Commercial tenants in the UK collectively dispute hundreds of millions of pounds in service charges every year — and the majority of those disputes stem from a single root cause: opacity. The RICS Professional Standard Service Charges in Commercial Property: RICS 2nd Edition Standards for Building Surveyors in 2026 Valuations and Disputes became effective on 31 December 2025, marking the most significant overhaul of service charge governance in nearly a decade [1][2]. For building surveyors, property managers, landlords, and occupiers, understanding this Standard is no longer optional — it is the benchmark against which professional conduct, valuations, and dispute outcomes will be measured throughout 2026 and beyond.

Key Takeaways 📋

- The RICS 2nd Edition Professional Standard became effective 31 December 2025, with full compliance expected for service charges with year-end dates of 31 December 2026 and beyond [2].

- Management fees must now be fixed at the start of each service charge year and can no longer be calculated as a percentage of budgeted or actual costs [1].

- The 100% cost recovery principle creates a strict ceiling: no more than actual, proper costs may be recovered from tenants [2].

- Eight mandatory minimum performance standards bind all RICS members and regulated firms, raising the bar for professional accountability [4].

- The Standard does not override lease terms but is increasingly used as a benchmark for reasonableness in dispute resolution and expert witness proceedings [1].

Why the RICS 2nd Edition Matters Right Now

The first edition of the RICS Service Charges in Commercial Property code set important foundations, but the commercial property landscape has shifted dramatically. Rising operating costs, greater tenant sophistication, and an increase in contentious lease disputes have exposed gaps in the old framework. The 2nd Edition responds directly to these pressures [5].

💬 "The Standard aims to ensure timely issuance of budgets and year-end certificates while encouraging reduction in dispute causes." — RICS [2]

The Standard applies across the full spectrum of commercial property — retail, office, industrial, and mixed-use — and binds RICS members and regulated firms as a mandatory professional obligation. Non-RICS parties are encouraged to adopt it as best practice [2].

Crucially, the Standard does not function as legislation. The lease remains the primary legal document governing any service charge relationship. However, where a lease is silent or ambiguous, the 2nd Edition is increasingly cited as the indicator of what is reasonable — a fact that every building surveyor acting in a valuation or dispute context must internalise [1].

For those working on commercial valuations, understanding how service charge obligations affect yield, tenant covenant strength, and net income is now inseparable from understanding the 2nd Edition framework.

Core Changes Under the RICS 2nd Edition: A Practical Breakdown

1. 🚫 Management Fee Restructuring

One of the most commercially significant changes is the prohibition on percentage-based management fees. Under the 2nd Edition, fees must be fixed at the start of each service charge year [1]. This eliminates the perverse incentive for managers to allow costs to inflate — since a higher total spend previously meant a higher fee.

What this means in practice:

- Fees must be agreed and documented before the service charge year begins.

- Any mid-year adjustments require transparent justification.

- Surveyors auditing accounts should flag any fee that appears to have been calculated retrospectively as a percentage of outturn costs.

2. 💰 The 100% Cost Recovery Principle

The Standard mandates that managers seek to recover no more than 100% of proper and actual costs of service provision [2][7]. This sounds straightforward, but its implications are wide-reaching:

| Cost Type | Recoverable? |

|---|---|

| Routine maintenance and repairs | ✅ Yes |

| On-site management staff costs | ✅ Yes (with full disclosure) |

| Landlord's asset management costs | ❌ No |

| Rent collection costs | ❌ No |

| Marketing of void units | ❌ No |

| Insurance for void properties | ❌ No |

| Initial fit-out or new plant installation | ❌ No (unless expressly agreed) |

| Improvement works beyond repair | ❌ No (unless justified) |

The expanded list of non-recoverable costs is particularly important for surveyors preparing service charge budgets or reviewing year-end accounts on behalf of tenants [1].

3. 🏦 Account Segregation and Interest

Service charge monies held in advance must now be kept in discrete or virtual accounts. Any interest earned on those funds must be credited to the service charge — not retained by the landlord or property manager — after bank charges and applicable tax deductions [1].

This is a direct response to longstanding complaints from occupiers about landlords benefiting financially from holding large advance payments. Building surveyors conducting audits should verify account structures as a standard step in their review process.

4. 📢 Commission and Rebate Disclosure

Any commissions, rebates, or third-party payments received in connection with service charge expenditure — most commonly buildings insurance commissions — must be declared in the service charge accounts [1]. Landlords may retain commission only where it reasonably reflects work undertaken on behalf of the service charge.

