Coastal flood damage in the UK costs an estimated £1.3 billion per year — and following the significant coastal flooding events of Spring 2026, surveyors, lenders, and property owners are urgently asking the same question: do flood-resilient retrofits actually add measurable value to a property? The answer is increasingly yes — but the methodology for capturing those adjustments in formal valuations remains a work in progress. This article examines Valuation Adjustments for Flood-Resilient Retrofits: RICS Guidance Post-Spring 2026 Coastal Events, exploring what the current RICS framework requires, where guidance gaps exist, and how professional valuers are navigating this fast-moving landscape.

Key Takeaways 📌

- No dedicated RICS guidance note specifically prescribing quantitative valuation uplifts for flood-resilient retrofits existed as of mid-2026 — the Red Book Global Standards remain the governing framework.

- Valuers must consider flood risk and resilience measures as material factors where market evidence supports a premium or mitigates a discount.

- Flood-resilient retrofits (flood doors, raised electrics, tanking, non-return valves) can positively influence insurance costs, mortgage availability, and buyer appetite — all of which feed into market value.

- Resilience certifications and compliance with emerging planning standards are becoming increasingly relevant to obsolescence assessments and future-proofing adjustments.

- Surveyors should never apply generic percentage uplifts without comparable market evidence — evidence-based, property-specific analysis is mandatory.

Understanding the Post-Spring 2026 Context

The Spring 2026 coastal flooding events accelerated conversations that had been building for years. Coastal communities from the Thames Estuary to the Solent experienced surge events that exposed the vulnerability of unretrofitted housing stock. Insurers tightened terms. Mortgage lenders requested additional flood risk assessments. And buyers began asking pointed questions about what — if anything — had been done to protect properties from future inundation.

This environment has placed flood-resilient retrofits firmly on the valuation agenda. A retrofit in this context typically includes one or more of the following interventions:

| Retrofit Type | Description | Typical Cost Range |

|---|---|---|

| Flood doors & barriers | Watertight door seals and demountable barriers | £1,000–£5,000 |

| Raised electrical systems | Sockets, fuse boards relocated above flood level | £2,000–£8,000 |

| Non-return valves | Prevent sewage backflow during flood events | £500–£2,000 |

| Tanking & waterproof renders | Internal/external waterproof coatings | £5,000–£20,000+ |

| Suspended ground floors | Raising floor levels above flood risk zones | £10,000–£30,000+ |

These measures reduce the depth of flooding, the duration of damage, and critically, the cost of reinstatement following a flood event. Understanding the reinstatement cost implications is essential — surveyors working on insurance reinstatement cost valuations will need to factor in both the cost of the retrofit itself and the reduced expected damage costs it delivers.

💬 "The question is no longer whether flood resilience matters to value — it clearly does. The question is how to evidence and quantify it consistently." — Emerging consensus among RICS practitioners, 2026

What the RICS Red Book Actually Says About Flood Resilience

The Governing Framework: Red Book Global Standards

The RICS Valuation – Global Standards (Red Book) remain the primary framework governing how UK valuers approach physical climate risks, including flood. There is, as of mid-2026, no standalone RICS guidance note that prescribes specific valuation adjustments for flood-resilient retrofits. This is an important clarification — some commentary in the property press has implied otherwise.

What the Red Book does require is clear and consequential:

- Material sustainability and climate factors must be considered where they could affect value.

- Valuers must report significant risks and assumptions transparently in their valuation reports.

- Market evidence must underpin any adjustments — generic percentage uplifts applied without comparable support are not compliant.

The RICS has published cross-cutting sustainability and ESG guidance that reinforces these principles, particularly in commercial property contexts. However, the residential sector has been slower to develop robust comparable evidence for resilience premiums, largely because flood-resilient retrofits have not yet been systematically recorded in transaction data at scale.

