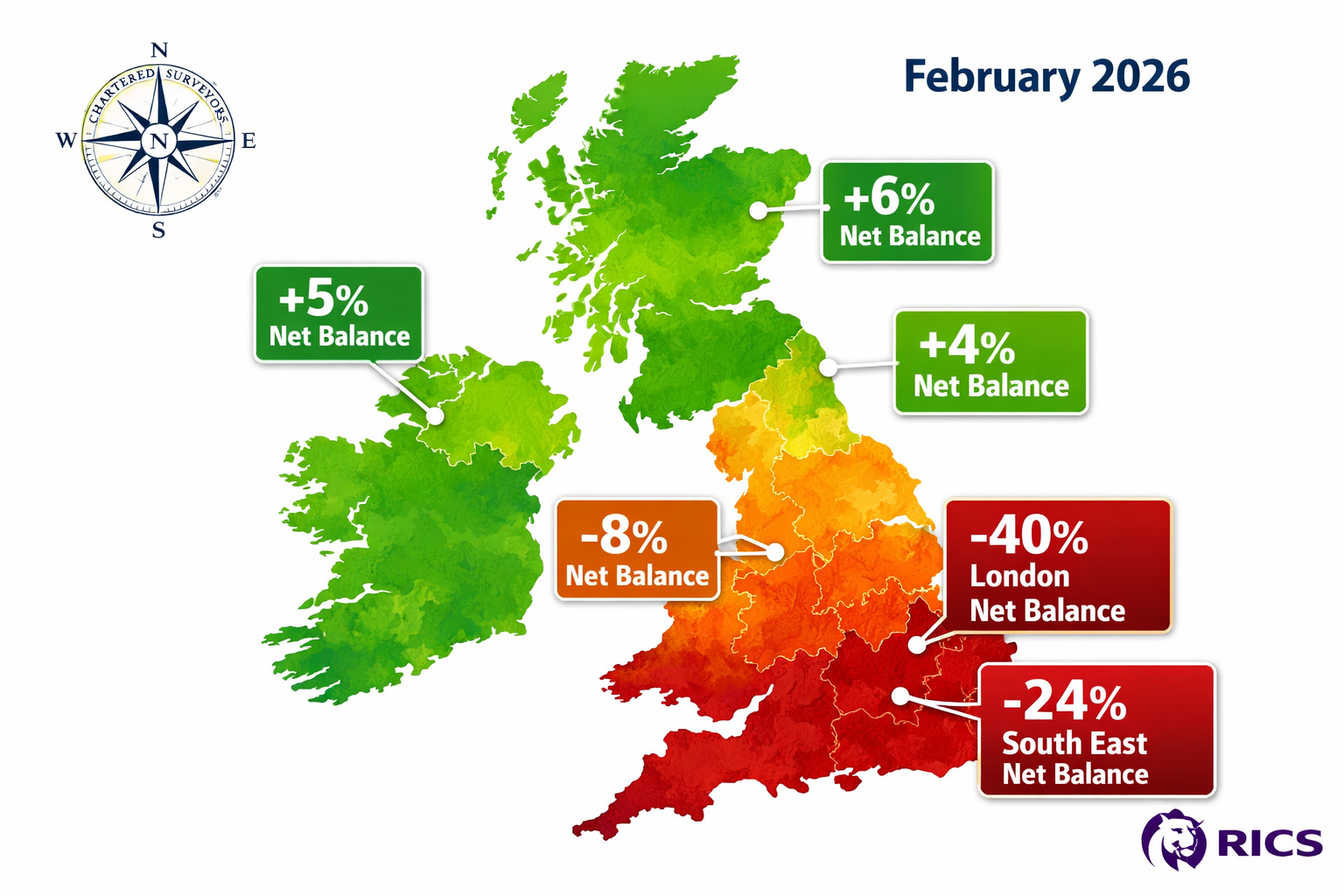

London's residential price net balance crashed to -40% in February 2026 — while Northern Ireland, Scotland, and the North West of England held firmly in positive territory. That single data point, drawn from the RICS UK Residential Market Survey, encapsulates one of the most pronounced regional splits in recent UK property history [2]. For chartered surveyors operating across this fractured landscape, applying a uniform national valuation framework is no longer adequate. The Regional Valuation Techniques for North-South Price Divergence: RICS February 2026 Insights for Chartered Surveyors explored in this article provide a structured response to that challenge.