This has direct relevance for service charge accounting and budgeting reviews, where undisclosed commissions have historically been a source of significant tenant grievance.

5. 📊 Industry Standard Cost Classifications

All service charge budgets and actual expenditure reports must now use Industry Standard Cost Classifications [7]. On-site management costs must be explicitly shown and allocated under the 'site management cost' heading. This standardisation makes it far easier to:

- Compare costs across similar properties.

- Identify anomalies during audit.

- Present clear evidence in dispute proceedings.

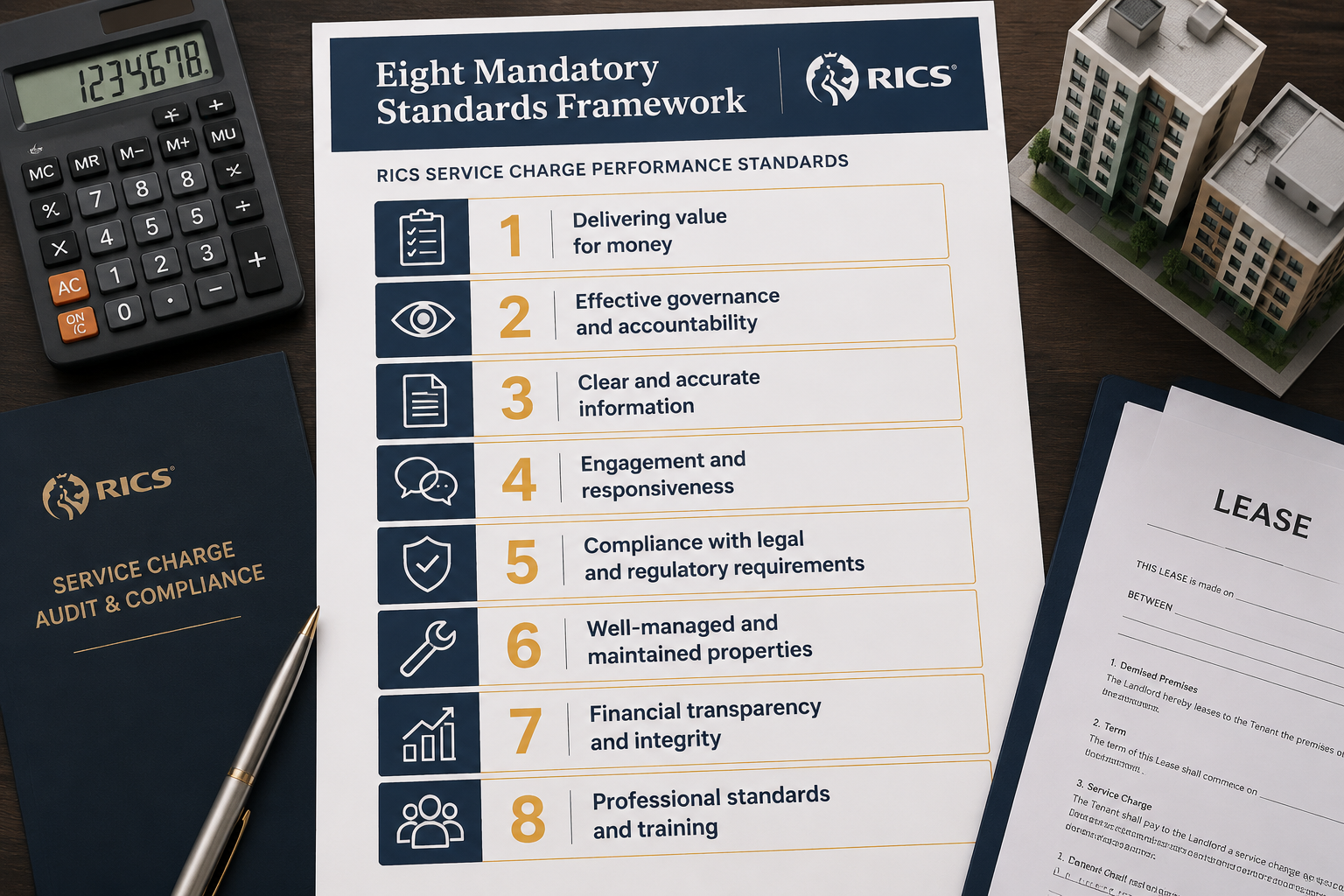

The Eight Mandatory Performance Standards: A Surveyor's Checklist

The 2nd Edition establishes eight mandatory minimum acceptable performance standards that bind all RICS members and regulated firms [4]. Building surveyors — whether acting for landlords, tenants, or as independent experts — should use these as a structured audit framework.

