The RICS January 2026 Residential Market Survey recorded a net balance of +29% for new buyer enquiries — the strongest reading since mid-2022. For chartered valuers working across the buy-to-let (BTL) sector, that single data point carries significant weight. It signals that the cautious, flat-line methodology applied throughout 2024 and much of 2025 may now need recalibrating. Valuation surveyor responses to RICS residential recovery signals, specifically adjusting BTL assessments for the Q2 2026 uptick, are becoming one of the most discussed topics in professional practice circles right now.

This article breaks down exactly what the latest RICS signals mean in practice, how the Renters' Rights Act overlays are reshaping rental income assumptions, and what comparable sales analysis tools surveyors should be deploying to produce defensible, accurate BTL valuations in the current market.

Key Takeaways 📌

- RICS January 2026 data shows demand stabilisation and rising buyer enquiries, requiring surveyors to revisit conservative valuation stances adopted during the 2023–2025 correction period.

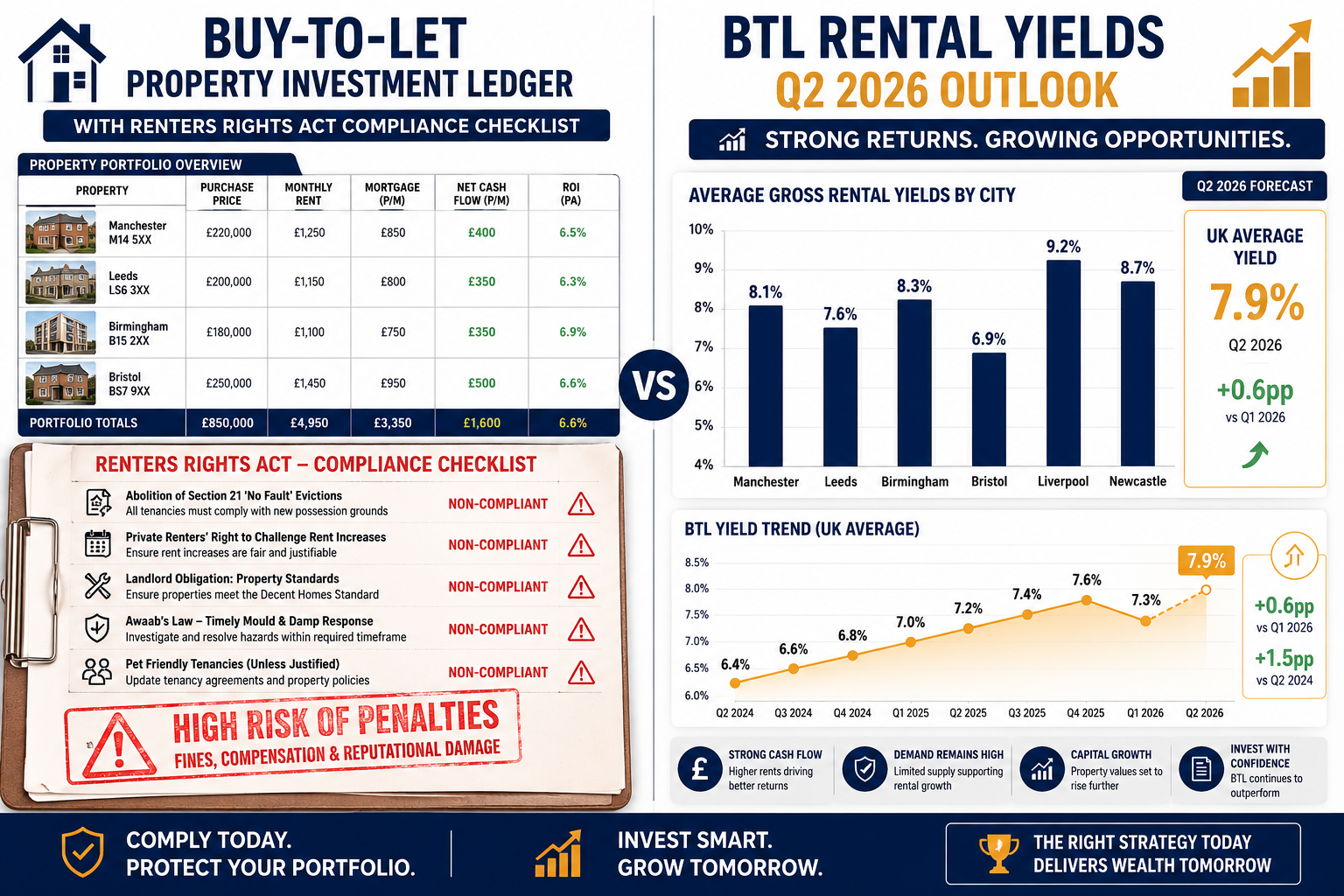

- BTL assessments must now factor in Renters' Rights Act 2025 implications, including the abolition of Section 21 and its effect on void risk and rental income capitalisation rates.

- Comparable sales analysis needs tighter geographic and temporal filters — using comparables older than 6 months in Q2 2026 risks systematic undervaluation.

- Yield compression in prime urban BTL markets is real but uneven; surveyors must distinguish between asset-class segments rather than applying blanket adjustments.

- Professional liability increases when valuations lag market recovery signals — robust methodology documentation is now essential.

Understanding the RICS January 2026 Recovery Signals

The RICS UK Residential Market Survey is one of the most closely watched leading indicators in the property profession. The January 2026 edition delivered several metrics that collectively point toward a genuine, if measured, recovery phase:

| RICS Metric | January 2026 Net Balance | Direction |

|---|---|---|

| New Buyer Enquiries | +29% | ▲ Rising |

| Agreed Sales | +18% | ▲ Rising |

| Price Expectations (3-month) | +22% | ▲ Rising |

| New Instructions | +11% | ▲ Modest increase |

| Rental Demand | +34% | ▲ Strong |

