}

The UK housing market is showing renewed strength in early 2026, with buyer enquiries climbing and confidence returning after years of uncertainty. For first-time buyers, this recovery presents both opportunity and challenge. While mortgage rates have stabilised and lending criteria have loosened, Building Surveys for First-Time Buyers in a Recovering Market: Addressing Affordability Pressures and Hidden Costs in 2026 has never been more critical. As property prices jumped 2.8% in January 2026—the largest increase for that month on record—understanding what lies beneath the surface of a potential purchase can mean the difference between a dream home and a financial nightmare.[2]

First-time buyers are re-entering the market in significant numbers, with activity levels above the long-run average throughout 2025 and continuing into 2026.[2] However, with asking prices rising and affordability still stretched, every pound counts. A comprehensive building survey doesn't just identify problems—it uncovers opportunities to negotiate, budget accurately, and avoid catastrophic hidden costs that could derail homeownership dreams.

Key Takeaways

✅ Market recovery brings opportunity and risk: Buyer enquiries increased by 15% net balance in January 2026, but rising prices mean first-time buyers must scrutinise every purchase carefully to avoid overpaying for properties with hidden defects.

✅ Building surveys deliver negotiating power: Identifying structural issues, damp problems, or outdated systems can reduce purchase prices by £10,000-£30,000 or more, offsetting survey costs many times over.

✅ Hidden costs can exceed deposits: Unexpected repairs for roof failures, subsidence, or electrical rewiring can cost £15,000-£50,000—potentially more than a first-time buyer's entire deposit.

✅ Survey type matters for budget protection: Choosing between Level 1, Level 2, and Level 3 surveys affects both upfront costs and long-term financial security, with comprehensive surveys essential for older or non-standard properties.

✅ Professional surveys enable informed decisions: With mortgage rates averaging 4.91% and first-time buyers spending 20-25% of household income on payments, understanding total ownership costs before committing is financially essential.[2][3]

Understanding the 2026 Housing Market Recovery and Its Impact on First-Time Buyers

Market Fundamentals Driving the Recovery

The opening weeks of 2026 have demonstrated remarkable resilience in the UK housing market. Industry data shows increased enquiries from prospective buyers and a rise in agreed sales compared with the final quarter of 2025.[1] This recovery stems from several converging factors that have restored confidence among both buyers and sellers.

Mortgage rate stabilisation has been particularly significant. As of January 23, 2026, the average UK mortgage rate stood at 4.91%, with two-year fixed rates at 4.86% and five-year fixed rates at 4.94%.[2] More importantly for first-time buyers, best-buy deals have become increasingly competitive, with two-year fixed rates available at 3.50% and five-year fixed rates at 3.72% as of January 30, 2026.[2]

This pricing stability represents a dramatic shift from the volatility of previous years. When mortgage costs become predictable, buyers can plan purchases with greater confidence, and lenders can offer more favourable terms. The result has been a measurable increase in market activity, particularly among first-time buyers who had been priced out during periods of higher rates.

Affordability Pressures Despite Improved Conditions

While market conditions have improved, affordability remains a central concern. Rightmove reported a 2.8% jump in asking prices in January 2026, the largest increase for that month on record.[2] This price acceleration, occurring simultaneously with increased buyer activity, creates a challenging dynamic for first-time buyers entering the market.

First-time buyers are currently spending approximately 20-25% of gross household income on mortgage payments, according to UK Finance data from 2025.[3] While this represents an improvement from peak affordability pressures—with the house price-to-income ratio reaching its lowest point in over a decade in December 2025[2]—it still represents a significant financial commitment.

Expert forecasts for 2026 vary but generally predict modest growth. Halifax forecasts 1-3% price growth, Nationwide predicts 2-4%, and Savills expects around 2%.[2] These projections suggest prices will continue rising, making early 2026 a potentially advantageous time for first-time buyers to enter the market before further appreciation occurs.

