43,937 new homes built across England between 2022 and 2024 sit in areas of medium or high flood risk — and that figure does not yet account for the extraordinary ground saturation left behind by the wettest winter in nearly two centuries [5]. For anyone buying, selling, or surveying a coastal UK property in 2026, understanding Flood Risk Valuation Adjustments After Spring 2026 Events: Building Survey Protocols for Coastal UK Properties is no longer optional — it is a professional and financial necessity.

Key Takeaways 📋

- Spring 2026 flooding conditions have materially changed the risk profile of coastal and low-lying UK properties, requiring updated survey protocols.

- Valuation adjustments of 5–25%+ are now realistic for properties in Flood Zones 2 and 3 without resilience measures in place.

- FCERM Guidance 2026 restructures public funding for coastal defences, directly affecting how surveyors assess long-term protection reliability.

- Level 3 Building Surveys are the minimum recommended standard for any coastal property purchase in the current risk environment.

- Flood Re insurance ends in 2039 — buyers purchasing today need to understand the long-term insurance cost trajectory built into any valuation.

Why Spring 2026 Has Changed Everything for Coastal Surveyors

The spring of 2026 arrived on the back of saturated ground across English regions following the wettest winter in close to two centuries. When soil is already at capacity, additional rainfall does not absorb — it runs directly off surfaces, overwhelming drainage systems and raising flood risk in low-lying areas, basements, gardens, and sloped sites [4]. For coastal UK properties, this compounding effect has pushed flood risk from a background consideration to an immediate valuation factor.

Research published by the University of Portsmouth demonstrates that flood predictions significantly affect real estate demand, with coastal areas including Chichester and Portsmouth showing measurable property devaluation when flood risk data is presented to prospective buyers [3]. Crucially, buyers show a clear preference for safer locations even when flood predictions contain uncertainties — meaning perceived risk can depress values almost as effectively as actual flood events.

💬 "Flood risk is no longer a footnote in a survey report. In 2026, it is a headline finding that shapes mortgage decisions, insurance premiums, and sale prices."

Properties within 400 metres of named water bodies — rivers, streams, or flood channels — carry elevated spring risk. Victorian and Edwardian properties with original drainage connections are significantly more vulnerable than modern-build infrastructure [4]. Surveyors operating in coastal zones must now treat these proximity and age factors as primary, not secondary, risk indicators.

Understanding the 2026 FCERM Guidance and Its Valuation Implications

The new Flood and Coastal Erosion Risk Management (FCERM) Guidance 2026 has restructured how public funding flows to coastal defence projects, and this has direct implications for property valuations [1].

The Three-Category Funding Framework

Under the revised guidance, flood risk projects fall into three distinct categories:

| Project Type | Funding Structure |

|---|---|

| Refurbishment of existing assets | 100% funded |

| Replacement schemes (up to £3m) | 100% funded |

| New/improved schemes (above £3m) | 90% funded |

This structure actively incentivises repair over replacement for ageing coastal defences [1]. For surveyors, this matters because a property protected by an older sea wall or flood barrier that is approaching end-of-life may now receive refurbishment funding rather than full replacement — meaning the quality and longevity of that protection is a legitimate valuation variable.

Optimism Bias and Benefit Area Mapping

The 2026 guidance introduces two further mechanisms that surveyors and valuers must understand:

- Optimism bias percentages — standardised uplifts applied to initial cost estimates to account for underestimation in early project phases, with higher percentages applied to engineered schemes compared to natural flood management approaches [1].

- Mandatory benefit area definition — precise geographic mapping and property counts based on national flood risk datasets must be completed before any funding submission [1].

This second point is particularly significant. It means that whether a specific coastal property falls within or outside a formally mapped benefit area will now influence whether local authorities prioritise defending it. Surveyors should check Environment Agency datasets and local authority flood risk management plans as part of every coastal property assessment.

Understanding statutory considerations in building surveys is essential here — planning and flood risk designations interact directly with how a property can be used, extended, and insured.

Flood Risk Valuation Adjustments After Spring 2026 Events: Building Survey Protocols for Coastal UK Properties — The Surveyor's Checklist

Conducting a resilience assessment for a coastal property in 2026 requires a structured, evidence-based approach. The following protocol reflects current best practice aligned with the spring 2026 risk environment.

