The institutional buy-to-let sector is experiencing a remarkable renaissance in 2026. After years of regulatory uncertainty, tax changes, and market volatility, professional investors are returning to the rental property market with renewed confidence. With rental income forecast to climb by 12% and long-term property values expected to appreciate by 22.2% over the next five years, institutional landlords are positioning themselves to capitalize on constrained supply and rising tenant demand [1][2]. However, success in this recovering market requires sophisticated valuation strategies for buy-to-let institutional portfolios in 2026: surveyor insights on recovering rental markets that account for tightened lending criteria, enhanced regulatory scrutiny, and evolving risk assessment frameworks.

Key Takeaways

✅ Market Recovery Momentum: Institutional buy-to-let portfolios are benefiting from a 12% rental income growth forecast and 22.2% property value appreciation over five years, creating substantial opportunities for professional investors [1][2].

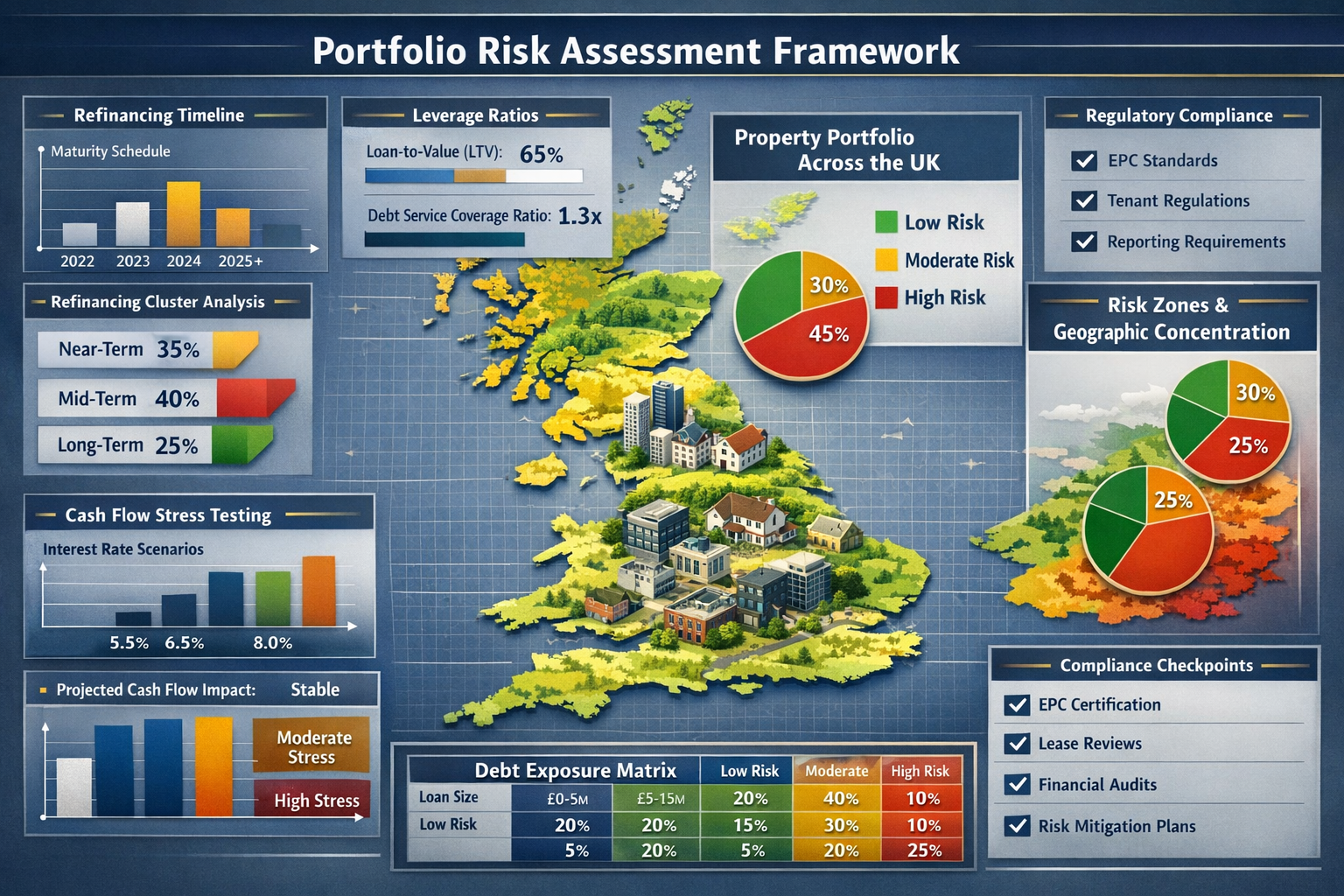

✅ Stricter Underwriting Standards: Lenders now apply stress rates between 5.5% and 8% with Interest Coverage Ratios (ICR) ranging from 125% to 145%, requiring comprehensive portfolio-wide stress testing rather than property-specific assessments [3].

✅ Risk-Based Valuation Approach: Modern surveyor methodologies emphasize concentration risk analysis, refinancing clustering reviews, and aggregate balance sheet resilience to meet PRA framework requirements [3].

✅ Strategic Acquisition Criteria: Successful institutional investors prioritize geographic diversification, property type variation, and staggered refinancing schedules to optimize portfolio sustainability [3].

✅ Professional Surveyor Expertise: Engaging qualified chartered surveyors with institutional portfolio experience is essential for accurate valuations that satisfy both lender requirements and investment objectives.

Understanding the 2026 Institutional Buy-to-Let Landscape

The institutional buy-to-let market has transformed significantly since the challenges of recent years. In 2026, professional landlords are witnessing a sector characterized by improved fundamentals and renewed investor confidence. The combination of housing supply constraints, demographic shifts toward renting, and stabilizing interest rates has created a favorable environment for institutional-scale investments.

Market Fundamentals Driving Portfolio Growth