Why Building Surveys Matter More in a Recovering Market

In a rising market, the temptation to move quickly and skip due diligence intensifies. Competition for desirable properties increases, and buyers may feel pressured to make offers without thorough investigation. This environment makes Building Surveys for First-Time Buyers in a Recovering Market: Addressing Affordability Pressures and Hidden Costs in 2026 absolutely essential.

Property tax changes introduced in the Autumn Budget 2025 are leading to sales among professional investors, freeing up housing stock.[2] While this increases available properties, it also means more rental properties—potentially with deferred maintenance—are entering the market. First-time buyers purchasing former rental properties face particular risks without comprehensive surveys.

House prices have shown resilience with modest price movements rather than widespread declines, helping restore confidence among homeowners.[1] However, this price stability can mask individual property issues. A structurally sound property in a good location may justify current asking prices, while a property with hidden defects may be overvalued by tens of thousands of pounds.

Understanding which building survey you need becomes crucial in this environment. The right survey type can reveal whether a property represents genuine value or a costly mistake.

The True Cost of Building Surveys for First-Time Buyers in a Recovering Market: Addressing Affordability Pressures and Hidden Costs in 2026

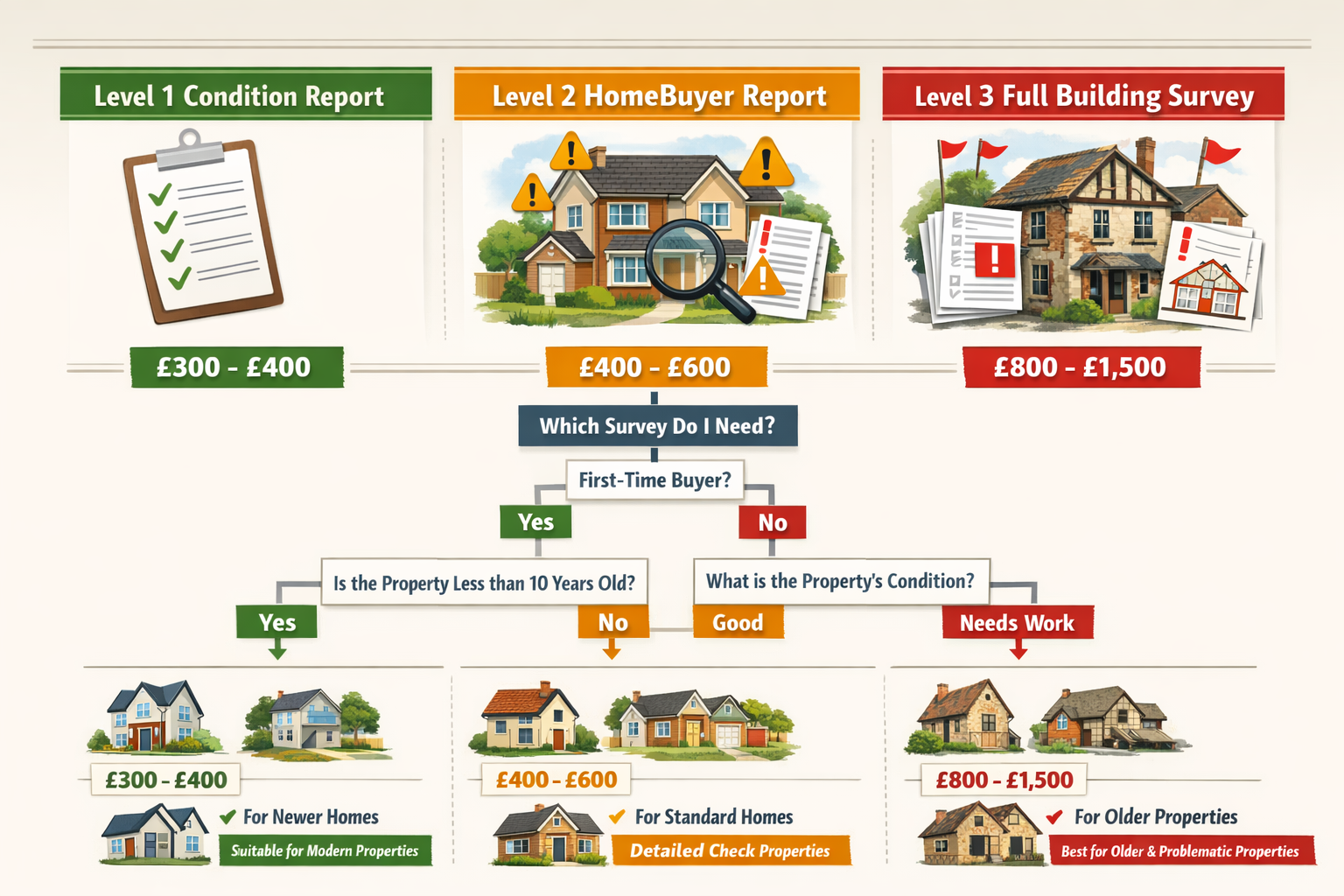

Survey Types and Associated Costs

Understanding the different survey levels and their costs helps first-time buyers make informed decisions about which option provides the best value for their specific circumstances.

| Survey Type | Typical Cost | Property Suitability | Key Features |

|---|---|---|---|

| Level 1 (Condition Report) | £300-£400 | New builds, modern properties in good condition | Basic condition assessment, traffic light rating system, no valuation |

| Level 2 (HomeBuyer Report) | £400-£600 | Standard properties built post-1900 in reasonable condition | Detailed inspection, defect identification, market valuation, repair advice |