🔍 Stage 1: Pre-Inspection Data Gathering

Before visiting the property, surveyors should compile:

- Environment Agency Flood Map for Planning zone classification (Zone 1, 2, or 3)

- Surface water flood risk mapping — distinct from river/coastal flood risk and increasingly relevant given 2026 ground saturation conditions [4]

- Local authority SFRA (Strategic Flood Risk Assessment) data

- Historic flood event records — including any spring 2026 incidents

- Flood Re eligibility status — noting that this scheme is scheduled to end in 2039 [6]

- FCERM benefit area maps to establish whether the property falls within a funded defence zone [1]

For a comprehensive understanding of how environmental factors feed into survey findings, the environmental issues section of a Level 3 Full Building Survey provides the relevant framework.

🏗️ Stage 2: On-Site Structural and Resilience Assessment

On-site inspection for coastal flood risk should include:

External checks:

- Tide marks, staining, or salt efflorescence on lower external walls

- Condition of air bricks, vents, and subfloor ventilation (flood-vulnerable entry points)

- Drainage gradient and surface water routing away from the building

- Condition of boundary walls, gates, and any existing flood barriers

- Evidence of previous flood resilience works (raised thresholds, flood doors, tanking)

- Proximity and condition of any sea walls, flood banks, or tidal barriers

Internal checks:

- Damp or moisture readings at ground floor and basement level — use calibrated moisture meters

- Condition of ground floor finishes for evidence of past inundation

- Electrical installation height (consumer units, sockets below 75cm are high-risk)

- Boiler and utility positioning relative to potential flood levels

- Evidence of previous flood damage to structural timbers, plasterwork, or insulation

Moisture in buildings is a complex issue that extends well beyond visible damp patches — understanding what causes moisture in buildings helps surveyors distinguish flood-related damage from other sources.

For older coastal properties, a construction and condition survey provides the detailed structural baseline needed to assess how a building has responded to historic flood events and how it is likely to perform in future ones.

