The abolition of Section 21 "no-fault" evictions marks the most significant shift in landlord-tenant law in a generation, fundamentally altering how property surveyors must approach buy-to-let (BTL) valuations. With rolling periodic tenancies replacing fixed-term assured shorthold tenancies (ASTs), rental income streams have transformed from predictable to volatile overnight. Valuation Adjustments for Renters' Rights Act 2026: What Property Surveyors Must Factor Into BTL Assessments now require a complete recalibration of yield calculations, void period assumptions, and risk premiums to reflect this new regulatory landscape.

The stakes are considerable. Lenders are already implementing stricter stress tests and more conservative affordability calculations, while surveyors face enhanced due diligence requirements that extend far beyond traditional comparable analysis. From mandatory Decent Homes Standard compliance to restricted rent increase assumptions, every element of BTL property assessment demands fresh scrutiny in 2026.

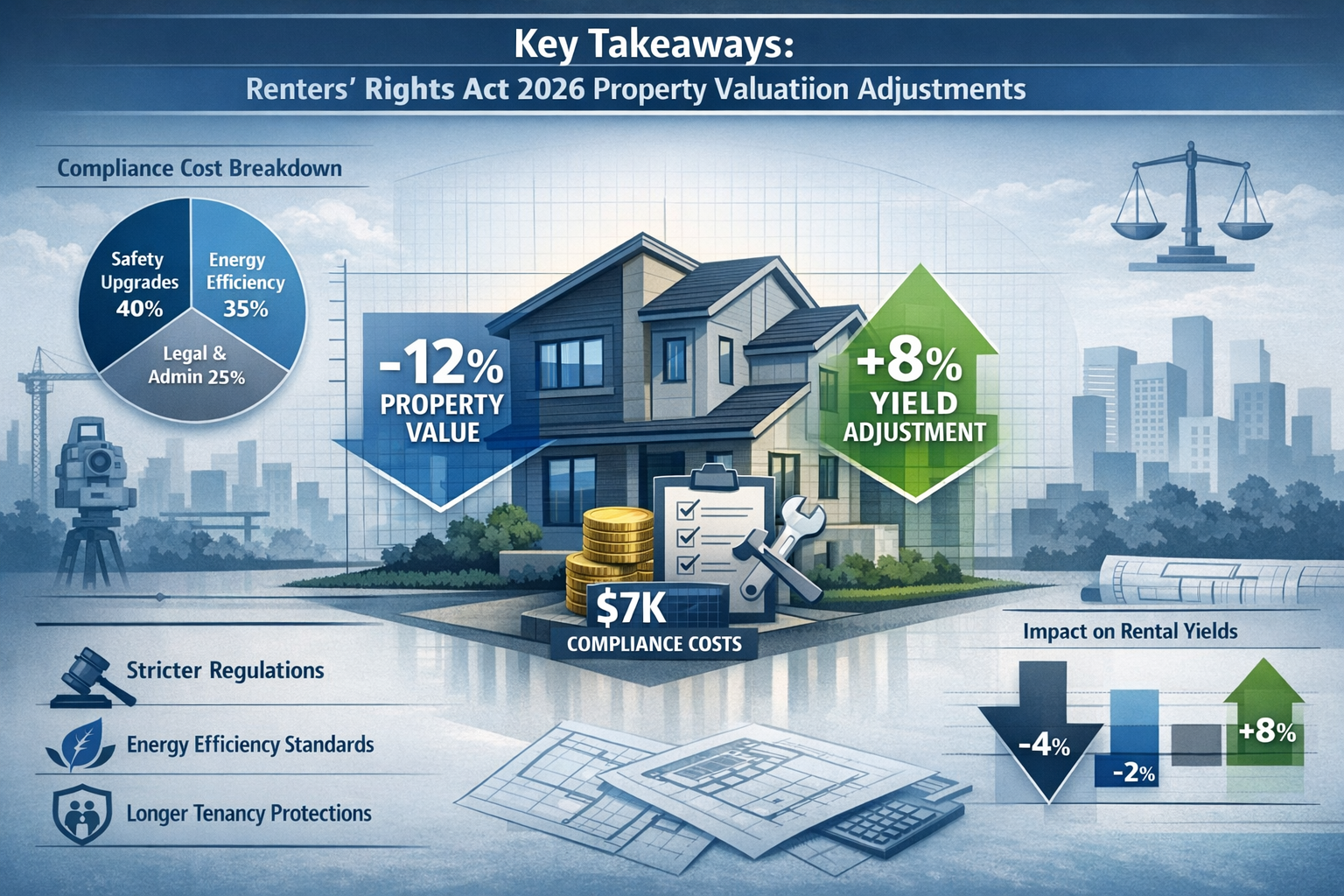

Key Takeaways

- 🏛️ Section 21 abolition creates unpredictable possession timelines requiring 50-100% increases in void period assumptions

