The UK property market has entered an unprecedented era of regional divergence in 2026, with Northern Ireland and Scotland dramatically outpacing traditional southern strongholds. Recent RICS data reveals a stark transformation: Northern Ireland leads the nation with 7.1% annual growth, while London languishes at -1.2%, marking the widest north-south divide in modern property history.[2] This seismic shift in Regional Divergence in UK Property Valuations: Why Northern Ireland and Scotland Are Outpacing the South in 2026 demands urgent attention from surveyors, valuers, and property professionals navigating increasingly complex regional dynamics.

For chartered surveyors and property advisors, understanding these regional variations has become essential for accurate valuations, strategic investment guidance, and client advisory services. The traditional assumption that London and the South East would perpetually lead UK property growth has been thoroughly dismantled.

Key Takeaways

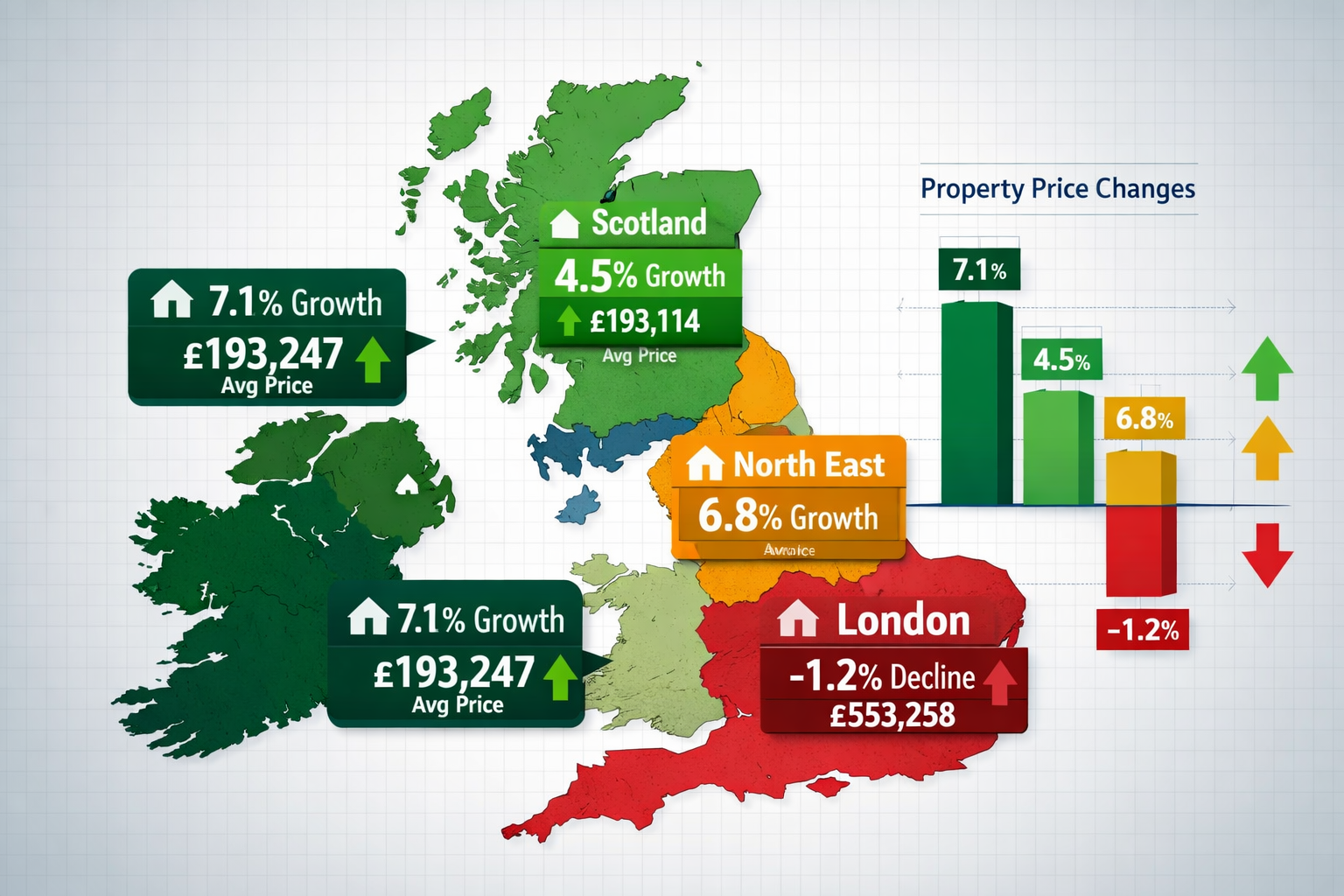

- 🏴 Northern Ireland leads all UK regions with 7.1% annual property price growth year-to-date through 2025, while London records negative growth at -1.2%[2]