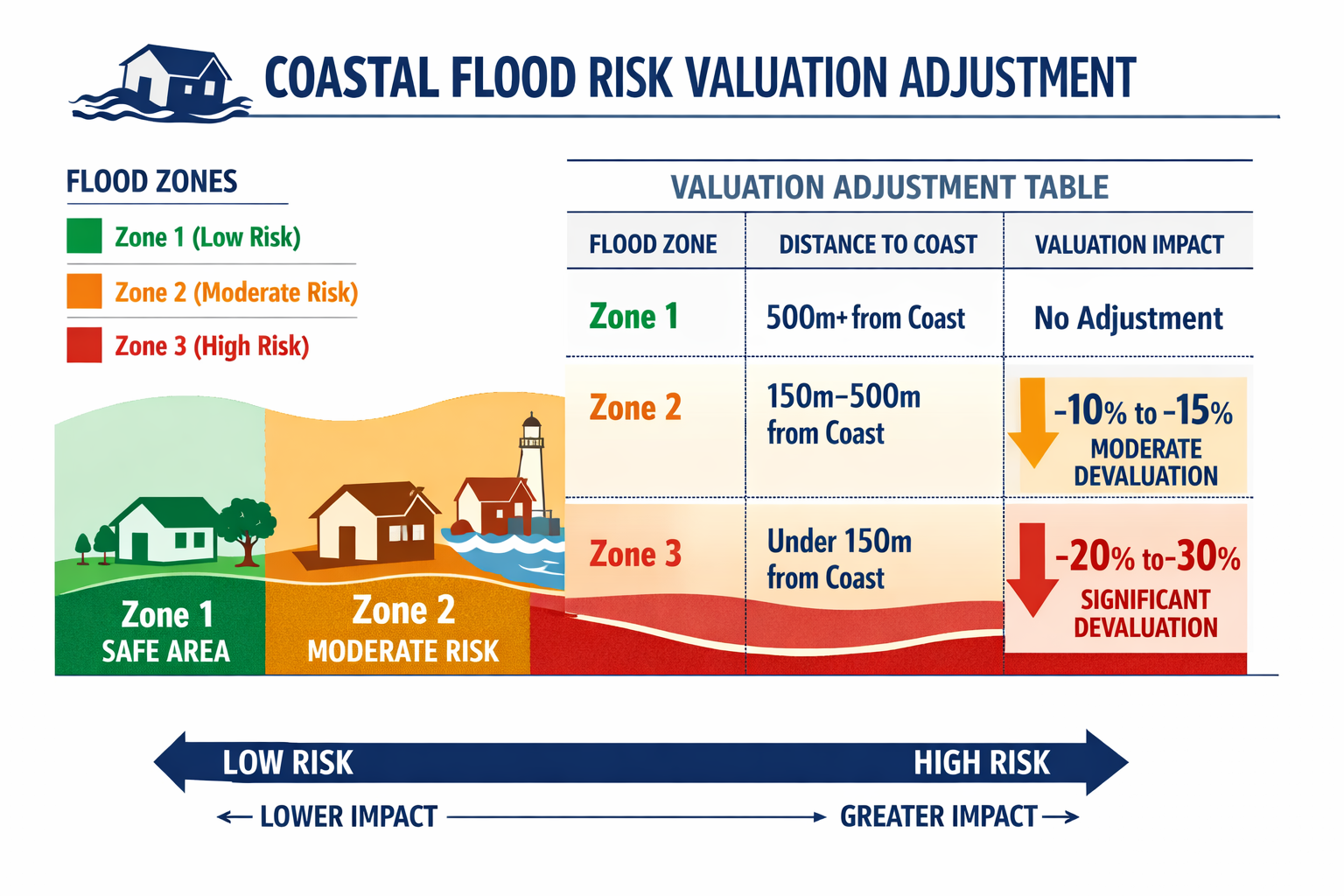

📊 Stage 3: Valuation Adjustment Framework

Once on-site data is gathered, surveyors and valuers should apply a structured adjustment framework. The following bands reflect current market conditions in 2026:

| Flood Zone | Resilience Measures Present | Indicative Valuation Adjustment |

|---|---|---|

| Zone 1 (low risk) | N/A | Nil adjustment |

| Zone 2 (medium risk) | Yes | -3% to -8% |

| Zone 2 (medium risk) | No | -8% to -15% |

| Zone 3a (high risk) | Yes | -10% to -18% |

| Zone 3a (high risk) | No | -18% to -25%+ |

| Zone 3b (functional floodplain) | Any | Case-by-case; significant discount |

⚠️ Important: These bands are indicative guidance for professional judgment, not fixed rules. Local market conditions, specific defence infrastructure, and individual property characteristics all influence the final figure.

69% of English constituencies are projected to see flood risk increases exceeding 25% by mid-century [5], meaning that valuation adjustments applied today may need to be reviewed at each transaction point as risk profiles evolve.

Insurance, Flood Re, and the Long-Term Buyer Risk Picture

One of the most consequential — and frequently underexplained — aspects of flood risk valuation is the insurance cost trajectory. The Flood Re scheme currently maintains affordable home insurance pricing for high-risk properties, acting as a reinsurance backstop that keeps premiums manageable [6]. However, Flood Re is a temporary mechanism scheduled to end in 2039, on the assumption that flood risk will decline and the market will transition to risk-reflective pricing [6].

For a buyer purchasing a coastal property today with a 25-year mortgage, the post-2039 insurance environment is a live financial risk. Surveyors and valuers have a professional responsibility to flag this in their reports.

Key points to communicate to buyers:

- Flood Re eligibility does not transfer automatically — it applies to the property, not the owner, but properties built after 2009 are excluded

- Risk-reflective pricing post-2039 could see premiums increase substantially for Zone 2 and Zone 3 properties

- One in nine new homes built between 2022–2024 are already in medium or high flood risk areas [5] — buyers of newer coastal properties should not assume modern construction equals low risk

For properties where insurance reinstatement costs need formal assessment — particularly relevant after flood damage — insurance reinstatement cost valuations provide the professional framework lenders and insurers require.

Flood Risk Valuation Adjustments After Spring 2026 Events: Advanced Survey Tools and Reporting Standards

Drone Surveys for Coastal Properties

Traditional ground-level inspections have limitations for coastal properties — particularly where sea walls, cliff edges, or tidal channels make close physical access difficult or hazardous. Premium drone surveys now provide surveyors with high-resolution aerial imagery of roof conditions, chimney stacks, parapet walls, and the interface between a property and adjacent flood defence infrastructure. In a post-spring-2026 environment where roof drainage and surface water management are critical, this technology adds material value to the assessment.