- 📉 Yield compressions of 1-2% are necessary to account for rental income volatility and increased operational costs

- 🏠 Decent Homes Standard compliance by 2035 mandates capital expenditure assessments of £5,000-£15,000 per property

- 📊 Rent increase restrictions limit growth to once annually after 12 months, requiring conservative inflation projections

- ⚡ EPC rating upgrades to minimum 'C' grade by 2030 necessitate substantial energy efficiency investment factoring

Understanding the Fundamental Shifts in BTL Valuation Methodology

The Renters' Rights Act 2026 introduces structural changes that challenge traditional valuation methodologies. Property surveyors must now incorporate legislative risk factors that were previously negligible or non-existent in their professional valuation assessments.

The End of Predictable Tenancy Terms

Rolling periodic tenancies represent a paradigm shift from the stability of fixed-term ASTs. Tenants can now exit with just two months' notice at any point, creating highly unpredictable rental income streams that fundamentally alter cash flow projections [2]. This volatility directly impacts:

- Gross yield calculations requiring downward adjustments of 0.5-1.5%

- Net operating income forecasts with increased uncertainty margins

- Capitalisation rates demanding higher risk premiums

- Comparative market analysis requiring peer properties under identical regulatory constraints

Surveyors must now assess comparable rents with the understanding that tenant retention has become significantly more uncertain. The traditional 12-month fixed-term benchmark no longer applies, necessitating more conservative income stability assumptions throughout the valuation process.

Section 21 Abolition and Possession Timeline Impacts

The removal of Section 21 "no-fault" evictions fundamentally alters the possession landscape for landlords. Previously, landlords could regain possession with two months' notice without providing justification. Now, all possession proceedings must follow grounds-based court processes under Section 8, creating lengthier and more expensive timelines [2][4].

RICS guidance emphasises that valuations must now account for:

- Extended possession periods averaging 6-9 months versus previous 2-3 months

- Legal costs ranging from £2,000-£5,000 per possession case

- Lost rental income during extended void periods

- Increased risk of property damage during protracted proceedings

The practical implication for surveyors conducting independent property valuations is clear: void period assumptions must increase by 50-100% to reflect realistic possession timelines under the new regime [2]. This directly reduces net yield calculations and impacts loan-to-value ratios for BTL mortgage applications.

Valuation Adjustments for Renters' Rights Act 2026: Quantifying the Yield Impact

Translating legislative changes into concrete valuation adjustments requires systematic analysis across multiple variables. Property surveyors must now apply quantifiable downward adjustments to reflect increased operational risks and reduced income certainty.

Revised Void Period Calculations

Traditional BTL valuations assumed void periods of 2-4 weeks annually for well-maintained properties in strong rental markets. Under the Renters' Rights Act 2026, these assumptions require substantial revision:

| Void Period Component | Pre-2026 Assumption | Post-2026 Adjustment |

|---|---|---|

| Standard tenant turnover | 2-4 weeks | 4-6 weeks |

| Possession proceedings (if required) | 8-12 weeks | 24-36 weeks |

| Annual void allowance | 4-6% of gross rent | 8-12% of gross rent |

| Emergency possession scenarios | Rare consideration | Mandatory stress test |

These extended void periods directly impact net operating income calculations. For a property generating £1,500 monthly rent, the difference between a 5% void assumption (£900 annually) and a 10% assumption (£1,800 annually) represents a £900 reduction in annual net income – equivalent to approximately 1-1.5% reduction in net yield on a typical £150,000 BTL property [2].

Rent Increase Restriction Impacts

The Act prohibits rent increases within the first 12 months of any tenancy and limits increases to once annually thereafter, with tenants gaining the right to challenge increases they consider above market value [2][5]. This creates several valuation challenges:

Conservative inflation assumptions must replace previous aggressive rent growth projections. Where surveyors might have previously factored 3-5% annual rent increases in strong markets, post-2026 assessments should adopt more cautious 2-3% projections to account for:

- Tenant challenge mechanisms reducing effective increase rates

- Extended notice periods for rent reviews

- Market value caps preventing above-inflation increases

- Increased administrative burden discouraging frequent reviews

For long-term investment valuations using discounted cash flow methodologies, these restrictions compress projected income growth significantly. A 10-year DCF model assuming 4% annual rent growth versus 2.5% growth creates valuation differences of 15-20% on identical properties [1].