✅ Mandatory Performance Standards Checklist:

- Budget issuance — Budgets must be issued before the start of the service charge year.

- Year-end certificates — Certified accounts must be issued within a defined timeframe after year-end.

- Cost classification — All costs must follow Industry Standard Cost Classifications.

- Management fee transparency — Fees must be fixed, disclosed, and agreed in advance.

- Account segregation — Advance payments must be held in discrete or virtual accounts.

- Interest allocation — Interest earned on held funds must be credited to the service charge.

- Commission disclosure — All commissions and rebates must be declared.

- Non-recoverable cost exclusion — Landlord investment and void costs must be excluded from recovery.

For surveyors undertaking property inspections or block management reviews, this checklist provides a robust, defensible framework for assessing compliance.

Implications for 2026 Valuations

The 2nd Edition has direct consequences for how commercial properties are valued in 2026. A service charge that is non-compliant with the Standard — whether through inflated management fees, undisclosed commissions, or improper cost recovery — represents a latent liability that affects the net income of a property and, therefore, its capital value.

Surveyors preparing commercial valuations should now routinely:

- Review service charge budgets and accounts against the 2nd Edition framework before opining on value.

- Assess tenant covenant strength in the context of service charge disputes — a tenant actively withholding payments represents a different risk profile than one paying under protest.

- Consider the impact of non-recoverable costs on net effective rent calculations.

- Flag undisclosed commissions as a potential adjustment to income.

For properties subject to leasehold extension or enfranchisement valuations, service charge compliance also affects the reasonableness of ground rent and maintenance obligations — factors that directly influence premium calculations.

Similarly, for capital gains valuations, a history of service charge disputes or non-compliance may indicate suppressed market value or deferred liability, both of which require careful consideration in the valuation narrative.

Service Charges in Commercial Property: RICS 2nd Edition Standards for Building Surveyors in 2026 Valuations and Disputes — The Expert Witness Dimension

When service charge disputes escalate to formal proceedings — whether through arbitration, expert determination, or the courts — the 2nd Edition has become the primary reference standard for expert witnesses [1][3].

Building surveyors acting as expert witnesses in 2026 should be prepared to:

Address Lease Primacy vs. Standard Benchmarking

The Standard does not override the lease. However, where a lease is ambiguous or silent, tribunals and courts are increasingly willing to use the 2nd Edition as evidence of what a reasonable landlord or manager would do [1]. Expert witnesses must be able to articulate clearly where the lease and the Standard align — and where they diverge.

Quantify Non-Compliant Charges

Using the expanded non-recoverable cost list and the Industry Standard Cost Classifications, surveyors can now produce structured, comparable analyses of disputed service charge accounts. This is far more persuasive in proceedings than a general assertion that costs seem high.

Navigate the ICAEW Alignment

The 2nd Edition references ICAEW Technical Release TECH 09/14, which sets best practice for accountants' reports on commercial property service charge accounts [6]. Building surveyors working alongside accountants in dispute proceedings should understand how this technical release interacts with the RICS Standard — particularly regarding the scope and limitations of accountants' review reports.

Apply the Dispute Resolution Guidance

The Standard provides explicit guidance on dispute resolution pathways, encouraging parties to resolve disagreements without litigation where possible [2]. Expert witnesses who can demonstrate familiarity with these pathways — and show that a party failed to follow them — strengthen their client's position considerably.

For surveyors involved in Section 20 major works disputes, where service charge recovery for large capital expenditure is frequently contested, the 2nd Edition's clarity on improvement works versus repair is especially valuable.

Service Charges in Commercial Property: RICS 2nd Edition Standards for Building Surveyors in 2026 Valuations and Disputes — Practical Audit Steps

Whether acting for a landlord, tenant, or as an independent auditor, a structured approach to service charge review under the 2nd Edition should follow these practical steps:

Step 1 — Obtain the lease and all service charge documentation

Review the lease's service charge provisions first. Identify any express inclusions or exclusions that differ from the Standard.

