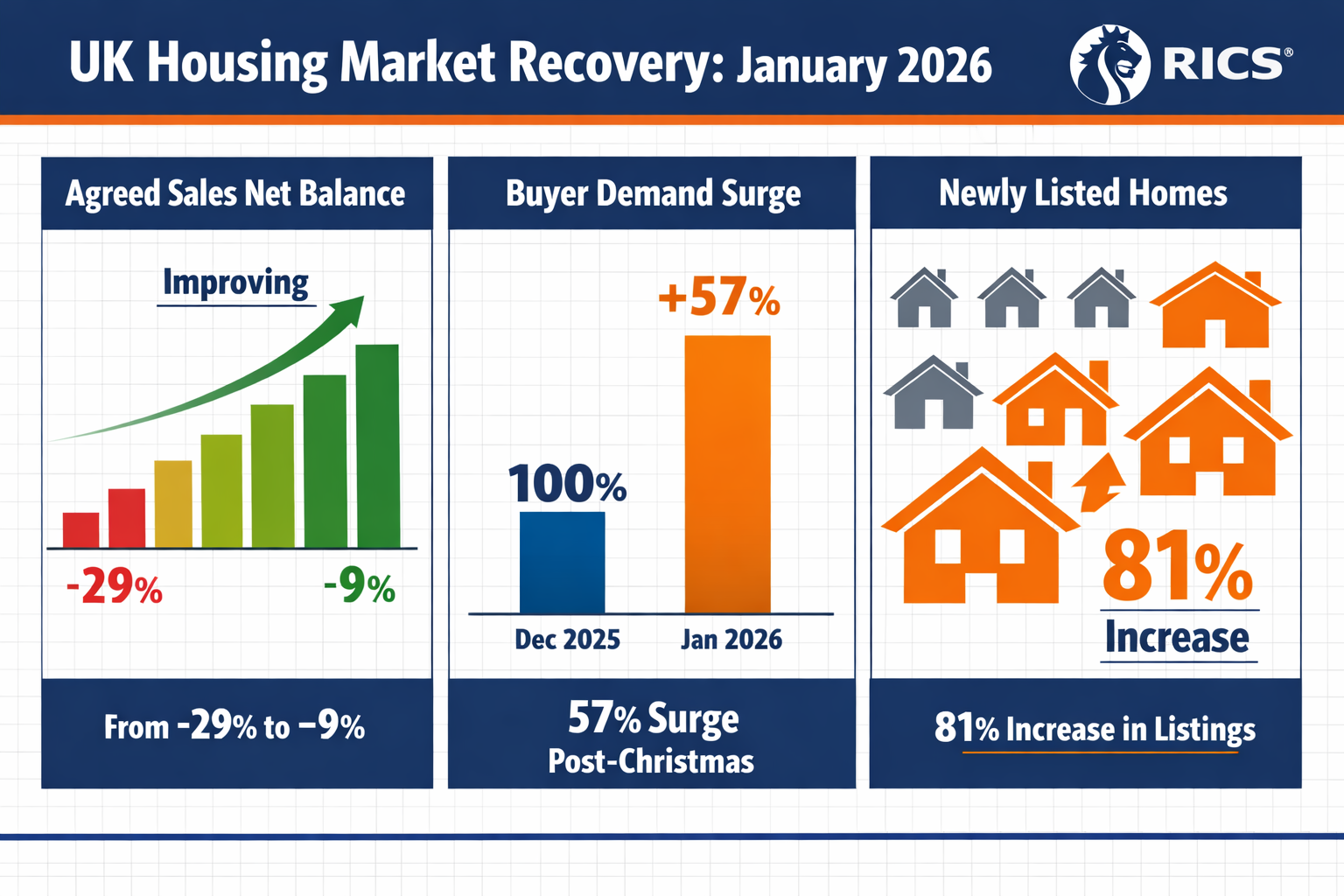

The UK housing market is experiencing a remarkable turnaround. After a challenging end to 2025, agreed sales have improved to -9% net balance in January 2026—the least negative reading since June 2025 and a dramatic improvement from -21% in December and -29% in November[1]. With the 12-month outlook reaching a positive +35%, the surveying profession faces a critical question: how can building surveyors prepare their operations, quality standards, and delivery capacity for the anticipated volume surge as transaction momentum accelerates through 2026?