What Valuers Are Expected to Do in Practice

Even without a specific post-Spring 2026 guidance note, RICS-registered valuers are expected to:

- Identify flood risk exposure using Environment Agency flood zone data, local authority strategic flood risk assessments, and site-specific surveys.

- Assess whether retrofits are present and document their type, age, and condition.

- Seek comparable evidence of sales transactions involving similar retrofitted properties in comparable flood-risk zones.

- Reflect resilience measures in the valuation where market evidence supports a premium or reduced discount.

- Avoid speculative uplifts — if the local market does not yet price in resilience measures, the valuation must reflect that reality.

For a broader understanding of what factors drive property valuations, the top things looked at during a property valuation provides a useful foundation — flood resilience is increasingly joining location, condition, and tenure as a core consideration.

How Flood-Resilient Retrofits Influence Valuation in Practice

The Three Channels of Value Impact

Flood-resilient retrofits affect market value through three primary channels:

1. 🏠 Reduced Physical Damage Risk

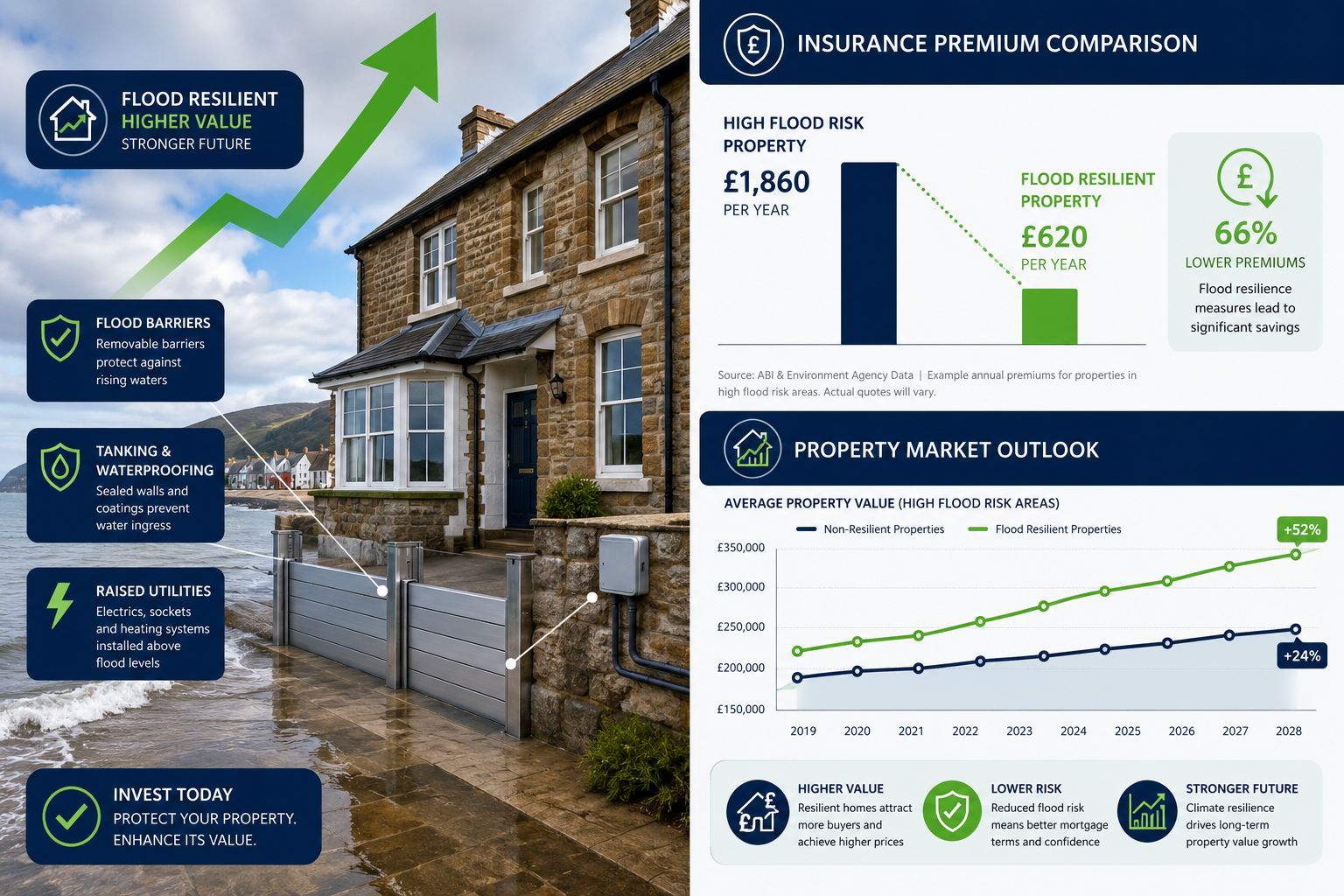

A property fitted with flood doors, raised electrics, and tanking will sustain significantly less damage in a flood event than an unretrofitted equivalent. This reduces the expected reinstatement cost and shortens the period during which the property is uninhabitable. Buyers and lenders increasingly recognise this distinction — particularly following the Spring 2026 events, which provided stark real-world evidence of the difference in outcomes between retrofitted and unretrofitted properties.

2. 🛡️ Insurance Cost and Availability

Flood Re, the UK's flood reinsurance scheme, has helped maintain insurance availability for high-risk properties. However, properties with documented flood-resilient retrofits may attract more favourable premium terms, particularly as insurers develop more granular risk-based pricing models. A reduction in annual insurance costs directly improves the net running cost of a property, which sophisticated buyers factor into offers — particularly in the buy-to-let and investment sectors.

For properties involved in block management, understanding insurance arrangements for blocks is particularly relevant, as flood resilience at the building level can affect premiums across all leaseholders.

