The landscape of Britain's luxury property market has transformed dramatically in 2026. Owners of high-value residential properties across London and the South East now face unprecedented challenges as new taxation measures reshape valuations, investment strategies, and market behavior. Valuation Adjustments for High-Value Properties Over £2m: Navigating 2026 Budget Tax Changes and Market Stability has become the critical focus for property professionals, investors, and homeowners navigating this complex new environment.

The introduction of the mansion tax surcharge—officially termed the "high-value residential property annual charge"—has created seismic shifts in how properties approaching or exceeding the £2m threshold are valued, marketed, and transacted. With the Valuation Office Agency (VOA) conducting comprehensive assessments throughout 2026 that will determine five-year tax liabilities commencing April 2028, chartered surveyors are recalibrating their appraisal methodologies to account for both the direct tax burden and the market distortions already emerging.

Prime central London assets, which historically attracted consistent foreign investment inflows, now face a dual challenge: plateauing price growth in southern markets combined with substantial new annual charges that fundamentally alter investment calculations. 📊

Key Takeaways

- 2026 valuations determine five-year liability: Property assessments completed this year establish tax obligations from April 2028 through 2033, making accurate valuation critical for long-term financial planning

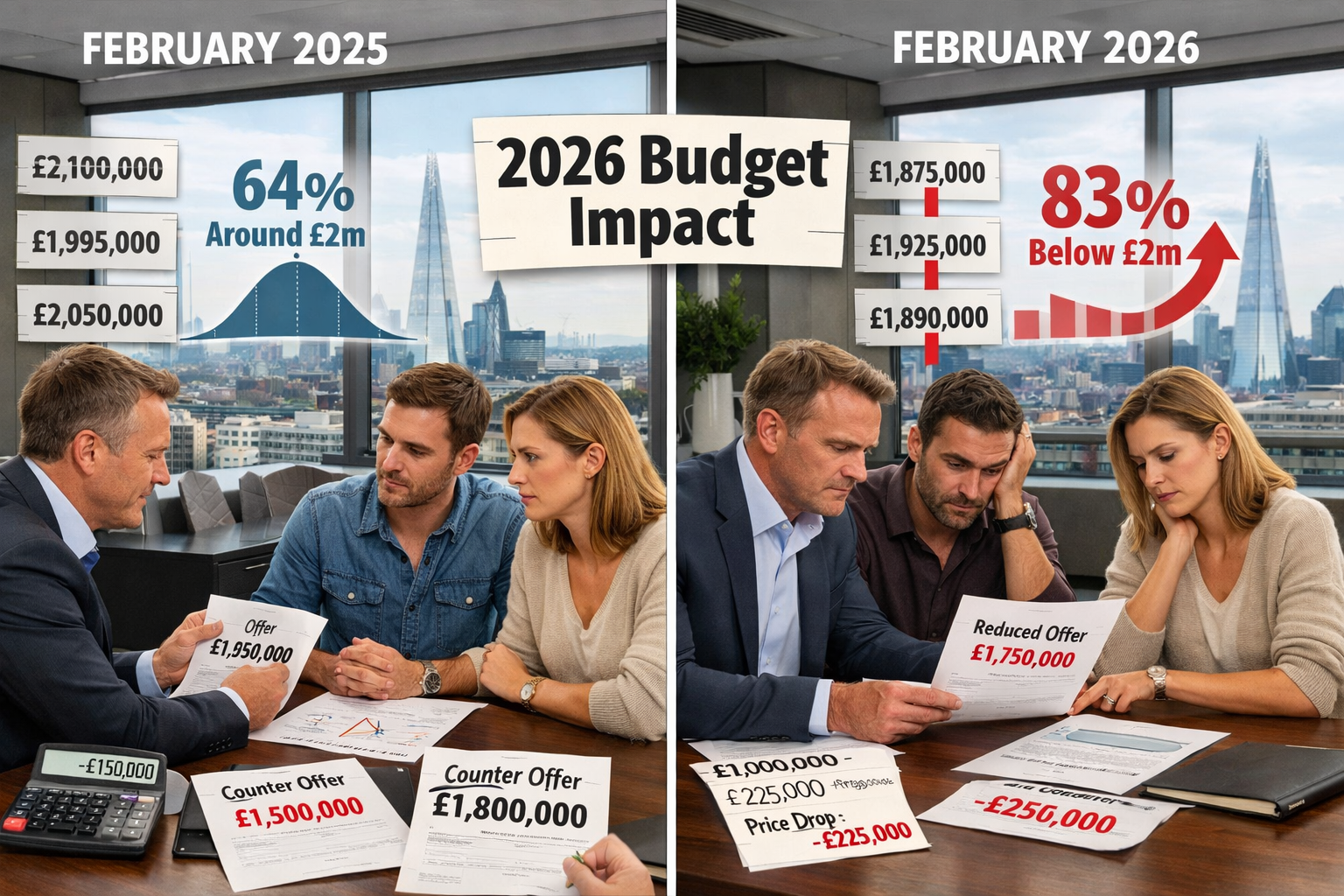

- Dramatic market behavior shifts: 83% of offers on properties near £2m now come in below the threshold, compared to just 64% in 2025, demonstrating significant "price bunching" behavior[3]

- Four-band surcharge structure: Annual charges range from £2,500 (£2m-£2.5m) to £7,500 (over £5m), with CPI-linked increases from 2029-30 onwards[2]

- VOA scrutiny extends below threshold: Properties valued as low as £1.5m will face examination to ensure accurate threshold classification[1]

- Government projects 2.5% average depreciation: Treasury analysis admits the mansion tax will reduce affected property values by an average of 2.5%, equating to approximately £50,000 on a £2m home[4]

