The 2026 Budget has sent shockwaves through the prime property market. With a new council tax surcharge targeting homes valued at £2 million or more, property owners across London and the South East face unprecedented challenges. The question on everyone's mind: how can professional surveyor strategies help navigate these Valuation Adjustments for Budget 2026 Tax Hits on High-Value Properties: Surveyor Strategies Over £2M Threshold while maintaining accurate, defensible property values?

The stakes couldn't be higher. Properties teetering just above the threshold face annual charges starting at £2,500, while the broader implications threaten to reshape the entire high-value property landscape. For homeowners, investors, and property professionals, understanding RICS-compliant valuation methodologies has become essential to managing this new fiscal reality.

Key Takeaways

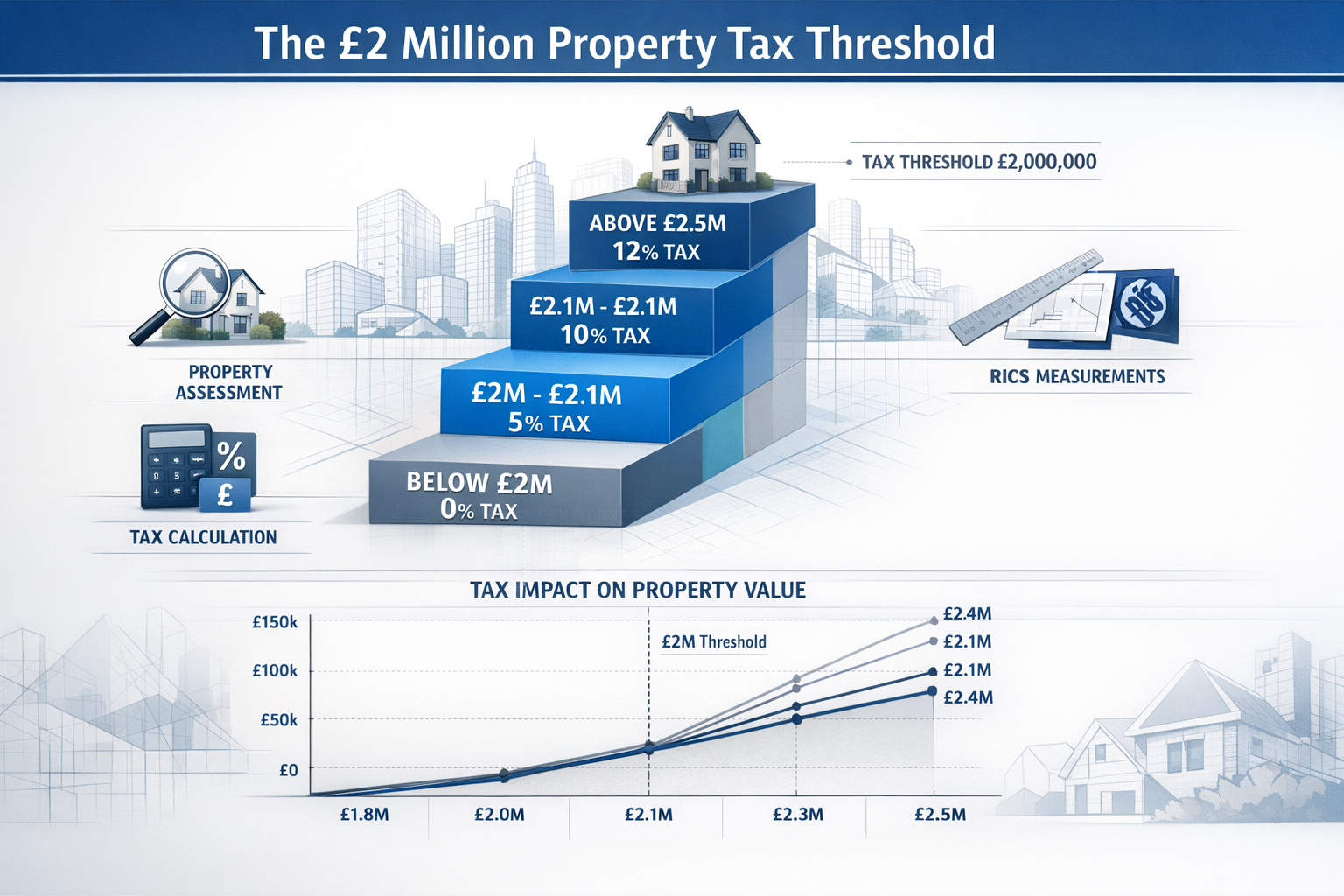

- 🏛️ New surcharge applies from April 2028 to properties valued at £2 million or more, with four distinct bands charging between £2,500 and £7,500 annually