Reporting Standards: What a Flood-Focused Survey Report Must Include

A Level 3 Building Survey for a coastal property in 2026 should explicitly address:

- ✅ Flood zone classification and source (Environment Agency, date of check)

- ✅ Surface water flood risk rating

- ✅ Evidence of past flood events (physical signs and historic records)

- ✅ Condition and adequacy of existing resilience measures

- ✅ Proximity to named water bodies and coastal defence assets

- ✅ Drainage condition and surface water management adequacy

- ✅ Electrical and utility installation heights relative to flood risk

- ✅ FCERM benefit area status and defence funding outlook [1]

- ✅ Flood Re eligibility and post-2039 insurance risk flag [6]

- ✅ Recommended further investigations (specialist drainage survey, structural engineer review)

For properties where flood-related findings require specialist follow-up, understanding areas of further investigation in a building survey ensures that the right professionals are engaged at the right stage.

Budgeting for Flood Resilience Works

Surveyors should provide clients with realistic cost guidance for remediation and resilience upgrades. Typical measures and indicative costs in 2026 include:

| Resilience Measure | Approximate Cost |

|---|---|

| Flood doors (per opening) | £1,500 – £4,000 |

| Air brick covers (set) | £200 – £600 |

| Non-return valves on drainage | £300 – £800 |

| Raised electrical installation | £1,500 – £3,500 |

| Tanking to basement walls | £5,000 – £15,000+ |

| Professional flood risk report | £500 – £1,500 |

Detailed guidance on budgeting for repairs and restoration helps buyers and owners understand the full financial picture before committing to a coastal property purchase.

The Buyer's Decision Framework: When to Walk Away

Not every coastal property with flood risk is a poor investment — but buyers need a clear decision framework. The following factors, taken together, should prompt serious reconsideration:

- 🚩 Zone 3b (functional floodplain) classification with no resilience measures

- 🚩 Evidence of repeated historic flooding with no remediation

- 🚩 Ageing coastal defence infrastructure with no confirmed FCERM funding for repair or replacement [1]

- 🚩 Property built after 2009 (Flood Re ineligible) in Zone 2 or 3

- 🚩 Mortgage lender requiring specialist flood report as a condition of offer

- 🚩 Insurance quotes already significantly above market average

If a valuation comes in below the agreed purchase price — which is increasingly common for coastal properties in the current environment — understanding what to do if your home valuation is less than an offer provides practical guidance on next steps.

Conclusion: Actionable Next Steps for Buyers, Sellers, and Surveyors

The spring 2026 flood events have accelerated a structural shift in how coastal UK properties are assessed, valued, and insured. The data is unambiguous: 43,937 homes in medium or high flood risk areas, 69% of English constituencies facing 25%+ risk increases by mid-century [5], and a Flood Re safety net that expires in 2039 [6] — these are not distant concerns. They are live valuation variables that belong in every survey report written today.

For buyers: Commission a Level 3 Building Survey with an explicit flood resilience assessment for any coastal or low-lying property. Check Flood Re eligibility and request an insurance reinstatement cost valuation before exchange.

For sellers: Invest in documented resilience measures before marketing. Properties with evidence of flood-proofing works achieve materially better valuations and attract stronger buyer confidence.

For surveyors: Adopt the three-stage protocol outlined above — pre-inspection data gathering, on-site structural and resilience assessment, and structured valuation adjustment — as standard practice for all coastal instructions in 2026. Reference FCERM benefit area maps and flag the post-2039 insurance environment in every relevant report.

The professionals who treat flood risk as a core competency — not an add-on — will provide the greatest value to clients navigating one of the most complex property risk environments the UK has seen in a generation.

References

[1] Flood Funding Reform 2026 The New Fcerm Guidance Explained – https://www.unda.co.uk/news/flood-funding-reform-2026-the-new-fcerm-guidance-explained/

[2] The Flood Map For Planning Is Changing Heres What It Could Mean For You – https://pfaconsulting.co.uk/the-flood-map-for-planning-is-changing-heres-what-it-could-mean-for-you/

[3] Study Warns Extreme Flood Predictions Can Sink Coastal Property Prices – https://www.port.ac.uk/news-events-and-blogs/news/study-warns-extreme-flood-predictions-can-sink-coastal-property-prices

[4] London Flood Risk April 2026 – https://disastercarecapital.co.uk/london-flood-risk-april-2026/

[5] Proportion Of New Homes Built In Flood Areas Rises To One In Nine – https://www.aviva.com/newsroom/news-releases/2026/02/proportion-of-new-homes-built-in-flood-areas-rises-to-one-in-nine/

[6] Keeping Flood Insurance Affordable – https://www.lboro.ac.uk/news-events/news/2026/february/keeping-flood-insurance-affordable/