Understanding the 2026 Mansion Tax Framework and Valuation Adjustments for High-Value Properties Over £2m

The mansion tax represents the most significant change to high-value residential property taxation in a generation. Understanding its mechanics is essential for property owners, investors, and professionals working in the luxury market.

The Four-Band Surcharge Structure

The government has implemented a tiered approach to the annual charge, creating four distinct valuation bands:

| Property Value | Annual Charge (2028-29) | Estimated 5-Year Cost |

|---|---|---|

| £2m – £2.5m | £2,500 | £12,500+ |

| £2.5m – £3m | £5,000 | £25,000+ |

| £3m – £5m | £6,000 | £30,000+ |

| Over £5m | £7,500 | £37,500+ |

These charges will increase in line with the Consumer Price Index (CPI) from the 2029-30 tax year onwards, meaning the cumulative burden will grow substantially over time[2]. For property investors conducting long-term financial modeling, these escalating costs must be factored into hold-versus-sell decisions.

Critical 2026 Valuation Timeline

The VOA is conducting comprehensive property valuations throughout 2026, with these assessments determining liability for the entire five-year period beginning April 2028[2]. This creates a critical window where property owners must:

✅ Ensure their properties are accurately valued

✅ Gather comparable transaction evidence

✅ Consider strategic improvements or modifications

✅ Prepare for potential valuation disputes

The permanence of these 2026 valuations across a five-year cycle amplifies the importance of accuracy. A property incorrectly valued £100,000 above the £2m threshold could face an additional £12,500+ in unnecessary charges through 2033.

VOA Scrutiny Extends Below the £2m Threshold

Perhaps most concerning for property owners is the VOA's confirmed intention to examine properties valued as low as £1.5m. The agency head revealed that professionals will "probably look at houses that have an indicative value of £1.5 million just to make sure we're not missing anything"[1].

This creates a £500,000 uncertainty zone where homeowners who believed themselves safely below the threshold may face unexpected scrutiny and potential reclassification. For those seeking professional valuation services, this extended examination zone makes expert assessment more critical than ever.