| Level 3 (Full Building Survey) | £800-£1,500+ | Older properties, listed buildings, properties requiring renovation | Comprehensive structural analysis, detailed defect reporting, extensive advice on repairs and maintenance |

The cost of a measured building survey varies based on property size, location, and complexity. For a typical three-bedroom semi-detached house valued at £300,000, first-time buyers should budget:

- £350-£450 for a Level 1 Condition Report

- £500-£650 for a Level 2 HomeBuyer Report

- £900-£1,200 for a Level 3 Full Building Survey

While these costs may seem substantial for buyers already stretching their budgets, they represent a tiny fraction of the purchase price—typically 0.15-0.4%—and can identify issues worth tens of thousands of pounds.

Hidden Costs That Surveys Uncover

The true value of building surveys lies in their ability to reveal hidden costs that could devastate a first-time buyer's finances. Consider these common findings and their associated repair costs:

Structural Issues:

- Subsidence or settlement: £5,000-£50,000+ for underpinning and repairs

- Roof structure problems: £8,000-£25,000 for major repairs or replacement

- Wall tie failure: £2,000-£8,000 for replacement and repointing

Damp and Water Damage:

- Rising damp treatment: £1,500-£4,000 depending on extent

- Penetrating damp repairs: £2,000-£8,000 including external works

- Condensation and mould remediation: £500-£3,000 plus ventilation improvements

Electrical and Plumbing:

- Complete rewiring: £3,000-£6,000 for a three-bedroom house

- Consumer unit replacement: £400-£800

- Plumbing system replacement: £2,500-£5,000

- Boiler replacement: £2,000-£4,000

Roofing:

- Roof covering replacement: £5,000-£12,000 for tiles or slates

- Flat roof replacement: £3,000-£8,000

- Chimney repairs: £1,000-£5,000

A comprehensive survey identifying even two or three major issues can justify its cost immediately. For example, discovering that a property requires £8,000 in roof repairs and £3,500 for rewiring provides powerful negotiating leverage—potentially reducing the purchase price by £10,000-£15,000 or more.

Understanding building problems and their solutions helps first-time buyers assess whether identified issues are manageable or deal-breakers.