These figures matter enormously for valuation surveyor responses to RICS residential recovery signals because they confirm that the demand-side recovery is outpacing supply — a classic precondition for upward price pressure.

What Demand Stabilisation Actually Means for Valuers

Demand stabilisation does not mean uniform price growth across all property types and locations. Surveyors must resist the temptation to apply a single uplift percentage across an entire portfolio. Instead, the January 2026 data points to three distinct sub-trends:

- Urban flats and smaller BTL units are benefiting most from rental demand growth, as first-time buyers remain constrained by mortgage affordability despite two Bank of England base rate cuts since October 2025.

- Larger HMO properties face a more complex picture — regulatory compliance costs under the Renters' Rights Act 2025 are compressing net yields even where gross rents are rising.

- Regional divergence remains significant. London, Manchester, and Bristol are showing the strongest recovery signals; parts of the East Midlands and some coastal markets remain subdued.

💡 Pull Quote: "A net balance of +29% on buyer enquiries does not give a valuer permission to abandon rigour — it gives them permission to revisit assumptions made in a different market."

For surveyors based in high-demand areas, understanding what factors drive property valuations is the essential starting point before applying any market-recovery adjustments.

Adjusting BTL Assessments: The Renters' Rights Act Overlay

No discussion of valuation surveyor responses to RICS residential recovery signals and adjusting BTL assessments for the Q2 2026 uptick is complete without addressing the Renters' Rights Act 2025, which received Royal Assent in late 2025 and is now fully operative.

Core Legislative Changes Affecting BTL Valuations

The Act introduces several provisions that directly affect how a valuation surveyor must model rental income and void risk:

- Abolition of Section 21 "no-fault" evictions — landlords can no longer recover possession without a specified ground. This increases the risk profile of tenanted BTL properties and must be reflected in capitalisation rates.

- Periodic tenancies only — fixed-term assured shorthold tenancies are abolished. All new tenancies are periodic from day one, giving tenants greater security but reducing landlord flexibility.

- Rent increase restrictions — landlords are limited to one rent increase per year, with tenants having an enhanced right to challenge increases at the First-tier Tribunal.

