The UK housing market stands at a critical juncture in 2026. After months of uncertainty, the Royal Institution of Chartered Surveyors (RICS) Q1 2026 survey data reveals a fascinating paradox: house prices are stabilizing at -10% net balance, yet surveyors report +43% of respondents expecting higher prices within twelve months. This dramatic contrast between current subdued momentum and optimistic forward projections creates unique challenges for property professionals conducting accurate valuations. Understanding how to apply Valuation Techniques for Stabilizing House Prices: Applying RICS Q1 2026 Survey for Accurate National Assessments has never been more critical for chartered surveyors, property investors, and homeowners navigating this complex landscape.

Key Takeaways

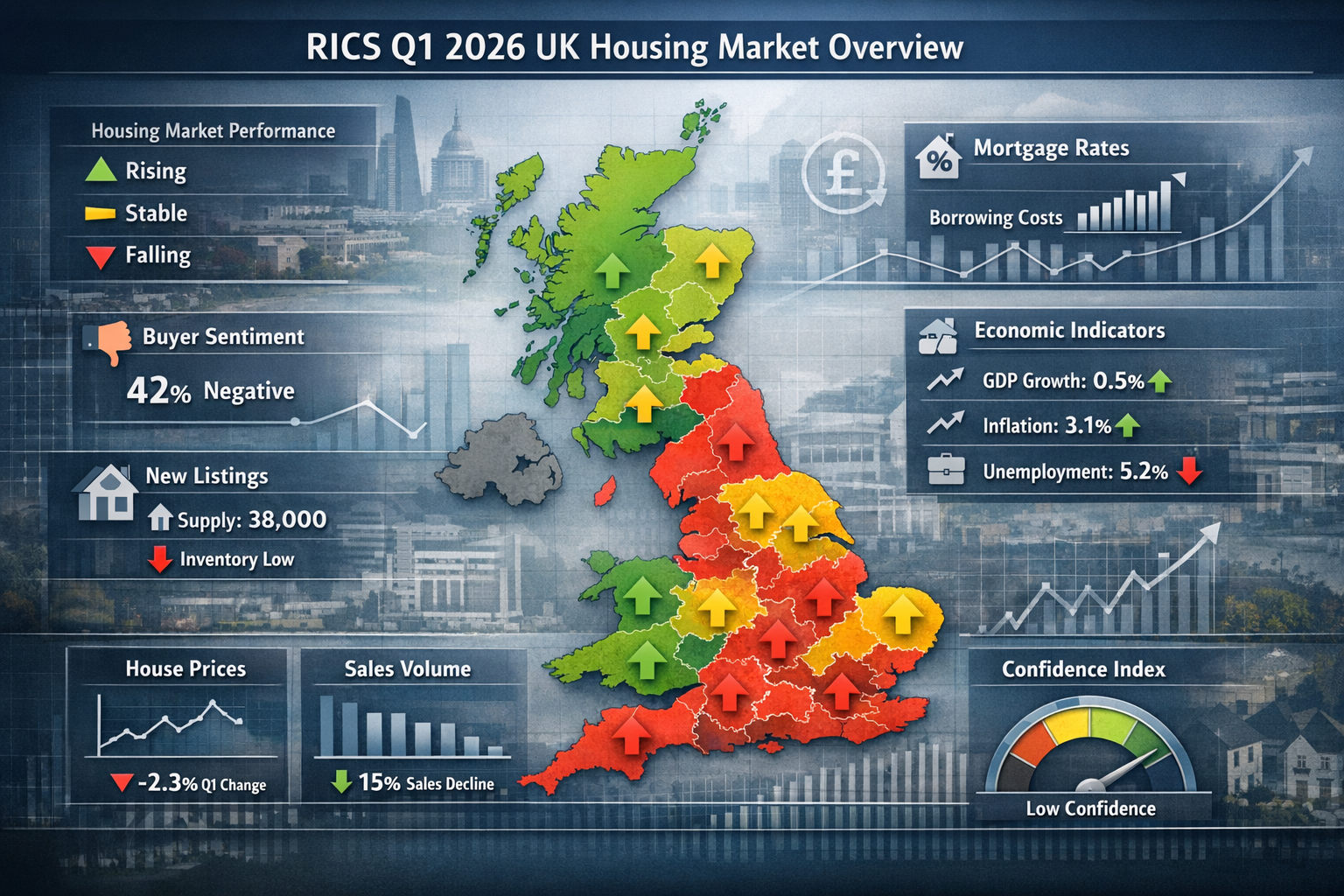

- 📊 House price net balance improved from -19% in October 2025 to -10% in January 2026, indicating stabilization, though it weakened slightly to -12% in February 2026

