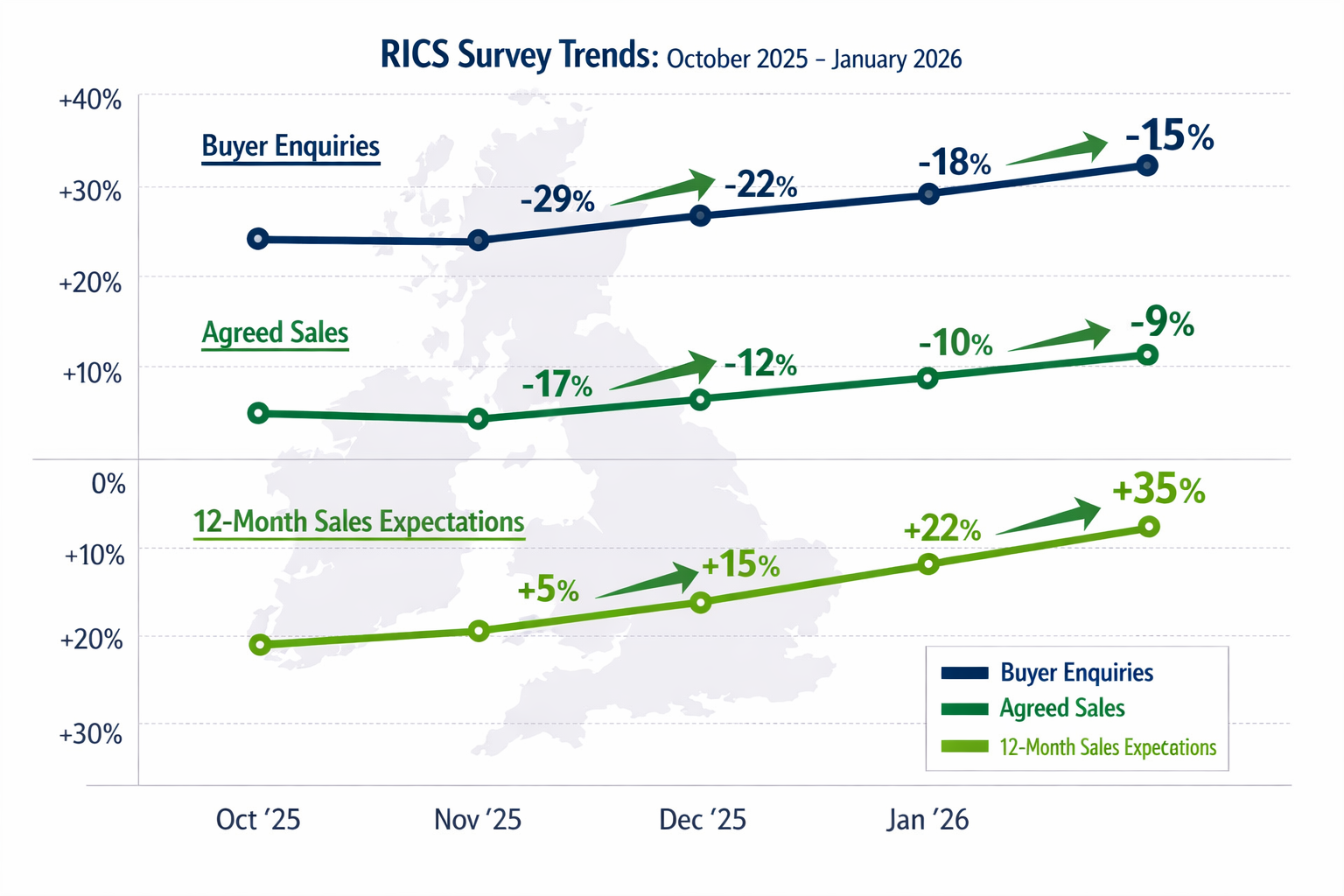

The UK residential property market recorded its first sustained improvement in buyer demand since mid-2025, with new enquiries climbing from -21% to -15% in January 2026—a development that demands immediate recalibration of valuation methodologies. For chartered surveyors navigating this transitional phase, the January 2026 RICS Residential Survey Insights: Valuation Adjustments for Emerging Market Uptick reveal critical inflection points that separate accurate property assessments from outdated assumptions rooted in the prolonged downturn of 2024-2025.

This comprehensive analysis examines how professional valuers must adapt their techniques to capture emerging market dynamics while maintaining rigorous standards during a period of cautious optimism. With twelve-month sales expectations surging to +35%—the strongest conviction since December 2024—understanding these shifts becomes essential for delivering credible valuations that reflect genuine market conditions rather than historical trends [2].