- Decent Homes Standard extension — now applies to the private rented sector, adding potential capital expenditure obligations that must be factored into investment value assessments.

Recalibrating Capitalisation Rates in 2026

The standard income capitalisation approach for BTL valuations involves dividing net annual rental income by an appropriate yield rate. The Renters' Rights Act changes the inputs on both sides of that equation:

Gross Rent: In many markets, gross rents are rising (RICS data confirms +34% net balance on rental demand). This is positive for income assumptions.

Deductions and Void Allowances: The removal of Section 21 means that evicting a non-paying or problematic tenant now takes longer. Prudent surveyors should increase void allowances from the traditional 4–6 weeks per year toward 6–10 weeks for properties in lower-demand locations.

Capitalisation Rate (Yield): The increased regulatory burden and reduced landlord flexibility justify a modest upward adjustment to the all-risks yield for BTL properties compared to pre-Act benchmarks — typically 0.25% to 0.50% depending on property type and location.

⚠️ Important: Surveyors who fail to document their Renters' Rights Act adjustments explicitly within their valuation reports face increased professional indemnity exposure. The RICS Red Book (Global Standards) requires clear disclosure of all assumptions affecting value.

For landlords seeking to understand how these legislative changes affect their assets, reviewing new property management laws provides useful context before commissioning a formal valuation.

Capital Gains and Disposal Value Considerations

The interaction between rising market values and the Renters' Rights Act also affects disposal valuations. A tenanted BTL property with a periodic tenancy and a sitting tenant now carries a different risk profile than a vacant possession asset. Surveyors preparing capital gains valuations must clearly distinguish between:

- Market Value with Vacant Possession (VP)

- Market Value Subject to Tenancy (STT)

- Investment Value (based on income capitalisation)

The gap between VP and STT values may widen in Q2 2026 as buyer demand for vacant BTL properties increases while tenanted stock becomes harder to sell to owner-occupiers.