- 🔮 Forward-looking optimism remains strong with +43% of surveyors expecting price rises over 12 months in January (moderating to +33% in February)

- 🗺️ Regional divergence is widening dramatically, with Northern England showing positive momentum while London (-40%) and South East (-24%) face significant downward pressure

- 🏠 Buyer demand is recovering gradually, with new enquiries improving from -29% in November to -15% in January 2026

- 📈 Rental market tightness continues with tenant demand at +2% and landlord instructions at -27%, supporting continued rental price growth expectations of +20%

Understanding the RICS Q1 2026 Market Context

The first quarter of 2026 presented property professionals with a complex valuation environment characterized by stabilization signals mixed with persistent economic headwinds. The RICS UK Residential Survey data from January and February 2026 provides crucial insights for surveyors seeking to apply accurate valuation techniques during this transitional period [1][3].

The Stabilization Narrative

House price indicators showed meaningful improvement during Q1 2026. The headline house price net balance—which measures the proportion of surveyors reporting price increases minus those reporting decreases—reached -10% in January 2026, a substantial improvement from the -19% recorded in October 2025 [1]. This represented the least negative reading in several months, suggesting that the downward pressure on prices was beginning to ease across the national market.

However, this stabilization proved fragile. By February 2026, the net balance had weakened slightly to -12%, reflecting renewed concerns about interest rates and broader macroeconomic uncertainty [3]. This volatility underscores the importance of applying robust valuation techniques that can account for short-term market fluctuations while identifying longer-term trends.

Transaction Activity Recovery

Beyond price movements, transaction metrics revealed encouraging signs of market recovery. Agreed sales reached -9% in January 2026, marking the least negative reading since June 2025 [1]. This improvement in transaction activity suggests that buyers and sellers were beginning to find common ground on pricing, even as broader economic concerns persisted.

New buyer enquiries showed similar improvement, with the net balance rising to -15% in January, up from -21% in December 2025 and -29% in November 2025 [1]. This gradual recovery in demand provides important context for surveyors conducting matrimonial valuations or other time-sensitive property assessments.

The Expectation-Reality Gap

Perhaps the most striking feature of Q1 2026 data was the significant gap between current market conditions and future expectations. While current price indicators remained in negative territory, +43% of respondents in January anticipated higher prices over the following twelve months—the most positive outlook since February 2025 [1].

This optimism moderated somewhat to +33% in February as renewed economic uncertainty took hold [3]. The RICS Head of Market Research noted that mortgage rates were likely to remain higher for longer than previously anticipated, tempering the earlier enthusiasm [3].

For property professionals, this expectation-reality gap creates a critical challenge: how should current valuations reflect forward-looking optimism while remaining grounded in present market conditions? This question lies at the heart of applying effective Valuation Techniques for Stabilizing House Prices: Applying RICS Q1 2026 Survey for Accurate National Assessments.

Core Valuation Methodologies for Q1 2026 Market Conditions

Applying accurate valuation techniques during periods of market stabilization requires a sophisticated understanding of multiple methodologies and their appropriate application contexts. The RICS Q1 2026 survey data highlights the need for surveyors to adapt traditional approaches to account for regional divergence, expectation gaps, and transaction activity patterns.

Comparative Market Analysis (CMA) Adjustments

The comparative market analysis remains the foundation of residential property valuation, but Q1 2026 conditions demand careful adjustment protocols. Traditional CMA relies on recent comparable sales, but the improving transaction activity from -9% agreed sales in January creates specific challenges [1].