- 📊 Strategic valuations matter: RICS-compliant methodologies can provide defensible assessments that accurately reflect market conditions and property-specific factors

- 💷 Market distortion expected: The Office for Budget Responsibility predicts "bunching" of sales just below thresholds, with properties near £2 million potentially adjusting valuations downward

- 🔍 Mandatory revaluations every five years by the Valuation Office Agency, with appeals deadline of 31 March 2026 for current rateable values

- 🎯 Professional surveyor strategies including comparative market analysis, property condition assessments, and timing considerations can help property owners navigate the new tax landscape

Understanding the £2 Million Threshold and Tax Structure

The council tax surcharge represents a fundamental shift in how high-value properties are taxed in England. Effective from April 2028, this new levy targets homes valued at £2 million or more, collected alongside standard council tax payments.[1][7]

The Four-Band Structure

The government has established a tiered system designed to increase charges proportionally with property values:

| Property Value Band | Annual Surcharge | Example Properties |

|---|---|---|

| £2M – £2.5M | £2,500 | Large family homes in prime suburbs |

| £2.5M – £3M | £5,000 | Luxury townhouses in desirable areas |

| £3M – £5M | £6,250 | Period properties in premium locations |

| £5M+ | £7,500 | Mansions and exceptional estates |

These amounts will be uprated annually by CPI inflation, meaning the burden will grow over time.[1][2] The Treasury projects this surcharge will raise approximately £400 million in revenue.[1]

Valuation Office Agency Methodology

The Valuation Office Agency will conduct a targeted valuation exercise to identify properties above the £2 million threshold. This represents a significant departure from traditional council tax banding, which hasn't been comprehensively updated since 1991. The agency will conduct mandatory revaluations every five years, creating ongoing uncertainty for property owners near the threshold.[1]

A public consultation on implementation details is scheduled for early 2026, providing a critical window for industry professionals and property owners to influence the final methodology.[1]

Market Impact and the Bunching Effect on Valuation Adjustments for Budget 2026 Tax Hits on High-Value Properties

The introduction of arbitrary tax thresholds creates predictable market distortions that professional surveyors must understand and account for in their valuations.

The £1.99 Million Phenomenon

The Office for Budget Responsibility has already recognized that the new surcharge will cause "bunching of sales just below the thresholds."[1] This isn't mere speculation—it's an established economic principle that tax cliffs create artificial price clustering.

For properties currently valued between £1.95 million and £2.05 million, sellers face a stark choice: price at £2 million and burden buyers with an additional £2,500 annual charge, or price at £1.99 million and avoid the surcharge entirely. The rational response is obvious, and the market will adjust accordingly.

"Who would want to purchase a £2 million house when facing the additional annual charge?" — Estate agents' fundamental concern about market liquidity[1]

Investment Freeze Risk

Industry experts have warned that the tax could "freeze investment in homes over £1 million overnight."[1] Property owners who might otherwise invest in improvements face a perverse incentive: any enhancement that pushes their property value above the £2 million threshold triggers the annual surcharge.

This creates a chilling effect on property maintenance and improvement, particularly for homes currently valued between £1.8 million and £2 million. Owners may deliberately defer necessary renovations to avoid crossing the threshold—a decision that ultimately damages property quality and market vitality.

Volatility in Prime Market Valuations

Jackson-Stops chairman Nick Leeming highlights a critical challenge: property values just above the threshold may adjust significantly in response to the tax, making government valuations difficult during short-term market fluctuations.[1] This volatility creates both risks and opportunities for property owners who engage professional valuation services.

The prime London and South East markets are particularly susceptible to these pressures. Post-budget forecasts indicate potential slowdowns in these traditionally robust markets as buyers and sellers recalibrate expectations around the new tax reality.

RICS-Compliant Surveyor Strategies for Valuation Adjustments for Budget 2026 Tax Hits on High-Value Properties: Surveyor Strategies Over £2M Threshold

Professional chartered surveyors employ sophisticated methodologies to ensure valuations are both accurate and defensible. For properties near the £2 million threshold, these strategies become critical.

Comparative Market Analysis (CMA) Refinement

Traditional CMA approaches must be refined to account for the new tax landscape. Surveyors should:

- Identify true comparables that reflect post-announcement market conditions

- Adjust for tax impact by considering whether comparable sales occurred before or after the Budget announcement

- Account for bunching effects by recognizing that properties just below £2 million may be artificially suppressed

- Document methodology thoroughly to support valuations during appeals or disputes

Professional surveyors working in areas like Hampstead, Islington, and Chiswick must be particularly vigilant, as these prime London locations contain high concentrations of properties near the threshold.

