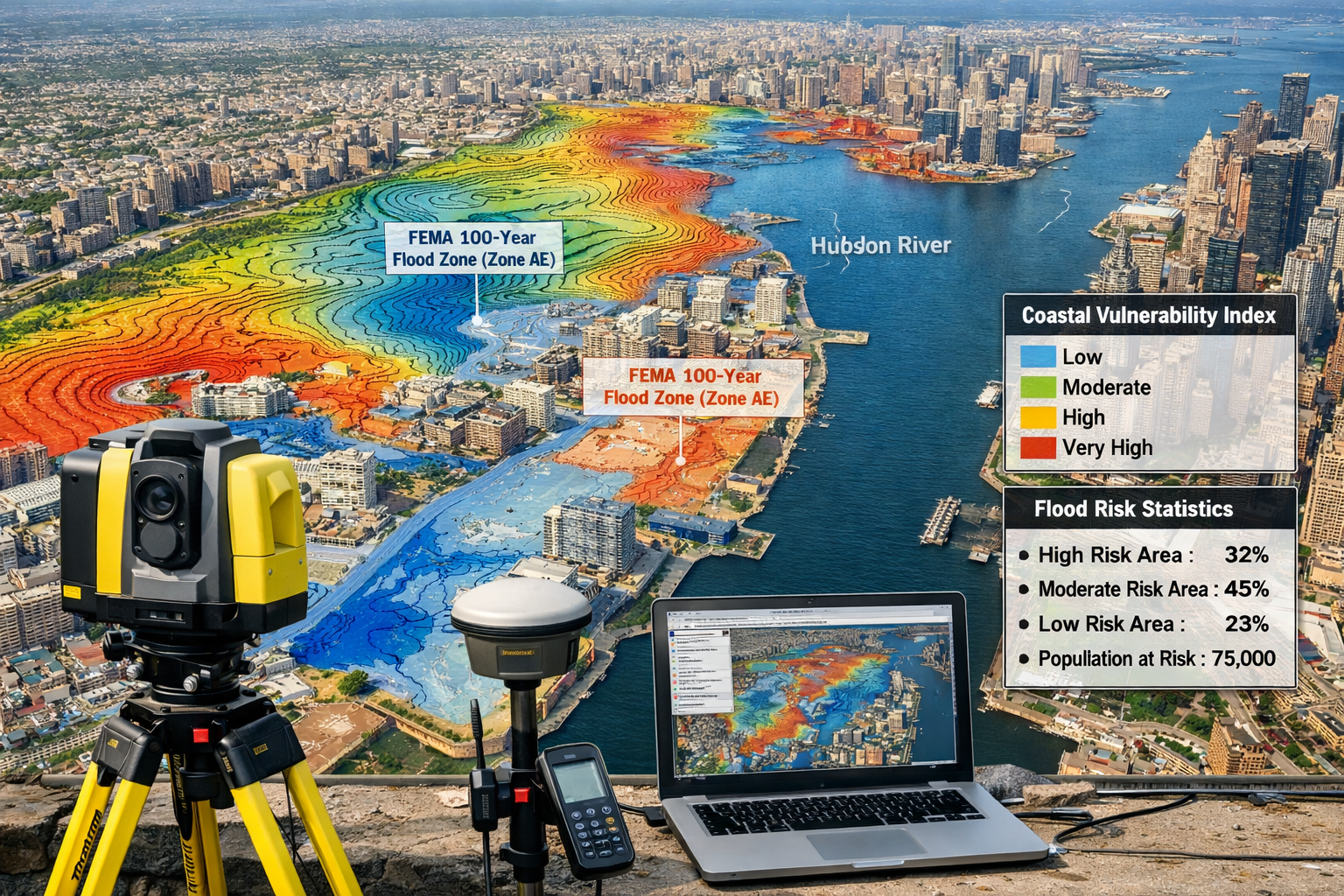

Coastal flood risk mapping is the process of using geospatial data, hydrological modeling, and survey measurements to identify which parcels of land are vulnerable to inundation under specific storm, tide, or sea-level scenarios. The outputs — flood zone designations, base flood elevations (BFEs), and coastal vulnerability scores — feed directly into insurance pricing, building codes, and mortgage underwriting.