Several key factors are propelling the institutional buy-to-let recovery:

Supply-Demand Imbalance 📊

The UK continues to face a significant shortage of rental properties relative to tenant demand. This structural deficit supports both rental growth and capital appreciation, providing institutional investors with dual income streams.

Rental Income Projections

Industry forecasts indicate rental income will increase by approximately 12% through the forecast period [2]. This growth trajectory strengthens cash flow dynamics and improves portfolio viability under stress testing scenarios.

Capital Appreciation Outlook

Long-term property value growth is projected at an average 22.2% increase over the next five years [2]. This substantial appreciation potential enhances total return profiles for institutional portfolios, making buy-to-let investments increasingly attractive compared to alternative asset classes.

Competitive Financing Environment

As of February 2026, buy-to-let pricing starts at 3.79% for two-year fixed products at 60% loan-to-value [4]. While lender fees typically hover around £1,995, the competitive landscape offers institutional investors access to relatively affordable leverage for portfolio expansion.

Regulatory Framework and Compliance Considerations

The PRA (Prudential Regulation Authority) portfolio landlord framework now applies to investors with four or more mortgaged buy-to-let properties [3]. This regulatory structure requires lenders to scrutinize entire balance sheets rather than evaluating individual property metrics in isolation.

Key compliance requirements include:

- Comprehensive debt exposure analysis across all portfolio holdings

- Aggregate leverage assessments at portfolio level

- Cash flow resilience modeling under stressed scenarios

- Refinancing risk evaluation across maturity schedules

- Geographic and property type concentration analysis

Professional commercial valuations conducted by qualified chartered surveyors have become essential for demonstrating portfolio quality and regulatory compliance to institutional lenders.

Valuation Strategies for Buy-to-Let Institutional Portfolios in 2026: Core Methodologies

Effective valuation strategies for buy-to-let institutional portfolios in 2026: surveyor insights on recovering rental markets require a multi-dimensional approach that extends beyond traditional single-property assessments. Chartered surveyors specializing in institutional portfolios employ sophisticated methodologies that align with both lender requirements and investment objectives.