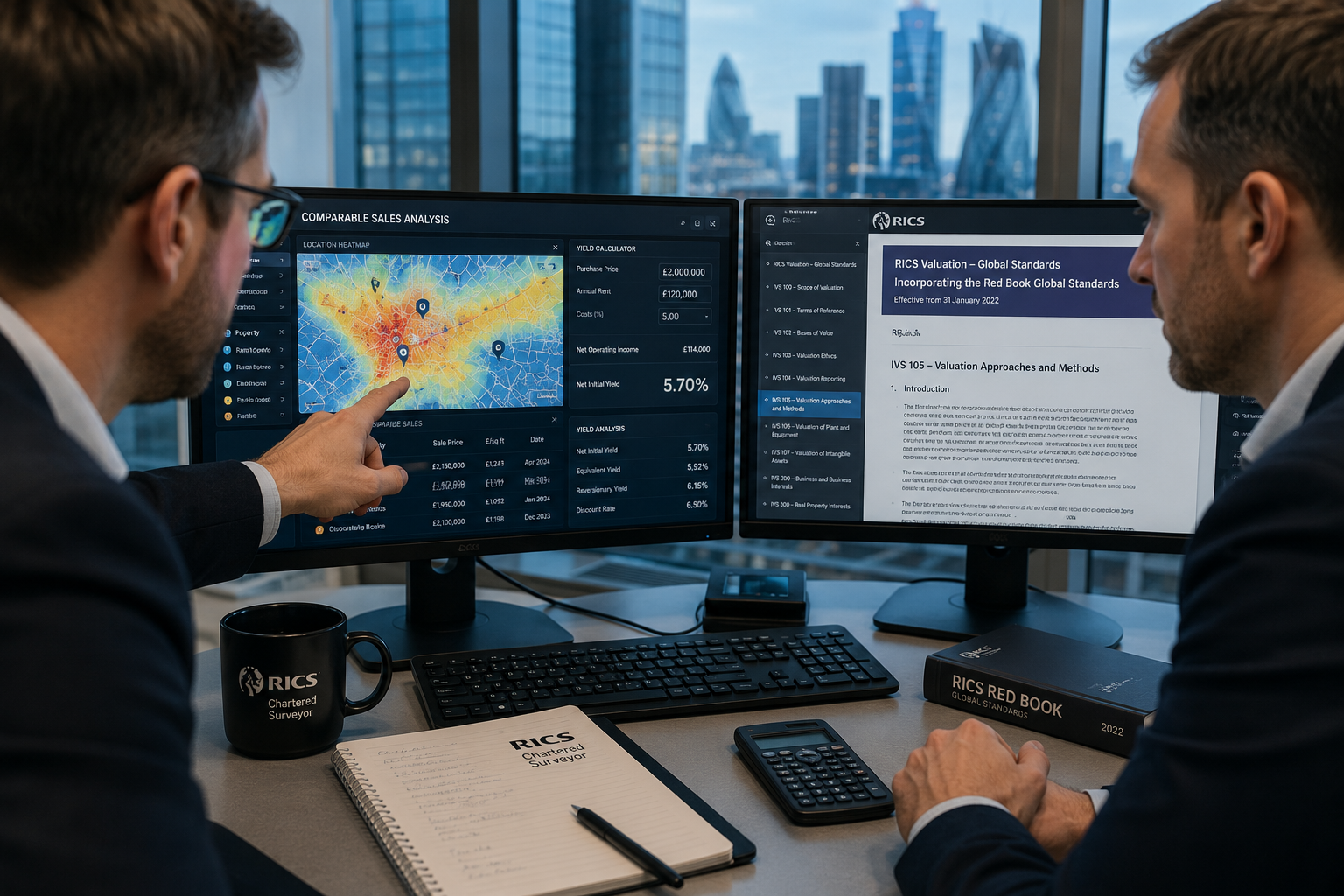

Comparable Sales Analysis Tools for Chartered Surveyors in Q2 2026

The third pillar of valuation surveyor responses to RICS residential recovery signals involves upgrading comparable sales analysis methodology. In a recovering market, stale comparables are a significant source of valuation error.

The 6-Month Comparable Rule in a Rising Market

During the 2023–2025 flat market, using comparables from 12 months prior was often defensible with a modest time adjustment. In Q2 2026, that window must tighten considerably. The recommended approach:

| Comparable Age | Adjustment Required | Reliability |

|---|---|---|

| 0–3 months | Minimal or none | ✅ High |

| 3–6 months | Time adjustment of 1–3% | ⚠️ Moderate |

| 6–12 months | Time adjustment of 3–7% | ⚠️ Use with caution |

| 12+ months | Avoid unless market was stable | ❌ Low reliability |

Key Data Sources for BTL Comparable Analysis

Surveyors should be drawing on multiple data streams to build a robust comparable set:

- HM Land Registry Price Paid Data — essential for confirmed transaction prices, though typically 2–3 months behind the market.

- Rightmove and Zoopla sold price tools — useful for near-real-time signals, though asking prices must be discounted appropriately.

- RICS Comparable Evidence Tool — the profession's own database, increasingly valuable as transaction volumes recover.

- Local estate agent intelligence — particularly important for understanding the gap between asking and achieved prices in specific postcodes.

- EPC register data — increasingly relevant as energy efficiency ratings affect both rental compliance and buyer appetite.

Adjusting for Property-Specific Factors in BTL Comparables

A BTL-specific comparable analysis must go beyond simple £/sq ft adjustments. Key variables to weight include:

- EPC rating — properties below EPC Band C face potential future compliance costs; adjust downward by 2–5% for Band D or below.

- Lease length (for leasehold flats) — short leases below 80 years require significant negative adjustments and specialist advice. Surveyors should consider commissioning a full building survey to identify structural issues that could compound leasehold complications.

- HMO licensing status — licensed HMOs command a premium in high-demand areas but carry compliance costs that must be netted off.

- Condition and recent refurbishment — the Decent Homes Standard now applies to private rentals, making condition assessment central to BTL valuations. A thorough condition survey report should inform any BTL assessment where property condition is uncertain.