Key Takeaways

- Buyer demand improved significantly in January 2026, with new enquiries reaching -15% (up from -21%), marking the first sustained recovery signal after months of decline

- Sales expectations surged to +35% for the twelve-month outlook, representing the strongest confidence in market recovery since December 2024

- Valuation adjustments must account for momentum shifts, incorporating both near-term caution (-4% three-month price expectations) and long-term optimism (+43% twelve-month price outlook)

- Regional divergence requires localized approaches, with Northern Ireland, Scotland, and various English regions showing distinctly different recovery trajectories

- Rental market strength (+28% near-term price expectations) creates alternative valuation considerations, particularly for investment property assessments

Understanding the January 2026 RICS Residential Survey Context

The Data Behind the Recovery Signal

The Royal Institution of Chartered Surveyors (RICS) UK Residential Market Survey for January 2026 captured responses from property professionals across the United Kingdom during a pivotal moment. The survey revealed three consecutive months of progressively less negative readings for agreed sales, culminating in a -9% net balance—the least pessimistic figure since June 2025 [2].

This improvement didn't emerge in isolation. Several interconnected factors contributed to the shift:

- Stabilizing mortgage rates following the volatility of late 2024

- Improved economic sentiment as inflation pressures moderated

- Seasonal factors typical of early-year property market activity

- Pent-up demand from buyers who delayed decisions during the 2024-2025 downturn

The survey's net balance methodology—calculating the percentage of respondents reporting increases minus those reporting decreases—provides a nuanced view beyond simple transaction volumes. A reading of -15% for new buyer enquiries, while still negative, represents substantial improvement from the -29% recorded in November 2025 [2].

Comparing January 2026 to Historical Patterns

Historical context proves essential for interpreting these figures. The January 2026 readings sit within a broader recovery narrative that contrasts sharply with:

| Metric | January 2026 | October 2025 (Low Point) | Change |

|---|---|---|---|

| New Buyer Enquiries | -15% | -29% | +14 points |

| Agreed Sales | -9% | Not specified | Improving trend |

| House Price Balance | -10% | -19% | +9 points |

| 12-Month Sales Expectations | +35% | Significantly lower | Strong recovery |

This trajectory demonstrates consistent improvement over four consecutive months, suggesting the uptick represents genuine market momentum rather than statistical noise [2].

For chartered surveyors conducting RICS building surveys, these macro trends directly influence valuation approaches, particularly when assessing properties in transitional market conditions.

January 2026 RICS Residential Survey Insights: Key Valuation Adjustment Factors

Price Expectation Divergence: Near-Term vs. Long-Term

One of the most striking features of the January 2026 data involves the significant divergence between near-term and long-term price expectations. While three-month price expectations remained cautiously negative at -4%, the twelve-month outlook surged to +43%—indicating professional surveyors anticipate substantial appreciation over the medium term despite immediate hesitation [2].

This divergence creates specific challenges for valuation work:

For immediate sale valuations, the -4% three-month expectation suggests:

- Conservative comparable selection weighted toward recent transactions

- Downward adjustments for properties requiring extended marketing periods

- Recognition that buyer negotiating power remains relatively strong in Q1 2026

For longer-term assessments (including matrimonial valuations or capital gains purposes), the +43% twelve-month outlook indicates:

- Upward trajectory assumptions for development appraisals

- Enhanced residual land values in areas showing strong recovery signals

- Justification for optimistic growth scenarios in investment valuations

Incorporating Market Momentum into Comparable Analysis

Traditional comparable evidence analysis relies heavily on recent transaction data, typically from the preceding three to six months. However, during periods of rapid market transition—such as the emerging uptick identified in January 2026—this approach risks anchoring valuations to outdated market conditions [1].

Professional surveyors must now implement momentum adjustments by:

- Time-weighting comparable evidence more heavily toward recent transactions (last 30-60 days)

- Applying trend adjustments to older comparables based on documented market improvement

- Segmenting analysis by property type and price bracket, as recovery patterns vary significantly

- Incorporating forward-looking indicators such as the +35% twelve-month sales expectations

For example, a comparable sale from October 2025 (when house price balance stood at -19%) requires upward adjustment when valuing a similar property in January 2026 (with improved -10% balance), particularly if the subject property benefits from characteristics aligned with current buyer preferences [2].

Regional Variation and Localized Adjustments

The January 2026 survey highlighted pronounced regional divergence across the UK market, with Northern Ireland and Scotland showing patterns distinctly different from national trends [2]. This geographic variation demands location-specific valuation approaches.