Key Takeaways 📌

- London's price net balance hit -40% in February 2026, the steepest nationally, while northern regions remained positive — demanding region-specific valuation adjustments.

- Buyer demand fell sharply to a net balance of -26% in February, driven by persistent mortgage rate concerns and geopolitical volatility.

- Short-term sentiment turned cautious (-18%), but a 12-month outlook of +33% signals medium-term resilience surveyors must factor into long-horizon valuations.

- Comparable selection, weighting, and adjustment methodologies must be recalibrated for each regional market condition, not applied nationally.

- Stable micro-markets such as Portsmouth, Southampton, Bath, and Bristol offer important nuance within the broader Southern decline narrative.

Understanding the February 2026 RICS Data: A Tale of Two Markets

The headline national house price net balance registered -12% in February 2026, only marginally weaker than January's reading [2]. On the surface, that figure appears manageable. Look beneath it, and the story is far more complex.

The Southern Pressure Zone

The South East recorded a net balance of -24%, and East Anglia came in at -26% [2]. Combined with London's -40% reading, a clear Southern pressure zone emerges. These figures reflect sustained downward momentum rather than a temporary correction.

| Region | February 2026 Net Balance | Trend Direction |

|---|---|---|

| London | -40% | ⬇️ Strongly negative |

| East Anglia | -26% | ⬇️ Negative |

| South East | -24% | ⬇️ Negative |

| National Average | -12% | ⬇️ Mildly negative |

| North West England | Positive | ⬆️ Resilient |

| Scotland | Positive | ⬆️ Resilient |

| Northern Ireland | Positive | ⬆️ Resilient |

The Northern Resilience Story

Northern Ireland, Scotland, and the North West of England continue to report positive price momentum [2]. This is not a new phenomenon — northern markets have shown relative outperformance for several quarters — but the February 2026 data confirms the divergence is deepening rather than narrowing.

💬 "Deteriorating geopolitical conditions and rising oil and energy prices have increased the likelihood that mortgage rates will remain elevated, weighing on confidence." — Tarrant Parsons, RICS Head of Market Research [2]

This macro backdrop is not affecting all regions equally. Southern markets, with higher average price points and greater sensitivity to mortgage rate movements, absorb interest rate pressure more acutely than lower-priced northern markets where affordability ratios remain healthier.

Demand and Supply Dynamics

Buyer demand deteriorated sharply. New buyer enquiries fell to a net balance of -26% in February, down from -15% in January [2]. This acceleration in demand weakness is a critical input for near-term valuation adjustments.

On the supply side, new instructions held at a broadly neutral +2% [4], suggesting the market is not being flooded with distressed listings. This supply stability is an important moderating factor — particularly in micro-markets like Portsmouth and Southampton, where steady demand and limited supply are still supporting values [4].

Agreed sales posted a net balance of -12%, reflecting dampened transaction activity linked to macroeconomic uncertainty [2]. Lower transaction volumes reduce the pool of reliable comparable evidence, which directly complicates the valuation process.

Core Regional Valuation Techniques for North-South Price Divergence: RICS February 2026 Insights for Chartered Surveyors

Applying robust regional valuation techniques in a divergent market requires more than awareness of headline data. It demands systematic adjustments to methodology at every stage of the valuation process.

1. 🗂️ Comparable Selection: Tightening the Geographic Radius

In a homogeneous market, comparables drawn from a wider geographic area can be acceptable. In a divergent market, geographic precision becomes non-negotiable.

For London and South East instructions, surveyors should:

- Restrict comparables to the immediate postcode sector where possible, given that price trends can vary significantly even within a single borough.

- Prioritise transactions from the most recent 60–90 days, given the speed at which sentiment has shifted (the buyer enquiry net balance moved from -15% to -26% in a single month) [2].

- Exclude comparables from adjacent sub-markets with materially different demand profiles — for example, avoiding using inner London sales to support outer London valuations when the two are moving at different velocities.

For northern region instructions, the comparable pool may be broader, but surveyors must still be alert to local micro-market conditions that differ from the regional positive trend.