RICS Valuation Standards and Portfolio Applications

The Royal Institution of Chartered Surveyors (RICS) provides the professional framework for property valuations in the UK. For institutional buy-to-let portfolios, surveyors apply these standards with particular emphasis on:

Investment Method Valuation

This approach capitalizes rental income streams at appropriate yields to determine property values. Surveyors analyze:

- Current rental income (actual or market rent)

- Void periods and tenant turnover rates

- Property management costs and maintenance reserves

- Appropriate capitalization rates based on location, property type, and tenant quality

- Comparable evidence from recent portfolio transactions

Comparable Sales Analysis

Surveyors examine recent transactions of similar properties in comparable locations, adjusting for:

- Property condition and specification differences

- Market timing and transaction circumstances

- Tenure considerations (freehold vs. leasehold)

- Portfolio premiums or discounts based on scale

Residual Value Considerations

For properties requiring refurbishment or repositioning, surveyors calculate residual values by:

- Estimating completed property value

- Deducting development costs, professional fees, and finance charges

- Applying appropriate profit margins and risk adjustments

Stress Testing and Interest Coverage Ratio Analysis

Modern lender requirements mandate rigorous stress testing of portfolio cash flows. Surveyors must understand and incorporate these criteria into valuation assessments:

Elevated Stress Rates

Lenders apply stress rates between 5.5% and 8% when assessing portfolio landlord applications [3]. These rates significantly exceed current pay rates, modeling resilience against future interest rate volatility.

Interest Coverage Ratio Thresholds

ICR requirements now range between 125% and 145% depending on:

- Tax status of the borrower (higher-rate taxpayers face stricter requirements)

- Borrower structure (limited companies vs. personal ownership)

- Portfolio size and complexity

- Geographic concentration and property type diversity

For example, a property generating £15,000 annual rental income with stressed interest costs of £10,000 would achieve an ICR of 150% (£15,000 ÷ £10,000), meeting most lender requirements.

Portfolio-Wide Stress Testing

Increasingly, lenders conduct aggregate analysis where total rental income across the entire portfolio is compared against total stressed interest obligations [3]. This holistic approach requires surveyors to consider portfolio composition and interdependencies rather than treating each property as an isolated asset.

Geographic and Property Type Diversification Assessment

Concentration risk analysis has become a critical component of institutional portfolio valuations [3]. Surveyors evaluate:

Geographic Exposure

Portfolios heavily concentrated in single regions face elevated risk from:

- Local economic downturns

- Regional oversupply conditions

- Area-specific regulatory changes

- Natural disaster or environmental risks

Surveyors assess whether geographic diversification adequately mitigates these concentration risks, potentially applying valuation discounts for over-concentrated portfolios.

Property Type Clustering

Similar concerns apply to portfolios dominated by single property types:

- Student accommodation faces term-time vacancy risks

- Houses in multiple occupation (HMOs) encounter specific regulatory challenges

- City center apartments may be vulnerable to remote working trends

- Family houses in suburban locations offer different risk-return profiles

Professional surveyors working on institutional portfolios often recommend optimal diversification strategies that balance risk mitigation with operational efficiency. For properties requiring detailed condition assessments, a comprehensive building survey can identify potential maintenance issues that affect valuation.

Risk Assessment Frameworks for Institutional Buy-to-Let Portfolios

Sophisticated valuation strategies for buy-to-let institutional portfolios in 2026: surveyor insights on recovering rental markets must incorporate comprehensive risk assessment frameworks that address both property-specific and portfolio-level considerations.

Refinancing Clustering and Maturity Schedule Analysis

Refinancing clustering has emerged as a critical underwriting consideration in 2026 [3]. Credit committees escalate cases where multiple portfolio loans mature within 12-month windows, even when individual property metrics appear strong.

Why Refinancing Clustering Matters:

- Concentrated maturity dates create vulnerability to adverse market timing

- Interest rate spikes at refinancing could dramatically increase debt service costs

- Lender appetite changes could restrict refinancing options

- Property value declines at maturity could trigger equity shortfalls

Surveyor Recommendations for Maturity Management:

- Stagger Loan Maturities: Structure portfolio financing with varied maturity dates spread across 3-5 year periods

- Maintain Refinancing Reserves: Hold liquidity buffers equivalent to 6-12 months of debt service

- Monitor Market Conditions: Track interest rate trends and lender appetite 18-24 months before maturity dates

- Pre-emptive Refinancing: Consider early refinancing when favorable market conditions emerge