The recovery signals are unmistakable. Buyer demand surged 57% in the two weeks following Christmas 2025, newly listed homes rose 81% in early January 2026, and surveyor sentiment has reached its most optimistic levels since late 2024[2]. This isn't merely a temporary spike—early 2026 activity has surged more than 20% above early-2023 levels, suggesting a sustainable medium-term trend[2]. For building surveyors, this recovery presents both significant opportunity and operational challenge.

Key Takeaways

- Agreed sales recovered to -9% net balance in January 2026, marking the strongest reading in seven months and signalling sustained transaction growth ahead

- Surveyor capacity planning is critical, with firms needing to scale operational resources, quality control systems, and delivery timelines to meet projected 35% growth in 12-month sales expectations

- Technology integration and workforce development are essential preparation strategies, enabling surveyors to handle increased volumes while maintaining professional standards

- Government reforms may fundamentally change survey timing, potentially requiring upfront property condition assessments that shift demand patterns earlier in the transaction process

- Regional market variations require flexible approaches, with London and the Southeast showing different supply dynamics compared to Northern regions

Understanding the Agreed Sales Recovery and Building Survey Demand Trajectory Through 2026

The Numbers Behind the Recovery 📊

The statistics paint a compelling picture of market resurgence. New buyer enquiries improved to -15% net balance in January 2026, up from -21% in December, indicating easing downward pressure on demand[1]. This improvement coincides with the busiest start-of-year for property listings since 2014, with the average estate agent beginning January 2026 with 32 homes for sale—the highest early-January figure in eight years[2].

House prices have stabilised at a national level, although regional disparities continue to widen. London and the Southeast are experiencing sharper price adjustments, while Scotland and Northern Ireland maintain growth trajectories[1]. The average price of homes coming to market climbed 2.8% in January 2026, representing the largest January rise since records began, despite one-third of properties reducing their asking prices[2].

For building surveyors, these market dynamics translate directly into survey demand patterns. As agreed sales increase and transaction volumes build, the requirement for comprehensive building surveys intensifies proportionally. The 12-month sales growth projection of +35% suggests surveyors should prepare for volume increases of similar magnitude.

What's Driving the Transaction Momentum?

Several fundamental factors underpin the recovery:

- Improved affordability conditions as mortgage rates stabilise and buyer confidence returns

- Reduced market uncertainty following the turbulent close to 2025

- Increased housing stock availability particularly in London and the Southeast

- Pent-up demand release from buyers who delayed decisions during the uncertain period

- Seller confidence returning as evidenced by record January price increases

The surveying sector expects positive volume growth through 2026, with many lenders forecasting increased mortgage volumes and lending activity to support rising transaction levels[3]. This creates a clear operational imperative for survey firms to enhance capacity and streamline processes.

Operational Capacity Planning: Preparing Survey Firms for Increased Volumes

Assessing Current Capacity and Identifying Bottlenecks

The first step in preparing for volume increases involves honest assessment of current operational capacity. Survey firms should evaluate:

| Capacity Factor | Assessment Questions | Action Threshold |

|---|---|---|

| Surveyor Availability | How many surveys can current staff complete weekly? | <85% utilisation suggests capacity |

| Booking Lead Times | What's the average wait time for survey appointments? | >10 days indicates strain |

| Report Turnaround | Days from inspection to report delivery? | >5 days suggests process review needed |

| Quality Control | Percentage of reports requiring significant revision? | >15% indicates quality pressure |

| Client Satisfaction | NPS scores and complaint rates? | Declining trends signal issues |

Understanding these metrics provides the foundation for strategic capacity expansion. Many firms discover that bottlenecks exist not in surveyor availability but in administrative processes, report writing efficiency, or quality assurance workflows.

Scaling Surveyor Resources Strategically

With agreed sales recovery and building survey demand building momentum through 2026, firms face critical decisions about resource scaling:

Recruitment strategies should focus on both experienced surveyors and graduate talent pipelines. RICS is working on clearer pathways for graduates to gain qualifications, which will help build the talent pipeline[3]. However, recruitment alone cannot solve immediate capacity challenges given the time required for proper training and qualification.

