The luxury property market in 2026 faces unprecedented challenges as the government's new mansion tax looms on the horizon. Following Chancellor Rachel Reeves's Budget announcement, Post-Budget 2026 Valuation Tactics for Luxury Homes Over £2 Million: Navigating Stamp Duty and Market Shifts have become essential knowledge for property owners, buyers, and professionals navigating this transformed landscape. With valuations scheduled for 2026 and the annual council tax surcharge taking effect from April 2028, estate agents are already witnessing strategic pricing maneuvers as sellers position properties just below the critical £2 million threshold.

This seismic shift in property taxation demands a fundamental reassessment of valuation methodologies, particularly for RICS-qualified chartered surveyors tasked with delivering accurate assessments amid market distortion and affordability pressures.

Key Takeaways

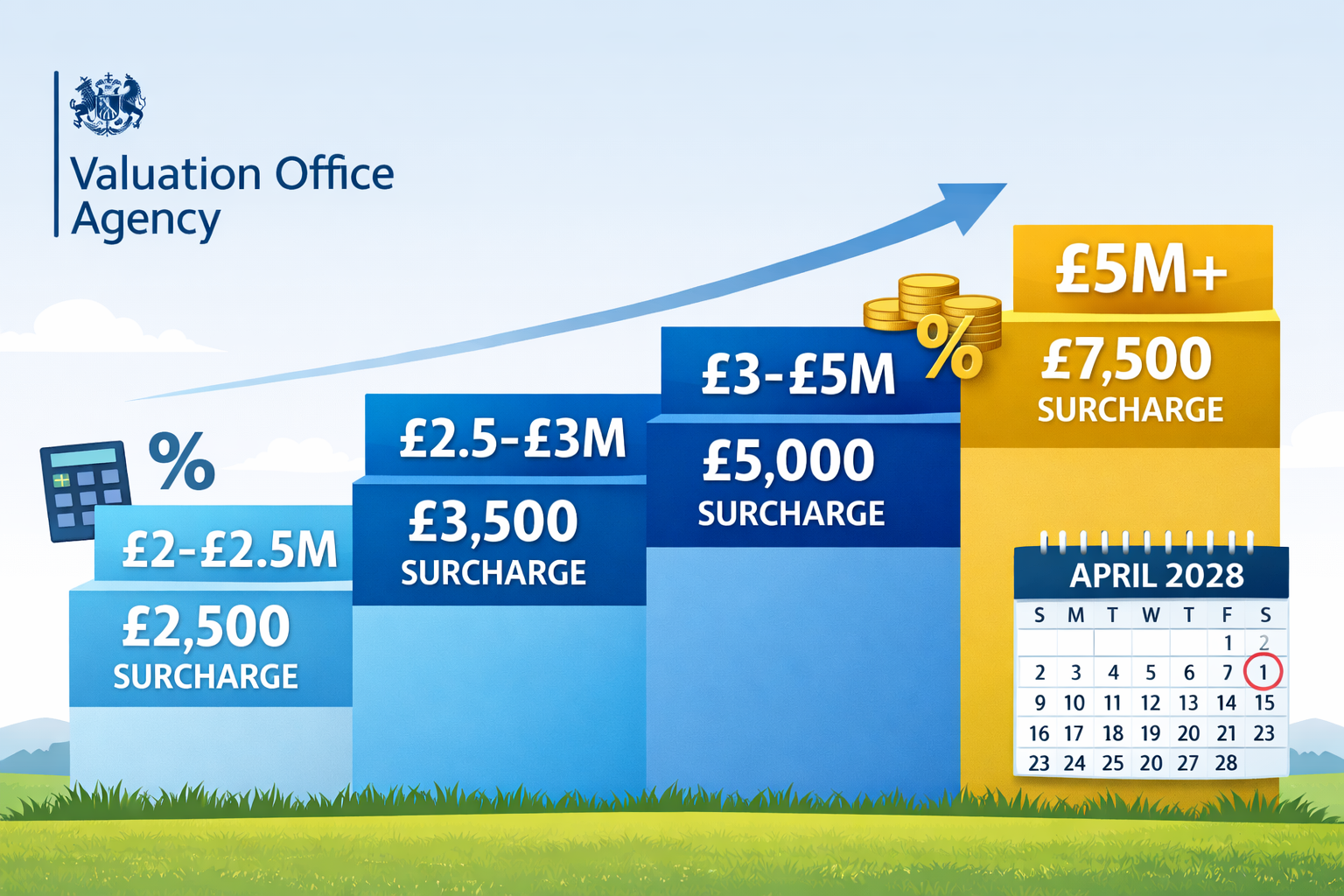

- The mansion tax introduces four price bands with annual surcharges ranging from £2,500 to £7,500 for properties valued above £2 million, with government valuations occurring in 2026 for April 2028 implementation