Balance Sheet Resilience and Aggregate Leverage

The PRA framework requires underwriting to scrutinize entire balance sheets rather than individual property metrics [3]. Surveyors assessing institutional portfolios must evaluate:

Aggregate Leverage Ratios

Total debt across all portfolio properties relative to total portfolio value. Institutional investors typically target:

- Conservative portfolios: 50-60% aggregate loan-to-value

- Moderate portfolios: 60-70% aggregate loan-to-value

- Aggressive portfolios: 70-75% aggregate loan-to-value (approaching lender limits)

Cash Flow Coverage

Net rental income after all operating expenses relative to total debt service obligations. Strong portfolios demonstrate:

- Positive cash flow under current market conditions

- Adequate coverage under stressed scenarios (5.5-8% interest rates)

- Sufficient reserves for void periods, maintenance, and capital expenditure

Liquidity Position

Available cash reserves and unencumbered assets that provide financial flexibility:

- Emergency reserves for unexpected expenses

- Opportunity capital for value-add acquisitions

- Refinancing buffers to navigate adverse market conditions

Tenant Quality and Income Stability Analysis

Portfolio valuations increasingly incorporate tenant quality assessments that affect both rental income reliability and property condition:

Tenant Profile Considerations:

- Professional tenants: Generally provide stable income with lower void risk

- Benefit-dependent tenants: May face payment interruptions but often backed by local authority guarantees

- Student tenants: Seasonal occupancy patterns with parental guarantees

- Corporate lets: Premium rents with institutional tenant backing

Lease Structure Impact:

- Longer lease terms (2+ years) provide income certainty

- Break clauses create refinancing uncertainty

- Rent review mechanisms (fixed increases vs. market reviews)

- Tenant responsibility for repairs and maintenance

Surveyors conducting annual tax valuations for institutional portfolios must accurately reflect tenant quality in rental income projections and void period assumptions.

Property Condition and Capital Expenditure Forecasting

Institutional portfolio valuations require comprehensive assessment of:

Current Property Condition

Surveyors identify:

- Immediate repair requirements affecting habitability

- Deferred maintenance accumulating across the portfolio

- Building safety compliance issues (fire safety, electrical, gas)

- Energy efficiency ratings and improvement opportunities

Capital Expenditure Forecasting

Projecting future investment requirements over 5-10 year periods:

- Roof replacements and structural repairs

- Heating system upgrades and modernization

- Kitchen and bathroom refurbishments

- External decoration and grounds maintenance

Regulatory Compliance Costs

Anticipating expenses related to:

- Energy Performance Certificate (EPC) minimum standards

- Electrical safety inspections and certifications

- Gas safety annual checks

- Selective licensing requirements in regulated areas

Professional surveyors often recommend building defects surveys for older properties in institutional portfolios to accurately quantify capital expenditure requirements.

Strategic Acquisition and Portfolio Optimization

Successful institutional investors in 2026 combine rigorous valuation methodologies with strategic acquisition criteria that optimize portfolio performance and risk-adjusted returns.

Target Property Selection Criteria

High-Yield Opportunities in Recovery Markets

Institutional investors are identifying properties that offer:

- Rental yields exceeding 5-6% in recovering regional markets

- Below-replacement-cost acquisition prices

- Value-add potential through refurbishment or repositioning

- Strong tenant demand fundamentals (employment, demographics, transport links)

Geographic Targeting

Strategic investors focus on locations with:

- Employment growth and economic diversification

- Infrastructure investment and connectivity improvements

- Undersupply relative to household formation rates

- Favorable local authority planning policies

Regional markets outside London often provide superior yield profiles while maintaining strong appreciation potential. Investors working with chartered surveyors in Guildford, chartered surveyors in St Albans, and other strategic locations benefit from local market expertise.