Flexible staffing models offer interim solutions:

- Associate surveyor networks for overflow capacity

- Retired surveyors available for part-time work

- Regional partnerships with complementary firms

- Specialist sub-contractors for specific survey types

Surveyor retention becomes equally critical during growth periods. Firms must ensure that increased volumes don't lead to burnout, quality deterioration, or talent loss. This requires careful workload management, competitive compensation adjustments, and investment in tools that reduce administrative burden.

Technology Integration for Volume Management

Modern survey firms increasingly rely on digital tools to enhance capacity without proportional staff increases:

Digital inspection tools including thermal imaging cameras, moisture meters, and laser measuring devices accelerate on-site data collection while improving accuracy. These technologies enable surveyors to conduct more thorough inspections in less time, directly increasing daily capacity.

Cloud-based reporting platforms streamline the report creation process, offering standardised templates, automated formatting, and collaborative editing capabilities. This reduces report turnaround times and minimises quality control iterations.

Client communication systems automate booking confirmations, inspection scheduling, progress updates, and report delivery, freeing administrative staff to focus on higher-value activities. Understanding building surveyor access requirements and coordinating with clients becomes more efficient through automated systems.

Workflow management software provides visibility across all active surveys, enabling managers to identify bottlenecks, balance workloads, and maintain consistent delivery timelines even during volume surges.

Quality Control and Professional Standards During Volume Growth

Maintaining RICS Standards Under Pressure ⚖️

As agreed sales recovery drives building survey demand higher through 2026, the greatest risk facing the profession is quality deterioration under volume pressure. The temptation to rush inspections, abbreviate reports, or reduce thoroughness can have severe professional and reputational consequences.

RICS building surveys maintain their value proposition precisely because they adhere to rigorous professional standards. Compromising these standards to accommodate volume destroys the fundamental trust relationship with clients and lenders.

Quality control systems must scale alongside capacity:

✅ Peer review protocols ensuring experienced surveyors review reports from less experienced colleagues before delivery

✅ Standardised checklists covering all essential inspection elements for different property types and survey levels

✅ Continuous professional development maintaining surveyor knowledge of emerging defects, construction techniques, and regulatory changes

✅ Client feedback mechanisms capturing satisfaction data and identifying quality issues before they escalate

✅ Regular calibration sessions where surveyors discuss challenging cases and align assessment approaches

Understanding the difference between Level 2 and Level 3 surveys becomes particularly important during volume growth, ensuring clients receive appropriate recommendations and surveyors allocate appropriate time to each inspection type.

Specialisation vs. Generalisation Strategies

Firms must decide whether to position surveyors as generalists capable of handling diverse property types or specialists focused on specific property categories. Each approach offers distinct advantages during volume growth:

Generalist advantages:

- Maximum scheduling flexibility

- Broader market coverage

- Reduced dependency on individual surveyors

- Simpler resource allocation

Specialist advantages:

- Higher quality assessments for complex properties

- Premium pricing for specialist knowledge

- Stronger referral relationships with niche agents

- Reduced inspection time through familiarity

Many successful firms adopt a hybrid model, developing core generalist capabilities while maintaining specialist expertise for period properties, listed buildings, or properties with specific challenges. For example, surveyors with expertise in Edwardian cottages or properties requiring areas of further investigation can command premium fees while generalists handle standard residential surveys.

Training and Development Infrastructure

Surveyor training and recruitment is critical as the sector prepares for increased activity[3]. Firms should establish structured development programmes that:

- Provide graduated responsibility levels for trainee surveyors

- Pair junior surveyors with experienced mentors for complex inspections

- Offer regular technical training on emerging defects and construction methods

- Create clear qualification pathways aligned with RICS requirements

- Maintain knowledge libraries covering common and unusual defect patterns

Investment in training infrastructure pays dividends during volume growth, enabling firms to leverage junior talent effectively while maintaining quality standards. This approach also supports long-term sector sustainability by attracting the next generation of surveying professionals.

Strategic Positioning for Agreed Sales Recovery and Building Survey Demand Growth

Anticipating Regulatory and Process Changes

Proposed government reforms to the homebuying process could require surveyors to conduct property condition assessments as a standard upfront requirement, potentially increasing survey demand earlier in the process and fundamentally changing operational timelines[3]. This represents both opportunity and challenge for the surveying profession.