- London and the South East face disproportionate impact, with approximately 80% of affected properties concentrated in these regions, creating localized market distortions

- Strategic pricing below £2 million is already emerging, with sellers structuring deals at £1,999,000 and separating fixtures or land parcels to avoid the surcharge threshold

- RICS valuation methodologies require refinement to account for comparable sales analysis distortions, risk adjustments, and the behavioral impacts of cliff-edge taxation

- Market segmentation is accelerating, with demand shifting from the £2-£4 million bracket toward the £1-£1.7 million range, creating price compression and reduced liquidity

Understanding the 2026 Mansion Tax Structure and Timeline

The mansion tax represents one of the most significant changes to luxury property taxation in recent UK history. The annual council tax surcharge applies to approximately 150,000 properties valued above £2 million across England, with the Valuation Office Agency conducting official valuations throughout 2026.[1][5]

The Four-Tier Surcharge Framework

The surcharge structure creates distinct price bands that will fundamentally reshape valuation considerations:

| Property Value Range | Annual Surcharge | Market Impact |

|---|---|---|

| £2 million – £2.5 million | £2,500 | Highest concentration of affected properties |

| £2.5 million – £3 million | £3,500 | Moderate market segment |

| £3 million – £5 million | £5,000 | Upper-middle luxury bracket |

| £5 million and above | £7,500 | Ultra-prime properties |

These surcharge amounts will be uprated annually for inflation, creating ongoing valuation considerations for property owners and requiring surveyors to factor in long-term cost implications when assessing market value.[1]

Implementation Timeline and Strategic Windows

The two-year gap between the 2026 valuation exercise and the April 2028 tax implementation creates a critical strategic window. Property owners have limited time to:

- Commission professional RICS valuations to establish baseline assessments

- Implement property modifications or structural changes that might affect valuation

- Consider market timing for sales or purchases

- Explore legitimate valuation reduction strategies

Understanding property market legislation changes becomes essential for navigating this transition period effectively.

Post-Budget 2026 Valuation Tactics for Luxury Homes: RICS Methodologies Under Pressure

The mansion tax creates unprecedented challenges for chartered surveyors conducting valuations in the luxury segment. Traditional comparable sales analysis faces significant distortion as market participants respond to the £2 million threshold.

Comparable Sales Analysis in a Distorted Market

The fundamental principle of valuation—using comparable sales evidence—becomes problematic when market behavior shifts dramatically. Estate agents report clients already structuring deals to avoid the surcharge, including:

- Pricing properties at £1,999,000 to stay just below the threshold

- Separating fixtures and fittings from the sale price to reduce the property valuation

- Parceling off land or outbuildings to create separate transactions below £2 million[4]

These tactics create artificial price clustering near the threshold, making it difficult to determine genuine market value. Surveyors must now distinguish between:

- Genuine market value based on property characteristics and location

- Tax-motivated pricing designed to avoid surcharge thresholds

- Distressed pricing from sellers facing affordability pressure

Risk Adjustment Factors for 2026 Valuations

RICS-qualified surveyors must incorporate additional risk factors when assessing properties in the £1.8 million to £2.5 million range:

Market Liquidity Risk 📉

Properties priced between £2-£4 million are experiencing significant discounting, with some country properties seeing 25% price reductions even before the tax takes effect.[4] This pre-tax market softening indicates reduced buyer appetite and longer marketing periods.

Threshold Sensitivity Risk 🎯

Properties valued close to any of the four surcharge thresholds face heightened valuation scrutiny. A difference of £50,000 in assessed value could trigger an additional £1,000-£2,500 in annual tax liability.

Geographic Concentration Risk 🗺️

With 80% of affected properties located in London and the South East,[4] regional market dynamics create localized distortions that don't exist in other UK markets. Surveyors must calibrate their assessments to account for this geographic clustering.