- 🏴 Scotland maintains strong momentum at 4.5% annual growth, positioning it as the second-strongest performer with an average property price of £193,114[2]

- 📊 Northern English regions dominate growth rankings, with the North East achieving 6.8% growth and forecasts suggesting 28.8% price increases by 2030[1][2]

- 💷 Affordability constraints drive the divide, as easing mortgage rates and steady wage growth disproportionately benefit lower-priced northern markets while southern regions face persistent affordability pressures[2]

- 🔮 Long-term forecasts amplify disparities, with affordable northern regions projected to see substantially higher growth than London and the South East through 2030[1]

Understanding the Current Regional Divergence in UK Property Valuations

The 2026 Regional Performance Landscape

The Regional Divergence in UK Property Valuations: Why Northern Ireland and Scotland Are Outpacing the South in 2026 represents more than a temporary market fluctuation—it signals a fundamental restructuring of UK property dynamics. The latest data paints a clear picture of this transformation across the four nations and English regions.

Northern Ireland has emerged as the undisputed leader, with property values climbing 7.1% year-to-date through 2025.[2] The average property price stands at £193,247, representing exceptional value compared to southern counterparts. This growth trajectory has caught many industry observers by surprise, as Northern Ireland historically lagged behind other UK nations.

Scotland follows closely with 4.5% annual growth and an average property price of £193,114.[2] Scottish property markets have benefited from strong economic fundamentals, steady employment growth, and increasing appeal to buyers priced out of southern markets. Edinburgh and Glasgow continue to attract both domestic and international investment.

England presents a fragmented picture, with overall growth of just 2.2% year-to-date through 2025 masking substantial internal variations.[2] The average English property price of £293,131 reflects the significant weight of expensive southern markets, but regional performance varies dramatically:

| Region | Annual Growth | Average Price | 2030 Forecast Growth |

|---|---|---|---|

| Northern Ireland | 7.1% | £193,247 | Strong projected gains |

| Scotland | 4.5% | £193,114 | Sustained momentum |

| North East England | 6.8% | £166,568 | +28.8% by 2030[1] |

| North West England | 4.1% | £216,741 | Above-average growth |

| Yorkshire & Humber | 3.7% | £209,236 | +28.8% by 2030[1] |

| London | -1.2% | £553,258 | +13.6% by 2030[1] |

| South East | 1.0% | £381,369 | Below-average growth |

| Wales | 0.7% | £208,935 | Modest expectations |

Wales records the weakest performance among the four nations at just 0.7% annual inflation, despite an average property price of £208,935.[2] Welsh markets face unique challenges including limited employment growth in some areas and competition from more dynamic neighboring regions.

For surveyors conducting professional property valuations, these regional variations demand careful consideration of local market conditions rather than relying on national trends.

The London Paradox: Negative Growth in the Capital

Perhaps the most striking element of the Regional Divergence in UK Property Valuations: Why Northern Ireland and Scotland Are Outpacing the South in 2026 is London's unprecedented decline. The capital recorded -1.2% annual inflation year-to-date through 2025, despite maintaining the UK's highest average property price at £553,258.[2]

This represents a dramatic reversal for a market that historically set the pace for UK property growth. Several factors contribute to London's underperformance:

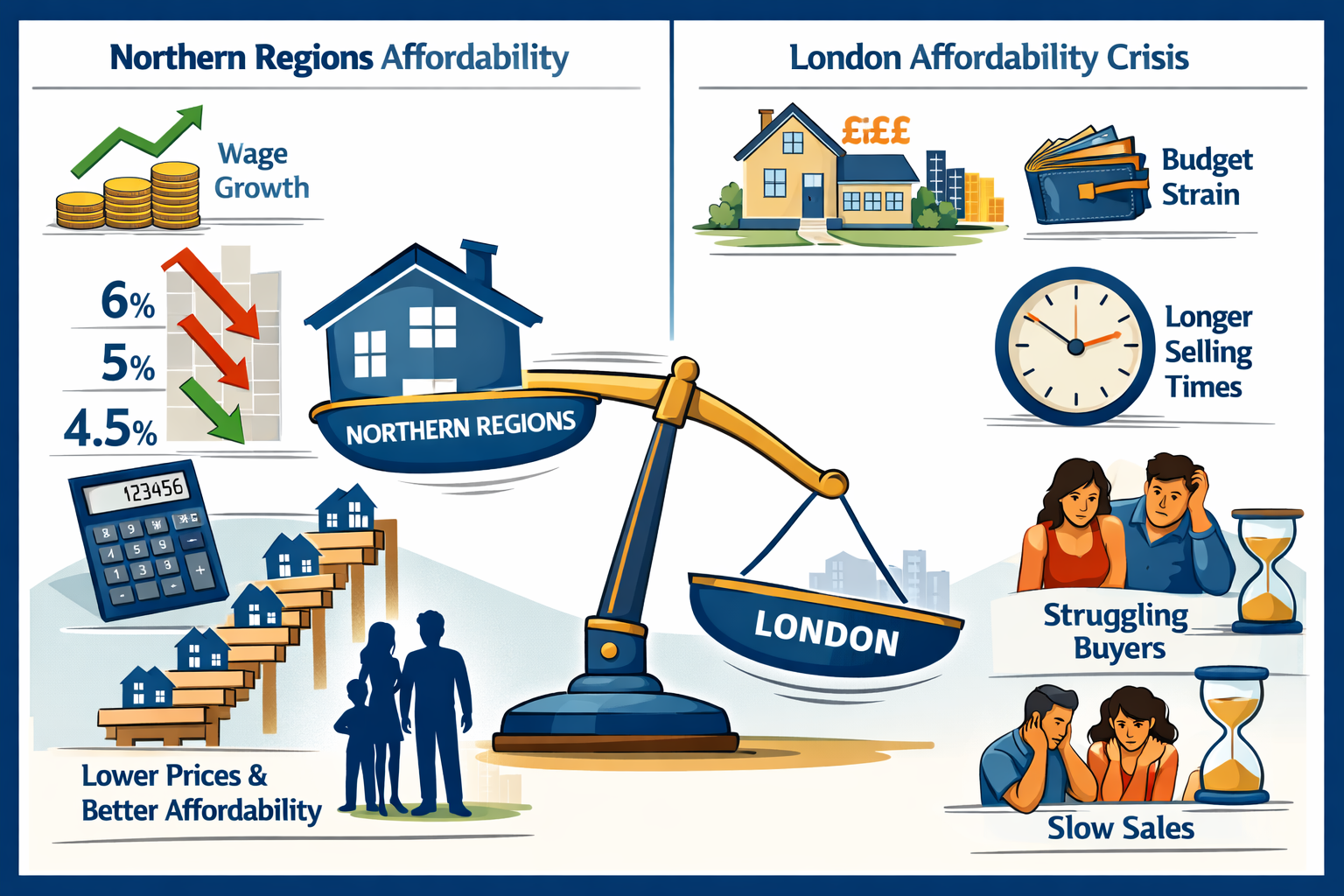

Extended selling times have become the norm in the capital, with properties taking significantly longer to sell compared to the rest of the country.[3] This reflects reduced buyer urgency and increased price sensitivity in a market where affordability has reached breaking point for many potential purchasers.

Affordability constraints have reached critical levels. With average prices exceeding £550,000, even dual-income professional households struggle to access the property ladder. The gap between London wages and property prices has widened to historically extreme levels, fundamentally limiting the buyer pool.

Post-pandemic migration patterns continue to impact London's market. Remote and hybrid working arrangements have enabled thousands of households to relocate to more affordable regions while maintaining London salaries, reducing demand in the capital while boosting markets in commuter regions and beyond.

Investment reallocation has seen both domestic and international investors shift focus toward higher-yielding regional markets. Commercial valuations increasingly favor northern cities offering better rental yields and growth potential.

