Nearly half of all UK homes listed for sale in April 2026 were withdrawn unsold — and overvaluing is the primary culprit. That single statistic should give every buyer pause before signing on the dotted line. In a market where asking prices and true property values are diverging at alarming rates, a RICS building survey in 2026 is no longer a nice-to-have — it is your most powerful tool for UK buyer protection against overvalued homes.

At Prince Surveyors, we are seeing this play out daily. Buyers who skip an independent survey are walking into properties priced on optimism, not evidence. This article explains exactly what is happening in the 2026 market, what each RICS survey level offers, and how to use one to protect your investment.

Key Takeaways 📋

- 46.7% of UK homes listed in April 2026 were withdrawn unsold, largely due to overvaluing by estate agents.

- Buyer demand hit its weakest point since August 2023, with a net balance of -39% recorded in March 2026.

- Halifax and Nationwide diverged in April 2026 (-0.1% vs +0.4% month-on-month), reflecting genuine market uncertainty.

- Three RICS survey levels exist — choosing the right one for your property type can save you thousands.

- Survey findings give you legal grounds to renegotiate the purchase price or walk away entirely.

The 2026 UK Housing Market: A Fragile and Contradictory Picture

The April 2026 data tells a story of a market pulling in two directions at once. Halifax reported a -0.1% month-on-month price fall, while Nationwide recorded a +0.4% rise over the same period. These contradictory headline figures mask a much more turbulent reality beneath the surface.

The March 2026 RICS Residential Market Survey painted a stark picture. New buyer enquiries fell to a net balance of -39% — the weakest demand reading since August 2023. Agreed sales collapsed to -34% net balance, down sharply from -13% in February. Near-term price expectations plummeted to -43% net balance, signalling that many in the industry expect further downward pressure in the months ahead.

"Committed purchasers are continuing, but the recent increase in mortgage rates is going to negatively affect an already fragile buying market." — James Perris, surveyor, London

Regional divergence is stark. London faces the sharpest price pressure at -40%, followed by East Anglia (-26%) and the South East (-24%). By contrast, Northern Ireland, Scotland, and the North West are reporting firmer price trends. This means the risk of overpaying is not uniform — it is concentrated in specific regions and property types.

Adding to buyer risk: a recurring issue flagged across the industry is the absence of Building Regulations Completion Certificates on many properties. This is a significant due diligence gap that a thorough survey will flag.

Despite near-term pessimism, 33% more surveyors still expect prices to be higher in 12 months' time — so this is not a crash, but it is a correction. In that environment, overpaying by even 5–10% today carries real financial consequences.

Why are so many homes being withdrawn unsold? Estate agents, incentivised to win instructions, have been systematically overvaluing properties to secure listings. When buyers either cannot secure mortgage offers at inflated asking prices, or when surveys reveal defects that justify lower valuations, sales collapse. The 46.7% withdrawal rate in April 2026 is the direct result.

RICS Building Survey 2026: UK Buyer Protection Starts Here

Understanding which survey you need is the first step in protecting yourself. RICS offers three distinct levels, and choosing the wrong one is a costly mistake. You can explore which building survey is right for your property in more detail, but here is a clear breakdown.

