Forty-three percent of surveyor respondents in January 2026 anticipated higher prices over the year ahead — the most optimistic price outlook recorded since February 2025 [1]. That single data point captures the paradox at the heart of the current UK residential market: cautious optimism sitting alongside sharp regional divergence, short-term volatility, and long-term confidence that is quietly building. For building surveyors, this creates both a challenge and a significant professional opportunity.

The RICS January 2026 Residential Survey: Building Surveyor Strategies for Regional Price Divergences and Buyer Confidence Boosts is more than a market snapshot. It is a strategic roadmap for surveyors who want to deliver genuinely useful, regionally tailored advice to buyers, sellers, and investors navigating one of the most geographically uneven property markets in recent memory. Understanding the data — and knowing how to act on it — is what separates good surveyors from great ones in 2026.

Key Takeaways 📋

- National prices are stabilising, with the house price net balance improving to -10% in January 2026, up from -19% in October 2025 [1].

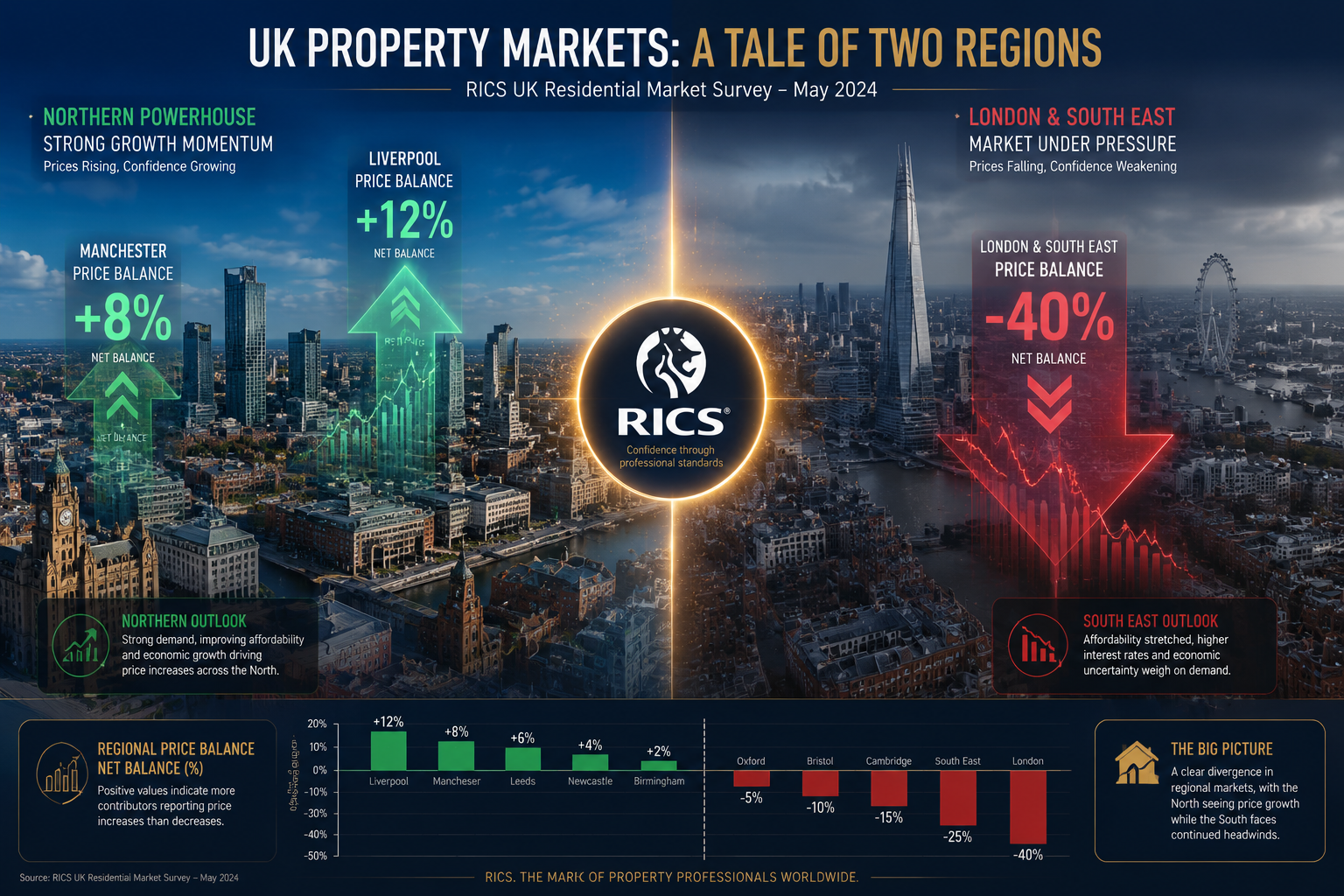

- Regional divergence is stark: Scotland, Northern Ireland, and the North West are rising, while London (-40% net balance in February) and the South East face sustained downward pressure [1][3].