Regional adjustment considerations include:

- 🏴 London and Southeast England: Showing earlier recovery signals with stronger buyer enquiry improvements

- 🏴 Scotland: Exhibiting different momentum patterns requiring separate comparable pools

- 🏴 Wales: Mid-range recovery with distinct affordability dynamics

- Northern Ireland: Unique market characteristics warranting isolated analysis

For surveyors working across multiple regions—such as those providing services in Central London, West London, or Hertfordshire—applying uniform national trends risks significant valuation errors.

The solution involves maintaining separate regional databases of comparable evidence and tracking local RICS member sentiment through regional survey breakdowns when available.

Practical Valuation Techniques for the Emerging Market Uptick

Adjusting Depreciation Rates and Obsolescence Factors

During market downturns, surveyors typically apply higher depreciation rates to account for reduced buyer willingness to undertake renovation work and tighter mortgage lending on properties requiring improvement. The January 2026 recovery signals suggest recalibrating these assumptions.

Recommended adjustments include:

✅ Reducing functional obsolescence penalties for properties with minor defects, as improving buyer confidence increases willingness to purchase properties requiring cosmetic work

✅ Reassessing location obsolescence factors in areas showing stronger recovery indicators, particularly suburbs benefiting from hybrid working patterns

✅ Moderating depreciation for older building components as buyers demonstrate increased acceptance of renovation projects during recovery phases

However, surveyors must maintain professional skepticism. The January data shows improvement but not yet positive territory for most indicators. Full building surveys remain essential for identifying genuine defects that warrant valuation adjustments regardless of market sentiment [1].

Rental Investment Valuation Adjustments

The rental market component of the January 2026 survey revealed particularly strong signals, with near-term rental price expectations jumping to +28% (from +16% previously) [2]. This creates specific considerations for investment property valuations.

Key rental valuation factors:

- Yield compression expectations: As rental growth outpaces house price growth in the near term, gross yields may appear temporarily elevated

- Tenant demand strength: The +28% expectation reflects genuine demand-supply imbalances favoring landlords

- Constrained supply: Landlord instructions at -24% (though improving from -34%) indicate limited new rental stock [2]

For commercial valuations and residential investment assessments, these factors justify:

- Lower exit yields in discounted cash flow models

- Higher rental growth assumptions for near-term projections (12-18 months)

- Premium valuations for properties with strong rental characteristics (proximity to transport, modern specifications)

Transaction Volume Adjustments and Marketing Period Assumptions

The agreed sales metric improving to -9% (least negative since June 2025) signals gradually improving market liquidity [2]. This directly impacts two critical valuation assumptions:

Marketing period adjustments:

- Properties in high-demand areas: Reduce assumed marketing periods from 16-20 weeks (typical during downturn) to 12-16 weeks

- Standard properties: Maintain moderate assumptions of 14-18 weeks given still-negative sales balance

- Properties requiring significant work: Keep conservative 20-24 week assumptions as buyer caution persists

Liquidity adjustments:

- Reduce illiquidity discounts for unique properties as improving transaction volumes increase buyer pools

- Maintain caution for properties above £1 million, where recovery typically lags

- Consider enhanced marketability for properties aligned with current buyer preferences (home offices, outdoor space, energy efficiency)

When advising clients on how to negotiate house prices down after survey, understanding these liquidity dynamics helps frame realistic negotiation parameters.

Regional Analysis: January 2026 RICS Residential Survey Insights by Location

London Market Dynamics

The London property market demonstrated mixed signals in the January 2026 survey, with prime central areas showing different patterns from outer boroughs. Surveyors operating in locations such as Chelsea, Barnes, and Hampstead reported varying recovery speeds.

Prime central London characteristics:

- Slower recovery due to higher price points and international buyer caution

- Stronger rental market performance supporting investment valuations

- Continued adjustment from 2022-2023 peak pricing

Outer London and commuter zones:

- Faster recovery aligned with national improvement trends

- Sustained demand from hybrid workers seeking space and value

- Stronger buyer enquiry improvements than central areas

Areas like Islington and Hounslow showed particularly strong momentum, benefiting from transport connectivity and relative affordability compared to central zones.

Home Counties and Commuter Belt Performance

The home counties surrounding London—including Hertfordshire, Surrey, and Buckinghamshire—exhibited robust recovery indicators in January 2026. Surveyors in Watford and similar locations reported buyer enquiry improvements exceeding national averages.