Portfolio Rebalancing and Disposal Strategies

Institutional investors regularly review portfolio composition to:

Identify Underperforming Assets

Properties that:

- Generate below-market rental yields

- Require excessive capital expenditure relative to value

- Face adverse local market conditions

- Create concentration risk concerns

Strategic Disposal Timing

Optimizing exit strategies by:

- Capitalizing on peak market conditions in specific locations

- Harvesting capital gains to redeploy into higher-yield opportunities

- Reducing geographic or property type concentration

- Simplifying portfolio management and reducing operational complexity

Acquisition-Disposal Balancing

Maintaining optimal portfolio size and composition through:

- Simultaneous disposal of mature, lower-yield assets

- Acquisition of higher-yield, value-add opportunities

- Net portfolio growth targeting 5-10% annual expansion

- Maintaining aggregate leverage within target parameters

Financing Strategy and Lender Relationship Management

Diversified Lender Relationships

Institutional investors cultivate relationships with multiple lenders to:

- Access competitive pricing and terms

- Mitigate refinancing risk through alternative options

- Leverage specialist lenders for specific property types

- Maintain flexibility for portfolio expansion

Optimal Financing Structures

Balancing fixed and variable rate debt:

- Fixed-rate mortgages provide payment certainty and stress test compliance

- Variable-rate options offer flexibility and potential cost savings

- Interest-only vs. repayment structures based on investment horizon

- Limited company vs. personal ownership tax optimization

Proactive Communication

Maintaining strong lender relationships through:

- Regular portfolio performance reporting

- Transparent disclosure of material changes

- Early engagement on refinancing requirements

- Professional presentation of valuation reports and financial projections

Professional Surveyor Selection and Engagement

The quality of valuation advice directly impacts acquisition decisions, financing outcomes, and portfolio performance. Selecting the right surveyor partner is crucial for institutional buy-to-let investors.

Qualifications and Specialist Experience

RICS Chartered Status

Ensure surveyors hold appropriate qualifications:

- MRICS (Member of the Royal Institution of Chartered Surveyors)

- FRICS (Fellow status indicating senior expertise)

- Specialist valuation qualifications and continuing professional development

Institutional Portfolio Experience

Seek surveyors with demonstrated expertise in:

- Multi-property portfolio valuations

- Lender-compliant reporting formats

- PRA framework requirements and stress testing

- Investment method and income capitalization approaches

Local Market Knowledge

Surveyors with deep understanding of target acquisition areas provide:

- Accurate comparable evidence and market rent assessments

- Insight into local supply-demand dynamics

- Awareness of area-specific risks and opportunities

- Relationships with local agents and market participants

Working with established firms offering services across strategic locations—such as chartered surveyors in Central London, chartered surveyors in West London, and chartered surveyors in North London—ensures consistent quality across geographically diverse portfolios.

Scope of Services and Deliverables

Comprehensive Valuation Reports

Professional surveyors provide detailed documentation including:

- Executive summary with valuation conclusion

- Property description and specification

- Tenure details and legal considerations

- Market analysis and comparable evidence

- Income approach calculations (rental value, yield, capitalization)

- Risk assessment and limiting conditions

- Photographs and supporting documentation

Portfolio-Level Analysis

Institutional-focused surveyors offer:

- Aggregate portfolio valuation summaries

- Concentration risk analysis and recommendations

- Capital expenditure forecasting across holdings

- Performance benchmarking against market indices

- Strategic acquisition and disposal recommendations

Ongoing Advisory Services

Leading surveyor practices provide:

- Regular portfolio revaluation (annual or bi-annual)

- Market intelligence and trend analysis

- Refinancing support and lender liaison

- Due diligence for acquisition opportunities

- Expert witness services for disputes or litigation

Cost Considerations and Value Optimization

Fee Structures

Surveyor fees typically vary based on:

- Property value and complexity

- Portfolio size (economies of scale for multiple properties)

- Scope of services and reporting requirements

- Urgency and turnaround time

Value Beyond Cost

Quality surveyor advice delivers returns through:

- Avoiding overpriced acquisitions that erode returns

- Identifying value-add opportunities that enhance yields

- Securing favorable lender terms through professional presentation

- Mitigating risks through comprehensive due diligence

Institutional investors recognize that professional surveyor fees represent a small percentage of transaction value while providing substantial protection against costly mistakes.

Technology and Data Analytics in Portfolio Valuation

The 2026 institutional buy-to-let landscape increasingly leverages technology to enhance valuation accuracy and portfolio management efficiency.