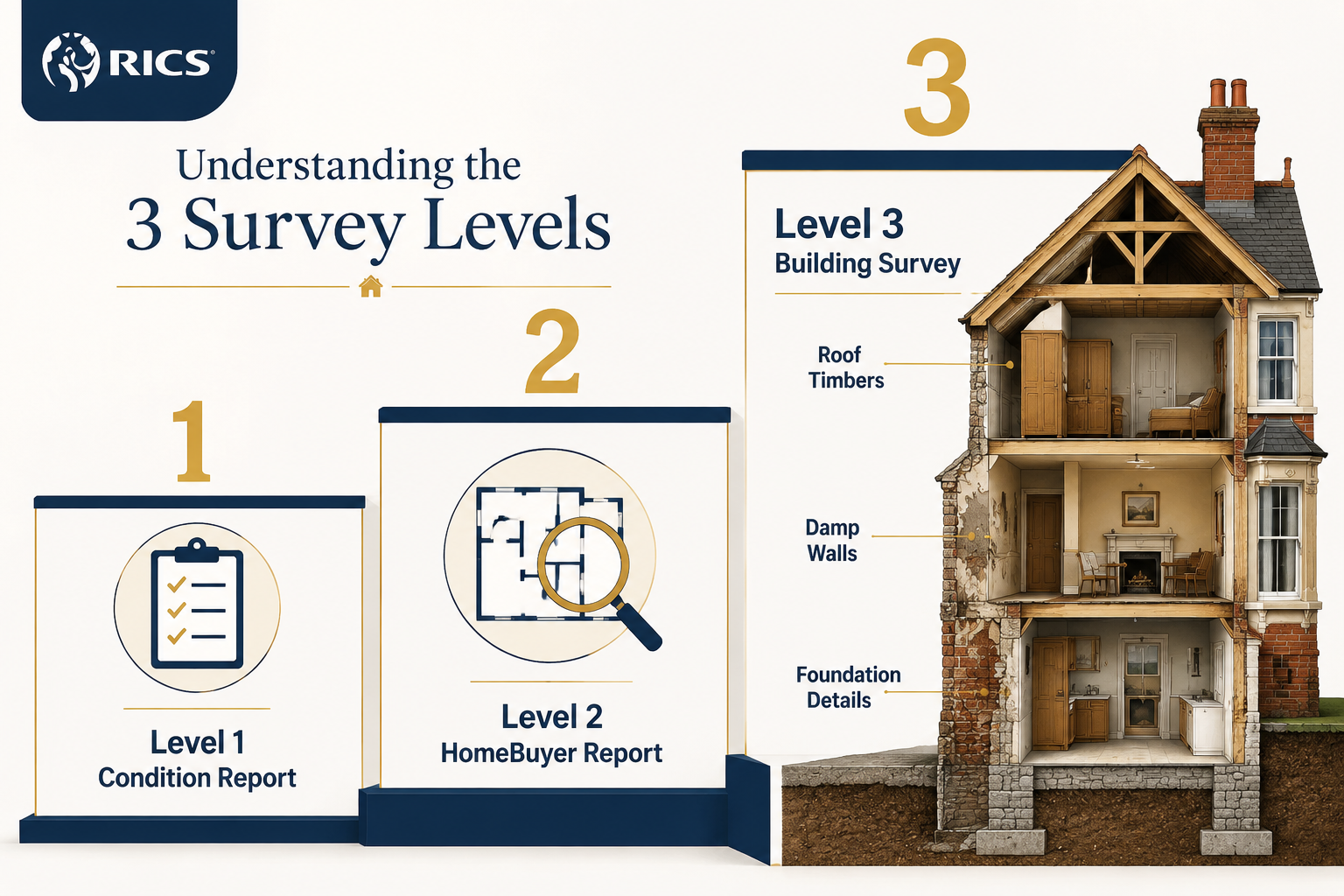

The Three RICS Survey Levels Explained

| Survey Level | Best For | Typical Cost | Valuation Included? |

|---|---|---|---|

| Level 1 – Condition Report | New builds, modern homes in good condition | £250–£400 | No |

| Level 2 – HomeBuyer Report | Conventional properties built post-1900 | £400–£1,000 | Optional |

| Level 3 – Building Survey | Older, larger, or non-standard properties | £600–£1,500+ | Optional |

🔵 Level 1: Condition Report

The most basic option, the Condition Report uses a traffic-light rating system to flag obvious issues. It is suitable for newer properties in demonstrably good condition. It does not include a valuation and offers limited narrative detail. For most buyers in 2026, this level provides insufficient protection.

🟡 Level 2: HomeBuyer Report

The RICS Level 2 HomeBuyer Report is the most commonly commissioned survey in the UK. It covers accessible and visible parts of the property, flags defects, and can include a market valuation. If you are buying a conventional semi-detached or terraced house built after 1900, this is typically the minimum you should commission. Learn more about what a RICS HomeBuyer Report covers before deciding.