Market Behavior Shifts: Valuation Adjustments for High-Value Properties Over £2m in Practice

The anticipation and implementation of the mansion tax has already triggered measurable changes in market behavior, particularly in how properties near the £2m threshold are valued, negotiated, and transacted.

The Price Bunching Phenomenon

February 2026 data reveals dramatic evidence of strategic buyer behavior. A striking 83% of offers on homes priced within 10% of £2m came in below the £2m threshold, compared to just 64% a year earlier[3]. This represents a fundamental shift in negotiation dynamics.

Buyers are now:

- Aggressively negotiating downward on properties listed between £1.8m-£2.2m

- Factoring in the cumulative tax burden when making offers

- Using the tax threshold as leverage in price discussions

- Delaying purchases of properties that cannot be negotiated below £2m

This "price bunching" creates valuation challenges for chartered surveyors who must determine whether recent comparable transactions reflect genuine market value or tax-avoidance positioning.

Government-Projected Price Depression

The Treasury has publicly acknowledged that the mansion tax surcharge will reduce affected house prices by an average of 2.5%[4]. For a property valued at £2m, this translates to approximately £50,000 in value depreciation.

However, this government projection may underestimate the true impact for several reasons:

- Psychological threshold effects: Properties just above £2m may experience greater than average depreciation as buyers seek to avoid the charge entirely

- Cumulative burden perception: Sophisticated investors calculate the full five-year cost (£12,500+ minimum), which may depress willingness to pay more significantly

- Liquidity reduction: Fewer buyers willing to transact above £2m reduces market depth and price support

For those considering whether to prepare properties for market in 2026, understanding these depreciation dynamics is essential for realistic pricing.

Regional Concentration and Market Stability

The impact of Valuation Adjustments for High-Value Properties Over £2m: Navigating 2026 Budget Tax Changes and Market Stability varies dramatically by region:

London and South East Dominate Exposure

Properties in prime central London locations—including Mayfair, Belgravia, Knightsbridge, Kensington, and Chelsea—contain the greatest concentration of properties above the £2m threshold[2]. These areas face:

- Higher baseline valuations making threshold avoidance impossible

- Plateauing price growth that limits appreciation to offset tax burden

- International buyer sensitivity to additional holding costs

- Potential portfolio restructuring by institutional investors

Scotland Implements Separate Framework

The Scottish Government has confirmed plans for its own mansion tax from April 2028, applying to properties worth more than £1 million—a full £1m below the English threshold[1]. This creates regional divergence that complicates UK-wide portfolio strategies and may influence location decisions for high-net-worth individuals.

Less Than 1% of English Properties Affected

Despite the significant attention, the Treasury estimates fewer than 1% of properties in England exceed the £2m threshold[1]. This concentration means the tax functions as a highly targeted measure affecting a small but economically significant segment of the market.

RICS Methodologies and Professional Valuation Strategies for High-Value Properties Over £2m

Chartered surveyors are adapting their valuation methodologies to address the unique challenges posed by the mansion tax environment. RICS (Royal Institution of Chartered Surveyors) standards provide the framework, but practical application requires nuanced judgment.

Comparable Evidence in a Distorted Market

The traditional comparable sales approach—identifying recent transactions of similar properties—becomes problematic when:

- Strategic pricing artificially clusters transactions below £2m

- Deferred transactions reduce the volume of recent comparables

- Tax-motivated negotiations create sale prices that don't reflect underlying value

Chartered surveyors must now:

- Adjust for tax-influenced transactions: Recognize when comparable sales reflect tax avoidance rather than true market value

- Weight pre-2026 evidence appropriately: Earlier transactions may better reflect underlying value but miss recent market shifts

- Consider the "shadow" tax burden: Even if a property sells below £2m, its true market value might exceed the threshold

For inheritance tax valuations and SIPP pension valuations, this complexity demands particularly careful analysis to ensure HMRC compliance.