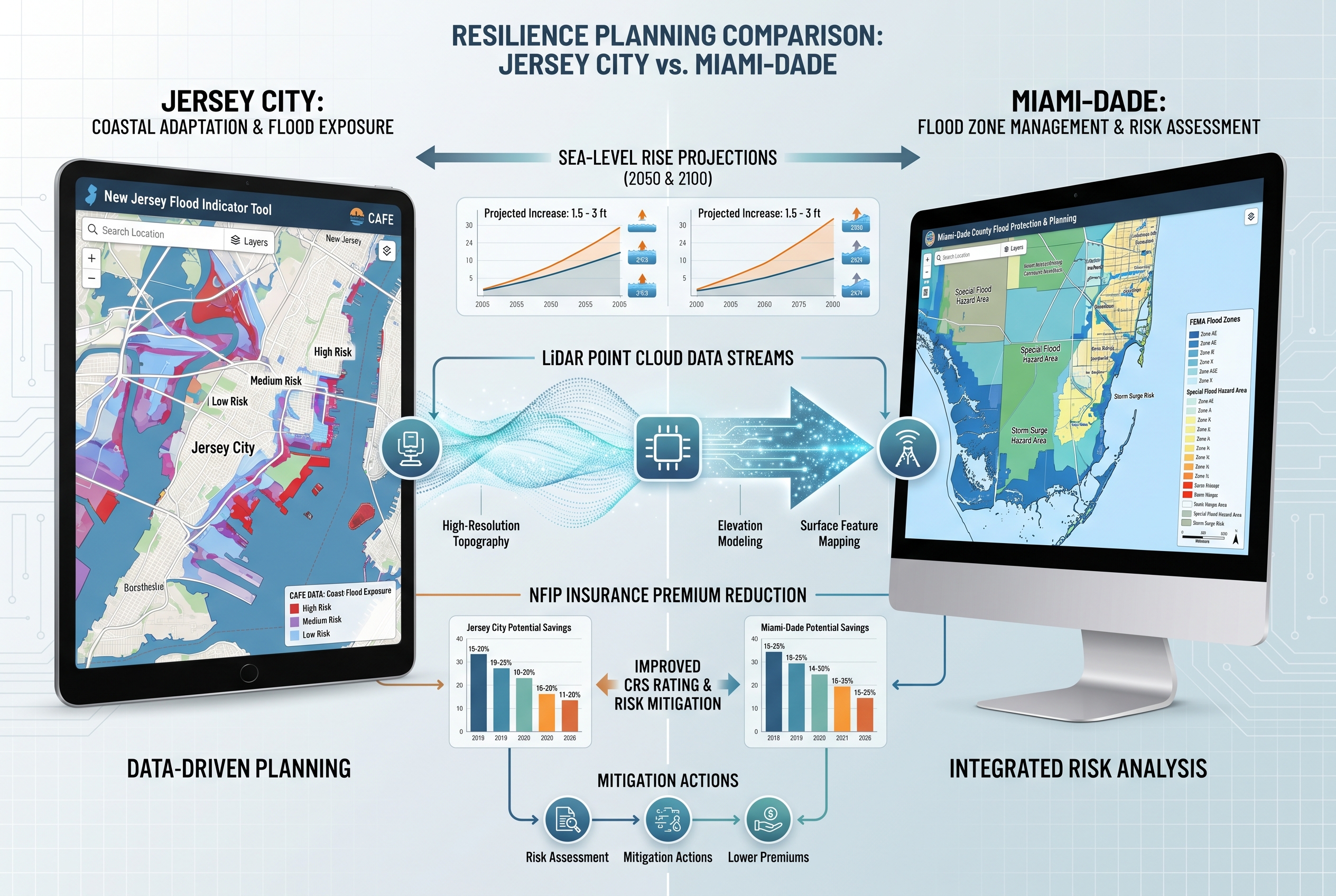

New Jersey's Coastal Vulnerability Index

The New Jersey Department of Environmental Protection (NJDEP) developed the Coastal Vulnerability Index (CVI) as a composite geospatial model designed to help community decision-makers understand natural risks at a granular level [1]. The CVI overlays multiple hazard indicators including:

- Geomorphology — the shape and composition of coastal landforms

- Slope — how quickly elevation changes across a parcel

- Flood-prone areas — historically documented inundation zones

- Storm surge scenarios — modeled water heights under named storm events

- Poorly drained soils — ground conditions that slow water absorption

- Erosion-prone areas — shoreline segments losing land mass over time

Critically, the CVI can be adapted to different sea-level rise scenarios, making it a forward-looking tool rather than a purely historical one [1]. For developers planning projects with 20- to 30-year investment horizons, this adaptability is essential.