3. 💰 Mortgage Lender Appetite

Some mortgage lenders are beginning to apply additional scrutiny — or outright restrictions — to properties in high flood-risk zones without documented resilience measures. A property with a certified retrofit may have a wider pool of available mortgage products, which directly supports market value by broadening the buyer pool.

The Evidence Gap Problem

The central challenge for valuers is that comparable transaction evidence for retrofitted properties remains thin in many areas. This is not a failure of the RICS framework — it is a market maturity issue. Coastal resilience conversations have intensified significantly in 2026, with regulators and planners in multiple jurisdictions tightening design standards [1][6]. The Florida Adaptation Planning Guidebook [7] and California's coastal resilience frameworks [9] illustrate how regulatory requirements can shift rapidly, creating obsolescence risk for non-compliant properties — a factor that valuers must begin to model even where direct comparable evidence is limited.

📊 Key Insight: Where comparable evidence is absent, valuers can use a cost-to-cure approach — estimating the cost of bringing an unretrofitted property to an equivalent resilience standard — as a proxy for the discount applicable to unretrofitted properties. This is not the same as prescribing an uplift, but it provides a defensible basis for adjustment.

Valuation Adjustments for Flood-Resilient Retrofits: RICS Guidance Post-Spring 2026 Coastal Events — Practical Methodology

Step-by-Step Approach for Valuers

The absence of a dedicated RICS guidance note does not leave valuers without a methodology. The following framework draws on existing Red Book requirements and emerging best practice:

Step 1: Flood Risk Classification

- Identify the property's Environment Agency flood zone (1, 2, or 3a/3b).

- Review the most recent strategic flood risk assessment for the local authority area.

- Consider residual risk after any community-level flood defences.

Step 2: Retrofit Inventory and Condition Assessment

- Document all flood-resilient measures present, including installation dates and maintenance records.

- Assess condition — a flood door that has not been maintained or tested may provide limited actual protection.

- Consider whether retrofits are certified (e.g., by the CIRIA Flood Resilience Standard) or self-installed without professional sign-off.