Ultra-High-Value Properties: Unique Challenges

Properties significantly above the £2m threshold—particularly those exceeding £5m—present distinct valuation difficulties:

Limited Comparable Transactions

Ultra-high-value properties trade infrequently, making recent comparable evidence scarce. Valuers must rely on:

- Properties in adjacent neighborhoods with different characteristics

- Older transactions requiring substantial time-based adjustments

- Properties that sold under unique circumstances (estate sales, distressed sales)

Bespoke Features and Improvements

High-value properties often include unique features—architectural significance, exceptional views, extensive renovations, luxury amenities—that complicate standardized valuation approaches. Understanding what property renovations add value becomes critical when assessing these bespoke elements.

International Buyer Considerations

Foreign investors—historically significant purchasers of prime London property—evaluate properties differently than domestic buyers. Chartered surveyors must consider:

- Currency exchange rate impacts on effective pricing

- Comparative value in international markets (New York, Hong Kong, Paris)

- Additional non-resident taxation and regulatory requirements

- Geopolitical factors affecting investment flows

Strategic Timing for Improvements and Modifications

Property owners face critical decisions about the timing of improvements that could affect 2026 valuations:

Pre-Valuation Considerations

- Defer value-adding improvements: Delay renovations, extensions, or luxury upgrades until after 2026 valuation to avoid higher tax band classification

- Accelerate value-reducing modifications: Complete any changes that might lower valuation before assessment

- Strategic presentation: Ensure property is presented in a manner that reflects accurate but not inflated value

Post-Valuation Opportunities

Once the 2026 valuation is locked in for five years, property owners gain certainty to:

- Invest in improvements without tax consequences until 2033 revaluation

- Optimize property value knowing the tax burden is fixed

- Plan long-term renovations with predictable holding costs

This creates a unique strategic window where owners just below the threshold might deliberately avoid improvements in 2026, then invest significantly in 2027-2032 to maximize value without tax penalty.

Valuation Disputes and Appeals: Preparing for Challenges

Legal experts anticipate significant disputes over valuations, particularly for properties valued within £100,000 of the £2m threshold[1]. Understanding the appeals process and preparing robust evidence is essential.

Common Grounds for Dispute

Property owners may challenge VOA valuations based on:

- Incorrect comparable selection: VOA used properties that aren't truly comparable

- Failure to account for defects: Structural issues, required repairs, or adverse factors not properly considered

- Market timing errors: Valuation doesn't reflect market conditions at the assessment date

- Unique property characteristics: Special features or limitations not adequately weighted

For properties with structural concerns, a comprehensive building survey can provide essential evidence of defects that should reduce valuation.

Building a Strong Appeals Case

Successful valuation appeals require:

Professional Valuation Report

Engage a RICS-qualified chartered surveyor to prepare an independent valuation report that:

- Uses robust comparable evidence

- Applies appropriate valuation methodologies

- Documents property-specific factors affecting value

- Provides clear reasoning for conclusions

Comprehensive Property Documentation

Gather evidence including:

- Recent survey reports highlighting defects

- Repair cost estimates for identified issues

- Planning restrictions or conservation area limitations

- Evidence of market conditions and recent local transactions

Timely Submission

Appeals must be submitted within specified timeframes. Missing deadlines can forfeit the right to challenge, locking in an inflated valuation for five years.

The Cost-Benefit Analysis of Appeals

Challenging a valuation involves professional fees, time, and potential stress. Property owners should evaluate:

- Potential savings: Moving from £2.05m to £1.95m saves £12,500+ over five years

- Professional costs: Chartered surveyor reports and potential legal fees

- Probability of success: Strength of evidence and grounds for dispute

- Time investment: Preparation and potential hearing attendance

For properties within £100,000 of any band threshold, the potential savings often justify professional representation.

Case Studies: Valuation Adjustments for High-Value Properties Over £2m in Stabilizing Markets

Examining real-world scenarios illustrates how the mansion tax impacts different property types and owner situations in the context of market stability.