Valuation Methodology Refinements

Professional surveyors should consider these tactical approaches when conducting property valuations:

Enhanced Comparable Selection Criteria

- Prioritize pre-announcement transactions (before Budget 2026) for baseline comparables

- Weight recent transactions lower if they show evidence of tax-motivated pricing

- Expand geographic search radius to capture genuine market movements

- Document and adjust for any separated fixtures, fittings, or land parcels

Detailed Property Component Analysis

- Separately assess land value versus improvements

- Document removable fixtures and fittings with independent valuations

- Consider potential for property subdivision or reconfiguration

- Evaluate whether ancillary structures could be separately valued

Temporal Adjustment Factors

- Apply downward adjustments to comparables from peak periods

- Account for market velocity changes in the luxury segment

- Consider seasonal variations with heightened sensitivity

- Document market sentiment shifts following Budget announcements

Market Segmentation and Strategic Positioning Around the £2 Million Threshold

The creation of a hard taxation threshold at £2 million fundamentally alters market dynamics, creating what economists call "cliff edge effects" that distort rational pricing behavior.

The Emerging Two-Tiered Market Structure

Estate agents predict demand will shift dramatically from the £2-£4 million bracket toward the £1-£1.7 million price segment, creating distinct market tiers with different characteristics:[4]

Below-Threshold Market (£1-£1.99 million)

- ✅ Increased buyer competition

- ✅ Stronger price resilience

- ✅ Faster transaction times

- ✅ Premium pricing for properties just below £2 million

Above-Threshold Market (£2+ million)

- ⚠️ Reduced buyer pool

- ⚠️ Extended marketing periods

- ⚠️ Downward price pressure

- ⚠️ Increased negotiation leverage for buyers

This bifurcation creates strategic implications for both buyers and sellers requiring sophisticated valuation approaches.

Strategic Pricing Tactics for Sellers

Property owners approaching the market in 2026 and beyond should consider these positioning strategies:

The £1.999 Million Strategy

Pricing at £1,999,000 has become increasingly common, but surveyors must ensure this pricing reflects genuine market value rather than wishful thinking. The strategy works when:

- Property genuinely falls in the £1.9-£2.1 million range based on comparables

- Fixtures and fittings can legitimately be separated (typically £50,000-£100,000)

- Minor property adjustments can justify the lower valuation

- Marketing emphasizes tax efficiency for buyers

The Premium Above-Threshold Strategy

For properties genuinely worth £2.2 million or more, attempting to price below the threshold creates credibility issues. Instead:

- Price competitively within the appropriate surcharge band

- Emphasize property features that justify the premium

- Target buyers less sensitive to the annual surcharge (£2,500-£3,500)

- Consider timing the market during periods of stronger demand

Geographic Hotspots and Valuation Challenges

The concentration of affected properties in London and the South East creates specific challenges for surveyors working in these markets. Industry experts warn the tax disproportionately impacts "London's upper-middle classes with mortgages rather than ultra-wealthy investors," as perfectly normal London properties naturally fall into the £2 million valuation range.[4]

Prime Central London

Areas like Hampstead, Fulham, and Clapham face particular challenges where standard family homes exceed £2 million. Surveyors in these areas should consult with specialists familiar with Central London market dynamics.

South East Commuter Belt

Locations in Hertfordshire, Berkshire, and Buckinghamshire see luxury properties affected by the threshold, requiring local market expertise.

Specialized Valuation Scenarios and Tax Implications

Beyond standard market valuations, the mansion tax creates specific considerations for various property transaction types and ownership scenarios.

Inheritance Tax and Estate Planning Valuations

The mansion tax adds complexity to inheritance tax valuations for luxury properties. Estate planners must now consider:

- Annual surcharge liability as an ongoing estate cost

- Valuation timing strategies to minimize both IHT and mansion tax exposure

- Property restructuring options such as splitting properties between beneficiaries

- Trust implications for properties held in family trusts

"The mansion tax signals to globally mobile wealth holders that the UK is willing to target assets when revenue is needed, with industry analysts warning this exodus of wealth will be systematic, rational and global."[4]

Matrimonial and Divorce Valuations

Matrimonial valuations require additional considerations when luxury properties are involved:

- Future tax liability allocation between divorcing parties

- Offsetting strategies where one party retains the property and assumes surcharge liability

- Timing considerations for property sales versus retention

- Valuation date selection to reflect pre- or post-tax market conditions

Leasehold Extension and Enfranchisement

For luxury leasehold properties, leasehold extension valuations must account for:

- Impact of annual surcharge on marriage value calculations

- Reduced buyer appetite affecting relativity percentages

- Landlord's position on properties near the threshold

- Strategic timing of extension applications

International Buyer Considerations and Capital Flight Concerns

The mansion tax has particular implications for international buyers and globally mobile wealth, potentially accelerating capital flight from the UK luxury property market.