Contributing factors include:

- Affordability advantages compared to London proper

- Quality of life considerations driving continued suburban demand

- School catchment areas maintaining property value resilience

- Transport infrastructure supporting commuter flexibility

Valuation adjustments in these areas should reflect the stronger recovery trajectory, with particular attention to properties offering:

- Modern specifications and energy efficiency

- Garden space and home office potential

- Proximity to railway stations with direct London connections

Regional Markets: Scotland, Wales, and Northern Ireland

The January 2026 survey specifically noted regional divergence with Scotland and Northern Ireland showing distinct patterns from English markets [2]. This geographic variation requires surveyors to avoid applying blanket national assumptions.

Scottish market characteristics:

- Different legal framework (Scottish property law) affecting transaction patterns

- Varied recovery speeds between Edinburgh, Glasgow, and regional areas

- Unique buyer behavior patterns requiring separate comparable analysis

Welsh market dynamics:

- Affordability-driven demand from English buyers continuing

- Second-home market considerations affecting certain areas

- Regional economic factors influencing employment and buyer confidence

Northern Ireland specifics:

- Distinct market cycles historically less correlated with UK mainland

- Different mortgage market dynamics

- Separate comparable evidence pools essential

For comprehensive property valuations, surveyors must maintain regional expertise and avoid extrapolating trends across borders.

Risk Factors and Cautionary Considerations

The March 2026 Reversal: Lessons for Valuation Caution

While the January 2026 data showed encouraging recovery signals, subsequent market developments demonstrated the fragility of the emerging uptick. The March 2026 RICS survey revealed a sharp reversal, with new buyer enquiries collapsing to -39%—the weakest reading since August 2023 [3].

This dramatic shift, attributed to geopolitical pressures and rising borrowing costs, provides critical lessons for valuation practice:

⚠️ Avoid over-optimistic momentum extrapolation: The January improvement proved temporary, highlighting the danger of assuming linear recovery trajectories

⚠️ Maintain conservative base assumptions: Even when data shows improvement, prudent valuations should incorporate scenario analysis and downside risks

⚠️ Monitor leading indicators continuously: The shift from January optimism to March pessimism occurred rapidly, requiring ongoing market intelligence

⚠️ Document assumption sensitivity: Valuation reports should clearly articulate how different market scenarios would impact assessed values

The March reversal—with agreed sales falling to -34% and near-term sales expectations turning sharply pessimistic at -33%—underscores that the January uptick represented a tentative improvement rather than confirmed recovery [3].

Interest Rate Sensitivity and Mortgage Market Impacts

The January 2026 market improvement occurred during a period of relative mortgage rate stability. However, the subsequent deterioration in March coincided with renewed borrowing cost pressures, demonstrating the critical linkage between financing conditions and market momentum [3].

Valuation adjustments must account for interest rate sensitivity:

- High loan-to-value scenarios: Properties typically purchased with 90-95% mortgages show greater price sensitivity to rate changes

- Remortgage pressures: Areas with high concentrations of fixed-rate mortgages expiring in 2026 face increased selling pressure

- Affordability constraints: First-time buyer segments demonstrate highest sensitivity to monthly payment changes

When conducting valuations for lending purposes, surveyors should consider documenting the interest rate assumptions underlying market activity and how alternative rate scenarios might impact property values.

Supply-Demand Imbalances and Inventory Levels

The January 2026 survey showed new property listings remaining constrained, with many homeowners reluctant to sell during uncertain conditions. This supply constraint provides a floor for property values even as demand fluctuates [2].

However, surveyors must consider potential supply dynamics:

- Forced sales risk: Economic pressures could trigger increased distressed selling

- New build completions: Developments initiated during stronger market conditions reaching completion

- Landlord exits: Continued regulatory pressures potentially increasing rental property sales

The rental market's constrained landlord instructions (-24%) combined with strong rental price expectations (+28%) creates a bifurcated market dynamic where rental investment properties may warrant different valuation approaches than owner-occupied equivalents [2].

Professional Standards and Reporting Considerations

RICS Red Book Compliance During Market Transitions

The RICS Valuation – Global Standards (Red Book) establishes mandatory requirements for valuation practice, with specific considerations during transitional market periods. The January 2026 market conditions trigger several key compliance areas:

Market uncertainty disclosures:

- VPS 3 requires valuers to report material uncertainty when market evidence is limited or conflicting

- The divergence between near-term caution and long-term optimism may warrant uncertainty language

- Clear documentation of assumptions becomes critical during transition periods

Comparable evidence standards:

- Sufficient quantum of recent, relevant transactions required

- Time adjustments to older comparables must be clearly explained and justified

- Regional variations must be explicitly addressed in valuation reasoning

Assumptions and special assumptions:

- Marketing period assumptions require clear justification

- Any departure from standard assumptions must be explicitly stated

- Scenario analysis may be appropriate for complex instructions

For detailed guidance on survey types and their valuation implications, surveyors should reference resources on which building survey is needed for specific property circumstances.

