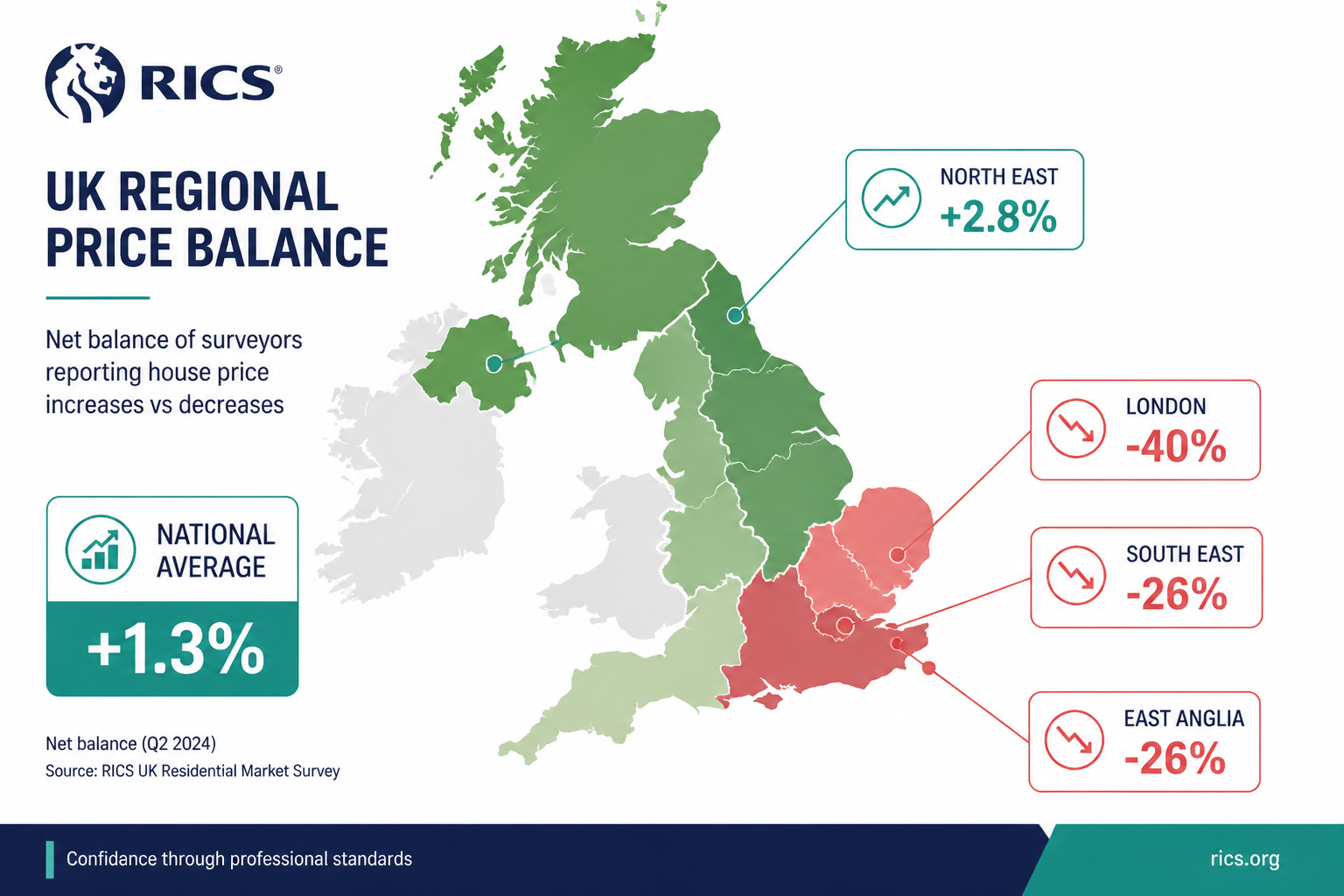

The North East of England recorded annual house price growth of 2.8% in Q1 2026 — more than double the UK national average of 1.3% — while London simultaneously posted a staggering price balance of -40%, its weakest reading among all UK regions [1][5]. That single data point captures the sharpest regional divergence the UK residential property market has seen in years.