The longer-term forecast for London remains subdued, with projected growth of just 13.6% by 2030—less than half the 28.8% forecast for affordable northern regions.[1] This projection represents a fundamental shift in the UK property market's center of gravity.

Key Drivers Behind Regional Divergence in UK Property Valuations

Affordability: The Primary Catalyst

Affordability dynamics stand as the single most important driver of Regional Divergence in UK Property Valuations: Why Northern Ireland and Scotland Are Outpacing the South in 2026. Paula Higgins, CEO of the HomeOwners Alliance, explains that "the north-south divide in house price growth in England [is expected to] persist with higher growth in the north of England than in the south," driven by easing mortgage rates and steady wage growth improving affordability in lower-priced regions.[2]

The mathematics of affordability create a powerful advantage for northern markets:

Lower entry prices in regions like the North East (£166,568 average), Northern Ireland (£193,247), and Scotland (£193,114) mean that mortgage rate reductions have a disproportionately positive impact.[2] A 1% reduction in mortgage rates saves a buyer in the North East approximately £1,665 annually on a typical property, compared to £5,532 in London—but the North East buyer's income-to-mortgage ratio improves far more substantially.

Wage growth convergence has narrowed regional income disparities over recent years. While London wages remain higher in absolute terms, northern regions have experienced stronger percentage wage growth, particularly in technology, professional services, and advanced manufacturing sectors. This convergence means that property prices in northern regions increasingly align with local earning capacity.

First-time buyer accessibility has become concentrated in northern markets. The deposit required for a typical property in the North East (approximately £16,657 at 10%) compares favorably to London (£55,326), making homeownership achievable for younger buyers and families who would face years of additional saving in southern markets.

Mortgage approval rates reflect these affordability dynamics. Lenders approve a higher percentage of applications for northern properties because loan-to-income ratios remain within acceptable parameters, whereas southern applicants increasingly fail affordability tests despite stable employment and good credit histories.

For property professionals offering capital gains tax valuations, understanding these affordability dynamics helps predict future growth trajectories and advise clients on optimal timing for acquisitions and disposals.

Mortgage Rate Sensitivity and Regional Impact

The mortgage rate environment of 2026 has created divergent impacts across UK regions. While rates have eased from their 2023 peaks, they remain elevated compared to the ultra-low rate environment of the 2010s. This normalization affects regions differently based on their price points.

Rate reduction benefits accrue disproportionately to affordable markets. As rates have declined from approximately 6% to around 4.5% for typical fixed-rate mortgages, the monthly payment reduction on a £193,000 property (Northern Ireland average) provides meaningful relief that can unlock demand from buyers previously priced out of the market.

Southern market constraints persist despite rate improvements. Even with reduced rates, the absolute mortgage payments on properties averaging £553,258 (London) or £381,369 (South East) remain prohibitively expensive for most households.[2] The monthly payment on a London property at 4.5% interest still exceeds £2,800, far beyond the reach of median-income households.

Buyer psychology responds more positively in affordable markets. In northern regions, mortgage rate reductions translate to tangible improvements in monthly budgets, encouraging buyers to enter the market. In southern markets, rate reductions merely make unaffordable properties slightly less unaffordable, failing to trigger the same psychological shift toward purchasing.

Economic Fundamentals and Regional Employment

Regional economic performance increasingly favors northern areas, contradicting historical patterns where London and the South East dominated economic growth. Several sectors drive this transformation:

Technology and innovation hubs have emerged in Manchester, Edinburgh, Glasgow, Belfast, and Leeds. These cities now host substantial technology clusters, attracting both established companies and startups seeking lower operating costs and access to skilled graduates from regional universities. This employment growth directly supports property demand.

Advanced manufacturing remains concentrated in northern regions, particularly in automotive, aerospace, and renewable energy sectors. Government investment in regional manufacturing capabilities has created high-quality employment opportunities that support mortgage applications and property purchases.

Public sector distribution provides stable employment bases in regional cities. Major government departments, healthcare facilities, and educational institutions create consistent demand for housing from professional workers with secure incomes—exactly the demographic that supports stable property markets.

Remote work transformation has enabled northern regions to capture economic value from London-based employers. Workers earning London salaries while residing in Belfast, Edinburgh, or Manchester possess exceptional purchasing power in local property markets, driving demand and supporting price growth.