The ROI of Comprehensive Surveys

First-time buyers often question whether investing in a Level 3 Full Building Survey justifies the additional cost compared to a basic Level 1 or Level 2 survey. The return on investment becomes clear when examining real-world scenarios:

Scenario 1: The Victorian Terrace

Purchase price: £325,000

Survey cost: £1,100 (Level 3)

Issues identified: Roof nearing end of life (£9,000), damp in rear extension (£3,500), outdated electrical system (£4,000)

Negotiated price reduction: £12,000

Net benefit: £10,900

Scenario 2: The 1930s Semi

Purchase price: £285,000

Survey cost: £550 (Level 2)

Issues identified: Minor damp, some roof tile slippage

Estimated repairs: £2,500

Negotiated price reduction: £2,000

Net benefit: £1,450

Scenario 3: The Avoided Disaster

Purchase price: £310,000

Survey cost: £1,050 (Level 3)

Issues identified: Active subsidence, structural movement, estimated repairs £35,000+

Decision: Purchase abandoned

Net benefit: Avoided catastrophic financial loss

The full building survey versus homebuyer survey comparison demonstrates how choosing the appropriate survey level protects first-time buyers from expensive mistakes.

Timing and Process Considerations

Understanding how long a building survey takes helps first-time buyers plan their purchase timeline effectively. Typically:

- Level 1 surveys: 1-2 hours on-site, report within 3-5 working days

- Level 2 surveys: 2-4 hours on-site, report within 5-7 working days

- Level 3 surveys: 4-8 hours on-site, report within 7-10 working days

In the competitive 2026 market, timing matters. Buyers should commission surveys immediately after offers are accepted to avoid delays that might jeopardise the purchase. Many surveyors now offer expedited services for additional fees, delivering reports within 48-72 hours when necessary.

The survey process also requires vendor cooperation for access. Understanding building surveyor access requirements ensures smooth scheduling and comprehensive inspections.

Strategic Use of Building Surveys to Address Affordability Pressures

Negotiating Power and Price Reductions

One of the most valuable aspects of building surveys for first-time buyers in 2026 is the negotiating leverage they provide. In a recovering market where prices are rising, the ability to negotiate based on objective professional findings can save thousands of pounds.

Effective Negotiation Strategies:

🔍 Present evidence systematically: Rather than simply requesting a price reduction, present the survey findings with cost estimates for required repairs. This transforms a subjective negotiation into an objective discussion about property condition.

💰 Prioritise critical defects: Focus negotiations on structural issues, safety concerns, and major system failures rather than cosmetic problems. Sellers are more likely to negotiate on genuine defects than aesthetic preferences.

📊 Request multiple remedies: Consider negotiating for repairs to be completed before completion, price reductions, or retention amounts held in escrow. Different sellers respond to different approaches.

⏰ Time negotiations appropriately: Present survey findings promptly but allow sellers time to consider options. Rushed ultimatums often backfire in competitive markets.

Learning how to negotiate house prices down after a survey provides first-time buyers with specific tactics for different scenarios.

Budgeting for Repairs and Restoration

Beyond negotiating purchase prices, building surveys enable accurate budgeting for post-purchase work. First-time buyers typically have limited reserves after paying deposits and transaction costs, making accurate repair budgeting essential.

A comprehensive survey provides:

Immediate Priority Repairs (Year 1):

- Safety-critical issues (electrical hazards, structural instability)

- Weather protection (roof leaks, broken windows)

- Security concerns (faulty locks, vulnerable access points)

- Estimated budget: £3,000-£15,000 depending on findings

Medium-Term Maintenance (Years 2-5):

- System replacements (boiler, consumer unit)

- Preventative treatments (timber treatment, damp-proofing)

- External decoration and weatherproofing

- Estimated budget: £5,000-£20,000 spread over period

Long-Term Planning (Years 5-10):

- Major component replacement (roof covering, windows)

- Significant improvements (insulation, heating system upgrades)

- Structural works if identified as future concerns

- Estimated budget: £10,000-£40,000 spread over period

Understanding budgeting for repairs and restoration helps first-time buyers plan financially for the entire ownership period, not just the purchase.