Case Study 1: Georgian Townhouse in Kensington (£2.1m Valuation)

Property Profile:

- Four-bedroom Georgian townhouse

- Prime Kensington location

- Listed building with period features

- Purchased in 2022 for £2.3m

2026 Challenges:

The property's 2026 valuation came in at £2.1m—reflecting both the government's projected 2.5% depreciation and broader market softening in prime central London. Despite being valued below the original purchase price, the property remains above the £2m threshold.

Owner Strategy:

The owner commissioned an independent RICS valuation highlighting:

- Extensive deferred maintenance (estimated £75,000)

- Listed building restrictions limiting modernization

- Comparable sales in adjacent streets at £1.85m-£1.95m

Outcome:

The VOA reduced the valuation to £1.98m based on documented repair requirements and appropriate comparable evidence, saving the owner £12,500+ over five years.

Key Lesson: Even properties in prime locations can successfully challenge valuations with robust evidence of defects and appropriate comparables.

Case Study 2: Modern Luxury Apartment in Battersea (£1.95m Valuation)

Property Profile:

- Three-bedroom luxury apartment

- New development completed 2024

- River Thames views

- Original purchase price £2.05m

2026 Challenges:

The property's 2026 valuation came in at £1.95m, reflecting the significant price bunching phenomenon in the Battersea market. The owner had been concerned about crossing the £2m threshold.

Owner Strategy:

Rather than challenging the valuation, the owner:

- Accepted the £1.95m assessment

- Planned significant interior improvements for 2027

- Locked in below-threshold status for five years

Outcome:

The owner will invest £100,000 in luxury upgrades in 2027-2028, potentially increasing market value to £2.2m+ while maintaining the fixed £1.95m tax valuation through 2033.

Key Lesson: The five-year valuation lock creates strategic opportunities for value-adding improvements without tax consequences.

For those considering property investments in areas like Battersea, understanding these strategic timing opportunities is crucial.

Case Study 3: Country Estate in Hampshire (£4.8m Valuation)

Property Profile:

- Historic country house with 15 acres

- Six bedrooms, multiple outbuildings

- Grade II listed

- Limited recent comparable sales

2026 Challenges:

Ultra-high-value properties with unique characteristics and limited comparables face particular valuation difficulties. The VOA's initial assessment of £5.2m would have placed the property in the highest tax band (£7,500 annually).

Owner Strategy:

The owner engaged specialists in heritage property valuations who:

- Identified comparable country estates in Hampshire and surrounding counties

- Documented extensive maintenance requirements for listed building

- Provided evidence of market softening for large country properties

- Highlighted limited buyer pool for properties of this scale

Outcome:

The VOA accepted a revised valuation of £4.8m, placing the property in the £3m-£5m band (£6,000 annually) rather than the over-£5m band, saving £1,500 annually or £7,500+ over five years.

Key Lesson: For ultra-high-value properties, specialist valuation expertise in the specific property type is essential for accurate assessment.

Investment Implications and Portfolio Strategy Adjustments

For property investors and portfolio managers, Valuation Adjustments for High-Value Properties Over £2m: Navigating 2026 Budget Tax Changes and Market Stability requires fundamental reassessment of acquisition, holding, and disposal strategies.

Modeling Cumulative Long-Term Costs

Sophisticated investors must project likely 2026 valuations and calculate cumulative holding costs across multiple valuation cycles[2]. This requires:

Five-Year Cost Projection (2028-2033)

For a property valued at £2.2m:

- Base annual charge: £2,500

- Estimated CPI increases (2029-2033): 2% annually

- Total five-year cost: approximately £13,000

Ten-Year Cost Projection (2028-2038)

Assuming the property remains in the same band at 2033 revaluation:

- Years 1-5: £13,000

- Years 6-10: £14,000+ (accounting for CPI escalation)

- Total ten-year cost: approximately £27,000+

These cumulative costs must be incorporated into:

- Yield calculations for rental properties

- Capital appreciation projections for investment holdings

- Exit strategy timing to optimize after-tax returns

For guidance on property investment strategies, understanding these long-term cost implications is fundamental.