For surveyors conducting building surveys in these growing northern markets, understanding local economic drivers helps assess long-term property viability and investment potential.

Supply Constraints and Development Patterns

Housing supply dynamics vary substantially across regions, contributing to divergent price trajectories. Northern Ireland and Scotland have managed to balance supply and demand more effectively than southern regions.

Planning system efficiency in Scotland and Northern Ireland has enabled more responsive housing delivery. While still subject to constraints, these nations have generally achieved better alignment between housing completions and population growth compared to southern England.

Development viability improves in northern markets as construction costs remain relatively consistent nationwide while sale prices vary dramatically. Developers can achieve acceptable margins on properties selling for £200,000-£250,000 in northern regions, whereas southern markets increasingly require premium pricing to justify development costs, limiting supply expansion.

Land availability remains more abundant in northern regions and Scotland, enabling development at scale without the intense land value competition that characterizes southern markets. This fundamental supply advantage helps moderate price growth while still delivering positive returns.

Brownfield regeneration has transformed former industrial sites in northern cities into attractive residential developments. Cities like Manchester, Glasgow, and Belfast have successfully converted industrial heritage into residential opportunities, expanding supply in desirable urban locations.

Strategic Implications for Surveyors and Property Professionals

Adapting Valuation Methodologies for Regional Markets

The Regional Divergence in UK Property Valuations: Why Northern Ireland and Scotland Are Outpacing the South in 2026 demands sophisticated valuation approaches that account for regional dynamics rather than relying on national assumptions.

Comparable selection requires heightened regional specificity. Surveyors must ensure comparables reflect local market conditions, recent transaction patterns, and regional growth trajectories. A comparable from six months ago may no longer reflect current values in rapidly appreciating northern markets, while southern market comparables may overstate current values if they predate recent declines.

Growth rate assumptions must be regionally calibrated. Applying national growth forecasts of 2% to a Northern Ireland property valuation would significantly understate likely appreciation, while applying it to a London property might overstate prospects.[2] Professional valuers should reference region-specific forecasts and adjust assumptions accordingly.

Market time considerations vary dramatically by region. Properties in London taking longer to sell require different marketing and pricing strategies compared to northern markets where well-priced properties may attract multiple offers within days.[3] This affects both valuation advice and client guidance on realistic timelines.

Risk assessment must account for regional economic resilience. Northern markets demonstrating employment growth, wage increases, and infrastructure investment present different risk profiles compared to southern markets heavily dependent on financial services and vulnerable to economic shocks.

Surveyors offering leasehold extension and enfranchisement valuations should particularly note regional variations in marriage value calculations and future growth assumptions.

Client Advisory Strategies in Divergent Markets

Investment guidance requires region-specific strategies aligned with client objectives and risk tolerance:

Growth-focused investors should receive analysis highlighting northern regions' superior growth trajectories. With the North East forecast to achieve 28.8% growth by 2030 compared to London's 13.6%, capital appreciation potential clearly favors northern markets.[1] However, investors must also consider liquidity, tenant demand, and management complexity when investing outside their local area.

Yield-focused investors benefit from northern markets' superior rental yields. Properties in northern regions typically generate 5-7% gross yields compared to 3-4% in London and the South East, providing better cash flow and investment returns even before accounting for capital appreciation.

Portfolio diversification becomes essential in an era of regional divergence. Clients with concentrated southern holdings should consider rebalancing toward northern exposure to capture growth opportunities and reduce concentration risk. This requires careful analysis of disposal timing, tax implications, and reinvestment strategies.

First-time buyer clients in southern markets face difficult choices. Surveyors can provide valuable guidance on the trade-offs between remaining in expensive southern markets versus relocating to affordable northern regions where homeownership becomes achievable. This involves analyzing commuting viability, employment transferability, and lifestyle considerations alongside pure financial metrics.

Navigating Regional Legislation and Valuation Standards

Regulatory variations across UK nations require careful attention from surveyors operating in multiple jurisdictions:

Scottish property law differs substantially from English law, particularly regarding property transactions, leasehold arrangements (which are rare in Scotland), and tenancy regulations. Valuers must understand these distinctions when advising clients on Scottish property acquisitions or conducting cross-border comparisons.