Identifying Properties That Offer True Value

In a market where prices are rising 2-4% annually, identifying properties that offer genuine value becomes increasingly important. Building surveys help first-time buyers distinguish between properties that justify their asking prices and those that are overvalued relative to their condition.

Value Indicators to Assess:

✅ Structural soundness: Properties with solid foundations, stable walls, and sound roofs retain value better than those with deferred structural maintenance.

✅ Modern systems: Updated electrical, plumbing, and heating systems reduce near-term capital expenditure and improve energy efficiency.

✅ Preventative maintenance: Properties showing evidence of regular maintenance typically have fewer hidden problems and better long-term prospects.

✅ Appropriate improvements: Quality renovations using proper materials and techniques add value; poor-quality DIY work often creates problems.

❌ Red flags indicating poor value:

- Multiple structural issues requiring immediate attention

- Evidence of water ingress or long-term damp problems

- Outdated or dangerous electrical installations

- Roof coverings at or beyond their design life

- Signs of subsidence or significant structural movement

A Level 3 survey provides detailed analysis of these factors, enabling first-time buyers to make informed decisions about whether a property represents good value at its asking price.

Leveraging Survey Findings for Mortgage Applications

Building surveys can also influence mortgage applications, particularly for properties requiring significant work. Mortgage lenders conduct their own valuations, but comprehensive survey reports can:

Support mortgage applications by:

- Demonstrating buyer awareness of property condition

- Providing evidence for retention amounts if repairs are needed

- Justifying lower valuations if significant defects exist

- Supporting applications for renovation mortgages or additional borrowing

Prevent mortgage problems by:

- Identifying issues that might cause lender valuations to fall short

- Revealing defects that could make properties unmortgageable

- Highlighting safety issues that must be addressed before completion

First-time buyers should share survey findings with mortgage brokers and lenders early in the process. This transparency can prevent last-minute surprises that derail purchases or force renegotiations under time pressure.

Advanced Considerations: Building Surveys for First-Time Buyers in a Recovering Market: Addressing Affordability Pressures and Hidden Costs in 2026

Specialist Surveys and Additional Investigations

Comprehensive building surveys often identify areas requiring specialist investigation. Understanding when to commission additional surveys helps first-time buyers avoid unexpected costs after purchase.

Common Additional Investigations:

Structural Engineering Reports: Required when surveys identify significant cracking, movement, or structural instability. Costs: £500-£2,000 depending on complexity. These reports provide detailed analysis of structural problems and specify remedial works.

Damp and Timber Surveys: Necessary when building surveys identify potential damp or timber decay. Costs: £200-£500. Specialists use moisture meters and invasive testing to determine extent and causes, then specify treatments.

Drainage Surveys (CCTV): Recommended for older properties or when surveys note drainage concerns. Costs: £150-£400. Camera inspections identify blockages, damage, or root ingress in underground drains.

Electrical Condition Reports: Essential when surveys flag outdated or potentially dangerous electrical installations. Costs: £150-£300. Qualified electricians test circuits and identify safety issues.

Asbestos Surveys: Required for properties built before 2000 if surveys identify potential asbestos-containing materials. Costs: £200-£500. Identifies presence, condition, and removal requirements.

Understanding areas requiring further investigation helps first-time buyers budget for these additional costs and understand their importance.

The survey report will typically recommend sourcing extra advice from specialists when findings warrant deeper investigation.

Environmental and Sustainability Considerations

First-time buyers in 2026 increasingly prioritise energy efficiency and environmental performance. Building surveys now commonly include observations about:

Energy Performance:

- Insulation levels in walls, roofs, and floors

- Window glazing quality and condition

- Heating system efficiency and age

- Ventilation adequacy

- Renewable energy installations

Environmental Risks:

- Flood risk indicators (evidence of previous flooding, proximity to water courses)

- Ground contamination potential (former industrial uses)

- Japanese knotweed or other invasive species

- Radon gas risk in affected areas

Understanding environmental issues identified in surveys helps first-time buyers assess long-term ownership costs, particularly energy bills and insurance premiums.