Modern flats may be adequately covered by a Level 2, though older or high-rise apartment blocks — particularly those with potential cladding concerns — often require specialist checks or a Level 3.

🔴 Level 3: Full Building Survey

The Level 3 Full Building Survey is the most comprehensive option available. It examines the structure and fabric of the building in detail, including roof spaces, subfloor areas, and wall construction. It provides a thorough assessment of defects, their likely causes, and recommended remedial action.

If you are buying a Victorian terrace, an Edwardian cottage, a period conversion, or any property over 80 years old, a Level 3 is not optional — it is essential. Our guide on what a Level 3 Building Survey involves explains the full scope in plain English.

How Survey Findings Protect You From Overpaying

This is where a RICS building survey in 2026 delivers direct, measurable UK buyer protection against overvalued homes.

Here is how the process works in practice:

- 🏠 You agree a purchase price based on the asking price or a competitive offer.

- 🔍 A RICS surveyor inspects the property and identifies defects — damp, structural movement, roof deterioration, or missing compliance certificates.

- 📄 The survey report quantifies the cost of remediation. For example: £15,000 for roof repairs, £8,000 for damp treatment.

- 💬 You formally request a price reduction equivalent to the repair costs — or ask the seller to complete works before exchange.

- ✅ You either renegotiate to a fair price, or you walk away with your deposit intact.

This is not aggressive — it is informed. And it is entirely standard practice. A mortgage lender's valuation, by contrast, is a desk-based or brief inspection conducted for the lender's benefit, not yours. It will not identify a failing roof or rising damp. It simply confirms whether the property offers sufficient security for the loan.

A mortgage valuation protects the bank. A RICS survey protects you.

For a deeper understanding of the differences between survey types and when each applies, our full building survey vs HomeBuyer survey comparison is an excellent starting point.

Common Defects That Justify Price Renegotiation in 2026

Older UK housing stock — which makes up the vast majority of the market — carries predictable risks. Our surveyors regularly identify the following in Level 2 and Level 3 reports:

- Roof defects – missing tiles, failing flashings, deteriorated felt (see our roofing survey guidance)

- Damp and penetrating moisture – particularly in pre-1919 solid wall properties

- Structural movement – cracking, subsidence, lintel failure

- Electrical and heating systems beyond serviceable life

- Absence of Building Regulations certificates for extensions or conversions

- EPC and MEES compliance issues — increasingly relevant given upcoming energy efficiency requirements (see our EPC and MEES building survey guide)

Each of these findings represents a negotiating lever. In a market where 46.7% of properties are being withdrawn because sellers have priced unrealistically, buyers with survey evidence are in a stronger position than at any point in recent years.

For a comprehensive list of what to look out for, our piece on 11 common defects in older homes is essential reading before you exchange.

Conclusion: Do Not Let Overvaluing Cost You

The 2026 UK property market is not in freefall, but it is under significant stress. Buyer demand is at a near three-year low, agreed sales are collapsing, and nearly half of all listed properties are being pulled from the market because sellers and their agents have misjudged pricing. In this environment, the case for a RICS building survey as a UK buyer protection tool has never been stronger.

Here are your actionable next steps:

- Do not rely on a mortgage valuation as your only assessment of a property's condition or worth.

- Match the survey level to the property — Level 2 for post-1900 conventional homes; Level 3 for anything older, larger, or non-standard.

- Use survey findings to negotiate — defects discovered are legitimate grounds for price reduction.

- Commission early — a survey before you exchange gives you time to act on findings without pressure.

- Choose an independent RICS-regulated firm with no commercial relationship to the estate agent or seller.

At Prince Surveyors, we provide independent RICS-accredited surveys across London and the South East. Our surveyors work solely in your interest — not the lender's, not the agent's.

📞 Ready to Protect Your Purchase?

Get in touch with Prince Surveyors today. Whether you need a Level 2 HomeBuyer Report or a comprehensive Level 3 Full Building Survey, our team will ensure you know exactly what you are buying — and what it is genuinely worth.

👉 Explore our full range of building survey services or contact us directly to discuss your property.