Northern Ireland rating system operates differently from the rest of the UK, with regional rate setting and different revaluation cycles.[5] This affects property running costs and investment returns, requiring specific expertise when valuing Northern Ireland properties.

Welsh property regulations include unique requirements around language, energy efficiency standards, and licensing for rental properties. These regulatory costs impact investment viability and must be factored into valuations and client advice.

Building standards vary across nations, with Scotland maintaining distinct building regulations and energy efficiency requirements. Surveyors conducting insurance reinstatement cost valuations must apply nation-specific construction cost assumptions.

Understanding recent property market legislation changes helps surveyors provide comprehensive advice that accounts for regulatory impacts on property values.

Technology and Data Analytics for Regional Market Intelligence

Data-driven insights have become essential for navigating regional divergence effectively:

Regional market dashboards enable surveyors to track real-time performance metrics across different UK regions. Monitoring transaction volumes, average prices, time on market, and asking price reductions provides early warning of shifting dynamics and emerging opportunities.

Predictive analytics help forecast regional trajectories based on economic fundamentals, demographic trends, and infrastructure investment. Machine learning models can identify regions likely to outperform or underperform based on historical patterns and current indicators.

Comparable databases with robust regional filtering enable more accurate valuations. Access to comprehensive transaction data across all UK regions ensures valuers can identify truly comparable properties rather than relying on limited local knowledge.

Client reporting tools that visualize regional performance comparisons help communicate complex market dynamics effectively. Charts showing regional growth rates, affordability metrics, and forecast trajectories enable clients to understand recommendations and make informed decisions.

Future Outlook: Regional Divergence Through 2030

Long-Term Growth Projections and Regional Winners

The five-year outlook through 2030 suggests the Regional Divergence in UK Property Valuations: Why Northern Ireland and Scotland Are Outpacing the South in 2026 will intensify rather than moderate.

Northern regions maintain momentum with forecasts suggesting affordable areas like Yorkshire and Humber and the North East could see prices rise by approximately 28.8% by 2030.[1] This exceptional growth reflects sustained affordability advantages, economic development, and infrastructure investment that will continue attracting buyers and investors.

Scotland's steady trajectory positions it for continued outperformance relative to southern England. Edinburgh and Glasgow benefit from strong universities, technology sector growth, and quality of life advantages that attract both domestic and international residents. Political stability and pro-growth policies support property market confidence.

Northern Ireland's exceptional growth appears sustainable given the region's starting point of exceptional affordability and ongoing economic development. Belfast's transformation into a technology and professional services hub creates employment that supports property demand, while the region's average price of £193,247 remains accessible to median-income households.[2]

London's modest recovery is forecast at approximately 13.6% growth through 2030—less than half the rate expected in affordable northern regions.[1] This subdued outlook reflects persistent affordability constraints, limited scope for buyer pool expansion, and continued competition from regional alternatives offering better value.

Southern regions face headwinds with the South East and other expensive areas forecast for below-average growth. Until affordability improves substantially through either price corrections or exceptional wage growth, these markets will struggle to generate the transaction volumes and buyer competition necessary for strong appreciation.

For property professionals advising on investment strategies, these long-term forecasts provide essential context for portfolio positioning and acquisition timing.

Infrastructure Investment and Regional Transformation

Government infrastructure spending will significantly influence regional property markets through 2030:

Northern Powerhouse initiatives continue directing investment toward northern English cities, improving transport connectivity, digital infrastructure, and economic development. These investments enhance regional attractiveness and support property values by improving employment accessibility and quality of life.

Scottish infrastructure programs including renewable energy development, transport improvements, and digital connectivity expansion will support continued economic growth and property market strength. Scotland's leadership in renewable energy creates high-quality employment opportunities in engineering, technology, and professional services.

HS2 and regional connectivity improvements (despite project modifications) will continue enhancing northern cities' accessibility to London and each other. Improved connectivity supports both commuter demand and business investment, creating positive feedback loops for property markets.

Leveling Up funding directed toward regional regeneration, skills development, and economic diversification helps address historical disadvantages and creates conditions for sustained property market growth. Cities successfully leveraging this funding will likely see accelerated property appreciation.