Restructuring Strategies

Investors are employing various strategies to optimize portfolio structure:

1. Strategic Disposals

- Selling properties just above £2m where tax burden exceeds expected appreciation

- Reallocating capital to multiple properties below threshold

- Exiting markets with plateauing growth (prime central London) for higher-growth regions

2. Portfolio Rebalancing

- Increasing allocation to properties comfortably below £2m

- Concentrating ultra-high-value holdings where tax is unavoidable but properties offer superior returns

- Avoiding the £1.9m-£2.1m "danger zone" where small valuation changes trigger significant tax consequences

3. Ownership Structure Modifications

- Reviewing corporate versus personal ownership structures

- Considering trust arrangements for estate planning purposes

- Evaluating partnership structures to distribute tax burden

Important: Any ownership restructuring should be undertaken with professional tax and legal advice to ensure compliance and optimization.

Regional Market Dynamics: London, South East, and Beyond

The impact of valuation adjustments varies significantly by region, with London and the South East experiencing the most pronounced effects.

Prime Central London: Plateauing Prices Meet New Taxation

Prime central London neighborhoods have historically commanded premium valuations driven by:

- International buyer demand

- Limited supply of prestigious addresses

- Cultural and economic centrality

- Prestige and status considerations

However, 2026 presents a challenging confluence of factors:

Plateauing Price Growth

After years of rapid appreciation, prime central London has experienced:

- Stagnant or modest price growth (0-2% annually)

- Reduced international investment flows

- Brexit-related uncertainty affecting European buyers

- Competition from other global cities

Concentration of Affected Properties

Neighborhoods including Mayfair, Belgravia, Knightsbridge, Kensington, and Chelsea contain the highest concentration of properties above £2m[2], meaning:

- Virtually all properties face the mansion tax

- Buyers in these markets must accept the additional cost

- The tax becomes a "cost of entry" for prime addresses

Strategic Implications

For properties in prime central London:

- Accept the tax burden as unavoidable for desired locations

- Focus on properties offering superior long-term value to offset tax costs

- Consider rental yield as increasingly important versus pure capital appreciation

- Evaluate alternatives in emerging prime locations (Battersea, King's Cross) where values may be below threshold

South East: The £2m Threshold Zone

The South East contains numerous properties clustered around the £2m threshold, creating maximum sensitivity to valuation adjustments. Areas including parts of Surrey, Berkshire, and Buckinghamshire face:

High Valuation Volatility

Properties in the £1.8m-£2.2m range experience:

- Significant negotiation pressure from buyers

- Price bunching behavior as sellers reduce asking prices

- Valuation uncertainty during the 2026 assessment period

Strategic Buyer Behavior

Buyers in these markets are:

- Targeting properties with clear headroom below £2m

- Negotiating aggressively on properties near the threshold

- Delaying purchases until post-2026 valuation certainty

For those working with chartered surveyors in areas like Buckinghamshire or Guildford, understanding these local market dynamics is essential for accurate valuation.

Scotland: The £1m Threshold Creates Different Dynamics

Scotland's separate mansion tax threshold of £1m (effective April 2028) creates entirely different market dynamics[1]:

Broader Market Impact

- Significantly more properties affected than in England

- Greater proportion of "ordinary" family homes subject to charge

- Different buyer psychology around the lower threshold

Cross-Border Considerations

High-net-worth individuals with flexibility in location may:

- Favor English locations for primary residences (£2m threshold vs £1m)

- Consider tax implications in multi-property portfolio decisions

- Evaluate overall tax burden including income tax, property tax, and other Scottish tax policies

Preparing for 2026 Valuations: Practical Steps for Property Owners

With 2026 valuations determining five-year tax liabilities, property owners should take proactive steps to ensure accurate assessment.