New Jersey's Flood Indicator Tool

Alongside the CVI, the NJDEP operates a Flood Indicator Tool that allows users to assess flood risk for specific properties [2]. The tool integrates data from several sources:

| Data Layer | What It Shows |

|---|---|

| FEMA Flood Zones | Federal flood zone designations (A, AE, VE, X, etc.) |

| State Flood Hazard Areas | New Jersey-specific regulated floodplains |

| Tidal CAFE Data | Climate Adjusted Flood Elevation accounting for sea-level rise |

| Water Body Proximity | Distance to rivers, bays, tidal channels |

One important caveat: the absence of flood indicators in this tool does not guarantee a property is free from flood risk [2]. Surveyors and buyers should treat the tool as a starting point, not a definitive clearance.

Miami-Dade's Flood Zone Infrastructure

Miami-Dade County maintains a parallel but distinct flood risk infrastructure. The county provides publicly accessible flood zone maps and operates a dedicated Flood Zone Hotline (305-372-6466) to confirm exact flood zone designations for individual parcels [7]. The City of Miami's Building Department maintains elevation certificates for properties substantially improved or constructed since December 1992, and it offers site visits to inform property owners about flood zone classifications [5].

For properties near the Miami River, Biscayne Bay, and the county's extensive canal network, flood zone designations can change at the block level — making parcel-specific surveying indispensable rather than optional.

Elevation Certifications: The Core Document in Both Markets

At the heart of Surveying Jersey City and Miami's 2026 Boom: Coastal Flood Risk Mapping and Elevation Certifications is a single document that carries enormous financial weight: the elevation certificate (EC).

What an Elevation Certificate Contains

An elevation certificate records a building's elevation relative to the estimated floodwater levels in its designated high-risk area [3]. According to NFIP guidance, the document captures:

- The building's precise geographic location

- Flood zone designation and BFE

- The lowest floor elevation (including basement)

- Machinery and equipment elevations

- Enclosure and crawlspace information

- The certifying surveyor's license number and seal

The financial logic is direct: higher first-floor elevations relative to the BFE correlate with lower flood insurance premiums [9]. A property elevated two feet above the BFE can pay dramatically less in annual NFIP premiums than an identical structure built at grade.

Mandatory Requirements in New Jersey and Miami-Dade

In New Jersey, elevation certificates are required for buildings in high-risk flood zones (Special Flood Hazard Areas, or SFHAs) to determine accurate NFIP insurance premiums, confirm compliance with community floodplain management ordinances, and support Letters of Map Amendment (LOMA) requests [3]. A LOMA can remove a property from a SFHA designation if survey data proves the structure sits above the BFE — potentially eliminating mandatory flood insurance requirements entirely.

Miami-Dade County requires elevation certificates for all new construction and substantial improvements to structures [6]. The county's Building Department uses these certificates to confirm that a building meets or exceeds the required base flood elevation, which is a prerequisite for certificate of occupancy issuance [6]. Surveyors working in Miami must use the latest FEMA Flood Insurance Rate Maps (FIRMs) and precise elevation measurements to ensure compliance [8].

"An elevation certificate is not just a regulatory form — it is a financial instrument that can add or subtract thousands of dollars from annual operating costs on a single property."

Understanding what a full building survey covers helps contextualize why elevation data must be integrated into broader property assessments, not treated as a standalone regulatory task.

The Role of LiDAR in Producing Compliant Elevation Data

Light Detection and Ranging (LiDAR) technology has become the preferred method for generating the high-accuracy elevation data that FEMA-compliant surveys demand. LiDAR systems — whether mounted on aircraft, drones, or ground-based units — emit laser pulses and measure return times to build dense, three-dimensional point clouds of terrain and structures.