Potential Risks and Market Corrections

While northern regions appear well-positioned for continued outperformance, several risk factors warrant monitoring:

Economic shocks could disproportionately impact regional markets if they trigger unemployment in key sectors. Northern economies, while diversifying, retain concentrations in manufacturing and public sector employment that could face pressure during severe recessions.

Mortgage rate volatility remains a risk, particularly for affordable markets where buyer demand depends heavily on financing accessibility. A return to significantly higher rates could suppress demand and moderate growth expectations.

Oversupply risks may emerge in some northern markets if developers over-respond to current strong demand. Excessive development could create local supply-demand imbalances that moderate price growth or even trigger corrections.

London recovery potential should not be dismissed entirely. If affordability improves through wage growth, policy interventions, or price corrections, London could experience renewed demand that outpaces current forecasts. The capital retains fundamental advantages in employment, culture, and international connectivity that could reassert themselves.

Political and policy uncertainty including potential changes to property taxation, rental regulations, or planning systems could impact regional markets differently. Surveyors must monitor policy developments and assess their likely regional impacts.

Conclusion: Navigating the New Regional Reality

The Regional Divergence in UK Property Valuations: Why Northern Ireland and Scotland Are Outpacing the South in 2026 represents a fundamental restructuring of UK property market dynamics that will define the industry for years to come. With Northern Ireland achieving 7.1% growth, Scotland at 4.5%, and northern English regions substantially outpacing London's -1.2% decline, the traditional assumptions underlying property investment and valuation have been thoroughly disrupted.[2]

Affordability has emerged as the dominant force shaping regional performance, with lower-priced northern markets benefiting disproportionately from easing mortgage rates and steady wage growth while expensive southern markets remain constrained by fundamental affordability limits.[2] This dynamic appears structural rather than cyclical, suggesting sustained regional divergence through 2030 and beyond.

For chartered surveyors and property professionals, this new reality demands sophisticated regional expertise, data-driven valuation methodologies, and client advisory strategies tailored to specific regional dynamics. The days of applying national assumptions to local valuations have definitively ended.

Actionable Next Steps for Property Professionals

Enhance regional market intelligence by developing systematic processes for monitoring performance metrics across all UK regions. Subscribe to regional market reports, analyze transaction data, and build networks of professional contacts in key growth markets to maintain current knowledge.

Refine valuation methodologies to incorporate region-specific growth assumptions, comparable selection criteria, and risk assessments. Ensure valuation reports explicitly address regional market dynamics and justify assumptions with reference to local data rather than national trends.

Expand service offerings to address client needs in an era of regional divergence. Consider developing expertise in cross-border transactions, regional investment analysis, and portfolio rebalancing strategies that help clients capitalize on regional opportunities.

Invest in professional development focused on regional markets, particularly Scotland and Northern Ireland where legal and regulatory frameworks differ from England. Understanding these distinctions enhances service quality and reduces professional liability risks.

Leverage technology and data to maintain competitive advantage. Implement market intelligence platforms, comparable databases, and analytical tools that enable rapid, accurate regional market assessment and client reporting.

Build strategic partnerships with professionals in high-growth regions. Developing referral relationships with surveyors, solicitors, and mortgage brokers in northern markets enables comprehensive client service for cross-regional transactions.

The Regional Divergence in UK Property Valuations: Why Northern Ireland and Scotland Are Outpacing the South in 2026 presents both challenges and opportunities for property professionals. Those who adapt quickly, develop regional expertise, and provide sophisticated advisory services will thrive in this transformed market landscape.

For comprehensive property valuation services across all UK regions, explore our professional valuation offerings and discover how expert regional market knowledge delivers superior outcomes for clients navigating today's complex property market.

References

[1] House Prices What To Expect In 2026 And Beyond – https://meliorwealth.com/2026/01/14/house-prices-what-to-expect-in-2026-and-beyond/

[2] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/

[3] Uk House Prices In 2026 Where The Market Is Headed What It Means For Buyers Sellers And Landlor – https://www.approvedbusinessfinance.co.uk/post/uk-house-prices-in-2026-where-the-market-is-headed-what-it-means-for-buyers-sellers-and-landlor

[5] Executive Agrees Regional Rate 202627 – https://www.finance-ni.gov.uk/news/executive-agrees-regional-rate-202627