Properties with poor energy performance may require £5,000-£20,000 in improvements to achieve acceptable efficiency levels. However, these improvements can reduce annual energy costs by £500-£1,500, providing payback over 5-15 years while improving comfort and reducing carbon footprint.

Understanding Defects and Their Implications

Building surveys categorise defects by severity, helping first-time buyers prioritise responses:

Category 1 (Serious defects requiring urgent attention):

- Structural instability or movement

- Dangerous electrical installations

- Serious water ingress

- Failed damp-proof courses causing extensive damage

- Unsafe chimneys or parapets

Category 2 (Defects requiring attention but not urgent):

- Roof coverings nearing end of life

- Aging heating systems

- Minor damp issues

- Deteriorating external joinery

- Cracked or damaged render

Category 3 (Minor defects or maintenance items):

- Cosmetic damage

- Minor wear and tear

- Routine maintenance requirements

- Improvements for convenience or efficiency

Understanding building defects identified in surveys helps first-time buyers assess risk levels and prioritise spending.

The Consequences of Skipping Surveys

Some first-time buyers, pressured by tight budgets and competitive markets, consider skipping professional surveys. Understanding the consequences of failing to act on survey recommendations—or failing to commission surveys at all—illustrates the risks:

Financial Consequences:

- Unexpected repair costs exceeding available funds

- Inability to remortgage due to undisclosed defects

- Reduced property values if problems worsen

- Difficulty selling without addressing major issues

Legal Consequences:

- Potential liability if defects affect neighbouring properties

- Building control issues if unpermitted works are discovered

- Insurance claim rejections for pre-existing conditions

Personal Consequences:

- Stress and anxiety from unexpected problems

- Relationship strain from financial pressures

- Health risks from damp, mould, or structural hazards

- Forced sales at losses if problems become unmanageable

In 2026's recovering market, the temptation to move quickly without thorough due diligence is strong. However, the potential consequences of undiscovered defects far outweigh survey costs.

Maintenance Planning for Long-Term Affordability

A often-overlooked benefit of comprehensive building surveys is the maintenance planning guidance they provide. First-time buyers benefit from understanding:

Routine Maintenance Requirements:

- Annual gutter cleaning and inspection

- Boiler servicing

- External decoration cycles (typically 5-7 years)

- Garden and boundary maintenance

Cyclical Replacement Planning:

- Roof covering lifespan (40-60 years for tiles, 15-25 years for flat roofs)

- Window replacement (25-40 years depending on material)

- Heating system replacement (12-15 years)

- Kitchen and bathroom refurbishment (15-20 years)

Preventative Maintenance:

- Repointing brickwork before water penetration occurs

- Timber treatment before decay becomes extensive

- Damp-proofing before rising damp causes structural damage

- Drainage maintenance before blockages cause flooding

Understanding these cycles helps first-time buyers budget for ownership costs beyond mortgage payments. A property requiring £1,000 annually in routine maintenance and £3,000 annually in reserve for cyclical replacements represents significantly different affordability than one requiring minimal maintenance.

Practical Guidance for First-Time Buyers Commissioning Surveys in 2026

Selecting the Right Surveyor

Not all surveyors offer equal value. First-time buyers should consider:

Qualifications and Accreditation:

- RICS (Royal Institution of Chartered Surveyors) membership

- Specialist experience with property type (Victorian, Edwardian, modern)

- Professional indemnity insurance coverage

- Local knowledge and experience

Service Quality Indicators:

- Detailed, comprehensive reports with photographs

- Clear explanations accessible to non-specialists

- Availability for follow-up questions

- Reasonable turnaround times

- Transparent pricing without hidden fees

Red Flags:

- Unusually low prices suggesting rushed inspections

- Reluctance to provide sample reports

- Lack of professional accreditation

- Poor communication or unavailability

First-time buyers should request sample reports before commissioning surveys to assess quality and comprehensiveness.