Lender Stress Test Implications

Mortgage lenders have responded to the Renters' Rights Act by implementing tighter affordability controls and more conservative stress tests [2]. Surveyors must understand these lending criteria shifts as they directly impact property marketability and valuation:

- Interest coverage ratios (ICR) increasing from 125% to 145% of projected rental income

- Stress test interest rates rising from 5.5% to 6.5-7% for affordability calculations

- Minimum deposit requirements increasing from 20% to 25% for new BTL purchases

- Portfolio landlord scrutiny intensifying for investors with 4+ mortgaged properties

These lending restrictions reduce the pool of viable purchasers for BTL properties, creating downward pressure on market values. Understanding how property market legislation changes affect financing availability is essential for accurate market value assessments.

Valuation Adjustments for Renters' Rights Act 2026: Compliance Cost Integration

Beyond income volatility and possession risks, surveyors must now factor substantial compliance and upgrade costs into BTL valuations. These capital expenditure requirements represent deferred liabilities that reduce net asset values.

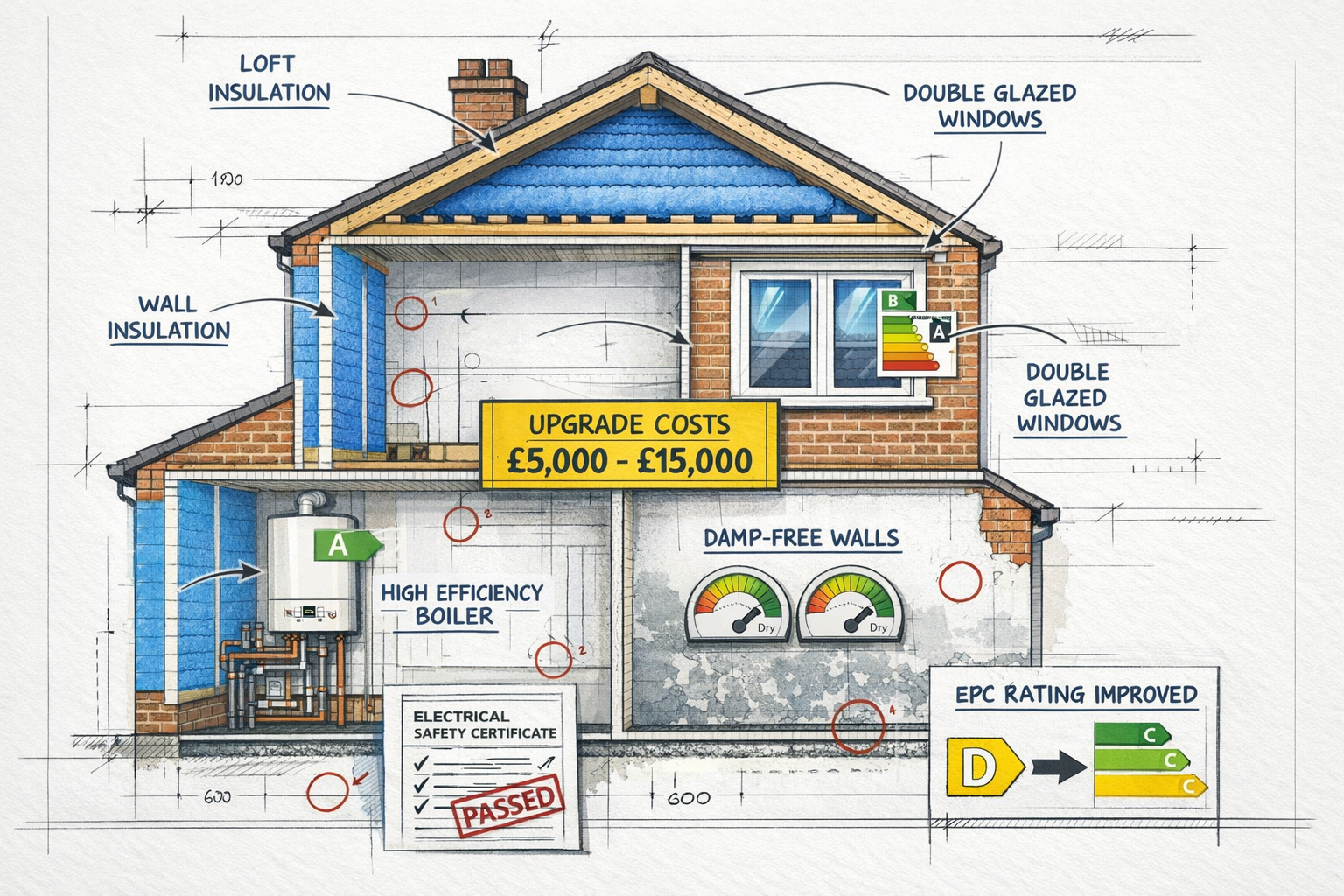

Decent Homes Standard Compliance Requirements

For the first time, the Decent Homes Standard applies to the private rented sector, with mandatory compliance required by 2035 [2][6]. This standard mandates that rental properties must be:

- Warm: Adequate heating systems and insulation

- Weatherproof: Free from serious disrepair to roof, windows, and external walls

- Safe: Free from Category 1 hazards under the Housing Health and Safety Rating System (HHSRS)

- Modern: Reasonably modern kitchen and bathroom facilities

Surveyors must assess compliance gaps and factor remediation costs into valuations. Typical upgrade costs include:

| Compliance Element | Estimated Cost Range |

|---|---|

| Loft and cavity wall insulation | £1,500 – £3,500 |

| Modern boiler replacement | £2,000 – £4,000 |

| Double glazing upgrades | £3,000 – £8,000 |

| Kitchen modernisation | £4,000 – £10,000 |

| Bathroom upgrades | £3,000 – £7,000 |

| Electrical rewiring | £3,000 – £6,000 |

| Damp and mould remediation | £1,000 – £5,000 |

For older properties currently falling short of these standards, total compliance costs can range from £5,000 to £25,000 depending on property condition and size [6]. These costs must be deducted from gross market value or factored into reduced comparables analysis.

Energy Performance Certificate (EPC) Rating Upgrades

The minimum EPC rating for rental properties is rising to 'C' grade by 2030, with the new assessment system launching in 2026 [6]. Properties currently rated D or E face substantial upgrade requirements:

Typical EPC improvement measures and associated costs:

- 🔥 Air source heat pump installation: £8,000 – £14,000

- 🪟 Triple glazing replacement: £5,000 – £12,000

- 🏠 External wall insulation: £8,000 – £15,000

- ☀️ Solar panel installation: £4,000 – £8,000

- 💨 Mechanical ventilation with heat recovery: £3,000 – £6,000

For properties requiring multiple interventions to achieve 'C' rating, total costs can exceed £15,000-£30,000 [6]. Surveyors must assess current EPC ratings, identify the improvement pathway to 'C' grade, and incorporate these costs into valuation adjustments.

Understanding EPC requirements and MEES compliance has become essential for accurate BTL valuations in 2026.

Enhanced Due Diligence Requirements

RICS guidance now mandates that valuations incorporate specialist expertise and enhanced due diligence processes [3]. This includes:

- Verification of Decent Homes Standard compliance status

- Deposit Protection scheme compliance confirmation

- Review of tenant deposit documentation

- Assessment of ongoing maintenance schedules

- Evaluation of landlord licensing compliance (where applicable)

- Analysis of historical void periods and tenant turnover rates

These enhanced requirements increase surveyor liability and necessitate more comprehensive building survey approaches that extend beyond traditional comparable analysis.

Practical Application: Adjusting Comparable Analysis

When conducting comparable market analysis for BTL valuations, surveyors must now apply systematic adjustments to reflect Renters' Rights Act impacts:

Step 1: Identify True Comparables

Ensure comparable properties are subject to identical regulatory constraints. Pre-2026 sales data requires adjustment to reflect current market conditions under new legislation.

Step 2: Apply Yield Compression Adjustments

Reduce gross yields by 1-2% to account for:

- Increased void period assumptions

- Rental income volatility

- Enhanced compliance costs

- Extended possession timelines

Step 3: Deduct Compliance Cost Liabilities

Calculate and deduct:

- Decent Homes Standard upgrade costs

- EPC rating improvement expenditure

- Deferred maintenance addressing HHSRS hazards

Step 4: Stress Test Against Lender Criteria

Verify that adjusted valuations support:

- Minimum 145% interest coverage ratios

- Stress tested affordability at 6.5-7% interest rates

- Required loan-to-value ratios for target purchaser profiles

Step 5: Document Adjustment Rationale

Provide detailed justification for all adjustments, referencing specific Act provisions and RICS guidance to support valuation conclusions.

