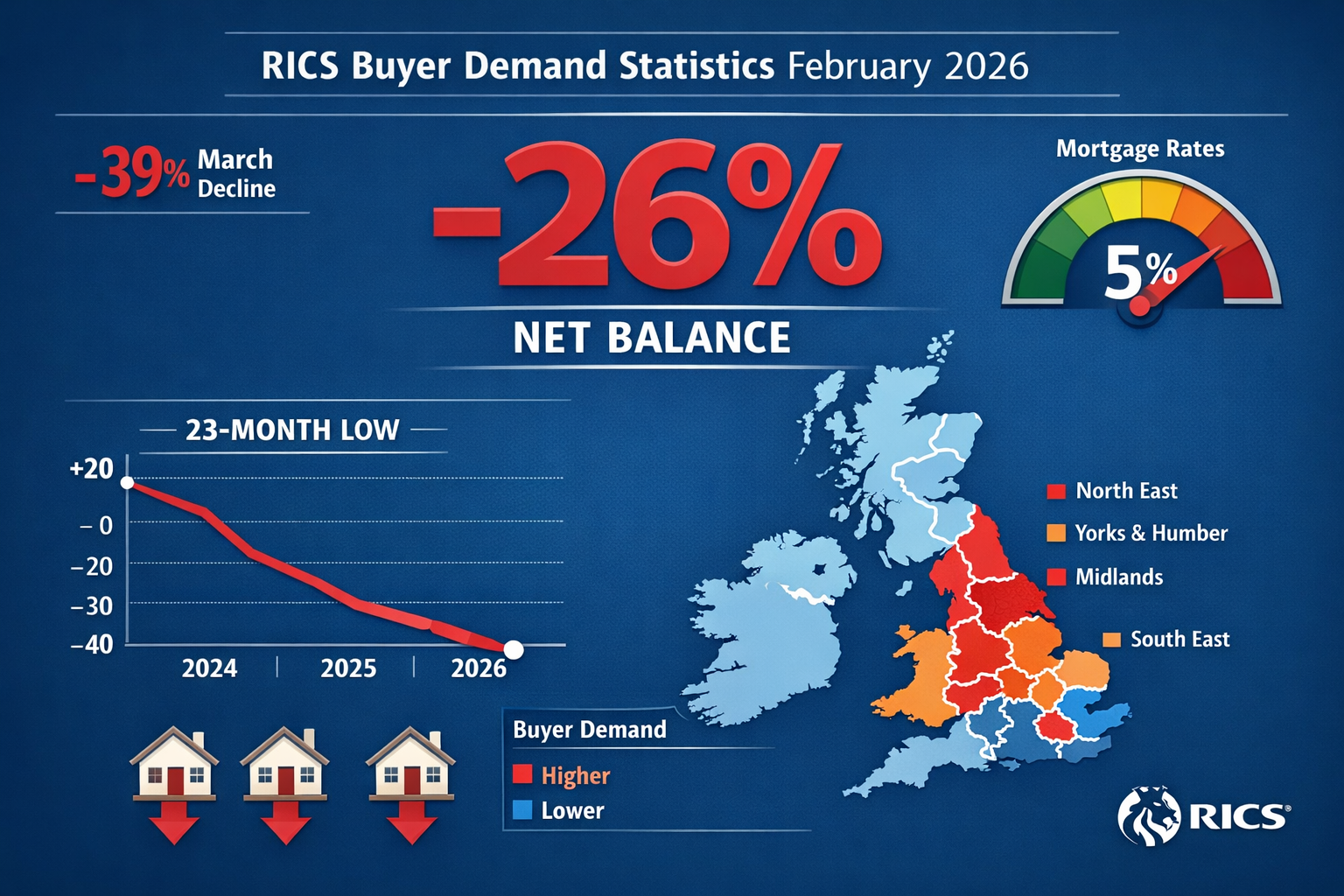

The UK residential property market witnessed buyer enquiries plummet to -26% net balance in February 2026, with conditions deteriorating further to -39% by March—the weakest reading since August 2023. [1] For chartered surveyors tasked with defending property valuations amid this demand collapse, the challenge has never been more acute. When geopolitical uncertainty drives sentiment into freefall while underlying fundamentals tell a different story, valuation accuracy becomes both a professional imperative and a competitive advantage. The Buyer Demand Collapse and Valuation Accuracy: RICS February 2026 Data for Surveyors Navigating Geopolitical Uncertainty presents a critical inflection point where short-term market pessimism must be carefully distinguished from longer-term value resilience.