Step 1: Obtain Independent Professional Valuation

Engage a RICS-qualified chartered surveyor to provide an independent valuation that:

- Uses current market evidence and appropriate comparables

- Identifies any property defects or issues that should reduce value

- Provides a defensible valuation methodology

- Serves as baseline for challenging VOA assessment if necessary

Professional valuation services provide both peace of mind and potential savings if the VOA assessment differs significantly.

Step 2: Document Property Condition and Defects

Comprehensive documentation of property condition is essential:

- Commission a building survey to identify structural issues, required repairs, and deferred maintenance

- Obtain repair cost estimates from qualified contractors

- Photograph defects and maintain dated records

- Gather historical maintenance records showing ongoing issues

This documentation becomes critical evidence if challenging a valuation that doesn't adequately account for property condition.

Step 3: Research Comparable Sales Evidence

Property owners should:

- Identify recent sales of similar properties in the immediate area

- Note sale prices, dates, and property characteristics

- Understand how their property compares to recent transactions

- Recognize any unique factors affecting their property's value

This research helps owners evaluate whether the VOA assessment is reasonable and provides evidence for potential challenges.

Step 4: Consider Strategic Timing of Improvements

As discussed earlier, timing of property improvements can significantly impact 2026 valuations:

Defer if Near Threshold:

- Delay extensions, luxury upgrades, or major renovations until after 2026 valuation

- Maintain property in good condition but avoid value-adding improvements

- Plan significant investments for 2027-2032 to benefit from locked-in valuation

Accelerate if Beneficial:

- Complete any modifications that might reduce value before assessment

- Address any issues that could justify lower valuation

- Ensure property is presented accurately but not optimally during valuation period

Step 5: Understand Appeals Process and Deadlines

Property owners should:

- Familiarize themselves with VOA appeals procedures

- Note critical deadlines for challenging valuations

- Prepare appeals documentation in advance

- Engage professional representation for significant disputes

Missing appeals deadlines can lock in unfavorable valuations for five years, making timely action essential.

The Role of Chartered Surveyors in Navigating 2026 Changes

Professional chartered surveyors play a critical role in helping property owners, buyers, and investors navigate the complexities of Valuation Adjustments for High-Value Properties Over £2m: Navigating 2026 Budget Tax Changes and Market Stability.

Expert Valuation Methodology

RICS-qualified surveyors bring:

- Professional standards and ethics ensuring objective, defensible valuations

- Market knowledge and experience understanding local market dynamics and appropriate comparables

- Technical expertise in valuation methodologies appropriate for different property types

- Regulatory understanding of VOA requirements and appeals processes

Strategic Advisory Services

Beyond pure valuation, chartered surveyors provide:

Pre-Purchase Advice

- Evaluating properties considering tax implications

- Identifying properties with valuation risk near thresholds

- Advising on negotiation strategies in the current market

Portfolio Optimization

- Reviewing existing property holdings for tax efficiency

- Identifying disposal candidates where tax burden exceeds returns

- Recommending acquisition strategies aligned with new tax environment

Dispute Resolution

- Preparing professional valuation reports for VOA challenges

- Representing owners in appeals processes

- Negotiating with VOA on behalf of clients

For comprehensive support navigating these changes, engaging experienced chartered surveyors provides essential expertise and advocacy.

Future Outlook: Beyond 2026 and the Next Valuation Cycle

While 2026 valuations determine liabilities through 2033, property owners and investors must consider longer-term implications.

The 2033 Revaluation Cycle

The next comprehensive valuation cycle in 2033 will:

- Reassess all properties based on 2033 market values

- Potentially reclassify properties into different tax bands

- Create a new five-year liability period (2033-2038)

Strategic Considerations:

Properties improved between 2027-2032 will face higher valuations in 2033, meaning:

- Timing of major improvements should consider proximity to next valuation cycle

- Properties approaching band thresholds in 2033 may benefit from deferring improvements until 2034

- Long-term investment planning must account for multiple valuation cycles

Potential Policy Evolution

The mansion tax framework may evolve through:

Threshold Adjustments

- Thresholds could be increased (or decreased) in future budgets

- CPI-linking from 2029 onwards creates automatic charge increases

- Political pressure may influence future threshold levels

Band Structure Modifications

- Additional bands could be introduced

- Charge levels within bands may be adjusted

- Regional variations might be implemented

Broader Property Tax Reform

The mansion tax exists within a broader context of potential property tax reform, including:

- Ongoing debates about council tax revaluation

- Discussions of wealth taxes on property holdings

- Potential changes to stamp duty, capital gains tax, or inheritance tax

Property investors must maintain flexibility to adapt to evolving tax policy while making decisions based on current known frameworks.

Conclusion: Navigating Valuation Adjustments for High-Value Properties Over £2m with Confidence

The 2026 mansion tax represents a fundamental shift in the high-value property landscape. Valuation Adjustments for High-Value Properties Over £2m: Navigating 2026 Budget Tax Changes and Market Stability requires property owners, investors, and professionals to adapt strategies, methodologies, and expectations.

Key Strategic Imperatives

For Property Owners:

✅ Obtain professional valuations to establish accurate baseline assessments

✅ Document property condition comprehensively to support potential appeals

✅ Time improvements strategically to optimize tax implications

✅ Understand appeals processes and prepare to challenge unfair assessments

✅ Plan for long-term holding costs incorporating cumulative tax burden

For Property Investors:

✅ Recalibrate investment models to account for ongoing tax charges

✅ Avoid the threshold danger zone (£1.9m-£2.1m) where small changes trigger significant tax

✅ Consider portfolio restructuring to optimize tax efficiency

✅ Focus on total return including tax costs, not just capital appreciation

✅ Maintain regional diversification recognizing different impacts across markets

For Property Professionals:

✅ Apply rigorous RICS methodologies adapted to tax-distorted market conditions

✅ Provide strategic advisory services beyond pure valuation

✅ Build robust comparable evidence accounting for tax-influenced transactions

✅ Support clients through appeals with professional representation

✅ Stay informed on policy evolution and emerging market dynamics

Taking Action in 2026

The window for influencing 2026 valuations is limited. Property owners and investors should act now to:

- Engage professional chartered surveyors for independent valuations and strategic advice

- Review property portfolios for optimization opportunities

- Prepare comprehensive documentation supporting accurate valuations

- Develop long-term strategies accounting for multiple valuation cycles

- Monitor market developments and policy changes affecting valuations

The mansion tax has already reshaped market behavior, with 83% of offers near £2m now coming in below the threshold[3]. This dramatic shift demonstrates the tax's profound impact on buyer psychology and negotiation dynamics.

For properties in prime central London where the tax is unavoidable, focus shifts to maximizing long-term value to offset the additional holding costs. For properties near thresholds in the South East and beyond, strategic positioning and robust valuation evidence become critical.

The stabilizing market conditions in southern England—characterized by modest growth rather than rapid appreciation—make the annual tax charges more significant as a proportion of total returns. This environment rewards careful planning, professional guidance, and strategic decision-making.

By understanding the valuation methodologies, market dynamics, and strategic opportunities outlined in this guide, property stakeholders can navigate the 2026 changes with confidence and optimize outcomes in this new taxation landscape.

References

[1] Mansion Tax Home Valuations – https://moneyweek.com/personal-finance/tax/mansion-tax-home-valuations

[2] Implications Of The Mansion Tax For High Value Residential Property Owners And Investors – https://www.barnes-law.co.uk/blogs-and-articles/implications-of-the-mansion-tax-for-high-value-residential-property-owners-and-investors

[3] Post Budget 2026 Valuation Challenges Surveyor Strategies For High Value Properties Over 2 Million – https://nottinghillsurveyors.com/blog/post-budget-2026-valuation-challenges-surveyor-strategies-for-high-value-properties-over-2-million

[4] mpamag – https://www.mpamag.com/uk/news/general/mansion-tax-to-cut-50000-from-2m-homes/559842