If implemented, mandatory upfront surveys would:

🔄 Shift demand timing from post-offer to pre-marketing stages

🔄 Change client relationships with sellers rather than buyers commissioning surveys

🔄 Alter report formatting to serve multiple potential buyers rather than single clients

🔄 Require process redesign around seller timelines rather than buyer urgency

🔄 Create standardisation pressure as surveys become directly comparable across properties

Surveyors should monitor these potential reforms closely and prepare operational models that can adapt quickly if regulations change. Early adopters of seller-commissioned survey models may gain competitive advantages as the market transitions.

Regional Market Positioning

London and the Southeast demonstrated the largest year-on-year increases in stock, while parts of the North show greater scarcity and stronger price resilience[2]. These regional variations create different strategic opportunities for survey firms.

High-volume, high-stock regions (London, Southeast) favour:

- Efficient, technology-enabled operations

- Competitive pricing strategies

- Fast turnaround commitments

- Strong lender relationships

- Geographic coverage breadth

Lower-volume, constrained-stock regions (Northern markets) favour:

- Relationship-based marketing

- Premium positioning for scarce opportunities

- Specialist expertise for local property types

- Estate agent partnerships

- Community presence

Firms operating across multiple regions should tailor their operational models and marketing approaches to match local market dynamics rather than applying uniform strategies nationally.

Building Lender and Intermediary Relationships 🤝

As mortgage volumes increase through 2026, strong relationships with lenders and mortgage intermediaries become increasingly valuable referral sources. Surveyors should:

- Maintain panel memberships with major lenders

- Deliver consistent quality meeting lender requirements

- Provide reliable turnaround times for mortgage-dependent surveys

- Communicate proactively about complex cases requiring additional time

- Demonstrate understanding of lender valuation and risk criteria

These relationships create stable demand flows that complement direct client instructions, smoothing volume fluctuations and providing predictable capacity utilisation.

Pricing Strategy During Market Recovery

Balancing Competitive Positioning and Profitability

Market recovery creates pricing opportunities, but premature price increases risk losing volume to competitors while excessive discounting erodes profitability needed for capacity investment. Strategic pricing requires understanding:

Market positioning: Are you the premium quality provider, the value option, or the balanced mid-market choice?

Cost structure: What are your true costs per survey including surveyor time, report production, quality control, and overhead allocation?

Competitive landscape: How do your prices compare to local competitors for equivalent survey levels?

Value differentiation: What additional services or quality factors justify premium pricing?

Understanding the cost of measured building surveys and other service types helps establish rational pricing frameworks that reflect true value delivery.

Value-Added Services and Bundling

Rather than competing solely on price, successful firms differentiate through value-added services that enhance the core survey offering:

- Detailed budgeting for repairs and restoration helping buyers understand financial implications

- Environmental issues assessment including flood risk and contamination

- Maintenance planning guidance for long-term property care

- Planning considerations for potential alterations or extensions

- Construction and condition surveys with detailed technical analysis

These services increase average transaction values while providing genuine additional value that justifies premium positioning.

Marketing and Client Acquisition Strategies

Digital Marketing for Increased Visibility

As buyer activity increases 57% and transaction momentum builds[2], digital visibility becomes critical for capturing market share. Effective strategies include:

Search engine optimisation ensuring your firm appears prominently when buyers search for "building surveyor [location]" or "property survey near me"

Content marketing providing educational resources about survey types, common defects, and property buying guidance that establishes expertise and builds trust

Google Business Profile optimisation with current information, client reviews, and service descriptions that appear in local search results

Social media presence sharing survey insights, property tips, and market commentary that demonstrates knowledge and builds brand awareness

Email marketing to past clients, estate agents, and solicitors maintaining relationships and encouraging referrals

Building Referral Networks 🌐

Estate agent relationships remain the most valuable referral source for many survey firms. Cultivating these relationships requires:

- Consistent quality that protects agent reputations

- Reliable communication about survey findings

- Reasonable turnaround times that don't delay transactions

- Professional handling of difficult conversations about property defects

- Occasional educational sessions for agent staff about survey value

Solicitor and conveyancer partnerships create additional referral channels, particularly for buyers who haven't yet selected a surveyor when instructing legal representation.

Previous client referrals from satisfied customers provide the highest-quality leads with strong conversion rates. Implementing systematic follow-up and referral request processes maximises this channel.