Key Takeaways

- Buyer enquiries collapsed to -39% in March 2026, marking a 23-month low driven by Middle East conflict escalation and rising borrowing costs above 5% [1]

- Agreed sales plummeted from -13% to -34% between February and March 2026, creating significant headwinds for transaction completions [1]

- Regional divergence remains pronounced, with London experiencing -40% price pressure while Scotland and Northern Ireland show firmer trends [3]

- Three-month price expectations weakened to -43%, yet 12-month forecasts remain at +2%, highlighting the gap between sentiment and fundamentals [1]

- Surveyors must adopt robust frameworks for adjusting valuations that account for temporary demand shocks without overcorrecting for geopolitical noise

Understanding the February 2026 Market Collapse Context

The Scale of Demand Deterioration

The RICS residential market survey data for February and March 2026 reveals an unprecedented velocity of decline in buyer activity. New buyer enquiries, which serve as a leading indicator of future transaction volumes, registered at -26% net balance in February before accelerating downward to -39% by March. [1] This represents the highest number of surveyors reporting falling enquiries since August 2023, creating a 23-month low that has caught many market participants off guard. [2]

The deterioration wasn't limited to enquiries alone. Agreed sales showed an even more dramatic collapse, moving from -13% in February to -34% in March 2026. [1] This sharp contraction in sales agreements signals that the pipeline of transactions moving toward completion has narrowed significantly, with direct implications for surveyors conducting valuations on properties where buyers are increasingly cautious or withdrawing entirely.

Geopolitical Triggers and Economic Headwinds

Two primary factors drove this demand collapse: the escalation of the Middle East conflict and rising borrowing costs. Average fixed mortgage rates climbed back above the psychologically significant 5% threshold, substantially increasing the cost of homeownership for buyers already stretched by elevated property prices. [1] The geopolitical uncertainty added a second layer of hesitancy, as potential buyers adopted a "wait and see" approach amid concerns about broader economic stability and potential spillover effects.

The inventory situation adds further complexity to the valuation environment. The average number of homes on estate agents' books rose from 45 at the start of 2026 to 47 by March, indicating increased supply pressure as demand weakens. [2] Meanwhile, market appraisals remained flat in March 2026, suggesting the pipeline of new sellers is unlikely to increase significantly in the near term. [2] This creates a classic supply-demand imbalance that typically exerts downward pressure on prices—yet surveyors must determine whether this pressure represents genuine value erosion or temporary market dysfunction.

For those conducting building surveys during this period, the challenge extends beyond identifying structural issues to accurately reflecting market conditions in valuation reports.

Buyer Demand Collapse and Valuation Accuracy: Frameworks for Defending Professional Opinions

Distinguishing Sentiment from Fundamentals

The core challenge facing surveyors navigating the Buyer Demand Collapse and Valuation Accuracy: RICS February 2026 Data for Surveyors Navigating Geopolitical Uncertainty lies in separating temporary sentiment-driven price pressure from genuine fundamental value changes. The RICS data reveals a telling divergence: while three-month price expectations plummeted to -43% in March 2026, indicating surveyors anticipate accelerating downward pressure in the immediate term, 12-month price expectations edged down only modestly to +2%. [1]

This gap between short-term and medium-term outlooks suggests professional surveyors recognize the current demand collapse as partially sentiment-driven rather than reflecting permanent structural weakness. When defending valuations, this distinction becomes crucial. A property's intrinsic value—determined by location, condition, comparable sales, and income-generating potential—doesn't change overnight simply because geopolitical events create temporary buyer hesitancy.