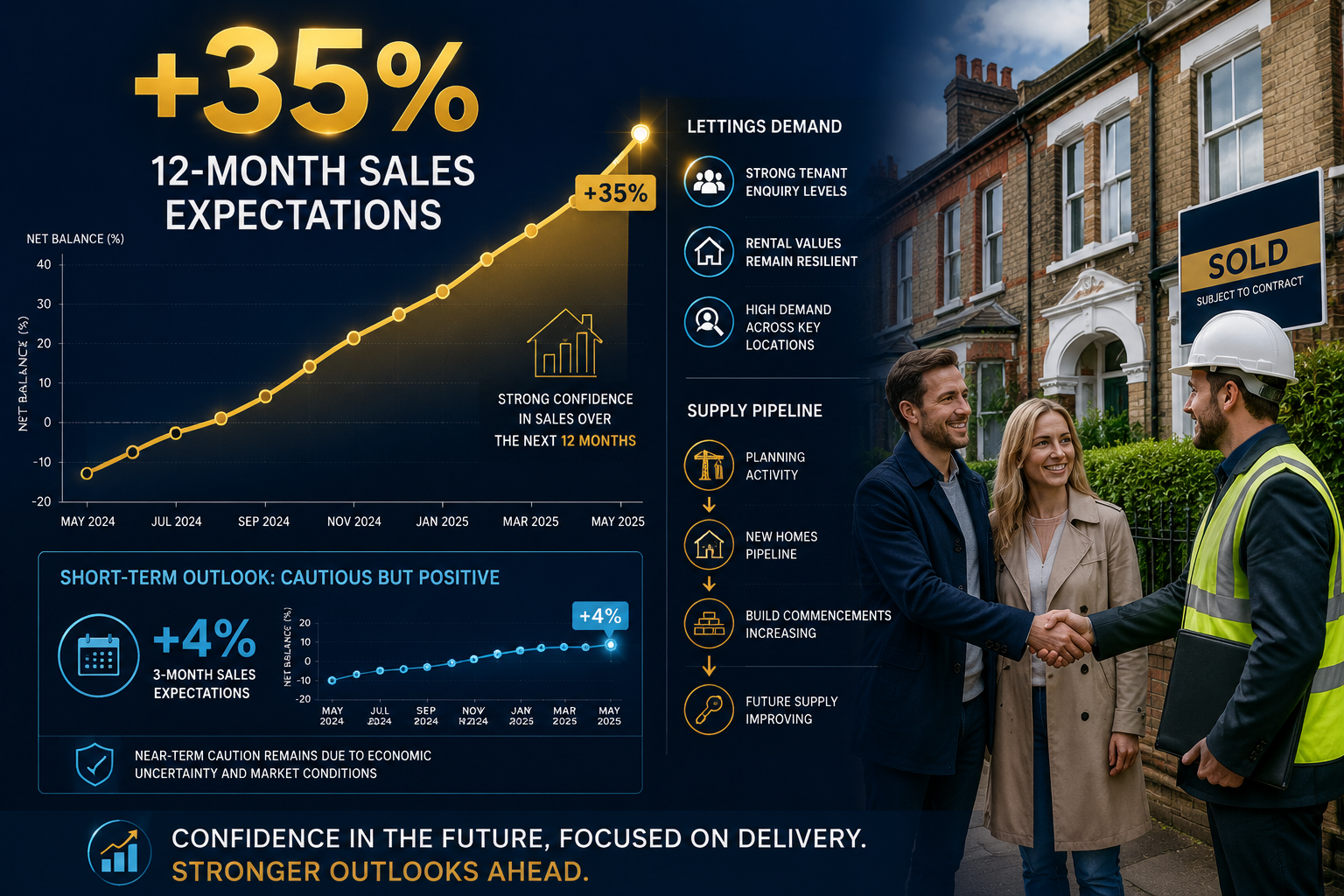

- Long-term buyer confidence is strong: 12-month sales expectations hit +35% net balance in January 2026 — the strongest reading since December 2024 [1].

- Short-term caution persists: Geopolitical uncertainty pushed new buyer enquiries back down to -26% in February after a January improvement to -15% [3].

- Surveyors must adapt: Tailored Level 3 building surveys, regionally specific defect checklists, and clear condition reporting are essential tools for boosting transaction certainty in this environment.

Understanding the RICS January 2026 Data: What the Numbers Really Mean

National Recovery Signals — With Important Caveats

The January 2026 RICS Residential Market Survey delivered a cautiously encouraging headline. The national house price net balance improved to -10% over the past three months, recovering meaningfully from the low of -19% recorded in October 2025 [1]. New buyer enquiries climbed to -15% net balance in January, up from -21% in December and -29% in November — a clear directional improvement [1].

Agreed sales also showed progress, recording a net balance of -9% in January 2026, the least negative reading since June 2025 [1]. These are not boom-time numbers, but they represent a market that is finding its floor and beginning to recover.

💬 "The data points toward a market in transition — not yet in full recovery, but no longer in retreat. For surveyors, that transition period is exactly when precise, evidence-based reporting matters most."

However, the February 2026 follow-up data introduced a note of caution. New buyer enquiries fell back to -26%, and agreed sales dipped to -12% as geopolitical tensions and interest rate uncertainty weighed on sentiment [3]. RICS Head of Market Research Tarrant Parsons noted that "deterioration in the geopolitical backdrop has clearly weighed on confidence" [3]. The lesson: early-year optimism is real, but it is fragile.

The Lettings Market: A Parallel Story