Communicating Uncertainty to Clients

The January 2026 data's mix of positive signals (improving enquiries, strong long-term expectations) and continued challenges (still-negative near-term readings) creates communication challenges when explaining valuations to clients.

Best practices include:

📋 Scenario presentation: Provide base, optimistic, and pessimistic valuation scenarios with clearly stated assumptions for each

📋 Trend contextualization: Explain how the January improvement fits within broader market cycles and subsequent developments

📋 Regional specificity: Avoid generic national statements when local market conditions diverge significantly

📋 Assumption transparency: Clearly document all key assumptions regarding market direction, comparable adjustments, and timing

📋 Update mechanisms: For valuations with extended validity periods, establish triggers for review if market conditions change materially

When preparing reports for Level 3 building surveys, the valuation component should reflect these communication principles while maintaining professional objectivity.

Documentation and Audit Trail Requirements

Professional indemnity considerations during transitional markets demand enhanced documentation of valuation reasoning. The January 2026 uptick, followed by March 2026 reversal, illustrates how market conditions can shift rapidly, potentially leading to valuation challenges.

Essential documentation includes:

- Comparable evidence files: Complete records of all transactions considered, including those rejected and reasons for exclusion

- Adjustment calculations: Detailed working papers showing how time, condition, location, and other adjustments were derived

- Market intelligence: Contemporaneous notes from RICS surveys, local agent feedback, and market reports

- Assumption justification: Clear reasoning for marketing periods, depreciation rates, and other key assumptions

- Client communications: Records of discussions regarding market conditions and valuation uncertainty

This documentation proves essential if valuations are subsequently questioned, particularly if market conditions deteriorate as they did between January and March 2026 [3].

Conclusion: Navigating Valuation Practice in Transitional Markets

The January 2026 RICS Residential Survey Insights: Valuation Adjustments for Emerging Market Uptick reveal a property market at a critical inflection point. With buyer enquiries improving to -15%, agreed sales reaching their least negative reading since mid-2025 at -9%, and twelve-month sales expectations surging to +35%, the data presented genuine signals of recovery momentum [2].

However, the subsequent March 2026 reversal—with enquiries collapsing to -39% and sales expectations turning sharply negative—demonstrates the fragility of the emerging uptick and the dangers of over-optimistic extrapolation [3]. For chartered surveyors, this volatility underscores the critical importance of:

✅ Balanced assessment: Incorporating both recovery signals and persistent risks into valuation reasoning

✅ Regional specificity: Recognizing that national trends mask significant geographic variation requiring localized analysis

✅ Assumption transparency: Clearly documenting the market conditions and expectations underlying valuations

✅ Continuous monitoring: Maintaining ongoing market intelligence rather than relying on point-in-time survey data

✅ Professional skepticism: Avoiding momentum-driven optimism while recognizing genuine improvement signals

Actionable Next Steps for Surveyors

To effectively navigate the current market environment, professional surveyors should:

- Review comparable evidence protocols to ensure time adjustments reflect documented market momentum changes

- Establish regional market intelligence systems tracking local RICS member sentiment and transaction patterns

- Enhance valuation report templates to better communicate uncertainty and assumption sensitivity

- Develop scenario analysis frameworks for complex instructions where market direction significantly impacts value

- Maintain continuous professional development on market analysis techniques and Red Book compliance during transitional periods

For property professionals seeking comprehensive survey services that incorporate these sophisticated valuation approaches, understanding how long building surveys take and what questions to ask during surveys helps ensure thorough property assessments.

The January 2026 data ultimately represents neither definitive recovery nor continued decline, but rather a transitional moment requiring enhanced professional judgment, rigorous methodology, and clear communication. Surveyors who successfully navigate this complexity—balancing optimism with caution, incorporating regional nuance, and maintaining documentation standards—will deliver valuations that withstand scrutiny regardless of subsequent market developments.

As the UK residential property market continues evolving through 2026, the professional surveyor's role becomes increasingly critical in separating genuine market signals from statistical noise, ensuring clients receive accurate, defensible property valuations grounded in comprehensive analysis rather than simplistic trend extrapolation.

References

[1] Valuation Strategies Amid January 2026 Rics Residential Survey Spotting Early Market Recovery Signals – https://nottinghillsurveyors.com/blog/valuation-strategies-amid-january-2026-rics-residential-survey-spotting-early-market-recovery-signals

[2] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[3] Uk Residential Market Survey March 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey-March-2026.pdf