The Adjustment Methodology Framework

Professional surveyors must adopt a systematic approach to adjusting valuations during periods of market volatility:

1. Comparable Selection Criteria 📊

- Prioritize recent transactions (last 3-6 months) but weight them according to market conditions at the time of sale

- Identify comparables completed before the February 2026 demand collapse and those after

- Apply time adjustments that reflect the velocity of market change rather than simple linear depreciation

2. Sentiment Discount Quantification 💷

- Separate observable price reductions (actual transaction data) from anticipated reductions (survey expectations)

- Apply a "geopolitical uncertainty discount" only when supported by concrete comparable evidence

- Document the rationale for any sentiment-based adjustments with reference to RICS survey data

3. Regional Variation Recognition 🗺️

- Acknowledge pronounced regional divergence, with London at -40% price pressure, South East at -24%, and East Anglia at -26% [3]

- Apply location-specific adjustments rather than national averages

- Recognize that Scotland, Northern Ireland, and North West England continue reporting firmer price trends [3]

4. Property-Specific Resilience Factors 🏠

- Assess whether the subject property possesses characteristics that insulate it from demand volatility

- Consider factors such as school catchment areas, transport links, and scarcity value

- Evaluate whether the property appeals to cash buyers or investors less affected by mortgage rate increases

Understanding what's looked at during a property valuation becomes even more critical when market conditions shift rapidly.

Documentation and Professional Standards

The RICS Valuation – Global Standards (Red Book) requires valuers to provide sufficient information to enable readers to understand the valuation properly. During periods of market uncertainty, this obligation intensifies. Surveyors must:

- Explicitly state assumptions about market conditions and how they've been incorporated into the valuation

- Quantify uncertainty ranges by providing confidence intervals or alternative scenarios

- Reference authoritative data sources such as RICS survey results, Land Registry data, and local market intelligence

- Distinguish between Market Value and other bases such as investment value or forced sale value

When conducting professional valuations, the quality of documentation becomes your primary defense if valuations are later challenged as market conditions evolve.

Practical Strategies: Buyer Demand Collapse and Valuation Accuracy in RICS February 2026 Context

Scenario Analysis and Sensitivity Testing

Given the divergence between short-term sentiment (-43% three-month expectations) and longer-term outlook (+2% twelve-month expectations), surveyors should consider providing scenario-based valuations:

| Scenario | Probability | Price Adjustment | Rationale |

|---|---|---|---|

| Rapid Recovery | 25% | -5% to -8% | Geopolitical tensions ease within 3 months; mortgage rates stabilize |

| Base Case | 50% | -10% to -15% | Gradual demand recovery over 6-9 months; modest price softening |

| Extended Weakness | 25% | -18% to -22% | Prolonged uncertainty; mortgage rates remain elevated through Q3 2026 |

This approach acknowledges uncertainty while providing clients with actionable intelligence. For Level 3 full building surveys, incorporating market condition commentary alongside structural findings creates a more comprehensive advisory product.

Regional Intelligence Integration

The RICS February 2026 data reveals significant regional variation that demands localized analysis. Surveyors operating in London and the South East face markedly different conditions than those in Scotland or Northern Ireland. [3] Practical strategies include:

London and South East Approach 🏙️

- Apply more conservative adjustments reflecting -40% and -24% regional price pressure respectively

- Emphasize comparable transactions from the past 60 days given rapid market deterioration

- Consider the impact of international buyer withdrawal due to geopolitical concerns

- Assess whether properties fall into resilient micro-markets (prime central locations, transport hubs)

Scotland and Northern Ireland Approach 🏴

- Recognize firmer price trends that may justify minimal or no sentiment-based discounts

- Focus on local employment conditions and regional economic fundamentals

- Consider whether areas benefit from relative affordability compared to southern markets

For surveyors working across multiple regions, maintaining location-specific market intelligence files becomes essential. Those offering services as chartered surveyors in Central London versus North West London must tailor their approaches accordingly.

Transaction Evidence Hierarchy

During periods of rapid market change, not all comparable evidence carries equal weight. Establish a clear hierarchy:

Tier 1: Recent Completed Sales ⭐⭐⭐

- Transactions completed in March-April 2026 (post-collapse)

- Highest reliability for current market conditions

- Limited availability may be an issue

Tier 2: February 2026 Agreed Sales ⭐⭐

- Agreed before the sharpest decline but completing now

- Require adjustment for changed market sentiment

- More abundant than Tier 1 evidence

Tier 3: Late 2025/Early 2026 Completions ⭐

- Reflect pre-collapse market conditions

- Require significant time and sentiment adjustments

- Useful for establishing baseline values before market shift

Tier 4: Asking Prices and Withdrawn Properties

- Indicative of seller expectations rather than market reality

- Useful for understanding supply-side psychology

- Should not be primary valuation evidence

Client Communication Protocols

The Buyer Demand Collapse and Valuation Accuracy: RICS February 2026 Data for Surveyors Navigating Geopolitical Uncertainty demands enhanced client communication. Surveyors should:

-

Set Realistic Expectations Early 📞

- Explain market volatility during initial instructions

- Clarify that valuations reflect a specific date and may require updating

- Discuss the distinction between valuation for purchase, mortgage, and insurance purposes

-

Provide Context-Rich Reports 📄

- Include a dedicated market conditions section referencing RICS data

- Explain how geopolitical factors have been considered

- Offer guidance on timing considerations for transactions

-

Establish Review Triggers 🔄

- Recommend valuation reviews if completion is delayed beyond 90 days

- Identify market indicators that would necessitate revaluation

- Create clear protocols for updating opinions as conditions evolve

For specialized valuations such as leasehold extension valuations or SIPP pension valuations, market volatility adds complexity that requires explicit discussion with clients.

Risk Management and Professional Indemnity Considerations

Valuation Uncertainty and Liability Exposure

The rapid deterioration in market conditions between February and March 2026—with agreed sales dropping from -13% to -34% in a single month [1]—creates heightened professional indemnity risk for surveyors. When valuations are challenged months after completion, demonstrating that the opinion was reasonable at the valuation date becomes critical.

Key Risk Mitigation Strategies:

✅ Material Uncertainty Clauses: Consider including material uncertainty declarations when market evidence is particularly sparse or contradictory, following RICS guidance on valuation uncertainty

✅ Shortened Validity Periods: Explicitly state that valuations are valid for 60-90 days rather than the traditional 6 months, given rapid market evolution

✅ Assumption Documentation: Clearly document all assumptions about market trajectory, buyer behavior, and geopolitical developments

✅ Peer Review Protocols: Implement internal review processes for valuations in volatile markets, particularly for high-value properties

✅ Continuing Professional Development: Ensure all valuers have completed recent training on valuing in uncertain markets and geopolitical risk assessment

Mortgage Lending and Down-Valuation Protocols

The collapse in agreed sales to -34% in March 2026 [1] has direct implications for mortgage valuations. Lenders are increasingly cautious, and surveyors conducting valuations for lending purposes face particular scrutiny. When market values fall below agreed purchase prices:

- Quantify the gap precisely with reference to specific comparable evidence

- Distinguish between overpricing and market movement since the offer was accepted

- Provide lenders with market velocity data from RICS surveys to contextualize the down-valuation

- Recommend appropriate loan-to-value ratios that reflect current market risk

For buyers who commissioned RICS building surveys and now face down-valuations, understanding average price reductions after survey becomes particularly relevant in the current market.

Looking Forward: 12-Month Market Trajectory and Valuation Implications

Interpreting the Sentiment-Fundamentals Gap

The most intriguing aspect of the RICS February 2026 data is the divergence between near-term pessimism and medium-term stability. While three-month price expectations collapsed to -43%, twelve-month expectations remained at +2%. [1] This suggests professional surveyors collectively believe:

- Short-term overshooting is likely – Current sentiment-driven weakness will push prices below fundamental value temporarily

- Recovery mechanisms exist – Market forces will eventually correct the sentiment-driven decline

- Geopolitical risks are temporary – The Middle East conflict and associated uncertainty will moderate over time

- Structural demand remains – Underlying housing need hasn't disappeared despite transaction volume collapse

For surveyors, this creates an opportunity to position themselves as market experts who can distinguish noise from signal. Valuations that acknowledge short-term weakness while recognizing medium-term resilience demonstrate sophisticated market understanding.