The lettings market added another layer of complexity. Tenant demand increased in the three months to January 2026, ending two consecutive quarters of flat or negative readings [1]. With rental prices expected to continue rising amid constrained supply, the lettings sector is providing an important counterbalance to sales market volatility. For surveyors advising landlord clients, this signals continued demand for condition assessments and compliance-focused inspections.

Regional Price Divergences: A Surveyor's Strategic Map

North vs South — The Defining Story of 2026

The RICS January 2026 Residential Survey: Building Surveyor Strategies for Regional Price Divergences and Buyer Confidence Boosts framework must begin with geography. The regional picture in early 2026 is arguably the most divergent it has been in years [1][3].

Regions showing upward price pressure:

- 🟢 Scotland — Strong upward price trends

- 🟢 Northern Ireland — Consistent growth momentum

- 🟢 North West England — Positive price trajectory

- 🟢 North of England — Resilient performance

Regions experiencing downward price pressure:

- 🔴 London — Net balance of -40% in February 2026

- 🔴 South East — Net balance of -24%

- 🔴 East Anglia — Net balance of -26%

- 🔴 South West — Continued negative readings

| Region | Price Trend (Jan–Feb 2026) | Key Driver |

|---|---|---|

| Scotland | ↑ Positive | Strong demand, lower affordability pressure |

| Northern Ireland | ↑ Positive | Supply constraints, local demand |

| North West | ↑ Positive | Lower entry prices, rental demand |

| London | ↓ -40% net balance | Affordability ceiling, geopolitical sensitivity |

| South East | ↓ -24% net balance | Stamp duty hangover, buyer caution |

| East Anglia | ↓ -26% net balance | Weak demand, supply overhang |

Sources: [1][3]

Lower entry prices and stronger rental demand in northern regions have created genuine resilience compared to southern markets where affordability constraints are most acute [3]. For investors and first-time buyers, this is increasingly where value lies. For surveyors, it means the nature of the advice — and the risks to flag — differs significantly by postcode.