The RICS Residential Survey Q1 2026: Valuation Strategies for Northern England Price Surge vs Southern Caution sits at the heart of a critical debate for surveyors, buyers, sellers, and investors: how do professionals accurately value property when the same national market is simultaneously booming in Bradford and stalling in Bromley? This article breaks down the Q1 2026 RICS data, explains what is driving the divergence, and outlines practical valuation strategies that professionals are using to navigate this split-market reality.

Key Takeaways 📌

- Northern England, Scotland, and Northern Ireland are the standout growth regions of Q1 2026, with the North East outperforming the national average at +2.8% annual growth.

- London (-40%), South East (-24%), and East Anglia (-26%) recorded the weakest price balances in February 2026, signalling sustained southern caution.

- Sales activity optimism is rising nationally (+35% net balance), creating a complex picture where transaction volumes and prices are not always moving in the same direction.

- Surveyors must adapt valuation methodologies to account for hyper-local comparable evidence, particularly in rapidly appreciating northern markets.

- Proactive due diligence — including professional building surveys and accurate professional valuations — is more important than ever in a divergent market.

Understanding the Q1 2026 RICS Data: A Tale of Two Markets

The RICS UK Residential Market Survey is one of the most closely watched indicators in the British property sector. Its monthly net balance figures — where a positive score means more surveyors report rising prices than falling — paint a granular picture of regional performance.

The National Picture: Tentative Stabilisation

The national house price net balance improved from -19% in October 2025 to -10% in January 2026, suggesting tentative stabilisation after a difficult period [1]. By February and March 2026, however, the national figure masked enormous regional variation that demands a more nuanced reading [8].

💬 "The headline number is almost meaningless without the regional breakdown. A -10% national balance could mean +20% in the North and -40% in London — and that is precisely what we are seeing."

Sales expectations, meanwhile, tell a more optimistic story. A net balance of +35% of surveyors reported rising sales optimism in Q1 2026, suggesting that transaction volumes may recover even as price growth remains geographically uneven [2].

Northern England: The Standout Performer 🟢

The RICS Residential Survey Q1 2026 data firmly establishes Northern England as the market's standout performer. Key regional data points include:

| Region | Price Balance / Growth | Trend |

|---|---|---|

| North East England | +2.8% annual growth | ⬆️ Strong upward |

| North West England | Positive balance | ⬆️ Upward |

| Scotland | +3–5% forecast 2026 | ⬆️ Strong upward |

| Northern Ireland | +3–5% forecast 2026 | ⬆️ Strong upward |

| National Average | +1.3% annual growth | ➡️ Flat/modest |

Sources: [5][7][8]

The North West sustained a positive trajectory in contrast to the wider national picture, positioning itself as a secondary growth area after Scotland and Northern Ireland [8]. Cities like Manchester, Leeds, Liverpool, and Newcastle are driving this momentum, underpinned by strong employment growth, infrastructure investment, and relative affordability compared to the South.

Southern England: Persistent Caution 🔴

The contrast with southern markets could scarcely be more stark:

- London: -40% price balance in February 2026 — the weakest of all regions [4]

- South East: -24% balance, indicating substantial downward pressure [4]

- East Anglia: -26% balance, reflecting weak buyer demand [4]

- South West: Continued underperformance relative to national averages, driven by affordability pressures [1]

For surveyors operating in areas like South East London or South West London, these figures demand a fundamentally different approach to comparable evidence selection and valuation adjustment.

RICS Residential Survey Q1 2026: Valuation Strategies for Northern England Price Surge vs Southern Caution

The divergence revealed by the RICS Residential Survey Q1 2026 is not merely an academic observation — it has direct, practical implications for how surveyors approach valuations. A one-size-fits-all methodology is no longer adequate.

Strategy 1: Hyper-Local Comparable Selection in Rising Northern Markets

In rapidly appreciating markets like the North East and North West, the age of comparable evidence matters enormously. Using sales data from six or twelve months ago can systematically undervalue a property in a market that has moved significantly upward.

Best practice for northern market valuations:

- ✅ Prioritise comparables from the most recent 3 months wherever possible

- ✅ Apply time adjustments to older comparables based on verified local price indices

- ✅ Cross-reference RICS data with Land Registry price paid data and local estate agent intelligence

- ✅ Document the rationale for any adjustments clearly within the valuation report

- ✅ Engage with local market participants to understand micro-level demand drivers

Understanding what surveyors look at during a property valuation is essential context for buyers and sellers navigating these fast-moving markets.