Time-based adjustments become critical when comparable sales occurred during different market phases. A property sold in November 2025 (when buyer enquiries stood at -29%) requires different weighting than one sold in January 2026 (when enquiries had improved to -15%) [1]. Surveyors should apply:

- Recency weighting factors that prioritize transactions from the past 60 days

- Market momentum adjustments reflecting the improving net balance trajectory

- Regional performance overlays accounting for geographic price divergence

The widening regional gap revealed in the RICS February 2026 data makes geographic comparables particularly important. Properties in Northern England, which showed positive momentum throughout Q1, require fundamentally different comparable selection criteria than those in London, where the net balance stood at -40% [3][7].

Income Capitalization Approach for Rental Properties

The rental market dynamics revealed in Q1 2026 data provide crucial inputs for income-based valuation methods. With tenant demand improving to +2% in February and landlord instructions remaining firmly negative at -27%, rental price growth expectations stood at +20% [3].

For capital gains assessments and investment property valuations, surveyors should incorporate:

- Rental yield premium adjustments reflecting the tight supply-demand balance

- Vacancy risk discounting based on positive tenant demand indicators

- Capitalization rate adjustments accounting for interest rate expectations

The persistent shortage of rental supply creates upward pressure on rental values, which in turn supports property valuations through income capitalization methods. However, surveyors must balance this against the higher-for-longer interest rate environment noted by RICS researchers [3].

Cost Approach Considerations

The cost approach—which estimates value based on land value plus construction costs minus depreciation—provides a useful reality check during periods of market uncertainty. Q1 2026 construction cost trends, combined with the stabilizing house price indicators, create specific application contexts.

This methodology proves particularly valuable for:

- New build properties where comparable sales may be limited

- Inheritance tax valuations requiring defensible methodology

- Unique properties where market comparables are scarce

The cost approach also helps surveyors identify situations where market values have fallen below replacement cost—a scenario that may occur in the heavily pressured London and South East markets where net balances stood at -40% and -24% respectively [3].

Reconciliation and Weighting Strategies

Professional surveyors rarely rely on a single valuation methodology. Instead, they apply multiple approaches and reconcile the results through weighted averaging. During Q1 2026's stabilization phase, appropriate weighting depends on:

- Property type and location (with greater CMA weighting for standard properties in active markets)

- Transaction activity levels (higher CMA weighting where agreed sales are improving)

- Client requirements (with income approach prioritized for investment decisions)

For properties in regions showing positive momentum like Northern England, CMA might receive 70-80% weighting. Conversely, in heavily pressured markets like London, a more balanced approach incorporating all three methodologies provides greater reliability [7].

Regional Divergence and Geographic Valuation Adjustments

The RICS Q1 2026 survey data reveals one of the most significant regional divergences in recent UK housing market history. This geographic variation demands location-specific valuation techniques that go far beyond simple comparable selection.

Northern England's Outperformance

Northern England emerged as the standout performer during Q1 2026, with respondents consistently reporting prices moving higher across the region [7]. This positive momentum contrasts sharply with the national picture and creates specific valuation considerations for surveyors working in Manchester, Liverpool, Leeds, and surrounding areas.

The sustained positive performance in Northern England reflects several structural factors:

- Affordability advantages compared to southern regions

- Economic regeneration in major northern cities

- Migration patterns with buyers relocating from higher-cost areas

- Infrastructure investment improving regional connectivity

Surveyors conducting valuations in Northern England should apply positive momentum adjustments to comparable sales, recognizing that properties are likely appreciating between comparable sale dates and valuation dates. This contrasts with the negative adjustments appropriate in declining markets.

London and South East Pressure Points

The capital and surrounding regions faced severe downward pressure during Q1 2026. London's net balance stood at -40% in February, while the South East recorded -24% and East Anglia -26% [3]. These figures represent some of the most negative regional readings in the entire RICS survey.

This weakness reflects multiple headwinds:

- Affordability constraints exacerbated by higher mortgage rates

- Economic uncertainty affecting higher-value markets disproportionately

- Stamp duty impacts on premium property segments

- Remote work patterns reducing London's location premium

For surveyors working with chartered surveyors in Hampstead, Chelsea, or Fulham, these conditions demand conservative valuation approaches that:

- Prioritize very recent comparables (within 30 days where possible)

- Apply downward time adjustments to older comparable sales

- Incorporate market condition clauses in valuation reports

- Document regional underperformance relative to national trends

Scotland and Northern Ireland Resilience

Scotland and Northern Ireland joined Northern England in showing relatively firm price trends during Q1 2026 [3]. This resilience provides important context for understanding the national stabilization narrative—the -10% to -12% national net balance masks significant regional variation.