Key advantages of LiDAR for coastal flood surveys include:

- Vertical accuracy of 10–15 centimeters or better, far exceeding traditional optical leveling in complex terrain

- Ability to penetrate vegetation to capture bare-earth elevations in marshland and wooded coastal zones

- Rapid data collection over large areas, reducing field time and cost per acre

- Direct integration with GIS platforms used to produce FEMA FIRMs and CVI overlays

For developers conducting due diligence on sites in Jersey City's waterfront districts or Miami's barrier island parcels, LiDAR-derived elevation models provide the granular accuracy needed to assess freeboard requirements, design stormwater systems, and model worst-case inundation scenarios. Knowing the cost of a measured building survey and how elevation data feeds into that process helps stakeholders budget appropriately from the earliest project stages.

Resilience Planning Strategies for ULI-Ranked Coastal Markets

Surveying Jersey City and Miami's 2026 Boom: Coastal Flood Risk Mapping and Elevation Certifications is ultimately about more than compliance — it is about building assets that retain value as climate conditions evolve. The following strategies reflect current best practice for both markets.

Strategy 1: Commission Pre-Purchase Flood Risk Assessments

Before any acquisition in a coastal market, a flood risk assessment that goes beyond FEMA zone lookup is warranted. This means:

- Obtaining or commissioning a current elevation certificate

- Running the property through the NJDEP Flood Indicator Tool [2] or Miami-Dade's flood zone confirmation service [7]

- Reviewing the CVI score for New Jersey properties [1]

- Modeling insurance costs at current and projected flood zone designations

Properties that appear to be in lower-risk zones today may face redesignation as FEMA updates its FIRMs to incorporate newer sea-level rise projections. Buyers who understand how to negotiate house prices based on survey findings can use flood risk data as a legitimate basis for price adjustments.

Strategy 2: Pursue Letters of Map Amendment Where Eligible

For properties that have been elevated above the BFE through fill, construction, or natural topography, a LOMA can remove the mandatory flood insurance requirement. The process requires a licensed surveyor to certify the lowest adjacent grade and lowest floor elevation relative to the BFE, supported by a current elevation certificate [3].

In Jersey City's rapidly developing waterfront, where many parcels have been raised during construction, LOMA applications represent a significant cost-saving opportunity that is frequently overlooked.

Strategy 3: Integrate Flood Data into Building Materials Decisions

Coastal flood exposure affects not just insurance costs but the physical durability of building materials. Properties in AE and VE zones — the highest-risk FEMA designations common in both markets — face regular exposure to saltwater intrusion, high humidity, and hydrostatic pressure. A thorough building materials assessment should account for:

- Corrosion resistance of structural steel and fasteners

- Moisture resistance of wall assemblies and insulation systems

- Foundation design that accommodates hydrostatic uplift forces

- Mechanical, electrical, and plumbing systems elevated above BFE

Strategy 4: Use Climate-Adjusted Flood Elevations for Long-Term Projects

New Jersey's Tidal Climate Adjusted Flood Elevation (CAFE) data, available through the NJDEP Flood Indicator Tool, provides flood elevation estimates that account for projected sea-level rise rather than only current conditions [2]. For projects with 25- to 40-year investment horizons — hotels, mixed-use developments, institutional buildings — designing to CAFE rather than current BFE provides a meaningful resilience buffer.

Miami-Dade has moved in a similar direction, with county flood maps increasingly incorporating future sea-level scenarios. Developers who design to current minimums only may find their properties reclassified into higher-risk zones within the financing period, triggering mandatory insurance requirements mid-project.

Strategy 5: Leverage Flood Risk Data in Property Valuation

Flood zone status is a material fact in property valuation. A property in a FEMA Special Flood Hazard Area carries mandatory flood insurance costs that directly reduce net operating income and, therefore, capitalized value. Conversely, a property with a current elevation certificate demonstrating significant freeboard above the BFE may qualify for substantially reduced premiums.

Understanding how independent property valuations are conducted in the context of flood risk data allows buyers, sellers, and lenders to price these factors accurately rather than relying on assumptions.

Strategy 6: Engage Qualified Surveyors Early in the Development Process

The complexity of coastal flood compliance — spanning FEMA regulations, state-level tools like the NJDEP CVI, county-level requirements in Miami-Dade, and NFIP insurance mechanics — makes early engagement with qualified surveyors a cost-effective decision rather than an optional one.

Surveyors who specialize in coastal elevation work bring:

- Current knowledge of FIRM revision cycles and pending map amendments

- Proficiency with LiDAR data processing and FEMA compliance documentation

- Experience with LOMA and Letter of Map Revision (LOMR) applications

- Familiarity with both New Jersey and Florida regulatory frameworks

For investors managing multiple coastal assets, understanding why property owners hire surveyors and the full scope of services they provide is foundational to effective portfolio risk management.