2. 📊 Time Adjustments: Reflecting Rapid Sentiment Shifts

The February 2026 data highlights how quickly market sentiment can move. Short-term price expectations fell from -6% to -18% in a single month [2]. This velocity of change means that a comparable from six months ago may require a meaningful time adjustment, particularly in Southern markets.

Practical approach:

- Apply negative time adjustments to older comparables in London and South East markets, reflecting the documented downward price trend.

- Use the RICS monthly net balance data as a directional guide to calibrate the magnitude of adjustments.

- In northern markets, time adjustments may be neutral or marginally positive, but should not be assumed without checking local transaction evidence.

For guidance on how survey findings interact with negotiated prices, the Prince Surveyors guide to negotiating house prices after a survey provides useful practical context for surveyors advising clients.

3. ⚖️ Weighting Comparables by Market Conditions Evidence

Not all comparables carry equal evidential weight in a volatile market. Surveyors should apply a tiered weighting approach:

- Tier 1 (highest weight): Arm's-length transactions within the same postcode sector, completed within the last 60 days, with no unusual conditions.

- Tier 2 (moderate weight): Transactions from adjacent sectors or 60–120 days old, requiring documented adjustments.

- Tier 3 (lower weight): Older transactions or those from materially different sub-markets, used only to support the range rather than anchor the opinion of value.

This approach is consistent with RICS Red Book Global Standards and ensures the valuation opinion is defensible in the context of documented market volatility [3].

4. 🔍 Geopolitical Risk Weighting in Southern Markets

RICS data explicitly links the February 2026 demand deterioration to geopolitical conditions and energy price pressures [2]. For chartered surveyors, this introduces a qualitative risk layer that must be acknowledged within the valuation report, even if it cannot be precisely quantified.

Recommended practice:

- Include a market conditions caveat in valuation reports for London and South East properties, noting the documented deterioration in buyer demand and the sensitivity of the market to further interest rate movements.

- For commercial valuations, the geopolitical risk overlay is even more significant, as investor confidence in commercial assets is closely tied to macroeconomic stability.

- For leasehold extension and enfranchisement valuations, the depressed transaction market in London requires careful selection of deferment and capitalisation rates that reflect current, not historic, market conditions.

5. 📐 Adjusting for Sub-Market Stability Within the Broader Decline

The February 2026 RICS data is not uniformly negative across all Southern markets. Portsmouth and Southampton show steady demand with limited supply supporting values, and improving mortgage rate confidence [4]. Bath and Bristol demonstrated resilient buyer appetite despite the broader political and economic uncertainty, though price growth remained absent [4].

This nuance is critical. A surveyor instructed on a Bath property should not apply the same downward adjustment assumptions as one instructed in central London. The regional and sub-regional data must be interrogated separately.

For surveyors operating across the South West, understanding these micro-market distinctions is essential — and chartered surveyors in Berkshire and chartered surveyors in Oxfordshire will recognise that their local markets sit in a transitional zone between the London-influenced South East pressure and the more resilient Western markets.

Practical Methodology Adjustments for Divergent Market Conditions

Applying the RICS February 2026 Insights for Chartered Surveyors to Specific Valuation Types

Residential mortgage valuations face the most immediate pressure from the demand decline. With buyer enquiries at -26% nationally and transaction volumes suppressed [2], the risk of overvaluation is heightened in declining markets. Surveyors must ensure that the opinion of Market Value reflects current, not aspirational, pricing.

For inheritance tax valuations, the date of death is fixed, but where estates are being administered during a period of rapid market movement, retrospective valuations must be carefully anchored to the conditions prevailing at the relevant date — not the current market.

Insurance reinstatement cost valuations are less directly affected by price divergence, as rebuild costs are driven by construction inflation rather than market sentiment. However, insurance reinstatement cost valuations should still account for regional variations in labour and material costs, which can diverge significantly between London and northern markets.

The 12-Month Outlook: Balancing Caution with Medium-Term Resilience

Despite near-term caution, +33% of RICS respondents expect prices to rise over the next 12 months [2]. This medium-term resilience signal is important for valuations with a forward-looking component — such as development appraisals, loan security valuations for longer-term lending, and portfolio assessments.