Surveyors working in these regions should recognize that local market conditions may be substantially stronger than national headlines suggest. This affects:

- Comparable selection criteria (avoiding over-reliance on national trend data)

- Marketing time estimates (properties may sell faster than national averages)

- Price negotiation dynamics (sellers may have stronger bargaining positions)

Applying Geographic Risk Premiums

The widening regional divergence revealed in Q1 2026 data suggests that surveyors should incorporate geographic risk premiums into their valuation frameworks. Properties in heavily pressured markets like London carry greater uncertainty about future value trajectories, which may justify more conservative valuation conclusions.

Conversely, properties in outperforming regions may warrant less conservative approaches, though surveyors must always balance regional optimism against the possibility of mean reversion over longer time horizons.

For professionals seeking expertise across multiple regions, working with firms offering coverage from chartered surveyors in North London to chartered surveyors in Hampshire ensures access to region-specific market intelligence.

Integrating Forward Expectations into Current Valuations

The dramatic gap between current market conditions and future expectations presents one of the most challenging aspects of applying Valuation Techniques for Stabilizing House Prices: Applying RICS Q1 2026 Survey for Accurate National Assessments. With +43% of surveyors expecting higher prices within twelve months (moderating to +33% in February), how should current valuations reflect this optimism? [1][3]

The Expectation Premium Debate

Traditional valuation theory holds that property values reflect current market conditions rather than future expectations. A valuation represents what a willing buyer would pay a willing seller in the present market, not what they might pay in twelve months.

However, sophisticated buyers and sellers do consider future expectations when negotiating prices. If the majority of market participants believe prices will rise over the coming year, this belief influences their willingness to pay today. This creates a subtle expectation premium that may be embedded in current transaction prices.

Surveyors must navigate this carefully:

✅ Appropriate: Recognizing that current transaction prices may reflect buyer optimism about future appreciation

✅ Appropriate: Noting forward expectations in valuation reports as market context

❌ Inappropriate: Directly adding a percentage premium to current market value based on future expectations

❌ Inappropriate: Valuing properties based on anticipated future prices rather than current market evidence

Time Horizon Considerations

The twelve-month expectation window reported in RICS surveys creates specific considerations for different valuation purposes. A valuation for matrimonial purposes requires current market value, while an investment analysis might appropriately incorporate twelve-month appreciation expectations into total return calculations.

Surveyors should clearly distinguish between:

- Current market value (appropriate for most formal valuation purposes)

- Investment value (which may incorporate future expectations)

- Market value subject to special assumptions (which might include assumptions about future market conditions)

Reconciling Optimism with Present Reality

The moderation of expectations from +43% in January to +33% in February 2026 demonstrates the volatility of forward-looking sentiment [1][3]. This volatility reinforces the importance of grounding valuations in current market evidence rather than sentiment indicators.

However, surveyors should use expectation data to:

- Inform marketing time estimates (optimistic buyers may enter the market more quickly)

- Assess negotiation dynamics (seller expectations may be influenced by positive forecasts)

- Identify potential value trajectories for scenario analysis

- Contextualize regional variations in sentiment and performance

For professionals conducting building surveys alongside valuations, understanding buyer expectations helps frame discussions about property condition and necessary improvements.

Supply Dynamics and Inventory Adjustments

The RICS Q1 2026 data revealed stabilizing supply dynamics, with new instructions remaining neutral at +2% in February [3]. This supply stabilization, combined with improving buyer demand, creates specific valuation considerations related to inventory levels and absorption rates.

Inventory-to-Sales Ratios

The relationship between available inventory and transaction activity provides crucial context for valuation work. With agreed sales at -9% in January (the least negative since June 2025) and new instructions broadly stable, the market is gradually moving toward better balance [1].

Surveyors should monitor:

- Local inventory levels relative to historical norms

- Absorption rates (how quickly properties are selling)

- Days on market trends for comparable properties

- Price reduction patterns indicating seller motivation

In markets with declining inventory and improving sales activity, properties may command premium pricing. Conversely, areas with growing inventory despite weak sales may require more conservative valuation approaches.