Understanding how property market legislation changes affect different regional markets is also essential context for surveyors advising clients in 2026, as regulatory shifts can amplify or dampen regional divergences further.

What Regional Divergence Means for Survey Scope

A buyer purchasing in Manchester faces a fundamentally different risk profile than one buying in Surrey. In rising northern markets, buyers may be tempted to move quickly and skip thorough due diligence. In cautious southern markets, sellers may be reluctant to accept price reductions even when surveys reveal significant defects.

Both scenarios create professional obligations for building surveyors:

- In rising markets: Clearly communicate defect costs so buyers understand true acquisition costs beyond the purchase price.

- In declining markets: Provide robust evidence to support renegotiation conversations, protecting buyers from overpaying for properties with hidden issues.

Building Surveyor Strategies for the RICS January 2026 Landscape

Choosing the Right Survey Level for Market Conditions

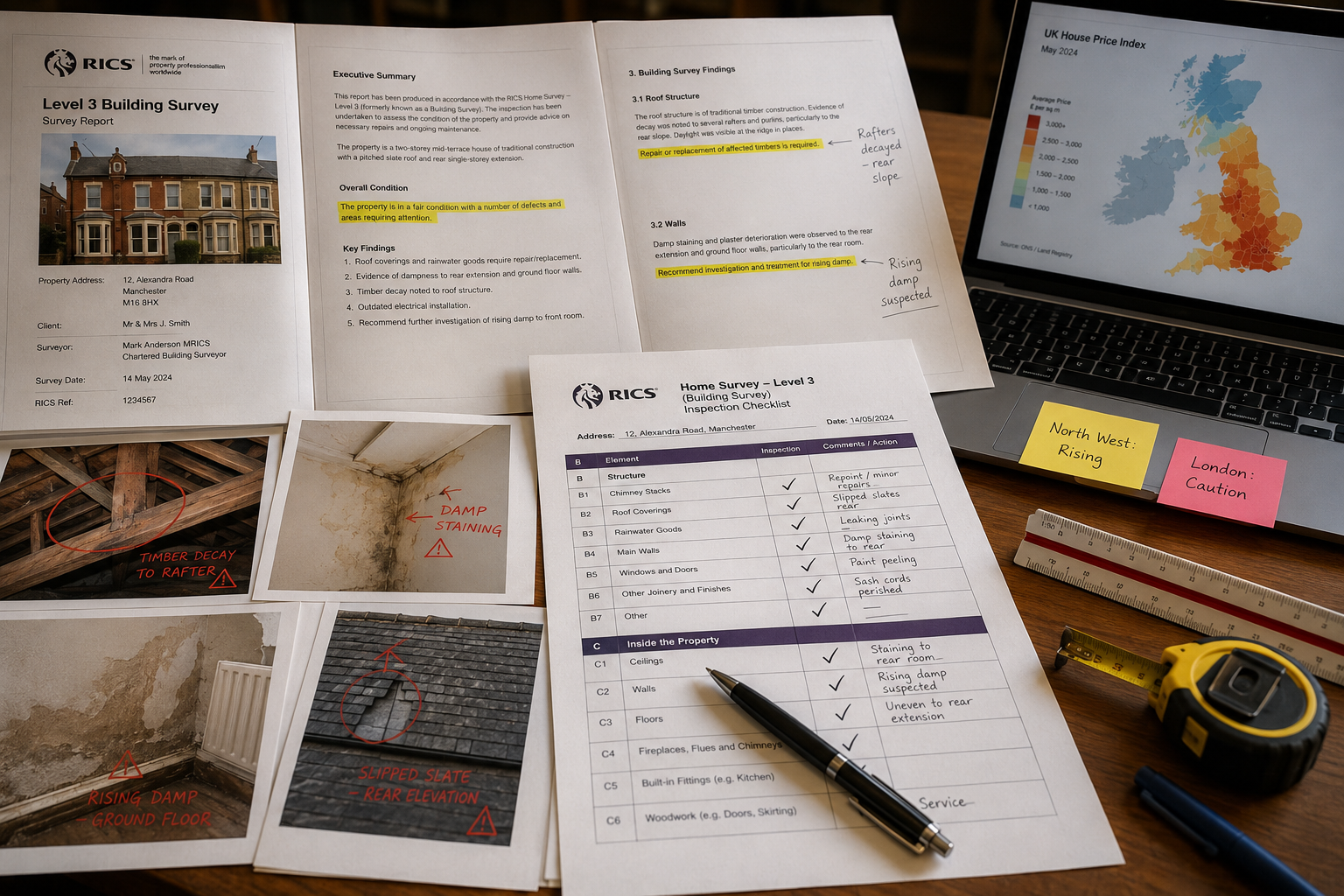

The single most impactful decision a buyer can make in the current market is choosing the right level of survey. In a market defined by regional uncertainty, a basic valuation is rarely sufficient. Understanding the difference between a full building survey and a homebuyer survey is the starting point for any informed buyer conversation.

For most properties in 2026 — particularly older stock in both rising northern markets and cautious southern ones — a Level 3 Full Building Survey offers the most comprehensive protection. This is especially true given that:

- Increased supply coming to market means more older, potentially unmaintained properties are entering the pipeline [3].

- Sellers under price pressure may have deferred maintenance.

- Buyers in competitive northern markets may be moving faster than due diligence warrants.

The complete guide to choosing the right property survey outlines the key decision factors, but in the context of the January 2026 RICS data, the case for comprehensive inspection has rarely been stronger.

A Practical Level 3 Survey Checklist for 2026 Market Conditions ✅

Building surveyors should ensure their Level 3 reports address the following in the current market environment:

Structural Integrity