Step 2 — Check budget issuance timing

Was the budget issued before the start of the service charge year? Late budgets are a compliance failure under the eight mandatory standards.

Step 3 — Verify cost classification

Are all costs presented using Industry Standard Cost Classifications? Are on-site management costs separately identified?

Step 4 — Audit management fees

Was the management fee fixed at the start of the year? Is there any evidence it was calculated as a percentage of outturn costs?

Step 5 — Review account segregation

Are advance payments held in discrete or virtual accounts? Has interest been credited to the service charge?

Step 6 — Identify non-recoverable costs

Has any landlord investment cost, void property cost, or improvement-beyond-repair cost been included? These must be excluded or expressly justified.

Step 7 — Check commission disclosure

Have all commissions and rebates — particularly insurance commissions — been declared in the accounts?

Step 8 — Assess year-end certification

Was the certified account issued within the required timeframe? Are the certifications compliant with ICAEW TECH 09/14 standards? [6]

For complex multi-let commercial properties, this audit process may also intersect with insurance reinstatement cost valuations, where the allocation of insurance premiums through the service charge must be clearly documented and disclosed.

Transition Timeline: What Happens Between Now and December 2026?

| Date | Milestone |

|---|---|

| 31 December 2025 | RICS 2nd Edition becomes effective [1][2] |

| January–June 2026 | Early adopters implement full compliance; RICS encourages proactive adoption |

| 31 December 2026 | Full compliance expected for all service charges with this year-end date [2] |

| 2027 onwards | Non-compliance increasingly difficult to defend in disputes or regulatory review |

The transition period creates a practical challenge: service charges with year-end dates before 31 December 2026 may still be governed primarily by the 1st Edition framework, while those with year-end dates from 31 December 2026 must fully comply with the 2nd Edition [2]. Surveyors advising clients during this window must be clear about which edition applies to each specific service charge year under review.

Conclusion: Actionable Next Steps for Building Surveyors in 2026

The RICS 2nd Edition represents a genuine step-change in how service charges in commercial property are managed, reported, and contested. For building surveyors, the practical implications are immediate and far-reaching — from how valuations are prepared to how expert evidence is structured in dispute proceedings.

Actionable next steps for building surveyors in 2026:

- Download and study the full RICS 2nd Edition Standard — familiarity with all eight mandatory requirements is non-negotiable for RICS members [7].

- Update audit templates and checklists to reflect Industry Standard Cost Classifications and the expanded non-recoverable cost list.

- Review existing management fee structures for any clients whose fees are currently percentage-based — these must be restructured before the relevant service charge year begins.

- Engage with ICAEW TECH 09/14 to understand how accountants' review reports interact with RICS obligations [6].

- Brief landlord and tenant clients on the transition timeline and the implications of non-compliance for both valuations and dispute outcomes.

- Seek specialist advice where lease terms conflict with the Standard — the interplay between lease primacy and Standard benchmarking is the most legally complex area of the new framework [1][3].

The Standard's transparency-first approach benefits the entire commercial property ecosystem. Tenants gain clearer, more defensible accounts. Landlords and managers who comply gain protection from disputes. And building surveyors who master the 2nd Edition gain a significant professional advantage in an increasingly complex market.

References

[1] The New RICS Service Charge Standard: What It Is And Changes For 2026 – https://www.stevens-bolton.com/insights/102miag/the-new-rics-service-charge-standard-what-it-is-and-changes-for-2026/

[2] Service Charges In Commercial Property – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/real-estate-standards/service-charges-in-commercial-property

[3] The New RICS Service Charge Code: What Landlords, Tenants And Advisers Need To Know – https://broadfield-law.com/thought-leadership/the-new-rics-service-charge-code-what-landlords-tenants-and-advisers-need-to-know/

[4] RICS Professional Standard — Watch – https://www.youtube.com/watch?v=sC_C-aVDAd8

[5] RICS Second Edition Service Charge Code – https://www.ube.ac.uk/whats-happening/articles/rics-second-edition-service-charge-code/

[6] What RICS New Professional Standard Means For Accountants – https://www.icaew.com/insights/viewpoints-on-the-news/2026/apr-2026/what-rics-new-professional-standard-means-for-accountants

[7] Service Charges In Commercial Property 2nd Edition (PDF) – https://www.rics.org/content/dam/ricsglobal/documents/standards/Service-Charges-in-Commercial-Property-2nd-edition.pdf