Automated Valuation Models (AVMs) and Limitations

AVM Applications

Technology-driven valuation tools offer:

- Rapid preliminary valuations for screening opportunities

- Portfolio-wide revaluation for monitoring purposes

- Trend analysis and performance tracking

- Desktop valuations for refinancing assessments

AVM Limitations

Automated systems cannot fully replace professional surveyors because:

- Unique property characteristics require expert judgment

- Local market nuances escape algorithmic analysis

- Lender requirements mandate RICS-qualified valuations

- Complex portfolios need holistic risk assessment

Optimal Integration

Sophisticated investors combine AVM technology with professional surveyor expertise:

- AVMs for initial screening and portfolio monitoring

- Professional valuations for acquisitions, disposals, and refinancing

- Technology platforms for data aggregation and reporting

- Surveyor interpretation and strategic recommendations

Portfolio Management Platforms

Integrated Systems

Modern institutional investors utilize platforms that consolidate:

- Property details and specifications

- Tenancy information and lease schedules

- Financial performance (rental income, expenses, yields)

- Maintenance records and capital expenditure

- Valuation history and market value tracking

- Debt schedules and refinancing calendars

Performance Analytics

Advanced platforms provide:

- Real-time portfolio performance dashboards

- Benchmarking against market indices

- Scenario modeling for acquisition and disposal decisions

- Risk metrics and concentration analysis

- Automated reporting for stakeholders and lenders

Market Intelligence and Forecasting Tools

Data Sources

Institutional investors access:

- Land Registry transaction data

- Rental market indices and trend analysis

- Economic indicators (employment, demographics, household formation)

- Planning application tracking and development pipeline monitoring

- Lender product comparisons and rate tracking

Predictive Analytics

Sophisticated investors employ:

- Machine learning models for rental growth forecasting

- Property value appreciation predictions

- Tenant demand modeling

- Risk probability assessments

Professional surveyors increasingly integrate these data sources into valuation methodologies, combining algorithmic insights with expert judgment to deliver superior advisory services.

Regulatory Outlook and Future Considerations

The institutional buy-to-let sector continues to evolve in response to regulatory developments and market dynamics. Understanding the trajectory of these changes is essential for long-term portfolio strategy.

PRA Framework Evolution

Current Regulatory Stance

The PRA framework is unlikely to loosen in the near term as regulatory focus remains on responsible lending and systemic risk management [3]. Portfolio sustainability remains a central credit decision criterion.

Future Developments

Institutional investors should anticipate:

- Continued emphasis on balance sheet resilience

- Potential tightening of stress test parameters if interest rate volatility increases

- Enhanced scrutiny of concentration risks and geographic exposure

- Greater transparency requirements for portfolio reporting

Strategic Response

Professional landlords must prioritize:

- Conservative leverage strategies that provide regulatory comfort

- Diversification across geographies and property types

- Proactive lender communication and relationship management

- Professional presentation of portfolio metrics and risk management

Energy Efficiency and Sustainability Requirements

Regulatory Trajectory

The UK government continues to raise minimum Energy Performance Certificate (EPC) standards for rental properties:

- Current minimum: EPC rating E

- Proposed future requirements: EPC rating C by 2028-2030

- Potential further increases to rating B for new tenancies

Investment Implications

Institutional portfolios must account for:

- Capital expenditure for energy efficiency improvements

- Potential rental premiums for high-efficiency properties

- Obsolescence risk for properties unable to achieve minimum standards

- Valuation adjustments reflecting compliance costs and timing

Opportunity Perspective

Forward-thinking investors view sustainability requirements as:

- Competitive advantages through superior property specifications

- Tenant attraction and retention benefits

- Future-proofing against regulatory tightening

- Alignment with ESG (Environmental, Social, Governance) investment criteria

Taxation and Legislative Changes

Ongoing Tax Considerations

Institutional investors navigate:

- Section 24 mortgage interest relief restrictions

- Capital gains tax on disposals

- Stamp duty land tax on acquisitions

- Inheritance tax planning for portfolio succession

Limited Company Structures

Many institutional investors operate through:

- Special purpose vehicles (SPVs) for individual properties or sub-portfolios

- Corporate structures for tax efficiency

- Professional management and governance frameworks

Legislative Monitoring

Successful investors maintain awareness of:

- Proposed changes to rental sector regulation

- Local authority selective licensing expansion

- Tenant protection and security of tenure reforms

- Planning policy changes affecting permitted development and conversions

Understanding how property market legislation changes affect portfolio valuations is essential for long-term strategic planning.