The Landlord Supply Constraint

The rental market data from Q1 2026 reveals a critical supply constraint, with landlord instructions at -27% despite improving tenant demand at +2% [3]. This persistent shortage of rental supply has implications for residential valuations through several channels:

- Buy-to-let investment demand supporting property values in rental hotspots

- First-time buyer competition with investors for entry-level properties

- Rental yield support for income-based valuation approaches

Surveyors conducting valuations in areas with strong rental markets should consider how rental supply constraints might support property values even if owner-occupier demand remains subdued.

Practical Application Framework for Surveyors

Translating RICS Q1 2026 survey insights into practical valuation work requires a systematic framework that incorporates market intelligence while maintaining professional standards and defensibility.

Step 1: Regional Market Classification

Begin each valuation by classifying the subject property's location according to Q1 2026 performance categories:

- Outperforming regions (Northern England, Scotland, Northern Ireland)

- National trend regions (broadly tracking the -10% to -12% net balance)

- Underperforming regions (London, South East, East Anglia)

This classification informs subsequent methodology selection and adjustment factors.

Step 2: Transaction Activity Assessment

Evaluate local transaction activity relative to the improving national picture:

- Review agreed sales trends in the specific locality

- Assess buyer enquiry patterns through estate agent consultations

- Analyze days on market for recent comparable sales

- Identify pricing pattern shifts over the past 90 days

For properties requiring Level 2 or Level 3 surveys, transaction activity assessment helps contextualize value conclusions within the broader market environment.

Step 3: Methodology Selection and Weighting

Select primary and secondary valuation methodologies based on:

- Property type and characteristics

- Regional market conditions (from Step 1)

- Transaction activity levels (from Step 2)

- Client requirements and valuation purpose

Apply appropriate weighting to each methodology when reconciling to a final value conclusion.

Step 4: Adjustment Factor Application

Apply time-based and condition adjustments to comparable sales:

- Positive adjustments for comparables in outperforming regions sold in earlier months

- Negative adjustments for comparables in underperforming regions sold in earlier months

- Neutral adjustments where market conditions have remained stable

Document adjustment rationale clearly in the valuation report.

Step 5: Expectation Context Documentation

Include market expectation context in valuation reports without allowing it to inflate current market value conclusions:

- Reference RICS survey data on regional and national expectations

- Note the expectation-reality gap as market context

- Avoid expectation-based value premiums in the final valuation figure

- Distinguish current market value from potential future appreciation

Step 6: Risk and Uncertainty Disclosure

Q1 2026's mixed signals warrant clear disclosure of market uncertainty:

- Acknowledge regional divergence and its implications

- Note interest rate uncertainty and potential impacts

- Reference the moderating expectation trend from January to February

- Include appropriate caveats about market volatility

Professional surveyors understand that thorough documentation protects both clients and practitioners. For those seeking comprehensive guidance on what questions to ask during a building survey, similar documentation principles apply.

Case Study Applications Across Property Types

Case Study 1: Prime London Residential Property

A five-bedroom Victorian house in Hampstead requires valuation for inheritance tax purposes. The property last sold in 2022 for £3.2 million.

Q1 2026 Context Application:

- London net balance: -40% (severe downward pressure) [3]

- National expectation: +33% anticipating rises over 12 months [3]

- Transaction activity: Improving but still negative

Valuation Approach:

- Heavy reliance on recent comparables (within 30 days)

- Downward time adjustments for older comparable sales

- Conservative reconciliation given severe regional underperformance

- Clear documentation of London-specific market conditions

Conclusion: The surveyor would likely conclude a value below the 2022 sale price, with careful documentation of the -40% regional net balance and acknowledgment that forward expectations suggest potential recovery over the coming year.

Case Study 2: Northern England Buy-to-Let Investment

A two-bedroom apartment in Manchester requires valuation for a portfolio refinancing.

Q1 2026 Context Application:

- Northern England: Positive momentum throughout Q1 [7]

- Rental market: Tenant demand +2%, landlord instructions -27% [3]

- Transaction activity: Improving agreed sales

Valuation Approach:

- Income capitalization primary methodology given buy-to-let purpose

- Positive momentum adjustments for older comparable sales

- Rental yield premium reflecting tight supply-demand balance

- CMA secondary methodology showing regional strength

Conclusion: The surveyor would likely conclude a value showing modest appreciation from recent comparables, supported by both positive regional momentum and strong rental market fundamentals.