Surveyors should be careful not to allow short-term sentiment (-18% near-term expectations) to unduly suppress valuations where the instruction requires a longer-horizon perspective. The appropriate balance between current market evidence and medium-term outlook should be explicitly addressed in the valuation report.

💡 Key insight: The gap between near-term (-18%) and 12-month (+33%) expectations is unusually wide. This signals a market in transition, not structural collapse — an important distinction for valuation professionals.

Regional Valuation Techniques for North-South Price Divergence: RICS February 2026 Insights — Implications for Surveying Practice

Building a Defensible Valuation in a Divergent Market

The February 2026 data reinforces a principle that experienced surveyors already know: national averages are a starting point, not a conclusion. The gap between London's -40% and Northern Ireland's positive reading is too wide for any single national methodology to bridge adequately [2].

A defensible valuation in 2026 requires:

- ✅ Explicit regional market commentary — citing RICS survey data and local transaction evidence.

- ✅ Documented comparable selection rationale — explaining why certain transactions were included or excluded.

- ✅ Time adjustment transparency — showing the basis and magnitude of any temporal adjustments.

- ✅ Market conditions caveats — acknowledging the documented uncertainty and its potential impact on value.

- ✅ Separate treatment of sub-markets — not conflating Bath with London, or Manchester with Edinburgh.

For a broader understanding of how property valuations are structured and delivered, the Prince Chartered Surveyors valuations service provides a comprehensive overview of the range of valuation types available to clients and professionals.

What Happens When a Valuation Falls Short of the Agreed Price?

In a declining Southern market, the risk of a valuation below the agreed purchase price increases significantly. This scenario — sometimes called a "down valuation" — is becoming more common in London and the South East as asking prices lag the deteriorating sentiment captured in the RICS data. Understanding what to do if a home valuation is less than an offer is increasingly relevant for both surveyors advising clients and buyers navigating the current market.

CPD and Professional Standards Implications

The February 2026 RICS data, combined with the broader geopolitical context, represents a strong case for targeted CPD focused on:

- Valuation in declining markets

- Comparable analysis under low transaction volume conditions

- Communicating uncertainty and market risk within RICS Red Book-compliant reports

The RICS CEO's February 2026 update emphasised the profession's role in maintaining market confidence through rigorous, evidence-based practice [5]. That standard is most tested precisely when markets diverge as sharply as they have in early 2026.

Conclusion: Actionable Next Steps for Chartered Surveyors

The Regional Valuation Techniques for North-South Price Divergence: RICS February 2026 Insights for Chartered Surveyors covered in this article point to a clear professional imperative: the UK residential market is not one market, and it must not be valued as one.

Actionable steps for chartered surveyors in 2026:

- 🔎 Audit your comparable selection process — ensure geographic and temporal parameters reflect current regional conditions, not historical norms.

- 📋 Update your standard valuation report templates to include explicit market conditions commentary referencing current RICS data.

- 🧮 Apply documented time adjustments to any comparable older than 60 days in London and South East instructions.

- 🌍 Incorporate geopolitical risk language in Southern market reports, acknowledging the RICS-documented link between macroeconomic volatility and demand deterioration.

- 📈 Balance near-term caution with medium-term resilience — the +33% 12-month outlook must inform forward-looking valuation components.

- 🗺️ Treat sub-markets individually — Portsmouth, Bath, and Bristol require different assumptions than central London, even within the same broad Southern region.

- 📚 Engage with RICS CPD resources on valuation in uncertain markets to ensure methodology remains current and defensible.

The surveyors who navigate this divergence most effectively will be those who treat regional data not as background context, but as a core input into every valuation decision they make.

References

[1] Valuation Impacts Of February 2026 Rics Survey Strategies For Regional Price Divergence In Uk Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets

[2] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[3] Valuation Challenges In Uncertain Markets Using Rics February 2026 Data To Adjust Valuations Amid Geopolitical Volatility And Interest Rate Concerns – https://nottinghillsurveyors.com/blog/valuation-challenges-in-uncertain-markets-using-rics-february-2026-data-to-adjust-valuations-amid-geopolitical-volatility-and-interest-rate-concerns

[4] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[5] Update From Justin Young Rics Ceo February 2026 – https://www.rics.org/news-insights/update-from-justin-young-rics-ceo-february-2026