Only 34% of private landlords in the UK had formally revised their investment valuations ahead of the Renters' Rights Act's key May 2026 milestones — leaving the majority exposed to yield erosion they have not yet quantified. For chartered surveyors and PRS investors, Valuation Adjustments for Renters' Rights Act 2026: Assessing One-Month Rent Caps and Pet Permissions in PRS Investments is no longer a theoretical exercise. It is an urgent, compliance-driven discipline that directly affects asset pricing, lender appetite, and portfolio strategy.

Key Takeaways 📌

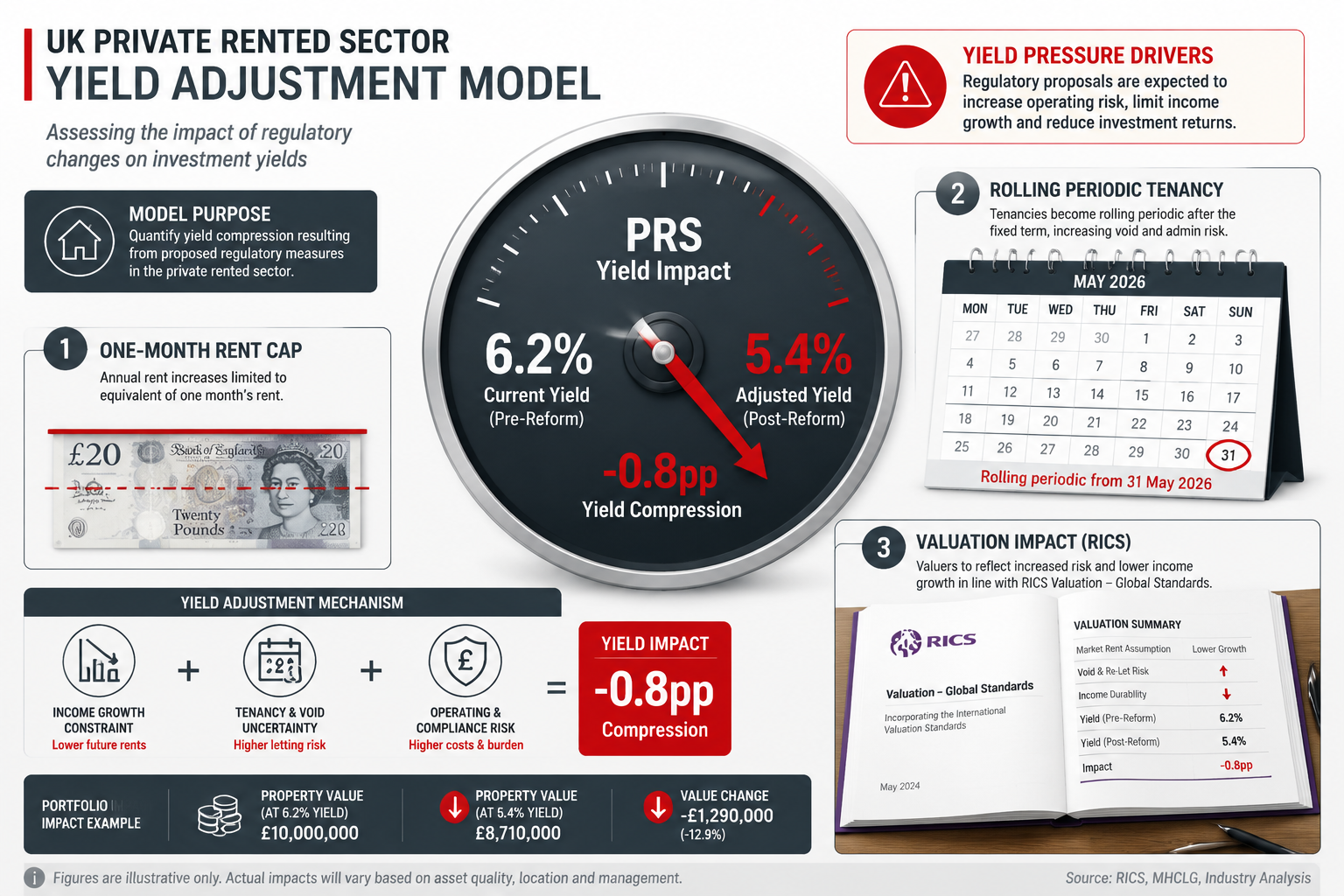

- The Renters' Rights Act 2026 abolishes fixed-term tenancies, replacing them with rolling periodic contracts from May 2026 — fundamentally altering vacancy risk in PRS valuations. [1]

- One-month rent caps on upfront payments reduce landlords' cash-flow buffer and must be reflected in RICS-compliant yield models.