Preparing for Market Recovery

History suggests that sentiment-driven market collapses often create sharp recovery trajectories once triggering factors resolve. Surveyors should prepare for:

Phase 1: Stabilization (Q2-Q3 2026) 🔄

- Buyer enquiries stabilize but remain subdued

- Transaction volumes remain below historical averages

- Price declines moderate as sellers adjust expectations

- Valuation approach: Conservative but recognize stabilization signals

Phase 2: Early Recovery (Q4 2026) 📈

- Mortgage rates begin to decline from 5%+ peak

- Geopolitical concerns ease or markets adapt

- Buyer enquiries turn positive

- Valuation approach: Begin incorporating recovery momentum into forward-looking assumptions

Phase 3: Normalization (2027) ✅

- Transaction volumes return to historical norms

- Regional variations persist but moderate

- Price growth resumes in most markets

- Valuation approach: Return to standard comparable methodologies with reduced uncertainty

Emerging Opportunities for Surveying Practices

The Buyer Demand Collapse and Valuation Accuracy: RICS February 2026 Data for Surveyors Navigating Geopolitical Uncertainty creates several business opportunities for forward-thinking practices:

Portfolio Revaluation Services 💼

- Investors and institutions require updated valuations reflecting current market conditions

- Opportunity to provide regular revaluation services with market commentary

- Particularly relevant for SIPP pension valuations and annual tax valuations

Market Intelligence Subscriptions 📊

- Package RICS data analysis with local market intelligence

- Provide clients with monthly market condition reports

- Position practice as thought leader in market analysis

Distressed Asset Valuation 🏚️

- As some sellers face financial pressure, specialized valuation expertise becomes valuable

- Opportunity to value properties requiring quick sales or facing urgent building issues

Advisory Services 🎯

- Expand beyond traditional valuation to strategic advisory

- Help clients optimize transaction timing based on market trajectory analysis

- Provide scenario planning for developers and investors

Conclusion

The Buyer Demand Collapse and Valuation Accuracy: RICS February 2026 Data for Surveyors Navigating Geopolitical Uncertainty represents one of the most challenging valuation environments in recent years. With buyer enquiries plummeting to -39% by March 2026 and agreed sales collapsing to -34%, surveyors face intense pressure to defend valuations amid rapidly deteriorating sentiment. [1] Yet the divergence between three-month expectations (-43%) and twelve-month forecasts (+2%) reveals a critical insight: professional surveyors recognize that current weakness reflects temporary sentiment rather than permanent fundamental erosion. [1]

The framework for maintaining valuation accuracy in this environment rests on several pillars: rigorous comparable selection that accounts for transaction timing, explicit documentation of market assumptions and uncertainty, regional analysis that recognizes London's -40% price pressure differs markedly from Scotland's firmer trends, and clear client communication that sets realistic expectations. [3] Surveyors who adopt scenario-based approaches, quantify uncertainty ranges, and distinguish between short-term noise and medium-term fundamentals will not only protect their professional liability but position themselves as trusted advisors capable of navigating market volatility.

Actionable Next Steps for Surveyors

- Review and update your valuation templates to include dedicated market conditions sections referencing current RICS data

- Establish regional market intelligence systems that track local transaction volumes, price movements, and inventory levels weekly

- Implement peer review protocols for all valuations exceeding £500,000 or in particularly volatile micro-markets

- Schedule CPD training focused on valuing in uncertain markets and geopolitical risk assessment

- Develop client communication materials explaining the February-March 2026 market collapse and its implications for valuations

- Consider specialized service offerings such as portfolio revaluations, market intelligence subscriptions, or advisory services

- Monitor leading indicators including mortgage approval volumes, RICS survey releases, and geopolitical developments to anticipate market turning points

The surveyors who emerge strongest from this period will be those who maintained rigorous professional standards, communicated transparently with clients, and demonstrated the analytical sophistication to separate temporary sentiment from enduring value. The Buyer Demand Collapse and Valuation Accuracy: RICS February 2026 Data for Surveyors Navigating Geopolitical Uncertainty is not merely a challenge to overcome—it's an opportunity to demonstrate the irreplaceable value of professional surveying expertise when markets become irrational.

For comprehensive surveying services that account for current market conditions, explore our full range of valuation and survey options or understand the difference between Level 2 and Level 3 surveys to determine the appropriate level of investigation for your property needs.

References

[1] Rising Borrowing Costs Knock Housing Buyer Demand – https://www.credit-connect.co.uk/news/consumer-lending/financial-services/rising-borrowing-costs-knock-housing-buyer-demand/

[2] Rising Number Of Surveyors Report Fall In Housing Market Activity Rics – https://www.mortgagesolutions.co.uk/mortgage-news/2026/04/09/rising-number-of-surveyors-report-fall-in-housing-market-activity-rics/

[3] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026