Step 3: Market Evidence Search

- Search for comparable sales in the same flood zone, distinguishing between retrofitted and unretrofitted properties where data allows.

- Engage with local estate agents to understand whether flood resilience is being marketed as a selling point and whether it is influencing achieved prices.

Step 4: Adjustment Methodology

- Where positive market evidence exists: apply a market-supported premium based on comparable analysis.

- Where evidence is absent: consider a cost-to-cure deduction on the unretrofitted comparables rather than an unsupported uplift on the subject property.

- Document all assumptions transparently in the valuation report.

Step 5: Reporting

- Clearly disclose flood risk classification and resilience measures in the valuation report.

- Flag any special assumptions made regarding the effectiveness or longevity of retrofit measures.

- Note where the market has not yet fully priced in resilience — this protects both the valuer and the client.

For properties where a full structural assessment is also needed, a Level 3 Full Building Survey can provide detailed information on building pathology, including moisture ingress, structural integrity, and the condition of flood-resilient measures — all of which feed into the valuation process.

Resilience Certifications, Planning Standards, and Future Obsolescence

The Growing Role of Compliance Standards

One of the most significant emerging valuation considerations is future obsolescence risk for properties that fail to meet evolving planning and design standards. Across multiple jurisdictions, flood resilience requirements are being formalised:

- New Jersey revised its coastal flood rules in early 2026, introducing design standards requiring buildings to be elevated 4 feet above base flood elevation in certain zones [1].

- Boston's Flood Resiliency Building Guidelines set minimum design expectations for flood-vulnerable areas [6].

- Florida's 2026 Adaptation Planning Guidebook provides a framework for how local governments should integrate sea-level rise and flood risk into planning decisions [7].

- California's coastal resilience programme has emphasised the economic case for proactive adaptation [9].

While these are primarily US examples, they illustrate a trajectory that UK planning policy is following. Properties that meet or exceed current resilience standards are better positioned against future regulatory change — a factor that valuers should begin to reflect in their obsolescence assessments, particularly for commercial and investment properties.

Resilience Certifications: What to Look For

No single UK certification standard for flood-resilient retrofits has achieved universal market recognition as of 2026. However, the following indicators carry weight with informed buyers, lenders, and insurers:

- ✅ CIRIA Code of Practice compliance — installation of flood resilience measures in line with industry standards

- ✅ Contractor certification — work carried out by contractors registered with recognised trade bodies

- ✅ Insurance-backed guarantees — particularly relevant for tanking and waterproofing

- ✅ Local authority approval — where planning permission was required for structural changes

- ✅ Flood risk assessment documentation — demonstrating the property-specific rationale for measures chosen

For properties subject to inheritance or capital gains events, the flood resilience status of a property can also affect the basis of valuation. Surveyors providing inheritance tax valuations or capital gains valuations need to apply the same rigorous analysis of flood risk and resilience measures as they would in any market valuation context.

Environmental Issues and Long-Term Value

The environmental issues associated with a property — including flood risk, ground contamination, and climate exposure — are increasingly scrutinised by buyers, lenders, and legal advisers. Post-Spring 2026, these issues have moved from footnotes in survey reports to headline considerations. Valuers who fail to address them adequately face both professional risk and potential liability.

Common Pitfalls and Professional Risk Considerations

What Valuers Must Avoid

Several practices carry significant professional risk in the current environment:

❌ Applying blanket percentage uplifts for flood-resilient retrofits without market evidence — this is non-compliant with Red Book standards and exposes valuers to challenge.

❌ Ignoring flood risk entirely in areas where it is material — post-Spring 2026, this is increasingly difficult to defend and may constitute a failure to report a significant factor.

❌ Over-relying on Flood Re availability as evidence that insurance is not a valuation concern — Flood Re covers only certain property types and does not eliminate all insurance-related value impacts.

❌ Failing to inspect or document retrofit measures — a valuation that references flood resilience without verifying the condition and effectiveness of measures is professionally exposed.