Building a Defensible Valuation Report

In a market where values are moving upward, the professional risk shifts from over-valuation (the primary concern during a falling market) to under-valuation — particularly where lenders or clients challenge figures that appear conservative relative to market evidence.

Surveyors should structure BTL valuation reports to include:

- Market commentary section referencing RICS survey data and local transaction evidence

- Explicit Renters' Rights Act assumptions with quantified adjustments

- Comparable evidence grid with time and condition adjustments shown transparently

- Sensitivity analysis showing value range under different yield assumptions

- Limitations and caveats clearly stated in accordance with RICS Red Book requirements

For surveyors working across London and the South East — where the Q2 2026 recovery signals are strongest — understanding the full scope of professional valuation services available can help ensure that BTL assessments are supported by complementary data, including reinstatement cost valuations that inform insurance adequacy.

Practical Workflow: Implementing Q2 2026 BTL Assessment Adjustments

The following step-by-step framework translates the above analysis into a practical workflow for chartered surveyors:

Step 1 — Baseline the Market Position 📊

Review the latest RICS monthly survey data alongside local Land Registry transaction volumes. Establish whether the subject property's micro-market is tracking ahead of, in line with, or behind the national recovery signal.

Step 2 — Audit Existing Comparable Sets 🔍

Discard any comparables older than 6 months without applying explicit time adjustments. Rebuild the comparable set using the most recent transactions within a 0.5-mile radius (urban) or 2-mile radius (suburban/rural).

Step 3 — Apply Renters' Rights Act Adjustments ⚖️

For each BTL property assessed, document the specific legislative provisions that affect value, quantify their impact on void allowances and capitalisation rates, and record these assumptions in the valuation report.

Step 4 — Stress-Test the Income Approach 💷

Run income capitalisation under three scenarios:

- Base case — current market rent, standard void allowance

- Downside — rent freeze scenario under tribunal challenge, extended void

- Upside — rental growth in line with RICS +34% demand signal

Step 5 — Cross-Check Against Sales Comparables 🏘️

Reconcile the income approach value against the comparable sales evidence. Where a significant gap exists, investigate the cause — it may reflect a genuine investment premium or discount, or it may signal an error in either approach.

Step 6 — Document and Disclose 📋

Ensure the final report explicitly records all adjustments, data sources, and assumptions. In a recovering market, a well-documented valuation is the surveyor's best professional protection.

Surveyors seeking an independent perspective on current market values — particularly where a client disputes a figure — can benefit from reviewing guidance on what to do if a home valuation differs from an offer, which helps contextualise the gap between market value and transaction price in the current environment.

Conclusion: Acting on the Q2 2026 Uptick with Professional Precision

The convergence of RICS January 2026 demand stabilisation data, the fully operative Renters' Rights Act, and a recovering transaction market creates both opportunity and obligation for valuation surveyors working in the BTL sector. Valuation surveyor responses to RICS residential recovery signals require more than a simple upward revision of comparable evidence — they demand a structured reassessment of income assumptions, legislative risk overlays, and comparable evidence methodology.

Actionable Next Steps for Surveyors 🎯

- Update internal comparable databases immediately — purge or time-adjust any evidence predating October 2025.

- Create a Renters' Rights Act adjustment protocol for your practice, with standardised void allowance and yield adjustment ranges by property type.

- Engage with RICS guidance on the Red Book application in a recovering market — updated professional statements are expected in H1 2026.

- Communicate proactively with clients — landlords and lenders may have outdated value assumptions based on the 2024–2025 flat market; a brief market update note adds significant professional value.

- Consider condition surveys as a standard precursor to BTL valuations where property age or condition is uncertain — the Decent Homes Standard makes physical condition a direct driver of investment value.

The Q2 2026 uptick is real, but it is not uniform, and it is not unconditional. The surveyors who will serve their clients best — and protect their own professional standing — are those who respond to recovery signals with precision, not enthusiasm.