Case Study 3: South East Family Home

A four-bedroom detached house in Hertfordshire requires valuation for a matrimonial settlement.

Q1 2026 Context Application:

- South East net balance: -24% (significant downward pressure) [3]

- National stabilization trend: -10% to -12% [1][3]

- Buyer demand: Improving but still negative

Valuation Approach:

- CMA primary methodology with recent comparable emphasis

- Modest downward time adjustments reflecting regional underperformance

- Balanced reconciliation acknowledging both regional weakness and improving national trends

- Market condition clauses noting volatility

Conclusion: The surveyor would conclude a current market value reflecting the -24% regional net balance while noting in the report that forward expectations suggest potential stabilization over the coming year. For chartered surveyors in Hertfordshire, this balanced approach proves essential for matrimonial work.

Technology and Data Integration

Modern valuation practice increasingly incorporates technology platforms and data analytics to enhance accuracy and efficiency. The RICS Q1 2026 survey data itself represents a valuable data source that can be integrated into valuation workflows.

Automated Valuation Models (AVMs)

AVMs use statistical modeling and comparable sales data to generate property valuations. During periods of market stabilization like Q1 2026, AVMs face specific challenges:

- Lagging indicators: AVMs rely on completed sales, which may lag current market conditions by several months

- Regional divergence: National AVM models may fail to capture the dramatic regional variations evident in Q1 2026

- Expectation gaps: AVMs cannot incorporate forward-looking sentiment data

Professional surveyors should use AVMs as initial screening tools rather than final valuation conclusions, particularly during transitional market periods.

Market Intelligence Platforms

Subscription-based market intelligence platforms aggregate transaction data, listing information, and market trends. These platforms become particularly valuable during Q1 2026-style conditions when:

- Regional variations require granular local market data

- Transaction activity shifts need real-time monitoring

- Comparable selection demands access to very recent sales

Surveyors should integrate these platforms into their workflow while maintaining professional judgment about data quality and relevance.

RICS Survey Data Integration

The quarterly RICS survey data itself provides valuable context that surveyors should systematically integrate into valuation reports:

- Reference specific net balance figures for the subject property's region

- Compare local conditions to national trends

- Cite expectation data as market context

- Track quarterly trends to identify momentum shifts

This integration demonstrates professional awareness of broader market conditions and enhances the credibility of valuation conclusions.

Professional Standards and Compliance Considerations

Applying Valuation Techniques for Stabilizing House Prices: Applying RICS Q1 2026 Survey for Accurate National Assessments requires strict adherence to professional standards and regulatory requirements.

RICS Valuation Standards (Red Book)

The RICS Valuation – Global Standards (commonly known as the Red Book) provides the mandatory framework for all RICS members conducting valuation work. Key requirements relevant to Q1 2026 conditions include:

- Basis of value clarity: Clearly stating whether the valuation reflects market value, investment value, or another basis

- Assumptions and special assumptions: Documenting any assumptions about future market conditions

- Market conditions disclosure: Describing relevant market conditions at the valuation date

- Uncertainty and risk: Acknowledging material uncertainty where appropriate

The mixed signals of Q1 2026—stabilizing prices combined with optimistic expectations—may warrant material uncertainty clauses in some valuation reports, particularly for properties in heavily pressured regions like London.

Conflicts of Interest

Surveyors must remain vigilant about potential conflicts of interest that might bias valuation conclusions:

- Client pressure: Resisting pressure to inflate valuations based on optimistic forward expectations

- Fee arrangements: Ensuring fees are not contingent on achieving particular value conclusions

- Previous involvement: Disclosing any previous involvement with the subject property

The expectation-reality gap evident in Q1 2026 data creates particular temptation to allow optimistic forecasts to influence current valuations—professional surveyors must resist this pressure.