Preparing for the Survey

Maximising survey value requires preparation:

Before the Survey:

- Ensure vendor provides full access to all areas

- Request access to loft spaces, basements, and outbuildings

- Inform surveyor of specific concerns or observations

- Provide property history if available (previous surveys, planning permissions)

During the Survey:

- Attend if possible to ask questions and gain insights

- Take photographs of areas of concern

- Request explanations of findings in accessible language

- Discuss preliminary observations

After the Survey:

- Review report thoroughly before discussing with vendor

- Seek clarification on unclear points

- Commission specialist reports if recommended

- Develop action plan based on findings

Interpreting Survey Reports Effectively

Survey reports can be lengthy and technical. First-time buyers should focus on:

Executive Summary: Provides overview of key findings and priority issues

Condition Ratings: Traffic light systems (red/amber/green) or numerical ratings indicating severity

Cost Estimates: Approximate repair costs for identified issues

Recommendations: Suggested actions, timescales, and specialist investigations

Photographic Evidence: Visual documentation of defects and concerns

First-time buyers should not hesitate to contact surveyors for clarification. Understanding findings thoroughly enables effective negotiation and planning.

Integrating Surveys into the Purchase Process

Building surveys should integrate seamlessly into the purchase timeline:

Optimal Timing:

- Offer accepted (subject to survey and contract)

- Survey commissioned immediately (within 1-2 days)

- Survey conducted (within 5-10 days)

- Report received and reviewed (within 7-14 days of offer)

- Negotiations based on findings (within 3-5 days of report)

- Specialist surveys if needed (within 10-14 days)

- Final decision and contract exchange

This timeline ensures surveys inform decisions without causing unnecessary delays that might jeopardise purchases in competitive markets.

Cost-Saving Strategies Without Compromising Quality

First-time buyers can manage survey costs while maintaining quality:

💡 Bundle services: Some surveyors offer package deals combining surveys with valuations or energy performance certificates

💡 Compare quotes: Obtain 2-3 quotes from qualified surveyors, but don't choose solely on price

💡 Time strategically: Book surveys during quieter periods when surveyors may offer better rates

💡 Negotiate with vendors: In some cases, vendors may contribute to survey costs, particularly if property has known issues

💡 Consider survey level carefully: Don't over-specify (Level 3 for a new build) or under-specify (Level 1 for a Victorian terrace)

However, false economy on surveys can prove extremely expensive. A £200 saving on survey costs is meaningless if it results in missing a £10,000 defect.

Future-Proofing Your Purchase: Long-Term Value Protection

Understanding Market Trends and Property Values

First-time buyers in 2026 should consider how survey findings affect long-term value:

Value-Enhancing Features:

- Sound structure with no significant defects

- Modern, efficient systems (heating, electrical, plumbing)

- Good energy performance (EPC rating C or above)

- Quality materials and construction

- Evidence of regular maintenance

Value-Diminishing Factors:

- Structural problems or movement

- Outdated or failing systems

- Poor energy efficiency

- Evidence of water ingress or damp

- Deferred maintenance creating backlog

Properties requiring significant investment to address survey findings may appreciate more slowly than well-maintained alternatives, affecting long-term wealth building for first-time buyers.

Building Equity Through Informed Improvements

Survey findings help first-time buyers prioritise improvements that build equity:

High-ROI Improvements:

- Addressing structural issues (prevents value depreciation)

- Upgrading heating systems (improves efficiency and appeal)

- Resolving damp problems (prevents ongoing damage)

- Modernising electrical systems (improves safety and functionality)

Lower-ROI Improvements:

- Cosmetic upgrades (personal preference, variable value return)

- Over-specification (luxury features in standard property areas)

- Niche modifications (may not appeal to future buyers)

Understanding which survey-identified issues to address immediately versus deferring helps first-time buyers maximise limited budgets while protecting and building equity.

Insurance and Survey Findings

Building surveys can affect insurance:

Disclosure Requirements: Buyers must disclose known defects when obtaining insurance. Survey findings constitute known defects.

Premium Implications: Properties with subsidence history, flood risk, or structural issues typically face higher premiums or coverage exclusions.