The Importance of Transparent Reporting

The Red Book's requirements around transparent reporting of assumptions and significant risks are not optional. In the post-Spring 2026 environment, a valuation report that does not address flood risk for a coastal or riverside property will face scrutiny from lenders, solicitors, and — in dispute scenarios — expert witnesses. Clear, documented, evidence-based reporting is the valuer's primary professional protection.

Conclusion: Actionable Next Steps for Surveyors and Property Owners

The landscape for Valuation Adjustments for Flood-Resilient Retrofits: RICS Guidance Post-Spring 2026 Coastal Events is clear in one respect: the RICS Red Book framework already requires valuers to address flood risk and resilience measures as material valuation factors. What remains less clear — and what the profession must urgently develop — is a robust, evidence-based methodology for quantifying the value impact of specific retrofit interventions.

For Surveyors and Valuers:

- Build your comparable evidence database now — actively track sales of retrofitted properties in flood-risk zones and document the evidence.

- Engage with local estate agents to understand whether resilience measures are influencing buyer behaviour and achieved prices in your market area.

- Document retrofit measures thoroughly in every valuation report for flood-risk properties — condition, certification, and maintenance history all matter.

- Apply the cost-to-cure methodology where direct comparable evidence is absent — it is defensible and Red Book-compliant.

- Stay current with RICS updates — a dedicated guidance note on flood-resilient retrofit valuations may well emerge in the 12–24 months following the Spring 2026 events.

For Property Owners:

- Commission a professional flood risk assessment before investing in retrofit measures — ensure the measures chosen are appropriate for the specific risk profile of your property.

- Retain all documentation — installation certificates, contractor details, and maintenance records will be required by valuers, lenders, and insurers.

- Seek specialist valuation advice from RICS-registered valuers with demonstrable experience in flood-risk properties. Explore the full range of chartered surveyor valuation services available to ensure the right expertise is applied.

- Consider the insurance implications — engage with your insurer before and after retrofit to document any premium impact.

The Spring 2026 coastal events have made flood resilience a mainstream valuation issue. The profession's response — grounded in the existing Red Book framework, enriched by emerging market evidence, and guided by transparent reporting — will determine how effectively property markets price in resilience and reward those who invest in it.

References

[1] State Walks Back Certain Proposed Changes To Coastal Flooding Regulations – https://www.connellfoley.com/blog/state-walks-back-certain-proposed-changes-to-coastal-flooding-regulations

[2] NHDES 2026 Coastal Resilience Grants Informational Webinar – https://www.youtube.com/watch?v=STxeaYmkk4g

[3] Taking the High Road – FHWA PROTECT Resilience Funding Discussion – https://www.youtube.com/watch?v=XFJnF1j2bqk

[4] Annual Coastal Resiliency Conference – https://www.same.org/event/annual-coastal-resiliency-conference/

[5] Q&A: What Does Coastal Resilience Look Like For US Communities – https://www.stantec.com/en/ideas/content/blog/2026/qa-what-does-coastal-resilience-look-like-for-us-communities

[6] Flood Resiliency Building Guidelines & Zoning Overlay – Boston Planning – http://www.bostonplans.org/planning-zoning/planning-initiatives/flood-resiliency-building-guidelines-zoning-over

[7] 2026 Florida Adaptation Planning Guidebook – https://floridadep.gov/sites/default/files/2026%20Florida%20Adaptation%20Planning%20Guidebook.pdf

[8] FEMA Flood Risk Attachment – https://downloads.regulations.gov/FEMA-2021-0021-0176/attachment_1.pdf

[9] Rising To The Challenge: Coastal Resilience In The Face Of Sea Level Rise – https://opc.ca.gov/2024/12/rising-to-the-challenge-coastal-resilience-in-the-face-of-sea-level-rise/

[10] Commonwealth Calendar Virginia – Coastal Resilience Event – https://commonwealthcalendar.virginia.gov/Event/Details/77160