Documentation and Defensibility

Thorough documentation becomes especially important during transitional market periods. Valuation reports should include:

- Detailed comparable analysis with clear adjustment rationale

- Regional market context referencing RICS survey data

- Methodology selection justification

- Reconciliation reasoning when multiple approaches are used

This documentation protects both the surveyor and the client if valuation conclusions are later questioned. For surveyors conducting property inspections alongside valuations, similar documentation standards apply.

Future Outlook and Emerging Considerations

While this article focuses on applying Q1 2026 survey data, professional surveyors must also consider emerging trends that may influence future valuation practice.

Interest Rate Trajectory

The RICS Head of Market Research noted in February 2026 that mortgage rates are likely to remain higher for longer than previously anticipated [3]. This expectation has significant implications:

- Affordability constraints may persist longer than the +43% optimistic expectations suggest

- Discount rate adjustments for income capitalization approaches may need upward revision

- Transaction activity recovery may prove slower than January's improvement suggested

Surveyors should monitor Bank of England policy decisions and mortgage market trends as key inputs to valuation work throughout 2026.

Regulatory Changes

Potential regulatory changes affecting property markets include:

- Stamp duty adjustments that could influence transaction activity

- Energy efficiency requirements affecting property values

- Rental market regulations impacting buy-to-let investment demand

Staying informed about regulatory developments ensures that valuations reflect all material factors affecting property values.

Climate and Sustainability Factors

Increasingly, climate risks and energy efficiency considerations affect property valuations:

- Flood risk assessments influencing values in vulnerable areas

- EPC ratings affecting marketability and regulatory compliance

- Retrofit costs for properties requiring energy efficiency improvements

For surveyors conducting EPC and MEES assessments alongside valuations, these sustainability factors represent growing importance.

Conclusion

The RICS Q1 2026 survey data presents property professionals with a complex but navigable valuation landscape. The headline stabilization—with house price net balance improving from -19% in October 2025 to -10% in January 2026, before moderating to -12% in February—signals that the market is finding its footing after a challenging period [1][3]. However, this national picture masks dramatic regional divergence, with Northern England showing positive momentum while London faces -40% downward pressure [3][7].

The gap between current subdued conditions and optimistic twelve-month expectations (+43% in January, moderating to +33% in February) creates the central challenge for surveyors applying Valuation Techniques for Stabilizing House Prices: Applying RICS Q1 2026 Survey for Accurate National Assessments [1][3]. Professional practice demands that current market value conclusions remain grounded in present transaction evidence while acknowledging forward expectations as important market context.

Key Implementation Steps for Surveyors

Immediate Actions:

- Review regional classification for all current valuation assignments using Q1 2026 RICS data

- Update comparable adjustment protocols to reflect improving transaction activity and regional divergence

- Enhance documentation standards to clearly distinguish current market value from forward expectations

- Integrate RICS survey data into valuation reports as market context

Ongoing Practices:

- Monitor quarterly RICS releases to track evolving market conditions throughout 2026

- Maintain regional market intelligence through local estate agent consultations and transaction monitoring

- Review methodology weighting periodically as market conditions evolve

- Participate in professional development focused on valuation during transitional markets

Strategic Considerations:

- Invest in technology platforms that provide real-time market intelligence and comparable sales data

- Develop regional expertise to better serve clients in specific geographic markets

- Build relationships with professionals offering complementary services from building surveys to party wall services

The stabilization evident in Q1 2026 data suggests that the UK housing market is transitioning from the acute uncertainty of late 2025 toward a more balanced environment. However, the moderation of expectations from January to February, combined with persistent regional divergence, indicates that this transition remains incomplete and potentially fragile [1][3].

Surveyors who successfully apply the techniques outlined in this article—combining rigorous methodology with market intelligence, regional awareness, and professional standards—will provide clients with accurate, defensible valuations that serve as reliable foundations for property transactions, financing decisions, tax assessments, and legal settlements throughout 2026 and beyond.

The path forward requires balancing optimism about recovery with realism about present conditions, regional awareness with national context, and forward expectations with current evidence. By applying these principles systematically, property professionals can navigate the stabilizing market with confidence and deliver valuations that stand the test of time.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[3] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[7] Rics Residential Market Survey Q1 2026 Building Survey Implications For Northern England Price Surges 2 – https://nottinghillsurveyors.com/blog/rics-residential-market-survey-q1-2026-building-survey-implications-for-northern-england-price-surges-2