Strategy 2: Conservative Adjustments in Declining Southern Markets

The inverse challenge applies in London and the South East. Here, the risk is overvaluation — relying on historic sale prices that no longer reflect current market conditions. With London's price balance at -40%, surveyors must apply downward adjustments with evidence-based rigour.

Best practice for southern market valuations:

- ✅ Scrutinise whether comparable sales reflect current market sentiment or a prior peak

- ✅ Consider marketing time and price reduction history as valuation inputs

- ✅ Account for increased buyer negotiating power in a buyer's market

- ✅ Flag uncertainty ranges clearly in reports where market evidence is thin or conflicting

For clients in areas such as Camden, Islington, or Central London, professional valuations must reflect the current subdued reality rather than historical peaks.

Strategy 3: Real-Time Data Integration

The most resilient valuation approaches in 2026 integrate multiple real-time data streams rather than relying solely on historical Land Registry records. Surveyors are increasingly using:

- Rightmove and Zoopla asking price indices (with appropriate discounting for achieved vs. asking)

- RICS monthly survey data as a directional indicator

- Bank of England mortgage approval data as a leading demand indicator

- Local authority planning data to identify supply pipeline pressures

- ONS regional employment and wage data to assess affordability trajectory

This multi-source approach is particularly valuable in markets like the North East, where the pace of change can outstrip the Land Registry's publication lag of several months [7].

Strategy 4: Condition-Adjusted Valuations in a Competitive Northern Market

In a rising market, buyers competing for limited stock may overlook structural or maintenance issues that would ordinarily suppress a price. This creates a specific risk: properties with significant defects being valued at or near market rate for sound stock.

A thorough Level 3 Full Building Survey becomes particularly valuable in this context — giving buyers an accurate picture of condition that can inform both negotiation and valuation adjustment. Surveyors should ensure that condition-related deductions are applied consistently, even when competitive market pressure might otherwise obscure them.

What Is Driving the North-South Divide in 2026?

Understanding the underlying drivers of regional divergence is essential for making informed valuation and investment decisions.

Factors Fuelling Northern Growth

1. Relative Affordability

Northern England's average house prices remain significantly lower than southern equivalents, making them accessible to a wider pool of buyers — including first-time buyers and those relocating from more expensive regions.

2. Employment and Infrastructure Investment

Major investment in transport infrastructure, digital connectivity, and public sector employment across northern cities has supported population growth and housing demand.

3. Remote Working Normalisation

The continued normalisation of hybrid and remote working has freed buyers from the requirement to live within commuting distance of London, redistributing demand northward.

4. Investor Activity

Buy-to-let and property development investors have increasingly focused on northern markets, attracted by higher rental yields and stronger capital growth prospects. Those considering property development valuations should factor these dynamics into feasibility assessments.

Factors Suppressing Southern Markets

1. Affordability Ceiling

London and the South East have reached an affordability ceiling for many buyer segments. Even with mortgage rates easing from their 2023–2024 peaks, monthly repayments on average London properties remain prohibitive for large portions of the population.

2. Stamp Duty Sensitivity

Higher-value properties in southern markets are disproportionately affected by stamp duty costs, reducing transaction volumes and suppressing price growth. Understanding stamp duty implications is increasingly important for southern market participants.

3. Reduced International Demand

London's prime and super-prime markets have faced headwinds from reduced international buyer activity, geopolitical uncertainty, and changes to non-domicile tax rules.

4. Oversupply in Certain Segments

New-build completions in some London boroughs have added supply at a time of weakening demand, creating localised price pressure.

RICS Residential Survey Q1 2026: Practical Implications for Buyers, Sellers, and Investors

The insights from the RICS Residential Survey Q1 2026: Valuation Strategies for Northern England Price Surge vs Southern Caution are not just for professionals — they carry direct implications for anyone active in the property market in 2026.