Conclusion: Navigating the 2026 Institutional Buy-to-Let Opportunity

The institutional buy-to-let sector in 2026 presents compelling opportunities for professional investors who combine sophisticated valuation strategies for buy-to-let institutional portfolios in 2026: surveyor insights on recovering rental markets with disciplined risk management and strategic portfolio construction. With rental income forecast to grow 12% and property values expected to appreciate 22.2% over the next five years, the fundamentals support continued institutional investment [1][2].

However, success requires navigating a more complex regulatory and financing environment. Lenders apply elevated stress rates between 5.5% and 8% with Interest Coverage Ratios ranging from 125% to 145%, demanding comprehensive portfolio-wide analysis rather than property-specific assessments [3]. The PRA framework's emphasis on balance sheet resilience, concentration risk management, and refinancing clustering means institutional investors must demonstrate sophisticated portfolio management capabilities.

Actionable Next Steps for Institutional Investors 🎯

1. Engage Qualified Chartered Surveyors

Partner with RICS-qualified professionals who specialize in institutional portfolio valuations and understand current lender requirements. Ensure your surveyor team has deep local market knowledge in your target acquisition areas.

2. Conduct Comprehensive Portfolio Audits

Review existing holdings for concentration risks, refinancing clustering, and capital expenditure requirements. Identify underperforming assets for potential disposal and redeployment of capital.

3. Optimize Financing Structures

Diversify lender relationships, stagger loan maturity dates, and maintain adequate liquidity reserves. Ensure aggregate leverage and portfolio-wide stress testing meet current regulatory standards.

4. Implement Technology Solutions

Adopt portfolio management platforms that consolidate property data, financial performance, and risk metrics. Leverage market intelligence tools while maintaining professional surveyor relationships for critical decisions.

5. Develop Strategic Acquisition Criteria

Define clear target property profiles that balance yield optimization with risk diversification. Focus on recovering markets with strong tenant demand fundamentals and below-replacement-cost acquisition opportunities.

6. Plan for Regulatory Evolution

Budget for energy efficiency improvements to meet future EPC requirements. Monitor legislative developments and adapt portfolio strategy proactively rather than reactively.

7. Maintain Professional Standards

Invest in quality property management, tenant screening, and maintenance programs. Professional operation enhances tenant retention, protects property values, and satisfies lender requirements.

The institutional buy-to-let market in 2026 rewards investors who combine rigorous valuation methodologies, comprehensive risk assessment, and strategic portfolio management. By partnering with experienced chartered surveyors and maintaining disciplined investment criteria, professional landlords can capitalize on the recovering rental market while navigating the enhanced regulatory framework that defines the modern institutional landscape.

For expert guidance on institutional portfolio valuations and strategic acquisition support, consider consulting with qualified professionals who understand the complexities of the 2026 buy-to-let market and can provide the insights necessary for informed investment decisions.

References

[1] Institutional Buy To Let Valuation Surveys Assessing High Yield Opportunities In The 2026 Recovery – https://nottinghillsurveyors.com/blog/institutional-buy-to-let-valuation-surveys-assessing-high-yield-opportunities-in-the-2026-recovery

[2] Buy To Let Valuation Surge 2026 Survey Strategies For Institutional Investors In A Recovering Market – https://nottinghillsurveyors.com/blog/buy-to-let-valuation-surge-2026-survey-strategies-for-institutional-investors-in-a-recovering-market

[3] Portfolio Landlords And Stress Testing In 2026 How Underwriting Has Tightened – https://www.willowprivatefinance.co.uk/portfolio-landlords-and-stress-testing-in-2026-how-underwriting-has-tightened

[4] Buy To Let Market Update February 2026 – https://www.nrla.org.uk/news/buy-to-let-market-update-february-2026