Impact on Foreign Investment

International buyers face compounded taxation when purchasing UK luxury property:

- Higher stamp duty rates for non-UK residents (additional 2% surcharge)

- Annual mansion tax from 2028 onwards

- Potential capital gains tax on future sales

- Currency risk on sterling-denominated assets

Industry analysts warn this taxation stack "will not be loud at first. It will be systematic, rational and global" as international wealth reconsiders UK property investment.[4]

Comparative International Markets

Wealthy buyers increasingly compare UK taxation to alternative markets:

- Portugal and Spain: No equivalent mansion tax, attractive golden visa programs

- Dubai and Singapore: No property taxes, favorable ownership structures

- Switzerland: Wealth taxes but stable, predictable regime

- United States: State-dependent property taxes but larger luxury market

Strategic Responses from International Buyers

Surveyors working with international clients should understand these emerging strategies:

Corporate Ownership Structures

While the mansion tax applies regardless of ownership structure, international buyers explore:

- Offshore holding companies (though subject to same tax)

- Lease arrangements versus outright purchase

- Short-term occupancy rather than permanent residence

Portfolio Diversification

Rather than concentrating wealth in a single UK luxury property, international buyers increasingly:

- Purchase multiple properties below the £2 million threshold

- Diversify across multiple countries

- Shift from UK property to other asset classes

Stamp Duty Rebate Opportunities and Professional Support

While the mansion tax creates new burdens, property owners should also explore potential stamp duty rebate support for historical transactions.

Overpayment Review Opportunities

Many luxury property purchasers may have overpaid stamp duty land tax (SDLT) due to:

- Incorrect property categorization (mixed-use versus residential)

- Valuation errors in the original transaction

- Annexe or separate dwelling claims not properly pursued

- Multiple dwellings relief overlooked in complex properties

Professional surveyors can conduct retrospective reviews to identify rebate opportunities that may offset future mansion tax liabilities.

Documentation and Evidence Requirements

Successful SDLT rebate claims require robust evidence:

- Professional valuation reports supporting alternative classifications

- Architectural plans demonstrating separate dwellings

- Planning documentation for mixed-use elements

- Comparable transaction evidence

- Expert witness testimony for tribunal proceedings

Preparing Properties for Optimal Valuation Outcomes

Property owners can take proactive steps to ensure their properties achieve fair valuations while potentially positioning below critical thresholds.

Property Presentation and Documentation

Following guidance on how to prepare your property for market, owners should:

Comprehensive Property Records

- Maintain detailed records of improvements and renovations

- Document any property defects or required repairs

- Compile planning permissions and building regulation approvals

- Organize warranties and guarantees for recent work

Strategic Property Improvements

- Address deferred maintenance that might inflate replacement cost

- Consider whether recent luxury additions could be reversed or separated

- Evaluate whether outbuildings or annexes could be independently valued

- Review garden features and landscaping that contribute to overall value

Engaging Professional Valuation Services

The complexity of Post-Budget 2026 Valuation Tactics for Luxury Homes Over £2 Million: Navigating Stamp Duty and Market Shifts demands professional expertise. Property owners should:

Select RICS-Qualified Chartered Surveyors

- Verify RICS membership and professional indemnity insurance

- Seek specialists with luxury property experience

- Request evidence of recent comparable valuations in the area

- Ensure familiarity with Valuation Office Agency methodologies

Commission Pre-Emptive Valuations

- Obtain professional valuations before the official 2026 VOA assessment

- Identify potential areas for legitimate valuation reduction

- Prepare evidence for any subsequent appeals or challenges

- Document market conditions and comparable sales contemporaneously

Consider Multiple Valuation Purposes

Different valuation scenarios may require separate assessments:

- Market value for potential sale

- Tax valuation for mansion tax purposes

- Insurance reinstatement cost (which may differ significantly)

- Probate or inheritance tax valuation

Long-Term Market Outlook and Adaptive Strategies

Looking beyond the immediate 2026-2028 transition period, the mansion tax will permanently reshape the luxury property landscape.

Predicted Market Evolution

Industry experts anticipate several long-term trends:

Price Compression Near Thresholds 📊

Properties valued between £1.95 million and £2.05 million will experience the greatest pricing pressure as buyers and sellers negotiate around the cliff edge. Expect:

- Increased price volatility in threshold zones

- Extended negotiation periods

- Creative deal structuring becoming standard practice

Premium for Sub-Threshold Properties 💷

Properties offering luxury features while remaining below £2 million will command premium pricing as buyers seek to avoid the surcharge while maintaining lifestyle expectations.