Property-Specific Condition Assessments

Detailed condition assessments become more valuable when valuations have significant tax implications. A comprehensive Level 3 Full Building Survey can identify factors that legitimately reduce property value:

- Structural issues requiring significant remediation

- Deferred maintenance that impacts market appeal

- Environmental concerns affecting property desirability

- Building problems that require immediate attention

These assessments provide objective evidence supporting lower valuations when appropriate, while maintaining professional integrity and RICS Red Book compliance.

Timing Considerations and Strategic Valuation Dates

The timing of valuations has always mattered, but the new surcharge elevates this consideration to critical importance:

Before April 2028: Property owners have a window to establish baseline valuations before the surcharge takes effect. These pre-implementation valuations may serve as reference points for future appeals.

Appeal Deadline: Ratepayers must submit requests for changes to their rateable value before 31 March 2026.[4] This approaching deadline creates urgency for property owners who believe their current assessments are too high.

Five-Year Revaluation Cycle: Understanding that mandatory revaluations occur every five years allows property owners to plan strategically around improvement projects and market timing.

Specialized Valuation Approaches for Different Property Types

Different property categories require tailored approaches:

Period Properties: Historic homes in areas like Guildford and Weybridge may have unique characteristics that affect valuation. Conservation restrictions, listed building status, and maintenance requirements can legitimately reduce market value.

Development Opportunities: Properties with development potential require careful consideration of whether to value as existing use or development opportunity, as this distinction can significantly impact threshold calculations.

Commercial Elements: Properties with commercial components may benefit from different valuation methodologies that appropriately segment residential and commercial values.

Cash Flow and Affordability Challenges for High-Value Property Owners

The new surcharge creates genuine hardship for certain property owner categories, making professional valuation strategies even more important.

Asset-Rich, Cash-Poor Retirees

Many retired homeowners who benefited from decades of house price inflation find themselves living in properties now valued above £2 million, despite not being "cash-rich."[1] These owners face difficult decisions:

- Can they afford the ongoing upkeep plus the new annual surcharge?

- Should they downsize, triggering stamp duty and moving costs?

- How can they challenge valuations that seem inflated relative to their property's actual condition?

Professional surveyors can help these owners by conducting thorough assessments that accurately reflect any factors reducing market value, potentially keeping properties below the threshold.

Mortgage-Holding Property Owners

Contrary to assumptions about high-value property owners, many remain "stretched, still paying big mortgages," having simply benefited from rising prices.[1] For these owners, an additional £2,500 to £7,500 annual charge represents a significant burden.

Strategic timing of improvements, careful monitoring of market conditions, and professional valuations that accurately reflect property condition become essential financial planning tools.

Liquidity Concerns in the Prime Market

The fundamental question raised by estate agents—"who would want to purchase a £2 million house" with the additional charge[1]—points to a potential liquidity crisis in the prime market. Properties just above the threshold may become harder to sell, creating a two-tier market with clear winners and losers.

Surveyors working with sellers in this position should provide realistic market assessments that account for reduced buyer appetite, potentially supporting lower asking prices that keep properties below the threshold.

Preparing for the 2026 Revaluation: Actionable Steps

With the appeal deadline of 31 March 2026 approaching[4] and the public consultation scheduled for early 2026[1], property owners should take immediate action.

Immediate Actions (Q1 2026)

✅ Commission a professional valuation from a RICS-qualified surveyor familiar with the new tax implications

✅ Document property condition through comprehensive surveys that identify any factors reducing value

✅ Review comparable sales in your area to understand how the market is responding to the Budget announcement

✅ Participate in the public consultation to influence implementation details

✅ Consider strategic improvements that enhance property value without pushing it above the threshold

Medium-Term Planning (2026-2028)

📋 Monitor market trends in your specific location, particularly if you're in high-value areas like Berkshire, Sussex, or Hampshire

📋 Maintain detailed records of all property maintenance, repairs, and improvements with associated costs

📋 Engage with professional advisors including surveyors, tax specialists, and financial planners

📋 Review property insurance to ensure adequate coverage that reflects accurate valuations

📋 Plan major improvements strategically considering timing relative to the April 2028 implementation date

Long-Term Strategies (Post-2028)

🎯 Prepare for five-year revaluation cycles with ongoing property condition monitoring

🎯 Build relationships with qualified surveyors who understand your property and local market

🎯 Stay informed about market conditions and comparable sales in your area

🎯 Consider portfolio restructuring if you own multiple high-value properties

🎯 Maintain appeal-ready documentation including professional valuations, condition reports, and comparable sales data

Regional Considerations Across the South East

The impact of the £2 million threshold varies significantly by location, requiring region-specific surveyor strategies.