Preparing for the Next Phase: 12-Month Outlook

Interpreting the +35% Sales Growth Projection

The 12-month sales growth expectation of +35% represents significant optimism from RICS surveyors about market trajectory[1]. This projection suggests:

📈 Sustained volume growth rather than temporary spike

📈 Confidence in fundamental market recovery beyond seasonal fluctuations

📈 Expectation of stable or improving economic conditions supporting buyer activity

📈 Belief in pent-up demand release as deferred buyers enter the market

For survey firms, this outlook justifies strategic investment in capacity, technology, and talent rather than merely managing temporary volume fluctuations through overtime and temporary measures.

Scenario Planning for Different Recovery Trajectories

Prudent firms prepare for multiple scenarios rather than assuming a single trajectory:

Optimistic scenario (>35% growth): Requires aggressive capacity expansion, potentially including acquisitions, significant recruitment, and major technology investment

Base scenario (25-35% growth): Supports measured expansion through selective recruitment, technology enhancement, and process optimisation

Conservative scenario (10-25% growth): Suggests cautious approach with flexible capacity (associates, part-time surveyors) and minimal fixed cost increases

Downside scenario (<10% growth): Requires focus on efficiency, market share gains, and service differentiation rather than capacity expansion

Developing contingency plans for each scenario enables rapid response as actual market conditions emerge through 2026.

Long-Term Sector Sustainability

Beyond immediate volume management, the surveying profession must address long-term sustainability challenges:

Talent pipeline development ensuring sufficient qualified surveyors enter the profession to meet ongoing demand

Technology adoption preventing the profession from falling behind client expectations for digital service delivery

Professional standards evolution maintaining relevance as property types, construction methods, and regulatory requirements change

Public awareness of survey value ensuring buyers understand the importance of professional property assessment

Regulatory engagement shaping potential reforms to support professional standards while improving homebuying efficiency

These long-term considerations should inform strategic decisions made during the current recovery phase, ensuring short-term capacity expansion aligns with sustainable sector development.

Conclusion

The agreed sales recovery and building survey demand trajectory through 2026 presents the surveying profession with significant opportunity tempered by operational challenge. Agreed sales improving to -9% net balance—the strongest reading since June 2025—combined with 12-month growth expectations of +35% signals sustained transaction momentum that will drive proportional survey demand increases[1].

Successful navigation of this growth phase requires strategic capacity planning that balances surveyor resources, technology infrastructure, and quality control systems. Firms must resist the temptation to sacrifice professional standards for volume, instead investing in tools, training, and processes that enable scalable quality delivery.

Technology integration, workforce development, and operational efficiency emerge as the critical success factors. Firms that leverage digital inspection tools, cloud-based reporting platforms, and workflow management systems will handle volume increases more effectively than those relying solely on traditional methods.

The potential for regulatory reform requiring upfront property condition assessments adds strategic complexity, suggesting firms should develop flexible operational models capable of adapting to changing market structures[3].

Actionable Next Steps for Survey Firms

✅ Conduct capacity assessment evaluating current utilisation, bottlenecks, and scalability constraints

✅ Develop recruitment and training plans addressing both immediate capacity needs and long-term talent pipeline

✅ Invest in technology infrastructure enabling efficient inspection, reporting, and client communication at scale

✅ Strengthen quality control systems ensuring professional standards remain robust during volume growth

✅ Build referral relationships with estate agents, lenders, and solicitors to capture market share

✅ Monitor regulatory developments preparing operational flexibility for potential process reforms

✅ Review pricing strategies balancing competitive positioning with profitability needed for sustainable growth

The agreed sales recovery represents more than a temporary market uptick—it signals a fundamental shift in transaction momentum that will shape surveying demand throughout 2026 and beyond. Firms that prepare strategically, invest wisely, and maintain unwavering commitment to professional standards will emerge as market leaders, while those caught unprepared risk losing market share or compromising the quality that defines professional surveying value.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Uk Housing Market 2026 Renewed Momentum Strengthening Demand And Signs Of Lasting Stability – https://bhwconveyancing.com/advice/uk-housing-market-2026-renewed-momentum-strengthening-demand-and-signs-of-lasting-stability/

[3] Surveying In 2026 Reform Recovery And Renewed Demand – https://www.lrg.co.uk/news-and-insights/surveying-in-2026-reform-recovery-and-renewed-demand/