For Buyers 🏠

In Northern England:

- Act with appropriate urgency — rising markets reward decisiveness

- Commission a thorough building survey before committing; competitive conditions can mask defects

- Ensure your valuation is based on the most recent comparable evidence, not outdated data

In London and the South:

- Negotiate confidently — market conditions favour buyers

- Avoid overpaying relative to current market evidence; lender valuations may come in below agreed prices

- Consider the medium-term outlook carefully before committing to high-value purchases

For Sellers 🏷️

In Northern England:

- Price realistically but confidently — the market supports well-priced stock

- Invest in presentation; competition among buyers does not mean condition is irrelevant

- Obtain a professional valuation to avoid underpricing in a rising market

In London and the South:

- Price to the current market, not to historical peak values

- Be prepared for extended marketing periods and negotiation

- Consider whether timing the sale for later in 2026 — if recovery signals strengthen — is feasible

For Investors and Developers 💼

The Q1 2026 data reinforces the case for northern market investment. Scotland and Northern Ireland are forecast to deliver 3–5% price appreciation across 2026 [7], while the North East and North West continue to outperform national averages.

For those exploring inheritance tax valuations or annual tax on enveloped dwellings, the regional divergence also has direct implications for asset values that must be accurately captured in professional appraisals.

The Rental Market: A Complicating Factor

The rental market adds another layer of complexity to the 2026 picture. RICS data indicates that rental supply continues to fall, with landlord instructions declining and tenant demand remaining elevated [6]. This dynamic:

- Supports higher rental yields in northern markets, reinforcing investor demand

- Creates affordability pressure for renters, potentially converting some to buyers and sustaining purchase demand

- Adds urgency to the need for accurate professional property valuations that reflect both sales and rental market conditions

Key Risks and Uncertainties to Monitor

Even the most bullish northern market data comes with caveats. Surveyors and market participants should monitor:

- Interest rate trajectory: Further Bank of England rate decisions will significantly influence mortgage affordability across all regions

- Labour market conditions: Employment stability underpins housing demand, particularly in northern markets where the public sector plays a larger role

- Policy changes: Stamp duty thresholds, planning reform, and rental regulation changes could shift market dynamics rapidly

- Mortgage availability: Lender appetite and product availability remain key constraints on transaction volumes

- Geopolitical and economic shocks: External events can rapidly alter sentiment in ways that regional data cannot anticipate

Conclusion: Navigating a Divided Market with Precision

The RICS Residential Survey Q1 2026 data presents a clear mandate for surveyors, buyers, and investors: regional context is everything. The days of applying a single national narrative to UK residential property are firmly over.

Northern England's price surge — anchored by the North East's 2.8% annual growth and the North West's sustained positive trajectory — demands valuation strategies that prioritise recency, hyper-local evidence, and careful condition adjustment. Meanwhile, London's -40% price balance and the South East's -26% reading require an equally disciplined but inverse approach: conservative, evidence-led, and alert to the risk of overvaluation.

Actionable Next Steps ✅

- Commission a professional valuation that explicitly accounts for current regional market conditions, not just historical comparables — explore chartered surveyor valuation services for expert guidance.

- Obtain a Level 3 Building Survey before purchasing in any market, but especially in competitive northern markets where defects may be overlooked — see the full building survey service.

- Review RICS monthly survey data as part of ongoing market monitoring — do not rely solely on annual or quarterly snapshots.

- Engage a RICS-qualified surveyor with demonstrable local market knowledge in the specific region of interest.

- Factor in tax implications — whether stamp duty, inheritance tax, or annual tax on enveloped dwellings — using accurate, current valuations.

The property market of 2026 rewards those who understand its geography. The data is clear: know your region, trust the evidence, and value with precision.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Rics Residential Market Survey Q1 2026 Building Survey Implications For Northern England Price Surges – https://nottinghillsurveyors.com/blog/rics-residential-market-survey-q1-2026-building-survey-implications-for-northern-england-price-surges

[3] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[4] Rics House Price Balance – https://tradingeconomics.com/united-kingdom/rics-house-price-balance

[5] Uk Residential Market Survey March 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey-March-2026.pdf

[6] Rics Warns Rental Supply Is Still Falling – https://www.property118.com/rics-warns-rental-supply-is-still-falling/

[7] Northern England Valuation Surge 2026 Rics Insights On Price Growth And Surveyor Adjustment Techniques – https://nottinghillsurveyors.com/blog/northern-england-valuation-surge-2026-rics-insights-on-price-growth-and-surveyor-adjustment-techniques

[8] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[9] Market View January 2026 – https://www.watsons-property.co.uk/market-view-january-2026/