Regional Variations and Market Segmentation

The impact of Valuation Adjustments for Renters' Rights Act 2026: What Property Surveyors Must Factor Into BTL Assessments varies significantly by region and property type:

High-Demand Urban Markets

Properties in London and major cities with strong rental demand may experience less severe valuation impacts (0.5-1% yield compression) due to:

- Shorter void periods despite increased tenant mobility

- Strong rental growth offsetting restriction impacts

- Higher-quality tenant pools reducing possession risk

Lower-Demand Regional Markets

Properties in areas with softer rental demand face more substantial adjustments (1.5-2.5% yield compression) reflecting:

- Extended void periods exacerbated by tenant mobility

- Limited rental growth constraining income projections

- Higher possession risk from challenging tenant circumstances

Property Condition Segmentation

Modern, compliant properties (post-2010 construction) require minimal compliance cost adjustments, while older housing stock (pre-1980) faces substantial deductions for Decent Homes Standard and EPC upgrades.

Surveyors operating across different regions should consult local chartered surveyors familiar with specific market dynamics, such as chartered surveyors in Bromley or chartered surveyors in Kingston for London-specific insights.

Risk Premium Adjustments and Capitalisation Rates

Beyond direct income and cost adjustments, surveyors must recalibrate capitalisation rates (cap rates) to reflect increased investment risk under the new regulatory framework.

Traditional Cap Rate Methodology

Pre-2026, BTL properties typically commanded cap rates of:

- Prime properties: 4-5%

- Secondary properties: 5-6.5%

- Tertiary properties: 6.5-8%

These rates reflected relatively stable regulatory environments with predictable possession mechanisms and limited tenant rights.

Post-2026 Cap Rate Adjustments

The Renters' Rights Act introduces systematic risk factors requiring cap rate increases of 0.5-1.5%:

- Regulatory risk premium: 0.3-0.5% for ongoing legislative uncertainty

- Possession risk premium: 0.2-0.5% for extended court proceedings

- Income volatility premium: 0.2-0.4% for unpredictable tenancy durations

- Compliance risk premium: 0.1-0.3% for evolving standards requirements

These adjustments result in revised cap rates of:

- Prime properties: 4.5-6%

- Secondary properties: 6-7.5%

- Tertiary properties: 7.5-9.5%

Higher cap rates translate directly to lower capital values for identical income streams, reflecting reduced investor appetite for BTL assets under more restrictive regulatory conditions.

Portfolio Valuation Considerations

For landlords with multiple properties, surveyors must consider portfolio-level factors that compound individual property risks:

Concentration Risk

Portfolios concentrated in single regions or property types face amplified exposure to:

- Local market downturns affecting multiple assets simultaneously

- Regional court system backlogs extending possession timelines

- Area-specific compliance requirements (selective licensing schemes)

Operational Complexity

Larger portfolios face increased operational burdens under the Act:

- Enhanced record-keeping requirements across multiple tenancies

- Coordinated compliance upgrades requiring substantial capital deployment

- Professional property management becoming essential rather than optional

Financing Constraints

Portfolio landlords face particularly stringent lender scrutiny [2], with some lenders imposing:

- Maximum portfolio size restrictions

- Enhanced personal income verification requirements

- Cross-collateralisation clauses affecting individual property values

Understanding property management requirements becomes critical for accurate portfolio valuations.

Valuation Reporting Best Practices Under the New Framework

To meet enhanced due diligence requirements and provide defensible valuations, surveyors should adopt comprehensive reporting practices:

Essential Report Components

✅ Regulatory compliance assessment: Document Decent Homes Standard status, EPC rating, and licensing compliance

✅ Void period justification: Provide detailed rationale for void assumptions with reference to local court processing times

✅ Comparable adjustment schedule: Itemise all adjustments applied to comparable properties with specific Act-related factors

✅ Compliance cost schedule: Detail required upgrades with cost estimates and implementation timelines

✅ Lender criteria verification: Confirm valuation supports target ICR and stress test requirements

✅ Risk factor disclosure: Explicitly identify regulatory risks affecting valuation certainty

Liability Management

Given increased valuation complexity, surveyors should:

- Maintain detailed working papers documenting all assumptions

- Obtain specialist advice for complex compliance assessments

- Include appropriate caveats regarding legislative uncertainty

- Recommend periodic revaluations as regulations evolve

- Consider professional indemnity insurance adequacy for expanded scope

Future Legislative Developments to Monitor

The Renters' Rights Act 2026 represents the beginning rather than the end of rental sector reform. Surveyors must monitor ongoing developments:

Awaiting Regulations

Several Act provisions require secondary regulations not yet published:

- Specific Decent Homes Standard criteria and assessment methodologies

- Rent tribunal procedures and market value determination processes

- Landlord database and registration requirements

- Enhanced enforcement mechanisms and penalty structures

Potential Further Reforms

Policy discussions continue around:

- Rent control mechanisms beyond current annual increase limits

- Mandatory landlord licensing expansion to all local authorities

- Enhanced tenant rights to request property modifications

- Stricter energy efficiency requirements beyond 'C' rating

Staying informed through professional bodies like RICS and monitoring new property management laws ensures valuations remain current as the regulatory landscape evolves.

Technology and Data Requirements

Accurate Valuation Adjustments for Renters' Rights Act 2026: What Property Surveyors Must Factor Into BTL Assessments demand enhanced data collection and analysis capabilities:

Essential Data Sources

- Local court processing times: Average possession case durations by jurisdiction

- Regional compliance costs: Area-specific upgrade cost databases

- Rental market dynamics: Tenant turnover rates under new tenancy structures

- Lender criteria: Current ICR requirements and stress test rates by institution

- EPC improvement costs: Technology-specific upgrade cost benchmarks

Analytical Tools

Surveyors should leverage:

- Cash flow modelling software: Incorporating variable void periods and restricted rent increases

- Compliance assessment tools: Decent Homes Standard gap analysis applications

- Energy efficiency calculators: EPC improvement pathway modelling

- Comparable adjustment matrices: Systematic adjustment application for Act-related factors

Conclusion

The Valuation Adjustments for Renters' Rights Act 2026: What Property Surveyors Must Factor Into BTL Assessments represent the most significant recalibration of buy-to-let property valuation methodology in decades. The abolition of Section 21 evictions, introduction of rolling periodic tenancies, and mandatory compliance standards fundamentally alter the risk-return profile of rental property investments.

Property surveyors must now incorporate systematic downward adjustments across multiple valuation components: yield compressions of 1-2%, void period assumptions increasing by 50-100%, compliance cost deductions of £5,000-£25,000 for non-compliant properties, and capitalisation rate increases of 0.5-1.5% to reflect heightened regulatory risk.

Actionable Next Steps for Property Surveyors

-

Update valuation templates to incorporate mandatory Act-related adjustment factors and compliance cost assessments

-

Establish data collection systems for local court processing times, regional compliance costs, and lender criteria changes

-

Develop specialist expertise in Decent Homes Standard assessment and EPC improvement pathway analysis

-

Enhance reporting protocols to document adjustment rationale and manage expanded professional liability

-

Monitor regulatory developments through RICS guidance updates and secondary legislation publications

-

Engage with lenders to understand evolving affordability criteria and stress test requirements

-

Consider specialist training in rental sector legislation and compliance assessment methodologies

For landlords and investors, obtaining professional property valuations that properly account for these legislative changes is now essential for informed decision-making. The regulatory landscape has fundamentally shifted, and property values must reflect this new reality.

The surveyors who master these Valuation Adjustments for Renters' Rights Act 2026 will provide the most accurate, defensible assessments in an increasingly complex market. Those who fail to adapt risk significant professional liability and client dissatisfaction as the gap between traditional valuations and market reality widens.

References

[1] Buy To Let Mortgage Valuations 2026 – https://www.property118.com/buy-to-let-mortgage-valuations-2026/

[2] The Renters Rights Act What 2026 Holds For Landlords Costs And The Impact On Buy To Let Btl Affordability – https://4-most.co.uk/insights/the-renters-rights-act-what-2026-holds-for-landlords-costs-and-the-impact-on-buy-to-let-btl-affordability/

[3] Consideration Of Implications Of Renters Rights Act On Valuation – https://www.rics.org/news-insights/consideration-of-implications-of-renters-rights-act-on-valuation

[4] Property Litigation, Buy-to-Let Strategy & the Renters' Rights Act 2026 – https://www.youtube.com/watch?v=HHwBPDxJlF0

[5] Landlords Guide To The Renters Rights Act 2026 – https://www.freelancerfinancials.co.uk/guides/landlords-guide-to-the-renters-rights-act-2026/

[6] Selling A Rental Property In 2026 How The New Renters Rights Bill Affects You – https://www.gorvinsresidential.com/selling-a-rental-property-in-2026-how-the-new-renters-rights-bill-affects-you/