Claims Considerations: Insurers may reject claims for pre-existing conditions identified in surveys but not addressed.

First-time buyers should obtain insurance quotes based on survey findings before completing purchases to ensure affordability and adequate coverage.

Creating a Five-Year Property Plan

Comprehensive surveys enable strategic planning:

Year 1: Address urgent defects, establish maintenance routines, build emergency fund

Years 2-3: Complete medium-priority repairs, begin energy efficiency improvements, build renovation fund

Years 4-5: Address long-term concerns identified in survey, plan major improvements, reassess property condition

This structured approach transforms survey findings from overwhelming lists into manageable, phased action plans that protect affordability while maintaining property condition.

Conclusion

Building Surveys for First-Time Buyers in a Recovering Market: Addressing Affordability Pressures and Hidden Costs in 2026 represents not just a prudent precaution but an essential investment in financial security and peace of mind. As the UK housing market continues its recovery, with buyer enquiries up 15% and prices rising 2.8% in January 2026 alone, first-time buyers face both unprecedented opportunity and significant risk.[1][2]

The statistics paint a clear picture: with mortgage rates stabilising around 4.91%, best-buy deals available at 3.50%, and the house price-to-income ratio at decade lows, conditions for first-time buyers have improved markedly.[2] However, rising asking prices and continued affordability pressures mean every pound must work harder. A comprehensive building survey costing £800-£1,500 can identify hidden defects worth £15,000-£50,000 or more, providing negotiating leverage that transforms purchase economics.

Key Actions for First-Time Buyers

✅ Commission appropriate surveys: Match survey level to property age, type, and condition—don't economise on older or non-standard properties

✅ Budget realistically: Include survey costs (0.15-0.4% of purchase price) and potential repair costs (2-5% of purchase price) in affordability calculations

✅ Negotiate strategically: Use survey findings to negotiate price reductions, repairs, or retention amounts—objective evidence drives successful negotiations

✅ Plan long-term: Use survey findings to create five-year maintenance and improvement plans that protect affordability and build equity

✅ Engage professionals: Work with RICS-qualified surveyors who provide comprehensive reports and accessible explanations

Next Steps

For first-time buyers preparing to enter the 2026 market:

- Research property types and understand which survey level each requires

- Budget comprehensively including survey costs, specialist investigations, and immediate repairs

- Select qualified surveyors with relevant experience and professional accreditation

- Review sample reports to understand what comprehensive surveys should include

- Integrate surveys into purchase timelines to inform decisions without causing delays

- Prepare for negotiations by understanding how to leverage survey findings effectively

The recovering market of 2026 offers genuine opportunities for first-time buyers willing to conduct thorough due diligence. Rising prices make comprehensive surveys more valuable than ever—identifying problems early prevents catastrophic financial consequences and enables informed decision-making that protects both immediate affordability and long-term wealth building.

In a market where first-time buyers spend 20-25% of household income on mortgage payments and have limited reserves for unexpected repairs, professional building surveys represent not a luxury but a necessity.[3] The difference between a dream home and a financial nightmare often lies in the quality of pre-purchase investigation.

By approaching property purchases with professional guidance, realistic budgeting, and comprehensive surveys, first-time buyers can navigate the 2026 market confidently, securing properties that offer genuine value while avoiding hidden costs that could derail homeownership dreams. The investment in knowledge and professional expertise pays dividends for decades, providing the foundation for successful, sustainable homeownership in a recovering but still challenging market.

References

[1] Uk Housing Market Showing Strength In Early 2026 – https://www.quickmortgages.com/uk-housing-market-showing-strength-in-early-2026/

[2] Whats Outlook Uk House Prices 2026 – https://global.morningstar.com/en-gb/personal-finance/whats-outlook-uk-house-prices-2026

[3] House Prices In 2026 What The Data Actually Shows – https://www.propertysolvers.co.uk/youtube/house-prices-in-2026-what-the-data-actually-shows/