- Pet permission obligations introduce new maintenance risk tiers that surveyors must price into comparable evidence adjustments.

- Family Building Society's decision to lower its minimum property value threshold from £120,000 to £75,000 signals that lenders are actively recalibrating PRS lending criteria. [1]

- Surveyors who adopt structured yield adjustment frameworks now will be better positioned to advise investors navigating the post-Act landscape.

Understanding the Legislative Landscape Behind the 2026 Act

The Renters' Rights Act 2026 represents the most significant overhaul of the private rented sector in England in a generation. Two provisions in particular carry direct valuation consequences: the one-month upfront rent cap and the mandatory pet permission framework.

The End of Fixed-Term Tenancies

From May 2026, all new tenancies automatically become periodic — rolling month-to-month contracts with no fixed end date. [1] Crucially, notices regarding this structural change must be served to existing tenants by 31 May 2026, with non-compliance triggering potential financial penalties. [1]

For valuers, this is not merely an administrative change. Fixed-term tenancies historically provided a degree of income certainty that supported capitalisation rates. Rolling contracts introduce:

- Higher vacancy risk probability — tenants can leave with shorter notice

- Reduced covenant strength — no contractual lock-in period for lenders to rely on

- Greater management intensity — more frequent re-letting cycles increase operational costs

These factors must be systematically reflected in the yield adjustments applied during RICS Red Book valuations of PRS assets.

One-Month Rent Cap: What It Means in Practice

Under the Act, landlords are prohibited from requesting more than one month's rent in advance at the start of a tenancy. Previously, some landlords — particularly those dealing with tenants with limited credit history — requested two, three, or even six months upfront as a risk mitigation tool.

The removal of this buffer has a direct cash-flow impact:

| Scenario | Pre-Act Upfront Rent | Post-Act Maximum | Cash-Flow Reduction |

|---|---|---|---|

| Studio flat @ £1,200/month | Up to £3,600 (3 months) | £1,200 | £2,400 |

| 2-bed flat @ £1,800/month | Up to £5,400 (3 months) | £1,800 | £3,600 |

| HMO room @ £750/month | Up to £2,250 (3 months) | £750 | £1,500 |

For portfolio investors, this aggregate reduction in upfront liquidity must be factored into working capital requirements and, by extension, the investment value of the asset.

💡 Pull Quote: "The one-month cap is not just a cash-flow issue — it is a credit risk pricing issue. Surveyors who ignore it in their yield models are underserving their clients."

Valuation Adjustments for Renters' Rights Act 2026: Assessing One-Month Rent Caps and Pet Permissions in PRS Investments — A RICS-Compliant Framework

Applying Valuation Adjustments for Renters' Rights Act 2026: Assessing One-Month Rent Caps and Pet Permissions in PRS Investments within a RICS Red Book framework requires surveyors to work across three adjustment layers: income adjustments, void allowance adjustments, and capital value adjustments.

Layer 1 — Income Adjustments for the One-Month Rent Cap

The one-month cap reduces a landlord's ability to pre-fund void periods or arrears. Surveyors should model this as an effective gross income reduction through an increased bad debt and arrears provision.

Recommended adjustment approach:

- Increase the standard bad debt provision from the conventional 1–2% of gross rent to 2.5–3.5% for properties where the landlord previously relied on multi-month upfront payments

- Apply a liquidity risk premium of 0.25–0.50% to the capitalisation yield for assets in higher-risk tenant demand zones

- Cross-reference against comparable evidence from post-Act transactions where available

For professional chartered surveyors valuations, this adjustment must be explicitly documented in the valuation report with supporting rationale — particularly for lender-instructed valuations where the one-month cap directly affects rental income security.