- Foundation assessment, particularly in clay-rich soils (subsidence risk)

- Roof structure inspection — pitched roof common defects and flat roof issues

- Wall tie condition in cavity walls (common in 1930s–1980s stock)

- Evidence of movement, cracking, or settlement

Moisture and Dampness

- Rising damp assessment with moisture meter readings

- Penetrating damp identification at roof junctions, windows, and parapets

- Condensation risk assessment, particularly in poorly ventilated properties

- Damp and mould prevention indicators

Services and Compliance

- Electrical installation condition (EICR status)

- Boiler and heating system age and condition

- EPC rating and MEES compliance implications for landlord buyers

- Asbestos-containing materials (ACMs) in pre-2000 properties

Regional Risk Factors

- Flood risk assessment (critical in many northern regions)

- Mining or ground instability (relevant in parts of Yorkshire, Wales, North East)

- Japanese knotweed or invasive species

- Planning history and permitted development compliance

Cost Transparency

- Repair cost estimates or ranges for all significant defects

- Prioritisation of urgent or dangerous building issues requiring immediate attention

- Long-term maintenance schedule recommendations

Tailoring Reports to Boost Buyer Confidence

The +35% 12-month sales expectations figure from the RICS January 2026 data tells an important story: buyers want to transact, but they need confidence to do so [1]. A well-structured, clearly written Level 3 survey report is one of the most powerful tools available for converting cautious intent into completed transactions.

Key report-writing strategies for 2026:

- Use plain language: Avoid jargon. A buyer who understands the report is a buyer who can act on it.

- Prioritise clearly: Use traffic-light systems or numbered priority ratings so buyers instantly understand severity.

- Quantify where possible: Cost ranges for repairs remove ambiguity and support renegotiation conversations.

- Contextualise regionally: Note whether identified issues are typical for the property type and area — this prevents unnecessary alarm in markets where certain defects are standard.

Knowing what questions buyers should ask during a building survey helps surveyors prepare clients for the process and builds the trust that underpins confident decision-making.