Prime London Boroughs

Areas like Camden, Hampstead, and Islington contain high concentrations of properties near or above the threshold. In these locations:

- Market liquidity concerns are most acute

- Bunching effects will be most pronounced

- Professional valuation expertise is essential

- Comparable sales data requires careful interpretation

Commuter Belt Locations

Towns like Guildford, Epsom, and Weybridge see fewer properties above the threshold, but those that exist often represent family homes rather than investment properties:

- Owner-occupiers may have stronger emotional attachments

- Downsizing decisions become more complex

- Local market knowledge becomes critical for accurate valuations

Outer Regions

Areas like Essex, Berkshire, and Sussex have fewer affected properties, but those that exist often have unique characteristics:

- Larger plots and land values become significant factors

- Period properties and estates require specialized valuation approaches

- Development potential may significantly impact valuations

Working with Professional Surveyors: What to Expect

Engaging a qualified chartered surveyor for valuation work related to the new surcharge should follow a structured process.

Initial Consultation

A professional surveyor will:

- Review your property's current estimated value

- Discuss your specific concerns about the threshold

- Explain relevant valuation methodologies

- Outline the scope of work required

- Provide transparent fee structures

Understanding why property owners hire surveyors helps set appropriate expectations for the engagement.

Inspection and Assessment

The surveyor will conduct a thorough property inspection, documenting:

- Overall condition and maintenance status

- Structural integrity and any defects

- Quality of fixtures, fittings, and finishes

- Unique features that affect value

- Comparable properties in the area

This process mirrors aspects of a full building survey but focuses specifically on factors affecting market value.

Valuation Report

The final report should include:

- Executive summary with clear valuation conclusion

- Methodology explanation demonstrating RICS compliance

- Comparable evidence supporting the valuation

- Property-specific factors affecting value

- Market context including post-Budget trends

- Photographic evidence documenting condition

- Professional opinion on threshold implications

This documentation becomes invaluable if you need to challenge a Valuation Office Agency assessment or support an appeal.

Alternative Strategies: Beyond Valuation

While accurate valuations form the cornerstone of managing the new surcharge, property owners should consider complementary strategies.

Portfolio Restructuring

For owners of multiple properties, strategic restructuring might involve:

- Selling properties just above the threshold

- Acquiring properties below the threshold

- Consolidating holdings to optimize tax efficiency

- Considering alternative investment vehicles

Property Improvement Timing

Strategic timing of improvements can help manage threshold risk:

- Defer major renovations until after establishing baseline valuations

- Complete necessary maintenance that doesn't significantly increase value

- Consider reversible improvements that can be removed if needed

- Document all work to support future valuation adjustments

Financial Planning Integration

The surcharge should be integrated into broader financial planning:

- Estate planning considerations

- Inheritance tax implications

- Cash flow management

- Insurance adequacy reviews

Conclusion

The Valuation Adjustments for Budget 2026 Tax Hits on High-Value Properties: Surveyor Strategies Over £2M Threshold represent a significant challenge for property owners across England, particularly in prime London and South East locations. With the surcharge taking effect in April 2028 and the appeal deadline of 31 March 2026 rapidly approaching, immediate action is essential.

Professional RICS-compliant valuation strategies offer property owners the best defense against excessive tax burdens. By engaging qualified chartered surveyors who understand the new tax landscape, property owners can ensure their valuations accurately reflect market conditions, property-specific factors, and the bunching effects already emerging in the market.

The key to success lies in proactive planning: commissioning professional valuations now, documenting property conditions thoroughly, monitoring market trends carefully, and preparing appeal-ready evidence before the Valuation Office Agency conducts its targeted assessment exercise.

Next Steps

Take action today:

- Schedule a professional valuation with a RICS-qualified surveyor before the 31 March 2026 deadline

- Participate in the early 2026 public consultation to influence implementation details

- Review your property portfolio for threshold exposure and restructuring opportunities

- Engage financial advisors to integrate the surcharge into your broader financial planning

- Monitor market conditions in your specific location to understand emerging trends

The £2 million threshold may seem arbitrary, but its impact will be real and lasting. Property owners who engage professional surveyor expertise now will be best positioned to navigate this new fiscal landscape, potentially saving thousands of pounds annually while maintaining accurate, defensible property valuations.

Don't wait until April 2028 to address these challenges. The time to act is now, while opportunities remain to influence valuations, participate in consultations, and implement strategic responses to this significant change in property taxation.

References

[1] Mansion Tax What Does Rachel Reevess New Property Tax For Expensive Houses Mean For You – https://moneyweek.com/personal-finance/tax/mansion-tax-what-does-rachel-reevess-new-property-tax-for-expensive-houses-mean-for-you

[2] Are You Ready For The 2026 Revaluation – https://bcconsultancy.co.uk/are-you-ready-for-the-2026-revaluation/

[4] What Is Revaluation – https://www.angliarevenues.gov.uk/services/businessrates/what-is-revaluation/

[7] New Property Tax – https://hoa.org.uk/news/new-property-tax/