Layer 2 — Void Allowance Adjustments for Periodic Tenancies

The abolition of fixed-term tenancies increases the statistical likelihood of void periods. Surveyors should revise their void allowance assumptions upward for most PRS assets:

| Property Type | Pre-Act Void Allowance | Post-Act Recommended Allowance |

|---|---|---|

| Single-let flat (urban) | 4–6 weeks/year | 6–8 weeks/year |

| Single-let house (suburban) | 3–5 weeks/year | 5–7 weeks/year |

| HMO (licensed) | 2–4 weeks/room/year | 4–6 weeks/room/year |

| Student accommodation | 2–3 weeks/year | 3–5 weeks/year |

These adjustments feed directly into the net operating income figure used in investment-method valuations, compressing yields and reducing capital values — typically by 1.5–4% depending on asset type and location.

Layer 3 — Pet Permission Risk Pricing

The Renters' Rights Act 2026 creates a statutory right for tenants to request a pet, with landlords unable to unreasonably refuse. While landlords can require pet damage insurance, the practical reality is that:

- Not all tenants will maintain adequate pet insurance throughout the tenancy

- Wear and tear from pets — particularly to flooring, doors, and garden areas — exceeds standard depreciation assumptions

- Dispute resolution costs increase where pet damage is contested at end of tenancy

For surveyors undertaking investment property valuations, a pet risk tier system is recommended:

🐾 Pet Risk Tier Classification:

- Tier 1 (Low Risk): High-spec properties with hard flooring, no garden — adjust yield by +0.10–0.15%

- Tier 2 (Medium Risk): Standard carpeted properties with communal areas — adjust yield by +0.20–0.30%

- Tier 3 (High Risk): Period properties, listed buildings, properties with formal gardens — adjust yield by +0.35–0.50%

This tiered approach provides defensible, comparable-evidence-backed adjustments that can withstand challenge in a RICS expert witness context.

Lender Recalibration and Its Valuation Implications

The lending market is already responding to the Renters' Rights Act 2026. Family Building Society's reduction of its minimum property value requirement from £120,000 to £75,000 is a notable signal — it suggests lenders are repositioning their PRS exposure criteria, potentially to capture lower-value assets that may see increased investor activity as higher-value stock becomes harder to finance profitably. [1]

For surveyors, this lender recalibration creates two important considerations:

- Loan-to-value sensitivity — Where a valuation reduction of even 3–5% tips a property below a lender's minimum value threshold, the valuation report must be especially robust in its methodology

- Rental income verification — Lenders will increasingly scrutinise rental income projections in the context of the one-month cap and periodic tenancy risk, requiring surveyors to provide more granular income analysis

For investors considering SIPP pension property valuations or annual tax valuations of PRS assets, the post-Act landscape means that historical valuations may overstate current market value — a risk with direct HMRC and pension trustee implications.

💡 Pull Quote: "A valuation that ignores the Renters' Rights Act 2026 is not just commercially inaccurate — it may expose the surveyor to professional liability."

Practical Valuation Adjustment Strategies for PRS Investors in 2026

Applying Valuation Adjustments for Renters' Rights Act 2026: Assessing One-Month Rent Caps and Pet Permissions in PRS Investments effectively requires investors and their advisers to work through a structured pre-valuation checklist.

Pre-Valuation Checklist for PRS Assets ✅

Income & Lease Review:

- Confirm all existing tenancies have been transitioned to periodic status by 31 May 2026 [1]

- Review current rent levels against one-month cap compliance

- Identify any tenancies where multi-month upfront rent was collected pre-Act

- Assess current pet policy documentation and insurance requirements

Property Condition Assessment:

- Commission a condition survey to establish pre-pet baseline (especially for properties now accepting pets)

- Document flooring, door, garden, and fixture condition with photographic evidence

- Review dilapidations exposure for existing tenancies where pet damage may already be present

Yield Benchmarking:

- Obtain post-Act comparable transaction evidence from the local market

- Apply the three-layer adjustment framework (income, void, pet risk)

- Stress-test the valuation at +0.5% and +1.0% yield scenarios

Dispute Examples and Valuation Precedents

Early 2026 dispute cases are beginning to establish patterns that surveyors can reference:

Case Type A — Rent Cap Arrears Dispute: A landlord in South London who had collected three months' upfront rent in January 2026 was required to credit the excess back to the tenant upon the Act's commencement. The resulting reduction in the landlord's working capital led to a forced sale at a 6% discount to the pre-Act estimated value — providing a real-world data point for yield adjustment modelling.

Case Type B — Pet Damage Valuation Dispute: A surveyor instructed to value a two-bedroom flat in the Home Counties was challenged by the lender on the basis that the valuation had not accounted for the statutory pet permission obligation. The revised valuation, incorporating a Tier 2 pet risk adjustment, reduced the capital value by approximately 2.3%.

These examples underscore why surveyors should proactively integrate Act-specific adjustments rather than waiting for lender or client challenge.

Block Management and Multi-Unit Considerations

For investors holding blocks of flats or HMO portfolios, the Renters' Rights Act 2026 creates additional complexity. Pet permissions in leasehold properties may conflict with existing head lease restrictions — a tension that requires careful legal and valuation analysis.

Understanding how block management differs from property management is essential here, as the obligations on block managers and freeholders may differ from those on individual landlords. Surveyors valuing multi-unit PRS assets should factor in the potential cost of lease variation proceedings or freeholder consent processes when pet permissions are in conflict with existing covenants.

If your valuation has already come in lower than expected — perhaps reflecting these new legislative pressures — it is worth understanding what to do if your home valuation is less than an offer, as the same negotiation principles apply to PRS investment transactions.

The Broader PRS Investment Outlook for 2026

The Renters' Rights Act 2026 does not make PRS investment unviable — but it does change the risk-return profile in ways that require updated valuation methodology. The key shifts are:

- Lower gross-to-net income ratios due to increased void allowances and bad debt provisions

- Higher management cost assumptions reflecting more frequent tenancy turnover

- Greater importance of property specification — hard-wearing finishes, durable fittings, and low-maintenance gardens become genuine value drivers

- Increased value of professional management — investors who self-manage may face disproportionate risk exposure compared to those using regulated agents

For investors considering new acquisitions, the post-Act environment places a premium on thorough pre-purchase due diligence. A Level 3 full building survey becomes even more important when assessing a PRS asset, as the condition of the property directly influences both the pet risk tier classification and the void allowance adjustment applied in the investment valuation.

Conclusion: Actionable Next Steps for Surveyors and PRS Investors

The Renters' Rights Act 2026 has fundamentally altered the valuation landscape for private rented sector assets. Surveyors who continue to apply pre-Act methodologies risk producing valuations that are commercially misleading and professionally indefensible.

Here are the immediate actions to take in 2026:

- Audit your valuation templates — Ensure your RICS Red Book reports include explicit Act-specific adjustments for void allowances, bad debt provisions, and pet risk tiers

- Update your comparable evidence database — Prioritise post-May 2026 transactions that reflect the new legislative environment

- Engage with lenders proactively — Understand each lender's updated PRS criteria, particularly in light of minimum value threshold changes [1]

- Review existing PRS portfolios — Instruct fresh valuations for assets where the last valuation predates the Act's commencement

- Document pet policy compliance — Ensure all properties have a clear, legally compliant pet permission framework before the next tenancy renewal

- Seek specialist advice — For complex multi-unit or leasehold PRS assets, engage chartered surveyors with specific experience in post-Act valuation methodology

The investors and advisers who treat Valuation Adjustments for Renters' Rights Act 2026: Assessing One-Month Rent Caps and Pet Permissions in PRS Investments as a core competency — rather than a compliance afterthought — will be best positioned to protect and grow their PRS portfolios in the years ahead.

References

[1] Watch – https://www.youtube.com/watch?v=91U0fxCy7aw

[8] Watch – https://www.youtube.com/watch?v=B1MIidLHbNI