Segmented Buyer Profiles 👥

The market will increasingly separate into:

- Value-conscious luxury buyers (£1.5-£1.99 million)

- Surcharge-accepting buyers (£2-£3 million)

- Ultra-prime buyers (£5 million+) for whom the capped £7,500 surcharge is immaterial

Adaptive Valuation Frameworks

Surveyors must develop adaptive frameworks that account for:

Dynamic Threshold Effects

As surcharge amounts are uprated annually for inflation, the real-terms impact changes over time. Valuation models should incorporate:

- Projected inflation rates

- Comparative annual cost analysis

- Long-term ownership cost modeling

- Break-even analysis for threshold positioning

Market Sentiment Indicators

Beyond traditional valuation metrics, surveyors should monitor:

- Transaction volumes in each price band

- Time-on-market trends across segments

- Discount rates from initial asking prices

- International buyer participation rates

Regulatory Evolution

The mansion tax framework may evolve through:

- Threshold adjustments in future budgets

- Additional surcharge bands

- Exemptions or reliefs for specific circumstances

- Changes to valuation methodologies

Conclusion: Navigating the New Luxury Property Landscape

The introduction of the mansion tax represents a fundamental shift in UK luxury property economics, requiring sophisticated Post-Budget 2026 Valuation Tactics for Luxury Homes Over £2 Million: Navigating Stamp Duty and Market Shifts from all market participants. With approximately 150,000 properties affected and 80% concentrated in London and the South East, the impact will reshape pricing dynamics, buyer behavior, and valuation methodologies for years to come.

Key Strategic Actions for Property Owners

Immediate Steps (2026)

- Commission professional RICS valuations to establish baseline assessments

- Review property structure for legitimate valuation optimization opportunities

- Explore stamp duty rebate opportunities for historical transactions

- Document all property improvements and maintenance comprehensively

Medium-Term Planning (2026-2028)

- Monitor market developments and comparable sales in your area

- Consider timing implications for any planned property transactions

- Evaluate whether property modifications might affect valuation outcomes

- Prepare evidence for potential VOA valuation appeals

Long-Term Positioning (2028 onwards)

- Incorporate annual surcharge costs into property ownership budgets

- Review estate planning and inheritance tax strategies

- Monitor regulatory changes and potential framework adjustments

- Maintain relationships with qualified surveyors for ongoing advice

The Critical Role of Professional Valuation

While the mansion tax creates challenges, it also underscores the essential value of professional surveying expertise. Accurate, defensible valuations grounded in RICS methodologies and supported by robust comparable evidence will prove invaluable as property owners navigate this transformed landscape.

The £2 million threshold may seem arbitrary, but its market impact will be profound and lasting. Those who approach valuation strategically, with professional guidance and thorough documentation, will be best positioned to optimize outcomes while ensuring compliance with the new taxation regime.

The luxury property market has always demanded sophisticated analysis and expert judgment. In 2026 and beyond, these qualities become more critical than ever as Post-Budget 2026 Valuation Tactics for Luxury Homes Over £2 Million: Navigating Stamp Duty and Market Shifts separate successful property strategies from costly missteps.

References

[1] Uk Will Now Tax Mansions Worth More Than 2 Million – https://economictimes.com/nri/invest/uk-will-now-tax-mansions-worth-more-than-2-million/articleshow/125631005.cms

[2] Uk Announces New Tax On Expensive Homes From 2028 – https://michaelwest.com.au/uk-announces-new-tax-on-expensive-homes-from-2028/

[3] Good News Lets Make The Gbp20 Million Deal Happen The Mansion Tax That Turned Out To Be The Least Worst Outcome For Prime Property And The Places That Will Be Hit – https://www.countrylife.co.uk/property/good-news-lets-make-the-gbp20-million-deal-happen-the-mansion-tax-that-turned-out-to-be-the-least-worst-outcome-for-prime-property-and-the-places-that-will-be-hit

[4] Uk Budget Introduces Mansion Tax On Homes Worth 2 Million – https://www.thenationalnews.com/news/uk/2025/11/26/uk-budget-introduces-mansion-tax-on-homes-worth-2-million/

[5] Update Property Tax Speculation Shifts Again As Budget Countdown Begins – https://www.buyassociationgroup.com/en-gb/news/update-property-tax-speculation-shifts-again-as-budget-countdown-begins/