Boosting Buyer Confidence: Long-Term Optimism Meets Short-Term Volatility

Interpreting the +35% Twelve-Month Signal

The RICS January 2026 Residential Survey: Building Surveyor Strategies for Regional Price Divergences and Buyer Confidence Boosts context would be incomplete without examining the confidence gap. Twelve-month sales expectations reached +35% net balance in January 2026 — the strongest reading since December 2024 [1]. Yet three-month expectations stood at just +4%, reflecting immediate caution about geopolitical and interest rate headwinds [1][3].

This gap between short-term hesitation and long-term optimism is a defining feature of the 2026 market. It creates a specific role for building surveyors: providing the certainty that allows buyers to bridge that gap and act now rather than waiting.

💬 "When buyers are confident about the long term but nervous about the short term, a thorough survey that removes uncertainty about the property itself can be the deciding factor in a transaction proceeding."

The Supply Pipeline: A Positive Signal Surveyors Should Acknowledge

Survey respondents highlighted the increasing supply of properties coming to market as an important positive signal for early 2026 activity [3]. More listings mean more choice for buyers — but also more due diligence work. Surveyors who can turn around high-quality reports efficiently will be well-positioned to support increased transaction volumes as the market recovers.

Understanding how long a building survey takes and communicating realistic timelines to clients helps manage expectations and keeps transactions on track during a period when pipeline management is increasingly important.

Strategies for Supporting Buyer Confidence in Regional Markets

For buyers in northern/rising markets:

- Emphasise the importance of thorough surveys even in competitive conditions

- Highlight that a survey protects against overpaying for defective stock even in a rising market

- Use budgeting for repairs and restoration analysis to give buyers a true total cost of ownership

For buyers in southern/cautious markets:

- Position the survey as a renegotiation tool — defect findings can support price reductions

- Provide detailed building defects survey documentation to support any post-survey negotiation

- Help buyers understand that in a buyer's market, thorough due diligence is a competitive advantage

For investor clients across all regions:

- Factor in EPC and MEES compliance costs as part of total investment analysis

- Assess rental yield potential alongside structural condition

- Consider transport links and local infrastructure as part of long-term value assessment, particularly in northern regions where infrastructure investment is supporting price growth

Conclusion: Turning Market Data Into Professional Action

The RICS January 2026 Residential Survey: Building Surveyor Strategies for Regional Price Divergences and Buyer Confidence Boosts analysis points to a clear professional mandate. The UK residential market in 2026 is not one market — it is many, each with its own risk profile, price trajectory, and buyer psychology. Building surveyors who understand this, and who tailor their approach accordingly, will deliver significantly more value to clients and support more successful transactions.

Actionable Next Steps for Building Surveyors in 2026 🎯

- Map your regional exposure: Understand which markets you serve and how the RICS January 2026 data applies to your specific geography.

- Upgrade your Level 3 reporting: Ensure reports include cost estimates, clear prioritisation, and regional context — not just defect lists.

- Educate clients early: Share the RICS market context with buyers before the survey so they understand why thorough due diligence matters in the current environment.

- Develop a northern market strategy: If you operate near rising regions, consider how your service offering supports buyers moving quickly in competitive conditions.

- Stay current on legislation: EPC requirements, planning changes, and building safety regulations continue to evolve — integrate compliance checks into every survey.

- Communicate turnaround times clearly: As supply increases and transaction volumes recover, efficient, high-quality survey delivery will be a key differentiator.

The market is recovering — unevenly, cautiously, but genuinely. Building surveyors who position themselves as trusted guides through regional complexity and short-term uncertainty will be indispensable partners in the transactions that define 2026's property landscape.

References

[1] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] RICS Hails Early Signs of Housing Market Improvement in Latest Survey – https://www.housingtoday.co.uk/news/rics-hails-early-signs-of-housing-market-improvement-in-latest-survey/5140683.article

[3] Latest RICS Survey Reveals Global Headwinds Are Weighing on Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/

[4] Valuation Strategies Amid January 2026 RICS Residential Survey: Spotting Early Market Recovery Signals – https://nottinghillsurveyors.com/blog/valuation-strategies-amid-january-2026-rics-residential-survey-spotting-early-market-recovery-signals

[5] UK Residential Market Survey – https://www.rics.org/news-insights/market-surveys/uk-residential-market-survey