Comparing Jersey City and Miami: Key Flood Risk Metrics

| Factor | Jersey City | Miami |

|---|---|---|

| Primary flood tool | NJDEP CVI + Flood Indicator Tool | Miami-Dade Flood Zone Maps + Hotline |

| EC requirement trigger | SFHA designation | All new construction + substantial improvements |

| Climate adjustment tool | Tidal CAFE data | Future sea-level scenario mapping |

| Flood zone hotline | NJDEP regional offices | 305-372-6466 |

| LOMA eligibility | Yes, with licensed EC | Yes, with licensed EC |

| Key high-risk zones | Hudson River waterfront, tidal marshes | Barrier islands, Miami River, canal corridors |

Common Defects Revealed by Flood-Focused Surveys

Flood risk surveys frequently surface property defects that standard inspections miss. In both Jersey City and Miami, surveyors working in coastal zones regularly identify:

- Inadequate foundation drainage — particularly in older structures built before modern floodplain management codes

- Mechanical equipment at or below BFE — HVAC units, electrical panels, and water heaters placed at grade rather than elevated

- Enclosures below BFE without flood vents — enclosed spaces that trap water and create hydrostatic pressure on foundations

- Outdated or missing elevation certificates — especially common in properties last transacted before the 2012 Biggert-Waters Act reforms

A Level 3 full building survey that incorporates flood risk findings provides the most complete picture of a coastal property's condition and compliance status. For older properties in particular, reviewing common defects found in older homes alongside flood risk data creates a comprehensive risk profile.

Conclusion

The convergence of rapid development activity and accelerating coastal flood risk makes 2026 a defining year for property stakeholders in Jersey City and Miami. The tools exist — LiDAR-based elevation surveys, FEMA elevation certificates, New Jersey's CVI and CAFE data, Miami-Dade's flood zone mapping infrastructure — to make informed, resilience-focused decisions at every stage of the property lifecycle.

Actionable next steps for stakeholders in both markets:

- Obtain a current elevation certificate for any coastal property being acquired, refinanced, or substantially improved. Outdated certificates may reflect superseded FIRM panels and incorrect BFEs.

- Run every New Jersey property through the NJDEP Flood Indicator Tool and review its CVI score before committing to acquisition or development.

- Contact Miami-Dade's Flood Zone Hotline (305-372-6466) to confirm parcel-level flood zone designations rather than relying on general map lookups.

- Commission LiDAR-based surveys for large-footprint or high-value coastal projects where centimeter-level accuracy is required for FEMA compliance and resilience design.

- Evaluate LOMA eligibility on any property where survey data suggests the structure sits above the BFE — the insurance savings can be substantial and immediate.

- Design to climate-adjusted elevations on projects with long investment horizons, using CAFE data in New Jersey and future sea-level scenarios in Miami-Dade.

Flood risk is not a future problem in these markets — it is a present financial reality. Surveyors, developers, and investors who treat coastal flood risk mapping and elevation certifications as strategic assets rather than regulatory burdens will be best positioned to protect and grow value through the decade ahead.

References

[1] Czm Cvi – https://www.nj.gov/dep/cmp/czm_cvi.html?utm_source=openai

[2] Flood Tool – https://dep.nj.gov/climatechange/flood-tool/?utm_source=openai

[3] Elevation Certificate – https://www.newjerseyfloodinsurance.org/elevation-certificate/?utm_source=openai

[4] Jersey City.nj – https://riskfinder.climatecentral.org/place/jersey-city.nj.us?utm_source=openai

[5] Hurricane Flood Information – https://www.miami.gov/My-Home-Neighborhood/Hurricane-Guide/Hurricane-Flood-Information?utm_source=openai

[6] Elevation Certificates – https://www.miamidade.gov/global/economy/building/flood-protection/elevation-certificates.page?utm_source=openai

[7] Flood Maps – https://www.miamidade.gov/environment/flood-maps.asp?utm_source=openai

[8] Elevation Certificatefema Flood Certificate – https://www.landsurveyingmiami.com/elevation-certificatefema-flood-certificate?utm_source=openai

[9] Elevation Certificates – https://www.floodsmart.gov/get-insured/elevation-certificates?utm_source=openai